Global Etanercept Market

Market Size in USD Billion

USD

20.05 Billion

USD

26.81 Billion

2025

2033

USD

20.05 Billion

USD

26.81 Billion

2025

2033

| 2026 - 2033 | |

| USD 20.05 Billion | |

| USD 26.81 Billion | |

| % | |

|

Etanercept Market Size

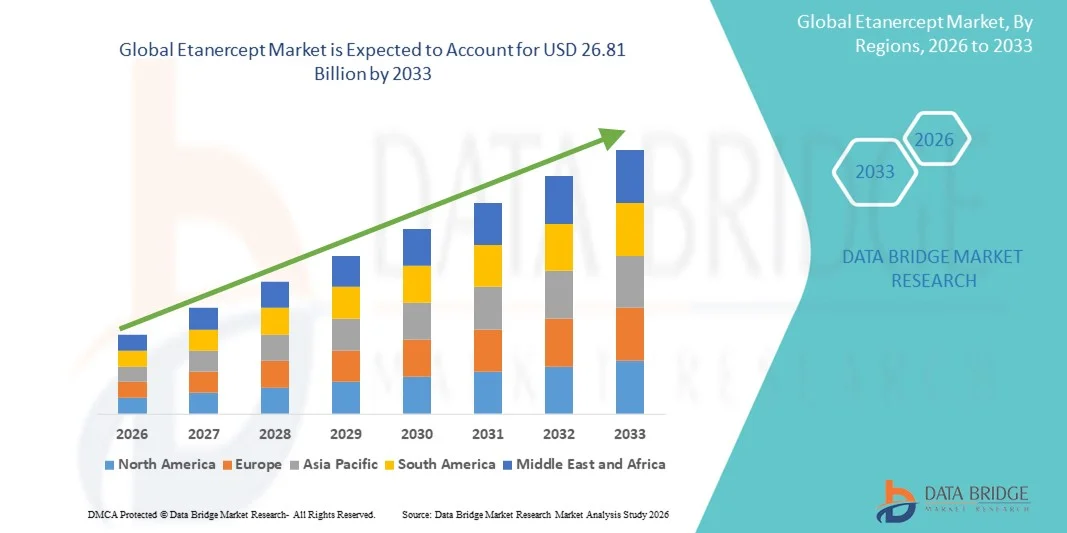

- The global etanercept market size was valued at USD 20.05 billion in 2025 and is expected to reach USD 26.81 billion by 2033, at a CAGR of 3.7% during the forecast period

- The market expansion is primarily driven by the increasing prevalence of autoimmune and inflammatory disorders, coupled with the rising adoption of advanced biologic therapies that offer targeted and effective treatment outcomes

- Furthermore, growing patient preference for reliable, long-term disease-modifying drugs, along with wider availability of biosimilar versions, is positioning etanercept as a key therapeutic option across global healthcare systems. These converging factors are accelerating the use of etanercept products, thereby significantly boosting the industry’s growth

Etanercept Market Analysis

- Etanercept, a biologic TNF-α inhibitor used for treating autoimmune and inflammatory disorders, remains a critical component of modern immunology therapeutics due to its proven efficacy, long-term disease management benefits, and wide adoption across rheumatology and dermatology clinical settings

- The rising demand for etanercept is primarily driven by the increasing global prevalence of rheumatoid arthritis, psoriatic arthritis, ankylosing spondylitis, and plaque psoriasis, along with growing patient preference for targeted biologic therapies over conventional systemic drugs

- North America dominated the etanercept market with the largest revenue share of 42.8% in 2025, supported by high biologics adoption, advanced healthcare infrastructure, and significant utilization in the U.S., where strong reimbursement structures and established physician familiarity with biologics continue to drive widespread etanercept usage across major autoimmune disease segments

- Asia-Pacific is expected to be the fastest-growing region in the etanercept market during the forecast period due to increasing diagnosis rates, expanding biologics availability, and improving access to biosimilar etanercept formulations across emerging markets

- The rheumatoid arthritis segment dominated the etanercept market with a market share of 49.8% in 2025, driven by the high global burden of the disease and the longstanding clinical preference for TNF-α inhibitors such as etanercept, which offer substantial improvements in symptom control, disease progression reduction, and overall quality of life for patients

Report Scope and Etanercept Market Segmentation

|

Attributes |

Etanercept Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Etanercept Market Trends

Growing Shift Toward Biosimilars and Expanded Clinical Utilization

- A significant and accelerating trend in the global etanercept market is the rapid emergence and adoption of biosimilar formulations, which are reshaping the competitive landscape by offering more affordable options while maintaining clinical efficacy across major autoimmune indications

- For instance, the launch of biosimilars such as Benepali and Enbrel biosimilar versions across Europe and Asia has expanded patient access, enabling healthcare systems to reduce biologic therapy costs and driving wider therapeutic penetration

- Improved biologic manufacturing technologies are enhancing formulation stability, delivery devices, and patient usability; for instance, newer autoinjector systems developed by companies such as Samsung Bioepis offer improved ergonomics, consistent dosing, and enhanced patient adherence, contributing to better long-term treatment outcomes

- AI-supported treatment monitoring and predictive analytics are increasingly being integrated into autoimmune disease management, enabling more personalized etanercept therapy; for instance, digital health platforms can analyze patient data to detect early flare patterns and optimize biologic treatment schedules

- The expansion of etanercept prescribing into wider clinical settings including earlier-line therapy in moderate disease categories is reshaping clinician adoption patterns; for instance, rheumatologists and dermatologists in key markets are increasingly recommending biologics sooner for improved disease control and quality-of-life outcomes

- The rising demand for biologics that offer proven long-term safety, sustained response rates, and convenient self-administration formats is accelerating the shift toward etanercept and its biosimilars, especially as patients prioritize accessible and manageable chronic disease therapies across global healthcare systems

Etanercept Market Dynamics

Driver

Growing Demand Due to Rising Autoimmune Disease Burden and Biologic Adoption

- The increasing global prevalence of autoimmune conditions such as rheumatoid arthritis, plaque psoriasis, and ankylosing spondylitis, combined with growing awareness of effective biologic options, is a major driver supporting the expanding demand for etanercept-based therapies

- For instance, in 2025 multiple manufacturers expanded production capacity for etanercept biosimilars to meet rising patient needs across Europe and Asia, with strategic collaborations enabling large-scale distribution and improved affordability

- As patients and healthcare providers increasingly seek advanced therapies capable of offering sustained symptom control and disease-modifying benefits, etanercept provides compelling advantages over conventional systemic treatments through targeted TNF-α inhibition

- Furthermore, the expanding acceptance of self-injectable biologics and the overall shift toward long-term chronic care management are positioning etanercept as an essential therapy integrated into evolving treatment algorithms across key regions

- The convenience of autoinjector pens, broader insurance coverage in developed nations, and the rising number of specialist clinics offering biologic administration are additional factors driving the widespread utilization of etanercept for chronic autoimmune disorders

Restraint/Challenge

Skin Irritation Issues and Regulatory Compliance Hurdle

- Safety-related concerns such as injection-site reactions, skin irritation, and potential immune suppression remain notable challenges associated with etanercept, particularly for new patients or those requiring long-term biologic therapy

- For instance, reports of adverse events associated with TNF-α inhibitors have led some patients to discontinue therapy prematurely, prompting clinicians to closely monitor tolerability and adjust treatment plans based on individual risk profiles

- Addressing these safety considerations through enhanced patient education, improved delivery devices, and ongoing post-marketing surveillance is essential for maintaining confidence in etanercept; manufacturers highlight robust safety data to support continued use

- In addition, the rigorous regulatory approval processes for biosimilars and biologic therapies particularly regarding interchangeability and long-term equivalence present a significant hurdle for companies aiming to enter high-value markets such as the U.S. and Europe

- While biosimilars offer cost advantages, regulatory compliance requirements, complex manufacturing, and the need for extensive clinical studies can hinder rapid market penetration, especially for smaller firms with limited resources

- Overcoming these challenges through advanced biologic engineering, stronger pharmacovigilance frameworks, and harmonized regulatory pathways will be vital to support sustained growth of the global etanercept market

Etanercept Market Scope

The market is segmented on the basis of drug type, application, dosage, route of administration, and distribution channel.

- By Drug Type

On the basis of drug type, the etanercept market is segmented into enbrel, benepali, and others. The Enbrel segment dominated the market in 2025 due to its strong global presence, extensive clinical validation, and long-standing use in treating rheumatoid arthritis, psoriatic arthritis, and other autoimmune diseases. Clinicians widely prefer Enbrel because of its proven therapeutic consistency and availability in convenient autoinjector formats that support self-administration. The segment also benefits from high reimbursement coverage across the U.S. and Europe, driving large-scale adoption among chronic disease patients. Continuous real-world evidence and established safety profiles further reinforce trust among physicians and healthcare systems. The strong manufacturing and supply chain capabilities behind the brand also help maintain market leadership through stable availability and clinical reliability.

The Benepali segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing global adoption of biosimilars and the demand for more affordable biologic therapies. Benepali offers clinical equivalence to the originator drug at a lower cost, making it a preferred option for healthcare systems seeking to reduce biologic treatment expenditure. The segment also benefits from expanding payer support and broader accessibility in Europe and emerging markets. Improvements in delivery devices and enhanced patient-friendly features support higher adherence. Growing physician confidence in biosimilar performance is accelerating uptake, especially in markets where cost sensitivity is high. Continued expansion of biosimilar distribution networks will further fuel strong growth in the coming years.

- By Application

On the basis of application, the etanercept market is segmented into juvenile idiopathic arthritis (jia), ankylosing spondylitis, rheumatoid arthritis, psoriatic arthritis, and others. The Rheumatoid Arthritis segment dominated the market in 2025 with a market share of 49.8% owing to the high prevalence of the disease and the long-established clinical role of etanercept in providing disease-modifying benefits. Rheumatologists rely heavily on etanercept for its ability to reduce inflammation, slow joint damage progression, and improve overall patient functioning. Its strong safety profile and suitability for long-term therapy make it a preferred biologic for chronic disease management. Widespread availability of both branded and biosimilar versions helps meet demand across diverse healthcare systems. Growing diagnosis rates and increasing awareness of advanced treatment options also support sustained uptake. The segment benefits further from strong inclusion in clinical guidelines and insurance coverage across multiple regions.

The Psoriatic Arthritis segment is expected to witness the fastest growth from 2026 to 2033 due to expanding awareness of early treatment interventions and the rising global burden of psoriatic disease. Etanercept is widely used for its dual benefit in addressing both joint inflammation and skin symptoms, offering comprehensive disease control. Increasing referrals between dermatologists and rheumatologists are expanding patient access to biologic therapies. Enhanced patient preference for biologics with convenient self-administration formats further supports rapid adoption. Healthcare providers are increasingly recommending biologics earlier in the treatment cycle, contributing to market acceleration. Growing availability of biosimilars is also making etanercept more accessible for patients in cost-sensitive markets.

- By Dosage

On the basis of dosage, the etanercept market is segmented into injection, solution, and others. The Injection segment dominated the market in 2025 as subcutaneous injections remain the standard dosage form for etanercept across all major indications. Prefilled syringes and autoinjectors support ease of administration and enhance adherence, particularly for long-term therapy. The reliability of injectable formats in delivering consistent dosing and therapeutic effectiveness ensures sustained clinical preference. Healthcare professionals also favor injections due to their predictable pharmacokinetics and simple administration process. For many patients, injectable dosing aligns well with structured treatment routines recommended by providers. As a result, injection-based etanercept formats remain the most widely prescribed and utilized globally.

The Solution segment is anticipated to experience the fastest growth from 2026 to 2033 as advancements in formulation technologies improve the stability and patient usability of liquid etanercept products. Ready-to-use solutions help reduce administration complexity for patients and caregivers by eliminating preparation steps. Increasing demand for biologics that simplify self-administration is supporting rapid uptake of this dosage form. Enhanced formulation characteristics, such as reduced viscosity, contribute to a more comfortable injection experience. Healthcare systems are also encouraging the use of simplified dosing formats to improve treatment adherence. These factors collectively position the solution segment for strong future growth.

- By Route of Administration

On the basis of route of administration, the etanercept market is segmented into subcutaneous and others. The Subcutaneous segment dominated the market in 2025 since subcutaneous administration is the primary and most effective method for delivering etanercept for autoimmune conditions. This route ensures efficient drug absorption and allows patients to self-inject at home using autoinjectors or prefilled syringes. The convenience and independence offered by subcutaneous delivery significantly enhance long-term adherence. Healthcare providers prefer this route because it reduces the need for frequent hospital visits and supports chronic disease management. For many patients, training to use subcutaneous devices is straightforward, making the method highly acceptable. These advantages ensure that subcutaneous administration remains the dominant approach globally.

The Others segment is expected to witness the fastest growth from 2026 to 2033 as emerging delivery innovations and supportive care technologies begin to diversify administration options. Although not widely adopted today, interest in alternative delivery mechanisms is increasing among biopharmaceutical developers. Novel device-based systems, slow-release mechanisms, and emerging formulation sciences are expanding possibilities beyond traditional delivery routes. These advancements may improve patient comfort and address unmet needs in certain specialized clinical scenarios. Growing investments in research are expected to gradually introduce new administration pathways. As innovation accelerates, this segment is such asly to gain traction in select parts of the market.

- By Distribution Channel

On the basis of distribution channel, the global etanercept market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market in 2025 due to the specialized nature of biologic therapy initiation, which typically requires physician supervision and structured patient assessment. Hospitals remain the central point for diagnosing autoimmune conditions and determining appropriate biologic interventions. For instance, initiation protocols, monitoring practices, and pharmacovigilance activities are commonly managed within hospital settings. Hospitals also benefit from preferred reimbursement frameworks for biologics, ensuring smoother patient access. In addition, patient training for self-injection often begins in hospital pharmacies under professional guidance. These factors collectively make hospital pharmacies the leading distribution channel.

The Online Pharmacy segment is projected to witness the fastest growth during 2026–2033 as digital healthcare adoption accelerates and e-pharmacy platforms expand specialty drug capabilities. Patients increasingly prefer home delivery services, especially for biologics requiring consistent monthly refills. Online pharmacies now employ temperature-controlled logistics to support safe biologic transport, improving reliability and patient trust. Subscription-based delivery models and transparent pricing further improve access for chronic disease patients. Regulatory support for electronic prescriptions and telehealth is also driving growth across several regions. As convenience and accessibility become top priorities for patients, online pharmacies are positioned for rapid expansion.

Etanercept Market Regional Analysis

- North America dominated the etanercept market with the largest revenue share of 42.8% in 2025, supported by high biologics adoption, advanced healthcare infrastructure, and significant utilization in the U.S., where strong reimbursement structures and established physician familiarity with biologics continue to drive widespread etanercept usage across major autoimmune disease segments

- The market benefits from strong healthcare infrastructure, wide availability of specialty biologics, and high treatment adoption rates among both physicians and patients owing to well-established reimbursement systems

- In addition, the presence of major manufacturers, strong regulatory support for biologics, and increasing acceptance of biosimilars contribute to maintaining North America’s leadership, with consistent growth fueled by rising biologic prescriptions and expanding patient access programs

U.S. Etanercept Market Insight

The U.S. etanercept market captured the largest revenue share within North America in 2025, supported by the high prevalence of rheumatoid arthritis, psoriasis, and other autoimmune disorders that continue to drive strong biologics utilization. Increasing patient access to specialty treatments through advanced insurance coverage and structured reimbursement pathways significantly contributes to market leadership. The rise in specialty pharmacy networks, along with growing physician preference for established TNF inhibitors, reinforces strong etanercept demand. Moreover, continuous awareness programs, evolving treatment guidelines, and the presence of major pharmaceutical manufacturers further strengthen adoption across the U.S. market.

Europe Etanercept Market Insight

The Europe etanercept market is projected to grow at a substantial CAGR throughout the forecast period, driven by the increasing burden of chronic inflammatory diseases and the adoption of cost-effective biosimilars. The region’s emphasis on affordable treatment access, coupled with supportive regulatory frameworks for biosimilar approval, is enabling wider patient reach. Growing awareness of biologic therapies and improvements in diagnostic rates also contribute to market expansion. Europe continues to see rising usage across hospital and specialty care settings, strengthening the overall uptake of etanercept products.

U.K. Etanercept Market Insight

The U.K. etanercept market is anticipated to grow steadily during the forecast period, supported by strong National Health Service (NHS) reimbursement policies that promote access to biologics and biosimilars. The increasing incidence of autoimmune diseases and evolving clinical guidelines encouraging early biologic intervention contribute to rising demand. Growing acceptance of biosimilars among healthcare providers further boosts market expansion. In addition, improvements in healthcare infrastructure and patient monitoring systems support broader adoption in both hospital and outpatient care settings.

Germany Etanercept Market Insight

The Germany etanercept market is expected to expand at a notable CAGR during the forecast period, driven by the country’s advanced healthcare system and high biologics adoption rates. Germany’s strong focus on innovation and treatment optimization supports increasing use of biosimilars for cost efficiency and improved patient access. The presence of leading pharmaceutical companies and well-developed distribution networks further enhances market penetration. In addition, rising awareness of autoimmune disorders and increased screening rates contribute to sustained growth in etanercept prescriptions.

Asia-Pacific Etanercept Market Insight

The Asia-Pacific etanercept market is poised to grow at the fastest CAGR during the forecast period, fueled by increasing disease prevalence, expanding healthcare access, and rising awareness of biologic therapies. Countries such as China, Japan, and India are witnessing significant improvements in treatment infrastructure and affordability, driving broader adoption of etanercept and its biosimilars. Government initiatives promoting healthcare modernization and greater availability of lower-cost biosimilar options are accelerating market expansion. As the region continues to enhance biologic production capabilities, the accessibility of etanercept is expected to increase across both urban and rural populations.

Japan Etanercept Market Insight

The Japan etanercept market is gaining momentum due to strong clinical acceptance of biologics and rising diagnosis rates for rheumatoid arthritis and related autoimmune disorders. The country’s focus on high-quality healthcare and advanced therapeutic options continues to support sustained etanercept use. Growing integration of digital health tools for disease monitoring is improving treatment precision, boosting physician confidence in biologic therapies. In addition, Japan’s aging population, which experiences higher autoimmune disease incidence, is expected to further drive demand during the forecast period.

India Etanercept Market Insight

The India etanercept market accounted for a significant revenue share within Asia-Pacific in 2025, supported by rising autoimmune disease awareness and expanding access to rheumatology and dermatology care. Increasing affordability of biosimilars and the presence of strong domestic pharmaceutical manufacturers contribute to wider patient adoption. The country’s rapidly expanding healthcare infrastructure, along with government-led initiatives promoting chronic disease management, supports consistent market growth. Furthermore, rising middle-class income levels and demand for advanced treatment options are accelerating the uptake of etanercept across hospitals and specialty clinics.

Etanercept Market Share

The Etanercept industry is primarily led by well-established companies, including:

- Amgen Inc. (U.S.)

- Biogen (U.S.)

- SAMSUNG (South Korea)

- Lupin (India)

- Cipla (India)

- YL Biologics (Japan)

- Novartis AG (Switzerland)

- Intas Pharmaceuticals (India)

- Hisun Pharmaceuticals (China)

- Shanghai CP Guojian Pharmaceutical (China)

- AryoGen Pharmed (Iran)

- Celltrion (South Korea)

- Organon (U.S.)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Fresenius Kabi (Germany)

- Hanmi Pharmaceutical (South Korea)

- Zydus Cadila (India)

- Biocon (India)

What are the Recent Developments in Global Etanercept Market?

- In April 2025, Sandoz filed a major antitrust lawsuit against Amgen in the U.S., alleging that the company constructed an unlawful “patent thicket” to block market entry of its etanercept biosimilar, Erelzi, which was FDA-approved years earlier. Sandoz claims Amgen’s patent strategy artificially extended Enbrel’s protection period, preventing patient access to lower-cost alternatives and inflating healthcare expenditures

- In April 2025, Forbes published an analysis highlighting the unusually prolonged monopoly of Enbrel in the U.S. market, despite the FDA approving two etanercept biosimilars Erelzi and Eticovo years earlier. The article emphasized that patent litigation and exclusivity strategies continued to prevent biosimilar launches

- In May 2024, Lupin officially launched Rymti in Canada following its regulatory approval, enabling nationwide availability of the biosimilar through a commercialization agreement with Sandoz. This launch immediately broadened treatment access for patients requiring etanercept, particularly those in provinces with supportive biosimilar switching policies

- In September 2023, the U.S. FDA granted interchangeability status to Eticovo (etanercept-ykro), developed by Samsung Bioepis, marking a major regulatory milestone for the biosimilar. Interchangeability allows pharmacists in many states to substitute Eticovo for Enbrel without consulting the prescriber, potentially accelerating adoption and reducing treatment costs

- In September 2022, Health Canada granted approval for Rymti, Lupin’s etanercept biosimilar, across all indications of reference product Enbrel, including rheumatoid arthritis, ankylosing spondylitis, and psoriatic arthritis. The approval followed comprehensive analytical, clinical, and pharmacokinetic comparisons confirming biosimilarity

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.