Global Digital Genome Market

Market Size in USD Billion

USD

2.26 Billion

USD

4.11 Billion

2024

2032

USD

2.26 Billion

USD

4.11 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.26 Billion | |

| USD 4.11 Billion | |

| % | |

|

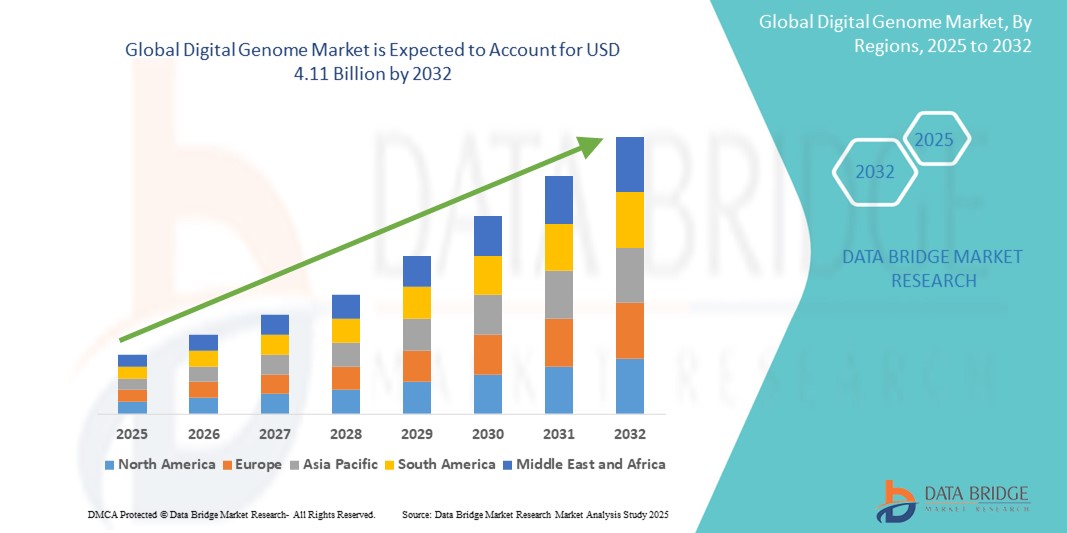

Digital Genome Market Size

- The global Digital Genome market was valued at USD in 2.26 billion 2024 and is expected to reach USD 4.11 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 8.80%, primarily driven by the advancements in genomic technologies and increasing demand for personalized medicine

- This growth is driven by factors such as the rising prevalence of genetic disorders, increased funding for genomics research, and the expanding application of digital genome solutions in diagnostics and drug development

Digital Genome Market Analysis

- The digital genome market encompasses advanced technologies used to digitize, store, and analyze genetic information, enabling high-precision diagnostics, personalized medicine, and targeted therapeutics. It plays a vital role in genomics, bioinformatics, and molecular diagnostics

- The demand for digital genome solutions is significantly driven by the rising prevalence of chronic and genetic diseases, increasing investments in genomic research, and growing public awareness of personalized healthcare. A substantial portion of the global demand is fueled by the application of genomics in cancer research and rare disease diagnostics

- North America emerges as a leading region in the digital genome market, supported by robust research infrastructure, widespread adoption of next-generation sequencing technologies, and strong government and private sector funding

- For instance, the major U.S. initiatives such as the Precision Medicine Initiative and large-scale genomics projects continue to accelerate the adoption and innovation of digital genome technologies across clinical and research setting

- Globally, digital genome platforms are considered one of the most transformative tools in modern healthcare, second only to next-generation sequencing systems, due to their ability to integrate and analyze complex genomic data for improved patient outcomes

Report Scope and Digital Genome Market Segmentation

|

Attributes |

Digital Genome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Digital Genome Market Trends

“Integration of AI and Big Data Analytics in Genomic Research”

- One prominent trend in the global digital genome market is the increasing integration of artificial intelligence (AI) and big data analytics to enhance genomic data interpretation and accelerate research outcomes

- These technologies enable rapid analysis of vast genomic datasets, uncovering patterns and associations critical for disease prediction, drug discovery, and personalized treatment planning

- For instance, AI-driven platforms can identify gene mutations and biomarkers linked to specific diseases, allowing researchers and clinicians to develop more precise and targeted therapies, especially in oncology and rare genetic disorders

- Big data integration also supports the creation of extensive genomic databases, fostering global collaboration and enabling more accurate population-wide genomic studies

- This trend is transforming the digital genome landscape, improving diagnostic accuracy, research efficiency, and ultimately, expanding the market for innovative genomic solutions.

Digital Genome Market Dynamics

Driver

“Rising Demand Due to Increasing Burden of Genetic and Chronic Diseases”

- The growing prevalence of genetic disorders, cancer, and other chronic diseases is a major driver fueling demand for digital genome technologies, as these tools play a critical role in identifying genetic mutations and guiding targeted therapies

- With the global population experiencing higher rates of non-communicable diseases and rare genetic conditions, there is an increasing reliance on genomic data to support early diagnosis, risk assessment, and treatment planning

- In oncology, for instance, genomic profiling enables clinicians to detect tumor-specific mutations, leading to more effective, personalized treatment strategies that improve survival rates and reduce adverse effects

- The advancements in genomic sequencing and data analysis have significantly lowered costs and improved accessibility, further driving adoption across both clinical and research settings

- This demand is compounded by the global shift toward precision medicine, where understanding a patient’s genetic makeup is key to delivering individualized healthcare

For instance,

- In January 2023, a report by the Global Alliance for Genomics and Health emphasized the increasing adoption of digital genome solutions in healthcare systems worldwide, particularly for cancer and rare disease diagnostics, due to their ability to provide actionable insights from genomic data

- According to the World Health Organization (WHO), over 400 million people globally are affected by rare diseases—80% of which have a genetic origin—highlighting the urgent need for advanced digital genome tools to support accurate diagnosis and research

- As a result, the growing burden of genetic and chronic diseases is significantly accelerating the adoption of digital genome technologies, driving growth in the global market

Opportunity

“Revolutionizing Genomic Medicine Through Artificial Intelligence Integration”

- The integration of artificial intelligence (AI) into digital genome platforms presents a significant opportunity to accelerate data analysis, enhance diagnostic precision, and drive innovation in personalized medicine

- AI algorithms can rapidly process and interpret complex genomic data, identifying patterns, mutations, and biomarkers that might be missed through conventional methods, thereby improving disease detection and therapeutic targeting

- In addition, AI enables predictive modeling of disease progression, drug response, and risk assessment, allowing healthcare providers to make more informed, data-driven decisions

For instance,

- In February 2024, a study published by Nature Biotechnology highlighted how deep learning models trained on large genomic datasets can accurately predict patient susceptibility to conditions such as cancer, cardiovascular diseases, and neurodegenerative disorders—paving the way for earlier intervention and tailored treatments

- In October 2023, the Broad Institute and Google Health partnered to enhance AI-driven genomic sequencing platforms capable of improving variant detection and reducing sequencing errors, significantly boosting the reliability of clinical genomic applications

- The AI integration is not only transforming genomic research and diagnostics but also reducing analysis time and healthcare costs, creating vast opportunities for the expansion and scalability of digital genome technologies across global healthcare systems

Restraint/Challenge

“High Implementation Costs and Data Management Complexities”

- The high cost associated with implementing digital genome technologies—including next-generation sequencing platforms, bioinformatics software, and data storage infrastructure—remains a significant barrier, especially for low- and middle-income countries

- Setting up a digital genome ecosystem requires substantial investment in equipment, skilled personnel, and IT infrastructure, which can hinder widespread adoption in smaller hospitals, clinics, and research institutions

- In addition, the management and interpretation of vast volumes of genomic data present ongoing challenges, including the need for secure storage, data standardization, and compliance with privacy regulations

For instance,

- In September 2024, a report by the Global Genomics Organization noted that genomic sequencing and analysis systems can cost upwards of USD 500,000, excluding ongoing operational and maintenance expenses, making them financially inaccessible for many smaller healthcare providers

- In June 2023, the European Society of Human Genetics highlighted the growing concern over genomic data privacy and the complexities involved in managing and analyzing terabytes of sensitive genetic data across diverse systems, which can delay research and clinical decision-making

- Consequently, high implementation costs and data handling complexities continue to act as restraints for the digital genome market, potentially slowing its penetration and adoption across under-resourced regions and institutions

Digital Genome Market Scope

The market is segmented on the basis of product, application, and end user.

|

Segmentation |

Sub-Segmentation |

|

By Product |

|

|

By Application |

|

|

By End User |

|

Digital Genome Market Regional Analysis

“North America is the Dominant Region in the Digital Genome Market”

- North America leads the global digital genome market, supported by a robust biotechnology sector, advanced research infrastructure, and widespread adoption of genomic technologies across healthcare and research institutions

- U.S. holds the largest share due to substantial government funding initiatives such as the Precision Medicine Initiative, along with strong participation from academic, clinical, and commercial stakeholders driving innovation in genomics

- The high demand for personalized medicine, a well-established reimbursement framework for genetic testing, and the presence of major players such as Illumina, Thermo Fisher Scientific, and Danaher Corporation further accelerate market growth in the region

- In addition, the increasing integration of AI and cloud-based bioinformatics tools in genomics, along with growing consumer interest in direct-to-consumer genetic testing, are also fueling expansion in the North American market

“Asia-Pacific is Projected to Register the Highest Growth Rate”

- Asia-Pacific is expected to witness the fastest growth in the digital genome market, driven by expanding healthcare infrastructure, growing investment in genomics research, and rising awareness of precision medicine

- Countries such as China, India, and Japan are emerging as major contributors due to their large patient populations, increasing burden of genetic disorders, and government-led initiatives to support genomic data collection and personalized healthcare

- Japan continues to lead in adopting genomic medicine, with strong collaborations between public and private sectors to develop advanced diagnostic and therapeutic solutions

- China and India are witnessing significant advancements in genomics, including local startups, partnerships with global companies, and investment in national genome sequencing programs, which are boosting the accessibility and affordability of genomic technologies across the region

Digital Genome Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Illumina, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- QIAGEN (Germany)

- Agilent Technologies, Inc. (U.S.)

- PacBio (U.S.)

- F. Hoffmann-La Roche AG (Switzerland)

- Bio-Rad Laboratories, Inc. (U.S.)

- Oxford Nanopore Technologies plc. (U.K.)

- PerkinElmer (U.S.)

- BGI (China)

- BIOMÉRIEUX (France)

- GE Healthcare (U.S.)

- Labcorp (U.S.)

- Bruker Spatial Biology, Inc. (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Lineagen, Inc. (U.S.)

- GRAIL, Inc. (U.S.)

- 23andMe, Inc. (U.S.)

Latest Developments in Global Digital Genome Market

- In March 2025, The Alliance for Genomic Discovery announced the completion of sequencing 250,000 whole genomes. This milestone aims to accelerate drug discovery and enhance the understanding of genetic variations associated with various diseases

- In September 2024, Variantyx introduced Genomic Unity 2.0, an advanced whole-genome diagnostic test that integrates long-read and short-read sequencing technologies. This innovation aims to provide comprehensive genetic analysis, enhancing diagnostic accuracy and patient care

- In August 2023, London-based biotech company Genomes.io raised Pound 18 million in a funding round led by GEM Digital Limited. The investment is intended to accelerate the company's technological growth and expand the use of its genomic data vault and reporting products, focusing on the secure and private monetization of genomic data

- In May 2022, Gencove partnered with NEOGEN Corporation to introduce InfiniSEEK, a groundbreaking and affordable solution for whole-genome sequencing and targeted SNP analysis. This collaboration aims to advance genomic research and applications in various fields

- In March 2022, Healthcare solutions company LetsGetChecked acquired Veritas Genetics Inc. and Veritas Intercontinental, both innovators in genomics. This acquisition is part of LetsGetChecked's strategy to expand its capabilities in genetic testing and personalized healthcare services

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.