Global Health Medical Simulation Software Market

Market Size in USD Billion

CAGR :

%

USD

2.96 Billion

USD

8.99 Billion

2025

2033

USD

2.96 Billion

USD

8.99 Billion

2025

2033

| 2026 –2033 | |

| USD 2.96 Billion | |

| USD 8.99 Billion | |

| % | |

|

Health/Medical Simulation Software Market Size

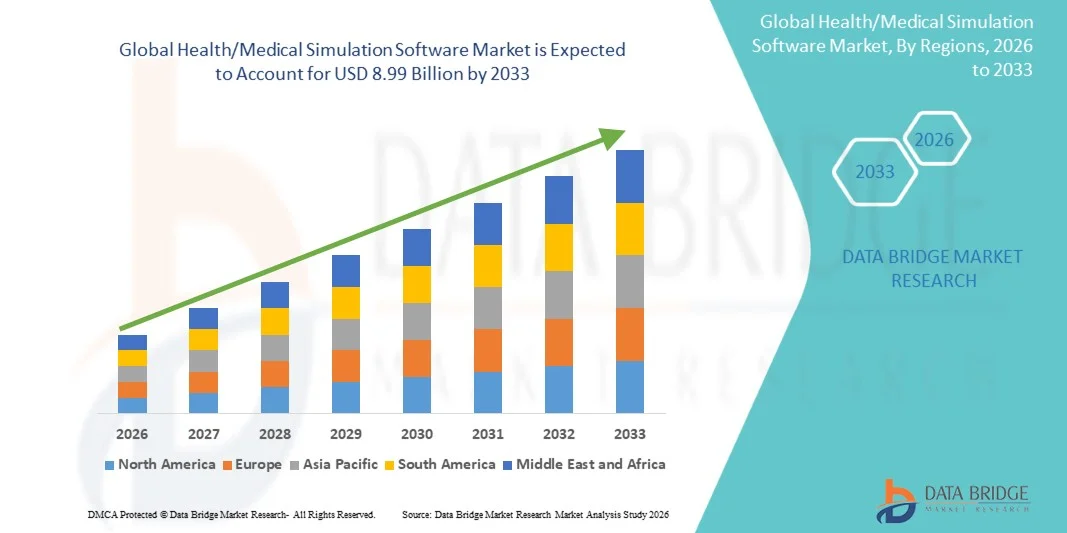

- The global health/medical simulation software market size was valued at USD 2.96 billion in 2025 and is expected to reach USD 8.99 billion by 2033, at a CAGR of 14.90% during the forecast period

- The market growth is largely fueled by the increasing adoption of digital training tools and advancements in simulation technologies within healthcare education, leading to improved clinical training outcomes across academic institutions and healthcare facilities

- Furthermore, rising demand for risk-free, cost-effective, and scalable training solutions for medical professionals is establishing simulation software as a critical component of modern healthcare education and workforce development. These converging factors are accelerating the uptake of medical simulation software solutions, thereby significantly boosting the industry's growth

Health/Medical Simulation Software Market Analysis

- Health/medical simulation software, providing virtual platforms for clinical training and education, is increasingly becoming a vital component of modern healthcare systems and academic environments due to its ability to improve clinical competency, enhance patient safety, and deliver immersive, risk-free learning experiences

- The escalating demand for medical simulation software is primarily fueled by the growing need for skilled healthcare professionals, rapid digital transformation in healthcare education, and the increasing adoption of advanced technologies such as virtual reality (VR), augmented reality (AR), and artificial intelligence (AI) to support interactive and realistic training modules

- North America dominated the health/medical simulation software market with the largest revenue share of 40.6% in 2025, supported by advanced healthcare infrastructure, strong presence of leading simulation software providers, and high adoption across medical schools, hospitals, and training centers, with the U.S. witnessing significant integration of simulation-based training programs and continuous investments in healthcare education technologies

- Asia-Pacific is expected to be the fastest growing region in the health/medical simulation software market during the forecast period due to increasing healthcare expenditure, rapid expansion of medical education infrastructure, rising adoption of digital learning solutions, and growing emphasis on improving clinical training standards across emerging economies

- The performance recording software segment dominated the health/medical simulation software market with a market share of 55.4% in 2025, driven by its ability to track, assess, and analyze trainee performance in real-time, enabling educators and institutions to evaluate competencies, identify skill gaps, and improve learning outcomes through data-driven insights

Report Scope and Health/Medical Simulation Software Market Segmentation

|

Attributes |

Health/Medical Simulation Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Health/Medical Simulation Software Market Trends

“Integration of AI, VR, and Immersive Learning Technologies”

- A significant and accelerating trend in the global health/medical simulation software market is the growing integration of artificial intelligence (AI), virtual reality (VR), and augmented reality (AR) into simulation platforms, enhancing the realism and effectiveness of clinical training environments

- For instance, VR-based simulation platforms such as those developed by CAE Healthcare enable learners to practice complex procedures in highly immersive, controlled environments with real-time feedback. Similarly, AI-enabled modules are being used to adapt training scenarios based on user performance

- AI integration in simulation software enables features such as adaptive learning paths, automated performance assessment, and predictive analytics to identify skill gaps and improve training outcomes over time

- The seamless integration of simulation software with learning management systems (LMS) and digital education platforms allows institutions to centralize training, track progress, and manage curricula efficiently across multiple users and locations

- This trend towards more intelligent, immersive, and data-driven training solutions is fundamentally reshaping medical education, with companies such as Laerdal Medical and Simbionix developing advanced platforms that support realistic scenario-based learning and competency evaluation

- The demand for simulation software that incorporates AI-driven analytics and immersive technologies is growing rapidly across academic institutes, hospitals, and military organizations, as healthcare systems increasingly prioritize effective, scalable, and standardized training solutions

- Moreover, the rising use of haptic feedback technologies in simulation systems is improving procedural realism by allowing trainees to experience tactile responses during simulated clinical procedures, further enhancing skill development

Health/Medical Simulation Software Market Dynamics

Driver

“Growing Need for Skilled Healthcare Workforce and Risk-Free Training Solution”

- The increasing global demand for skilled healthcare professionals, coupled with the need for standardized and risk-free clinical training, is a significant driver for the heightened adoption of medical simulation software

- For instance, in recent years, institutions such as medical universities and teaching hospitals have increasingly adopted simulation-based curricula to improve clinical competency and reduce errors in real-world patient care

- As healthcare systems face workforce shortages and rising patient volumes, simulation software offers a safe environment to train practitioners without compromising patient safety, thereby improving overall care quality

- Furthermore, the growing emphasis on competency-based education and certification requirements is encouraging the integration of simulation tools into medical training programs and professional development initiatives

- The convenience of virtual training modules, remote accessibility, and the ability to repeat complex scenarios multiple times are key factors propelling the adoption of simulation software across academic institutes, hospitals, and defense organizations

- In addition, increasing collaboration between healthcare institutions and simulation software providers is accelerating the development of customized training modules tailored to specific clinical specialties and learning objectives

Restraint/Challenge

“High Implementation Costs and Limited Infrastructure in Developing Regions”

- Concerns surrounding the high initial investment and operational costs of advanced medical simulation software and associated hardware pose a significant challenge to broader market penetration

- For instance, high-fidelity simulation systems and immersive VR setups often require substantial investment in equipment, maintenance, and trained personnel, making adoption difficult for smaller institutions and budget-constrained organizations

- Addressing these cost and infrastructure barriers through scalable cloud-based solutions, modular simulation platforms, and affordable software licensing models is crucial for expanding accessibility and adoption

- In addition, limited digital infrastructure and lack of trained instructors in developing regions further hinder the effective implementation of simulation-based training solutions

- While awareness of simulation benefits is increasing, the perceived complexity and resource requirements of deploying these systems can slow down adoption among new users

- Overcoming these challenges through cost optimization, training support, and improved accessibility will be vital for sustained growth of the medical simulation software market

- Furthermore, interoperability issues between different simulation platforms and existing healthcare IT systems can create integration challenges for institutions seeking unified training environments

- Moreover, concerns related to data privacy and compliance with healthcare regulations can add additional layers of complexity, particularly when handling sensitive training data and performance analytics

Health/Medical Simulation Software Market Scope

The market is segmented on the basis of software type, end user, and fidelity.

- By Software Type

On the basis of software type, the health/medical simulation software market is segmented into performance recording software and virtual tutors. The performance recording software segment dominated the market with the largest revenue share of 55.4% in 2025, driven by its ability to capture, track, and evaluate trainee performance during simulation exercises. Healthcare institutions and academic centers increasingly rely on these tools to assess competencies, identify skill gaps, and ensure standardized training outcomes. The growing emphasis on data-driven education and objective performance assessment further supports the adoption of performance recording solutions. In addition, integration with analytics dashboards and learning management systems enhances usability for instructors and administrators. The demand is also strengthened by regulatory and accreditation requirements that emphasize measurable training outcomes. Overall, its critical role in evaluation and feedback makes it the most widely adopted software type.

The virtual tutors segment is anticipated to witness the fastest growth from 2026 to 2033, driven by increasing demand for personalized, AI-enabled learning experiences in medical education. Virtual tutors leverage artificial intelligence to provide real-time guidance, adaptive learning pathways, and interactive feedback tailored to individual learner performance. These solutions are gaining traction as institutions shift toward self-paced and remote learning models. The rising adoption of digital education platforms and the need for scalable training solutions are further accelerating growth. Virtual tutors also help reduce instructor workload while maintaining consistent training quality. Continuous advancements in natural language processing and AI are expected to further enhance their capabilities and adoption across academic institutes and healthcare training programs.

- By End User

On the basis of end user, the health/medical simulation software market is segmented into academic institutes, hospitals, military organizations, and other end users. The academic institutes segment dominated the market with the largest revenue share in 2025, driven by the widespread integration of simulation-based learning into medical, nursing, and allied health curricula. Universities and training institutions increasingly use simulation software to provide students with hands-on clinical experience in a controlled environment. The growing number of healthcare education programs and rising emphasis on competency-based training further support this dominance. Academic institutes also benefit from simulation tools for standardized assessment and certification preparation. In addition, collaborations between educational institutions and software providers are enhancing curriculum integration and accessibility. The need to improve patient safety by training students before real-world exposure further reinforces adoption in this segment.

The hospitals segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing focus on continuous professional development and clinical skill enhancement among healthcare practitioners. Hospitals are increasingly adopting simulation software to train staff in emergency response, surgical procedures, and critical care scenarios. The growing need to minimize medical errors and improve patient outcomes is encouraging healthcare facilities to invest in simulation-based training solutions. Simulation platforms also enable hospitals to conduct multidisciplinary team training and scenario-based drills. The integration of simulation tools into hospital training programs supports ongoing skill validation and compliance with regulatory standards. Rising investments in healthcare infrastructure and digital transformation initiatives further contribute to the rapid adoption of simulation software in hospitals.

- By Fidelity

On the basis of fidelity, the health/medical simulation software market is segmented into low-fidelity, medium-fidelity, and high-fidelity simulation. The high-fidelity segment dominated the market with the largest revenue share in 2025, driven by its ability to provide highly realistic and immersive training environments that closely replicate real clinical scenarios. High-fidelity simulations incorporate advanced mannequins, realistic physiological responses, and integrated software systems, making them ideal for complex procedure training. These solutions are widely used in hospitals and academic institutions for critical care training, surgical practice, and emergency response scenarios. The growing demand for realistic, hands-on experience in medical education is a key factor supporting this segment’s dominance. In addition, high-fidelity systems are often preferred for advanced competency assessments and certification programs. Despite higher costs, their effectiveness in improving clinical preparedness drives strong adoption globally.

The medium-fidelity segment is expected to witness the fastest growth from 2026 to 2033, driven by its balance between cost, functionality, and realism. Medium-fidelity simulators offer a practical alternative for institutions seeking effective training solutions without the high investment required for high-fidelity systems. These solutions are increasingly adopted by emerging economies and mid-sized training institutions. The growing expansion of medical education infrastructure and the need for scalable training tools are key growth drivers. Medium-fidelity systems are also easier to deploy and maintain, making them accessible to a wider range of end users. Their ability to support a variety of training scenarios while maintaining affordability positions them as a rapidly growing segment in the market.

Health/Medical Simulation Software Market Regional Analysis

- North America dominated the health/medical simulation software market with the largest revenue share of 40.6% in 2025, supported by advanced healthcare infrastructure, strong presence of leading simulation software providers, and high adoption across medical schools, hospitals, and training centers

- Organizations in the region highly value the benefits of simulation-based training, including improved clinical competency, enhanced patient safety, and the ability to deliver standardized and measurable learning outcomes across healthcare professionals

- This widespread adoption is further supported by significant investments in healthcare education technologies, early integration of simulation into medical curricula, and a strong presence of leading simulation software providers, establishing the region as a key hub for innovation and adoption in medical simulation solutions

U.S. Health/Medical Simulation Software Market Insight

The U.S. health/medical simulation software market captured the largest revenue share within North America, fueled by the rapid adoption of advanced digital learning tools and the strong presence of leading healthcare institutions and simulation solution providers. Healthcare organizations and academic institutes in the country are increasingly prioritizing simulation-based training to enhance clinical competency and improve patient safety. The growing preference for technology-enabled medical education, combined with robust demand for AI-driven analytics, VR/AR-based training, and cloud-based platforms, further propels the industry. Moreover, the increasing integration of simulation software into medical curricula and hospital training programs is significantly contributing to the market’s expansion.

Europe Health/Medical Simulation Software Market Insight

The Europe health/medical simulation software market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent healthcare regulations and the escalating need for standardized and competency-based medical training. The increase in healthcare modernization initiatives, coupled with the demand for advanced digital learning solutions, is fostering the adoption of simulation platforms. European institutions are also increasingly focused on patient safety and skill validation, encouraging the use of simulation tools across academic institutes, hospitals, and training centers. The region is experiencing significant growth across medical education, clinical training, and research applications, with simulation software being integrated into both established healthcare systems and new training programs.

U.K. Health/Medical Simulation Software Market Insight

The U.K. health/medical simulation software market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the expanding adoption of simulation-based medical education and the increasing emphasis on improving healthcare training outcomes. Concerns regarding patient safety and the need for highly skilled healthcare professionals are encouraging both academic institutions and hospitals to adopt simulation solutions. The U.K.’s strong digital healthcare ecosystem, alongside its established academic and research infrastructure, is expected to continue stimulating market growth. In addition, the integration of simulation software with digital learning platforms and healthcare systems is supporting broader adoption across training and clinical environments.

Germany Health/Medical Simulation Software Market Insight

The Germany health/medical simulation software market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of advanced medical training technologies and the demand for high-quality, standardized healthcare education. Germany’s well-developed healthcare infrastructure and strong focus on precision, quality, and regulatory compliance are promoting the adoption of simulation-based training in academic institutes and hospitals. The integration of simulation software with digital healthcare systems and ongoing investments in medical research and innovation are further supporting market expansion. In addition, growing emphasis on sustainable and efficient training solutions is encouraging the use of simulation platforms across various healthcare applications.

Asia-Pacific Health/Medical Simulation Software Market Insight

The Asia-Pacific health/medical simulation software market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare investments, rapid expansion of medical education infrastructure, and rising adoption of digital training solutions in countries such as China, Japan, and India. The region’s growing focus on improving healthcare quality and addressing workforce shortages is accelerating the adoption of simulation-based learning. Government initiatives promoting digital healthcare transformation, combined with increasing availability of cost-effective simulation solutions, are further supporting market growth. As APAC emerges as a key hub for healthcare expansion and innovation, simulation software adoption is expanding across academic institutes, hospitals, and training centers.

Japan Health/Medical Simulation Software Market Insight

The Japan health/medical simulation software market is gaining momentum due to the country’s advanced healthcare system, strong technological capabilities, and emphasis on precision in medical training. The adoption of simulation software is driven by the need for efficient training solutions amid an aging population and increasing demand for healthcare services. Healthcare institutions in Japan are increasingly incorporating simulation platforms into training programs to improve clinical outcomes and enhance practitioner skills. The integration of simulation software with other digital healthcare technologies, such as IoT-enabled devices and intelligent learning systems, is further fueling growth across academic and clinical environments.

India Health/Medical Simulation Software Market Insight

The India health/medical simulation software market accounted for a significant market revenue share in Asia-Pacific, attributed to rapid urbanization, expansion of medical education institutions, and increasing adoption of digital learning technologies. India’s growing healthcare education sector and rising number of medical colleges are driving demand for simulation-based training to improve practical skills and clinical readiness among students. The government’s push towards digital healthcare and skill development initiatives, along with increasing investments from private players, is supporting market growth. In addition, the availability of scalable and cost-effective simulation solutions is enabling wider adoption across academic institutes and healthcare organizations.

Health/Medical Simulation Software Market Share

The Health/Medical Simulation Software industry is primarily led by well-established companies, including:

- CAE Inc. (Canada)

- Laerdal Medical (Norway)

- VirtaMed AG (Switzerland)

- SimX, Inc. (U.S.)

- Gaumard Scientific Company, Inc. (U.S.)

- Simulab Corporation (U.S.)

- FundamentalVR Ltd (U.K.)

- Medical-X (U.S.)

- Nasco Healthcare (U.S.)

- Kyoto Kagaku Co., Ltd. (Japan)

- Mentice AB (Sweden)

- Simulaids (U.S.)

- 3B Scientific GmbH (Germany)

- Oxford Medical Simulation (U.K.)

- Osso VR, Inc. (U.S.)

- ImmersiveTouch, Inc. (U.S.)

- OSSimTech (U.S.)

- SIMULATIONiQ (U.S.)

- Biomed Simulation, Inc. (U.S.)

- SimStation, LLC (U.S.)

What are the Recent Developments in Global Health/Medical Simulation Software Market?

- In March 2026, Operative Experience Inc. announced the launch of the TCCS Tier 3 Pro trauma care simulator, a high-fidelity medical training solution designed to support advanced tactical casualty care and medical simulation training globally, addressing rising demand for cost-effective, realistic simulation tools in both military and civilian healthcare education

- In December 2025, SmartWinnr launched a specialized Medical Simulation Center of Excellence aimed at advancing AI-driven simulation tools for pharma and medtech training, enhancing accuracy and compliance readiness for life sciences professionals worldwide

- In November 2025, Humber River Health announced the opening of the James B. Neill Simulation Centre in Ontario, a state-of-the-art facility featuring high-fidelity simulators to train healthcare professionals in critical decision-making and emergency response scenarios, strengthening workforce readiness and patient care capabilities

- In September 2025, Christus Health unveiled a new simulation center at St. Elizabeth Hospital in Beaumont, designed to enhance clinicians’ practical skills through realistic training environments equipped with advanced high-fidelity mannequins for emergency and complex procedure drills

- In August 2025, Munson Healthcare expanded its advanced simulation lab to Cadillac Hospital, bringing high-fidelity simulation capabilities to local staff to improve clinical education, emergency preparedness, and multidisciplinary teamwork through immersive, risk-free training

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.