Global Hypoxia Market

Market Size in USD Million

USD

163.72 Million

USD

291.99 Million

2024

2032

USD

163.72 Million

USD

291.99 Million

2024

2032

| 2025 - 2032 | |

| USD 163.72 Million | |

| USD 291.99 Million | |

| % | |

|

Hypoxia Market Size

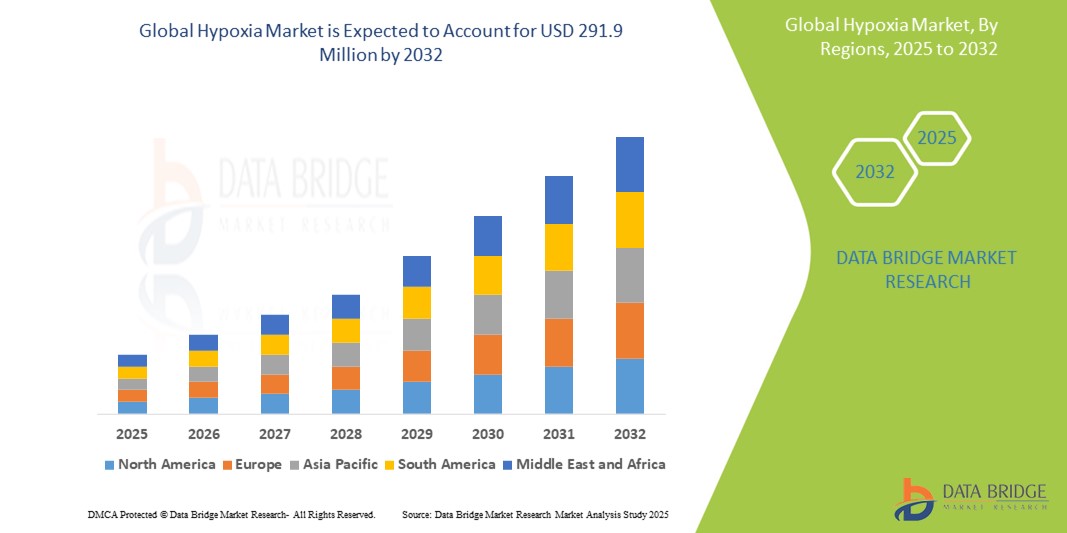

- The global hypoxia market size was valued at USD 163.72 million in 2024 and is expected to reach USD 291.99 million by 2032, at a CAGR of 7.50% during the forecast period

- The market growth is largely fuelled by the rising prevalence of respiratory conditions, cardiovascular diseases, and other medical conditions that lead to insufficient oxygen supply in the body. This is further propelled by ongoing technological advancements in oxygen therapy and monitoring devices, enhancing diagnostic capabilities and treatment outcomes

- Furthermore, rising awareness of hypoxia and its implications, coupled with increasing consumer demand for effective, non-invasive, and convenient solutions for managing oxygen levels, is establishing hypoxia solutions as a critical component of modern healthcare. These converging factors are accelerating the uptake of hypoxia solutions, thereby significantly boosting the industry's growth

Hypoxia Market Analysis

- The hypoxia market encompasses a wide range of solutions aimed at diagnosing, monitoring, and treating conditions characterized by insufficient oxygen supply to the body's tissues. These solutions are increasingly vital components of modern healthcare systems in both clinical and home settings due to their enhanced capabilities in improving patient outcomes, facilitating real-time monitoring, and integrating with advanced medical technologies

- The escalating demand for hypoxia solutions is primarily fueled by the widespread adoption of oxygen therapy devices, growing prevalence of respiratory and cardiovascular diseases (such as COPD, asthma, and sleep apnea), and a rising preference for non-invasive and personalized treatment approaches

- North America dominates the hypoxia market, with the largest revenue share of 41.6%, characterized by advanced healthcare infrastructure, significant research and development investments, high disposable incomes, and a strong presence of key industry players

- Asia-Pacific is expected to be the fastest-growing region in the hypoxia market during the forecast period, with a CAGR of 7.5%. This growth is attributed to increasing urbanization, rising disposable incomes, improving healthcare access, and a growing awareness of hypoxia-related conditions in countries such as China and India

- Hypoxic Hypoxia dominates the Hypoxia market by type, with a market share of 36.4% in 2024, owing to its higher prevalence among respiratory and altitude-related conditions, as well as its critical demand in emergency and intensive care settings

Report Scope and Hypoxia Market Segmentation

|

Attributes |

Hypoxia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Hypoxia Market Trends

“Technological Convergence and User-Centric Innovations”

- A significant and accelerating trend in the global hypoxia market is the deepening integration with advanced analytical capabilities and popular digital health ecosystems. This fusion of technologies is significantly enhancing user convenience and control over their oxygen therapy and monitoring systems

- For instance, portable oxygen concentrators are increasingly featuring smart connectivity, allowing users to monitor their oxygen saturation levels and device performance via smartphone apps. Similarly, continuous positive airway pressure (CPAP) machines can now be integrated with digital platforms, offering users real-time data on their sleep patterns and therapy effectiveness

- Advanced analytical integration in hypoxia solutions enables features such as learning user oxygen needs patterns to potentially suggest therapy optimizations and providing more intelligent alerts based on physiological activity. For instance, some pulse oximeters utilize advanced algorithms to improve accuracy over time and can send intelligent alerts if unusual oxygen level fluctuations are detected. Furthermore, remote monitoring capabilities offer users the ease of continuous oversight, allowing them to track their oxygen saturation and vital signs from anywhere

- The seamless integration of hypoxia solutions with digital health assistants and broader healthcare platforms facilitates centralized control over various aspects of patient care. Through a single interface, users can manage their oxygen delivery alongside medication reminders, activity tracking, and other health devices, creating a unified and automated wellness experience

- This trend towards more intelligent, intuitive, and interconnected hypoxia management systems is fundamentally reshaping user expectations for respiratory care. Consequently, companies such as ResMed and Philips are developing advanced hypoxia solutions with features such as automatic oxygen flow adjustment based on real-time physiological data and remote monitoring compatibility with healthcare provider platforms

- The demand for hypoxia solutions that offer seamless technological integration and user-centric functionalities is growing rapidly across both residential and clinical sectors, as patients and healthcare providers increasingly prioritize convenience and comprehensive health management

Hypoxia Market Dynamics

Driver

“Growing Need Due to Rising Health Awareness and Technological Advancements”

- The increasing prevalence of chronic respiratory and cardiovascular diseases, coupled with accelerating advancements in medical technology, is a significant driver for the heightened demand for hypoxia solutions

- For instance, in early 2024, leading medical device companies announced breakthroughs in compact, portable oxygen delivery systems with enhanced battery life. Such innovations are expected to drive the Hypoxia industry growth in the forecast period by making treatment more accessible and less cumbersome for patients

- As individuals and healthcare providers become more aware of the critical role of oxygen in managing various health conditions and seek improved diagnostic and therapeutic tools, hypoxia solutions offer advanced features such as real-time monitoring, personalized oxygen delivery, and data logging, providing a compelling upgrade over traditional methods

- Furthermore, the growing popularity of home healthcare and the desire for convenient, patient-centric treatment approaches are making hypoxia solutions an integral component of these systems, offering seamless integration with other health monitoring devices and digital health platforms

- The convenience of continuous oxygen supply, remote patient monitoring capabilities for healthcare providers, and the ability to manage conditions through user-friendly interfaces are key factors propelling the adoption of hypoxia solutions in both residential and clinical sectors. The trend towards personalized medicine and the increasing availability of user-friendly hypoxia options further contribute to market growth

Restraint/Challenge

“Concerns Regarding Regulatory Hurdles and High Treatment Costs”

- Concerns surrounding the stringent regulatory approval processes and the relatively high initial and ongoing costs associated with some advanced hypoxia solutions pose a significant challenge to broader market penetration. As hypoxia solutions are medical devices, they are subject to rigorous testing and approval by health authorities (such as FDA, CE), raising anxieties among manufacturers about time-to-market and compliance burdens.

- For instance, high-profile reports of delays in regulatory approvals for new medical devices have made some companies hesitant to invest heavily in certain innovative hypoxia technologies without clear guidance

- Addressing these regulatory concerns through streamlined approval pathways and international harmonization of standards is crucial for fostering innovation. Companies such as Philips Healthcare and ResMed emphasize their adherence to global quality standards and rigorous clinical trials in their marketing to reassure both regulators and potential buyers. In addition, the relatively high initial cost of some advanced hypoxia systems, such as long-term oxygen therapy devices or hyperbaric chambers, compared to more basic interventions, can be a barrier to adoption for price-sensitive consumers, particularly in developing regions or for healthcare systems with limited budgets. While basic pulse oximeters have become more affordable, premium features such as integrated telehealth capabilities or advanced respiratory support often come with a higher price tag

- While prices are gradually decreasing due to technological advancements and economies of scale, the perceived premium for advanced medical technology can still hinder widespread adoption, especially for those without adequate insurance coverage or government support

Hypoxia Market Scope

The Hypoxia market is segmented on the basis of type, disease type, end user, and distribution channel.

- By Type

On the basis of type, the Hypoxia market is segmented into hypoxic hypoxia, anaemic hypoxia, stagnant hypoxia, and histotoxic hypoxia. Hypoxic hypoxia held the largest market revenue share of 36.4% in 2024. This dominance is due to its direct association with respiratory and cardiovascular conditions, which are highly prevalent globally. The market for Hypoxic Hypoxia is driven by the increasing need for oxygen therapy and related medical devices to address insufficient oxygen in the lungs and arterial blood. The continuous rise in chronic lung diseases and high-altitude related health issues further solidifies its leading position.

The histotoxic hypoxia segment is projected to grow at the highest CAGR of 7.9% during the forecast period (2025–2032) in the global hypoxia market. This accelerated growth is attributed to increasing awareness and diagnosis of metabolic and toxicological disorders, such as cyanide poisoning and sepsis, which impair the body’s ability to utilize oxygen at the cellular level.

- By Disease Type

On the basis of disease type, the hypoxia market is segmented into chronic obstructive pulmonary disease (COPD), emphysema, bronchitis, pneumonia, sleep apnoea, pneumothorax, asthma, and others. The chronic obstructive pulmonary disease (COPD) segment held the largest market share of 31.5% in 2024. This is driven by the high global prevalence of COPD and the necessity for long-term oxygen therapy and continuous monitoring solutions.

The sleep apnoea segment is expected to witness the fastest growth rate from 2025 to 2032. This growth is fueled by increasing diagnosis rates, rising awareness of the condition's health implications, and the growing demand for non-invasive treatment options such as CPAP devices that often address nocturnal hypoxia.

- By End User

On the basis of end user, the Hypoxia market is segmented into hospitals, specialty clinics, research centres, and others. The hospitals segment held the largest market revenue share in 2024. Hospitals serve as primary care centers for acute and severe hypoxic conditions, requiring immediate medical intervention and advanced equipment.

The research centres segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing investments in biomedical research, drug discovery for hypoxia-related diseases, and the development of novel diagnostic and therapeutic approaches.

- By Distribution Channel

On the basis of distribution channel, the Hypoxia market is segmented into direct and indirect. The direct distribution channel held the largest market revenue share in 2024. This is due to the nature of medical device sales, where direct engagement between manufacturers and healthcare providers (hospitals, clinics) is common for high-value equipment and personalized solutions, ensuring proper installation, training, and support.

The indirect distribution channel is expected to witness the fastest CAGR from 2025 to 2032. This growth is driven by the expanding network of online pharmacies, medical supply retailers, and home healthcare providers, making oxygen therapy devices and related consumables more accessible to a broader consumer base, particularly for home use and long-term care.

Hypoxia Market Regional Analysis

- North America dominates the hypoxia market with a market share of 41.6% in 2024, driven by a high prevalence of chronic respiratory and cardiovascular diseases, advanced healthcare infrastructure, and strong investment in medical research and development

- Consumers and healthcare providers in the region highly value the sophisticated diagnostic tools, advanced oxygen therapy solutions, and seamless integration offered by modern hypoxia management systems with existing healthcare IT platforms

- This widespread adoption is further supported by high disposable incomes, a well-established regulatory framework that encourages innovation, and the growing preference for personalized medicine and home-based care solutions, establishing hypoxia treatments as a favored solution for both acute and chronic conditions in residential and clinical settings

U.S. Hypoxia Market Insight

The U.S. hypoxia market captured largest revenue share of 75.9% in 2024 within North America. This is fueled by the swift uptake of advanced medical devices and the expanding trend of personalized healthcare. Consumers and healthcare providers are increasingly prioritizing the enhancement of patient outcomes through intelligent oxygen delivery and monitoring systems. The growing preference for home-based care setups, combined with robust demand for remote patient monitoring and digital health platform integration, further propels the Hypoxia industry. Moreover, the increasing integration of telemedicine and AI-powered diagnostics is significantly contributing to the market's expansion.

Europe Hypoxia Market Insight

The Europe hypoxia market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent healthcare regulations and the escalating need for enhanced patient monitoring and treatment in hospitals and homes. The increase in urbanization, coupled with the demand for connected medical devices, is fostering the adoption of hypoxia solutions. European consumers are also drawn to the convenience and efficiency these devices offer. The region is experiencing significant growth across acute care, home care, and long-term care applications, with hypoxia solutions being incorporated into both new healthcare infrastructure and existing facility upgrades.

U.K. Hypoxia Market Insight

The U.K. hypoxia market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating trend of home healthcare and a desire for heightened patient safety and convenience. In addition, concerns regarding chronic respiratory diseases and an aging population are encouraging both patients and healthcare providers to choose advanced oxygen therapy and monitoring solutions. The UK’s embrace of connected medical devices, alongside its robust National Health Service (NHS) and digital health initiatives, is expected to continue to stimulate market growth.

Germany Hypoxia Market Insight

The Germany hypoxia market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of advanced diagnostics and the demand for technologically advanced, eco-conscious solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and sustainability in medical technology, promotes the adoption of hypoxia solutions, particularly in hospitals and home care settings. The integration of hypoxia solutions with electronic health records and telehealth systems is also becoming increasingly prevalent, with a strong preference for secure, privacy-focused solutions aligning with local consumer expectations.

Asia-Pacific Hypoxia Market Insight

The Asia-Pacific hypoxia market is poised to grow at the fastest CAGR of 7.5%, during the forecast period of 2025 to 2032. This is driven by increasing urbanization, rising disposable incomes, and rapid technological advancements in countries such as China, Japan, and India. The region's growing inclination towards digital health and improving healthcare access, supported by government initiatives promoting medical infrastructure development, is driving the adoption of hypoxia solutions. Furthermore, as APAC emerges as a manufacturing hub for medical components and systems, the affordability and accessibility of hypoxia solutions are expanding to a wider consumer base.

Japan Hypoxia Market Insight

The Japan hypoxia market is gaining momentum due to the country’s high-tech culture, rapid urbanization, and demand for advanced healthcare. The Japanese market places a significant emphasis on patient safety and quality of life, and the adoption of hypoxia solutions is driven by the increasing number of elderly individuals and chronic disease patients. The integration of hypoxia solutions with other IoT medical devices, such as continuous glucose monitors and vital sign trackers, is fueling growth. Moreover, Japan's aging population is likely to spur demand for easier-to-use, effective oxygen management solutions in both residential and clinical sectors.

China Hypoxia Market Insight

The China hypoxia market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country's expanding middle class, rapid urbanization, and high rates of technological adoption in healthcare. China stands as one of the largest markets for medical devices globally, and hypoxia solutions are becoming increasingly popular in hospitals, clinics, and home care settings. The push towards modernizing healthcare infrastructure and the availability of increasingly affordable hypoxia options, alongside strong domestic manufacturers, are key factors propelling the market in China.

Hypoxia Market Share

The hypoxia industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Merck KGaA (Germany)

- CASI Pharmaceuticals, Inc. (U.S.)

- Spotlight Labs (U.S.)

- AXXAM S.p.A. (Italy)

- HypOxygen (U.S.)

- Phio Pharmaceuticals (U.S.)

- Coy Laboratory Products, Inc. (U.S.)

- STEMCELL Technologies (Canada)

- Hypoxico Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Pharmaceuticals, Inc. (India)

- HYPOXIA Group s.r.o. (Czech Republic)

Latest Developments in Global Hypoxia Market

- In August 2023, Merck received FDA approval for WELIREG (belzutifan), a hypoxia-inducible factor-2 alpha (HIF-2α) inhibitor, for the treatment of certain tumors associated with Von Hippel-Lindau (VHL) disease. This approval highlights the therapeutic potential of targeting hypoxia-related pathways in cancer treatment, offering a new option for patients with this rare genetic condition

- In May 2023, Amgen announced positive Phase 3 results for tezepelumab (Tezspire), co-developed with AstraZeneca, showing significant reductions in asthma exacerbations across a broad patient population, including those with severe, uncontrolled asthma often associated with airway inflammation and hypoxia. While not directly a hypoxia-targeting drug, its effectiveness in severe asthma has implications for managing conditions that can lead to chronic hypoxia

- In February 2023, ResMed continued to expand its digital health offerings, with increased adoption of its AirView platform, which allows healthcare providers to remotely monitor and manage patients with sleep apnea and other respiratory conditions. This remote monitoring capability is crucial for managing chronic hypoxia conditions, ensuring patients receive optimal therapy and allowing for timely interventions

- In January 2023, Philips announced the expansion of its Philips Respironics DreamStation 2 sleep therapy platform with new features designed to enhance user comfort and adherence. Given that sleep apnea is a major cause of intermittent hypoxia, advancements in CPAP technology directly impact the management of hypoxia and improving patient outcomes in this significant disease segment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.