Global Intestinal Pseudo Obstruction Treatment Market

Market Size in USD Billion

USD

24.87 Billion

USD

36.86 Billion

2024

2032

USD

24.87 Billion

USD

36.86 Billion

2024

2032

| 2025 - 2032 | |

| USD 24.87 Billion | |

| USD 36.86 Billion | |

| % | |

|

Intestinal Pseudo Obstruction Treatment Market Size

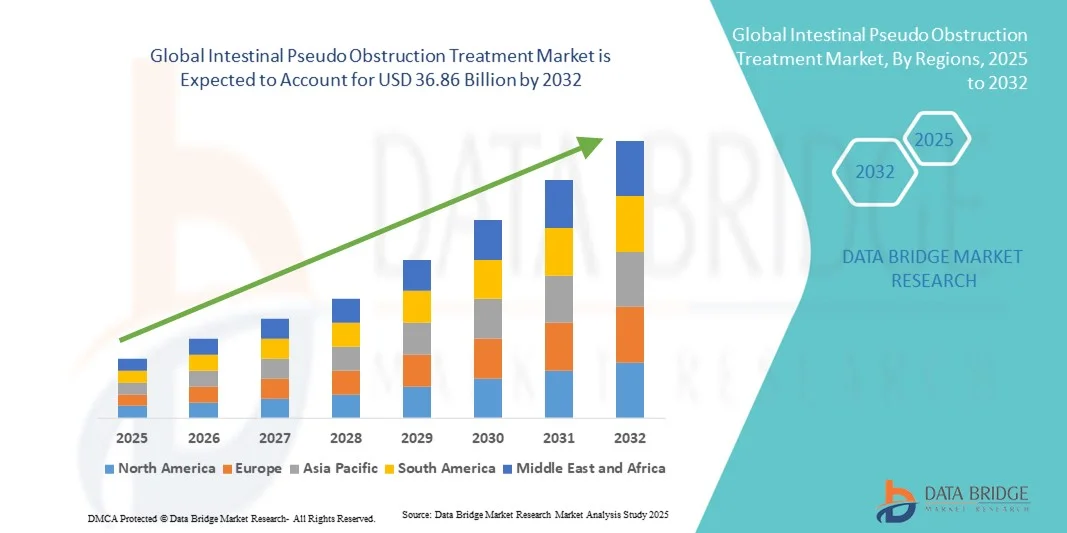

- The global intestinal pseudo obstruction treatment market size was valued at USD 24.87 billion in 2024 and is expected to reach USD 36.86 billion by 2032, at a CAGR of 5.04% during the forecast period

- The market growth is largely driven by increasing awareness and diagnosis of chronic intestinal motility disorders, coupled with advancements in pharmacological therapies, surgical interventions, and supportive care approaches that are enhancing patient management outcomes

- Furthermore, rising demand for effective, minimally invasive, and targeted treatment solutions, alongside ongoing research into novel drug development and improved diagnostic methods, is positioning intestinal pseudo obstruction treatment as a critical focus area in gastroenterology. These factors are accelerating adoption rates, thereby significantly boosting the industry’s growth

Intestinal Pseudo Obstruction Treatment Market Analysis

- Intestinal pseudo obstruction treatments, spanning medications, surgical procedures, dietary interventions, and decompression techniques, are increasingly vital for addressing impaired intestinal motility, with a strong focus on symptom control, complication prevention, and improving patient survival in both acute and chronic cases

- The rising demand for effective therapeutic options is primarily fueled by improved diagnostic capabilities, growing awareness of rare gastrointestinal motility disorders, and continuous research into advanced pharmacological agents and surgical innovations that enhance long-term outcomes

- North America dominated the intestinal pseudo obstruction treatment market with the largest revenue share of 40.3% in 2024, supported by robust healthcare infrastructure, specialized gastroenterology centers, early diagnosis rates, and active R&D initiatives by leading pharmaceutical and medical device companies

- Asia-Pacific is expected to be the fastest growing region in the intestinal pseudo obstruction treatment market during the forecast period due to expanding healthcare access, rising investments in rare disease management, and increasing recognition of gastrointestinal motility disorders in developing economies

- Medication segment dominated the intestinal pseudo obstruction treatment market with a market share of 41.9% in 2024, driven by its frontline role in reducing symptoms such as abdominal pain, bloating, nausea, and constipation, with oral and intravenous drug formulations widely adopted across hospitals and clinics through both hospital and retail pharmacy distribution channels

Report Scope and Intestinal Pseudo Obstruction Treatment Market Segmentation

|

Attributes |

Intestinal Pseudo Obstruction Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Intestinal Pseudo Obstruction Treatment Market Trends

Advancements in Diagnostic and Therapeutic Approaches

- A significant and accelerating trend in the global intestinal pseudo obstruction treatment market is the advancement of diagnostic imaging, manometry, and gastric emptying tests, which are improving early detection and treatment precision for both acute and chronic cases

- For instance, high-resolution manometry is increasingly being used in specialized centers, enabling clinicians to better identify motility dysfunctions and tailor treatment strategies accordingly. Similarly, imaging tests are becoming more sophisticated, aiding in accurate diagnosis

- AI-powered diagnostic support tools are beginning to enhance clinical decision-making, offering physicians improved insights into disease progression, patient response to therapy, and personalized treatment pathways

- The integration of telemedicine and remote patient monitoring technologies is providing patients with access to specialized gastroenterology care and ongoing management of symptoms without the need for frequent hospital visits

- This trend towards advanced diagnostics and digital health integration is reshaping expectations for gastrointestinal disorder management. Consequently, companies and research institutes are investing in novel drug development, surgical innovations, and digital health platforms

- The demand for diagnostic precision and effective multidisciplinary treatment approaches is growing rapidly across both developed and developing regions, as healthcare systems prioritize timely intervention for rare gastrointestinal conditions

Intestinal Pseudo Obstruction Treatment Market Dynamics

Driver

Growing Need Due to Rising Prevalence and Awareness of Motility Disorders

- The increasing recognition of chronic intestinal pseudo obstruction (CIPO) and other severe motility disorders, coupled with rising awareness campaigns, is a significant driver for the demand for advanced treatment solutions

- For instance, in March 2024, leading gastroenterology associations highlighted CIPO as a critical unmet medical need, calling for better diagnostic tools and patient access to specialized care. Such initiatives are expected to drive treatment adoption in the forecast period

- As patients and healthcare providers seek effective management of life-threatening complications, treatment options including medications, surgery, and decompression are viewed as vital components of care, offering a clear upgrade over conventional symptomatic relief approaches

- Furthermore, improvements in diagnostic accuracy and the expansion of gastrointestinal specialty centers are ensuring early detection, which enhances treatment success rates and patient outcomes

- The rising number of research collaborations and clinical trials targeting rare gastrointestinal disorders are further propelling innovation, supporting a growing pipeline of therapies with potential global adoption

- The convenience of accessing treatment through multiple channels such as hospital pharmacies, retail outlets, and online platforms is also driving growth, particularly in regions where healthcare access is rapidly improving.

Restraint/Challenge

Diagnostic Complexity and High Treatment Costs

- The complex and often time-consuming diagnostic process for intestinal pseudo obstruction, which relies on multiple tests such as biopsies, imaging, and manometry, poses a significant challenge to timely intervention

- For instance, patients often undergo years of testing before receiving a confirmed diagnosis, which delays effective treatment and contributes to worsening of symptoms and complications

- Concerns surrounding the high costs of long-term management, including hospitalizations, surgeries, and nutritional support, further limit access, particularly in low- and middle-income regions where healthcare coverage is limited

- The absence of standardized treatment guidelines across regions contributes to inconsistent care practices, creating barriers to uniform adoption of advanced therapies and interventions

- In addition, the limited availability of specialized gastroenterology centers and trained professionals restricts diagnosis and treatment in many developing markets, leaving a large pool of patients underserved

- Overcoming these challenges through expanded healthcare infrastructure, reduced treatment costs, clinical education, and accelerated regulatory approvals for new therapies will be crucial for sustaining global market growth

Intestinal Pseudo Obstruction Treatment Market Scope

The market is segmented on the basis of type, treatment, diagnosis, symptoms, dosage, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the intestinal pseudo obstruction treatment market is segmented into acute and chronic intestinal pseudo obstruction. The chronic segment dominated the market in 2024, as it accounts for the majority of diagnosed cases worldwide and requires ongoing medical attention. Patients with chronic intestinal pseudo obstruction (CIPO) rely heavily on repeated hospitalizations, medications, dietary management, and nutritional support, which increases healthcare utilization. The complexity of this condition leads to higher adoption of multidisciplinary treatment approaches in advanced healthcare systems. Rising awareness of chronic motility disorders, along with improved diagnostic techniques such as manometry and imaging tests, is further driving dominance of this segment. In addition, the long-term nature of chronic pseudo obstruction creates sustained demand for both pharmacological and surgical solutions, reinforcing its revenue share leadership.

The acute segment is anticipated to witness the fastest growth rate from 2025 to 2032, primarily due to increasing recognition of acute presentations that mimic mechanical obstruction but lack structural blockage. Hospitals are reporting a higher frequency of emergency admissions for acute pseudo obstruction, requiring rapid diagnosis and urgent treatment interventions. Improved imaging technologies such as CT and ultrasound are helping clinicians differentiate acute pseudo obstruction from mechanical causes quickly, ensuring timely care. Furthermore, expansion of emergency care facilities in developing countries is contributing to higher diagnosis rates of acute forms. Growing awareness among physicians regarding acute cases and their management with decompression or medications is accelerating growth. The segment is also benefiting from improvements in supportive care for sudden episodes, leading to faster adoption during the forecast period.

- By Treatment

On the basis of treatment, the intestinal pseudo obstruction treatment market is segmented into medication, surgery, diet, decompression, and others. The medication segment dominated the market in 2024 with a market share of 41.9%, driven by its frontline role in managing symptoms such as nausea, bloating, constipation, and abdominal pain. Medications including prokinetics, antibiotics, and antiemetics are widely prescribed across both acute and chronic cases, making them indispensable for patient care. Their availability in different formulations such as tablets and injections ensures broad accessibility across healthcare settings. Hospitals and retail pharmacies report consistent demand for medications due to their cost-effectiveness and non-invasive nature. The rise in research initiatives focused on novel drug development is further strengthening the medication segment’s dominance. In addition, medications are often combined with dietary adjustments and supportive therapies, increasing their adoption across multiple care pathways.

The surgery segment is projected to grow at the fastest rate during 2025–2032, as it becomes increasingly important in severe or refractory cases where medication fails to provide adequate relief. Surgical interventions such as bowel resections, intestinal decompression, or intestinal pacing are being adopted in tertiary care hospitals with advanced facilities. The development of minimally invasive surgical techniques is enhancing recovery rates and reducing post-operative complications, encouraging adoption. A rise in the number of patients requiring surgical solutions due to severe dilation or risk of perforation is driving growth. In addition, advancements in surgical devices and the expansion of gastrointestinal specialty units are making complex procedures more widely available. The demand for surgery is also supported by growing awareness among clinicians of when surgical intervention is necessary, positioning this segment for rapid expansion.

- By Diagnosis

On the basis of diagnosis, the intestinal pseudo obstruction treatment market is segmented into physical exam, biopsy, blood test, gastric emptying tests, imaging tests, manometry, and others. The imaging tests segment dominated the market in 2024, as techniques such as X-ray, CT scans, and ultrasound remain the gold standard for differentiating intestinal pseudo obstruction from mechanical obstructions. Imaging provides quick, non-invasive, and highly accurate results, making it the first line of investigation in both acute and chronic cases. Hospitals worldwide rely on imaging due to its availability and speed in emergency settings. The increasing sophistication of imaging technologies, such as high-resolution CT and MRI, is further strengthening their role. Growing adoption in both developed and developing countries ensures widespread utilization. In addition, imaging helps in monitoring disease progression, which is critical for long-term management of chronic pseudo obstruction.

The manometry segment is expected to witness the fastest growth from 2025 to 2032, due to its unique ability to directly measure intestinal motility and identify dysfunction patterns. High-resolution manometry is emerging as a highly reliable tool in specialized gastroenterology centers for diagnosing CIPO. As awareness grows among clinicians about the importance of early and accurate diagnosis, the demand for manometry is rising significantly. Technological improvements are making these devices more precise and user-friendly, encouraging adoption. Although currently limited to advanced healthcare systems, ongoing investments are expanding access to manometry worldwide. Furthermore, its use in research and clinical trials for new therapies is increasing, boosting market growth. Manometry’s ability to provide tailored diagnostic insights supports its rapid adoption as a specialized but essential diagnostic tool.

- By Symptoms

On the basis of symptoms, the intestinal pseudo obstruction treatment market is segmented into abdominal pain, bloating, diarrhea, vomiting, nausea, constipation, and others. The abdominal pain segment dominated the market in 2024, as it is the most commonly reported symptom and a primary reason for patients to seek medical attention. Abdominal pain in pseudo obstruction can be severe and recurrent, driving demand for medications, diagnostics, and hospital admissions. This symptom significantly impacts patients’ quality of life, making effective management a priority for clinicians. Hospitals and clinics frequently initiate treatment protocols focused on pain relief, highlighting its central role. Rising patient awareness and willingness to pursue treatment for pain relief are boosting this segment further. In addition, the development of new pharmacological agents targeting pain in gastrointestinal disorders strengthens this segment’s leadership.

The bloating segment is projected to grow at the fastest rate from 2025 to 2032, driven by the rising recognition of bloating as a major chronic symptom of intestinal pseudo obstruction. Unsuch as pain, bloating often persists despite traditional therapies, leading to increased demand for targeted treatments. Dietary modifications, medications, and decompression techniques are increasingly being applied to manage bloating effectively. Growing patient complaints about bloating in chronic cases are leading clinicians to prioritize its treatment in comprehensive care plans. In addition, clinical research is focusing more on bloating as a key measure of treatment efficacy. This shift towards addressing bloating as a critical quality-of-life issue is fueling the rapid growth of this segment across global markets.

- By Dosage

On the basis of dosage, the intestinal pseudo obstruction treatment market is segmented into tablet, injection, and others. The tablet segment dominated the market in 2024, due to its convenience, cost-effectiveness, and high patient compliance, especially for chronic management. Tablets are widely used for long-term administration of prokinetics, antibiotics, and antiemetic drugs. They are easily distributed across hospitals, retail pharmacies, and online platforms, making them highly accessible. Physicians often prefer tablets for stable dosing and outpatient care management. The dominance of tablets is further supported by the rising prevalence of chronic pseudo obstruction, which requires ongoing therapy. In addition, tablets provide flexibility in combination therapy with diet and supportive care, reinforcing their leadership in the market.

The injection segment is projected to witness the fastest growth from 2025 to 2032, as injectable formulations are essential for acute management and hospital-based interventions. Intravenous or intramuscular drugs act rapidly in severe cases with vomiting, dehydration, or malabsorption, ensuring timely symptom control. Growing hospital infrastructure and adoption of injectable prokinetics and antibiotics in emergency care are driving segment growth. Injections are also preferred when oral intake is not feasible due to severe obstruction or intolerance. Clinical research supporting new injectable therapies enhances their adoption rate. Furthermore, rising awareness among healthcare providers about the advantages of rapid-action injections is boosting this segment globally.

- By Route of Administration

On the basis of route of administration, the intestinal pseudo obstruction treatment market is segmented into oral, intravenous, and others. The oral route dominated the market in 2024, as it is convenient, cost-effective, and suitable for long-term outpatient therapy. Oral administration allows patients to manage chronic intestinal pseudo obstruction at home with tablets or capsules. The route is widely supported by hospitals, clinics, and retail pharmacies, making it highly accessible. Oral drugs are effective for symptom management, including bloating, nausea, and abdominal pain. Rising patient preference for non-invasive administration further strengthens dominance. In addition, the oral route facilitates combination therapy with dietary and lifestyle modifications, reinforcing its position as the leading route.

The intravenous segment is expected to grow at the fastest rate from 2025 to 2032, due to its critical role in acute hospital care where rapid therapeutic effect is required. IV administration ensures immediate delivery of medications for severe obstruction, dehydration, or infection management. Hospitals are increasingly adopting intravenous therapy for patients unable to tolerate oral intake. Growing availability of IV formulations and enhanced clinical guidelines are supporting adoption. The route is also preferred for newly developed prokinetic agents requiring precise dosing. Rising hospital investments in specialized gastroenterology units are expected to further accelerate growth in this segment.

- By End-Users

On the basis of end-users, the intestinal pseudo obstruction treatment market is segmented into clinics, hospitals, and others. The hospital segment dominated the market in 2024, as intestinal pseudo obstruction often requires advanced diagnostics, surgical interventions, and inpatient care. Hospitals provide the necessary infrastructure for imaging, manometry, and surgical management, making them the primary treatment setting. The prevalence of both acute and chronic cases in hospital settings drives consistent revenue. Specialized gastroenterology centers in hospitals enhance adoption of advanced therapies. Hospitals also serve as key points for medication dispensing and nutritional support. The dominance is reinforced by the need for continuous monitoring and multidisciplinary care in complex cases.

The clinic segment is projected to witness the fastest growth from 2025 to 2032, fueled by the rising adoption of outpatient management and follow-up care for chronic pseudo obstruction. Clinics are increasingly offering diagnostic services, dietary counseling, and medication management, reducing hospital dependency. Telemedicine integration in clinics enhances accessibility for patients in remote areas. Growing awareness among patients for early intervention encourages clinic visits. Expansion of specialized gastroenterology outpatient services is accelerating this trend. In addition, clinics provide convenient care for routine monitoring, driving rapid growth of this segment.

- By Distribution Channel

On the basis of distribution channel, the intestinal pseudo obstruction treatment market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market in 2024, as most acute and complex cases are treated within hospital settings requiring immediate access to medications. Hospital pharmacies provide controlled dispensing of injectable and specialized drugs, ensuring patient safety. They also support adherence to clinical protocols for severe or chronic cases. The segment benefits from the rising number of hospitalizations and increased use of advanced therapies. Hospitals remain a central distribution point for multidisciplinary care, strengthening their dominance. In addition, hospital pharmacies often collaborate with suppliers to ensure timely availability of essential medications for rare gastrointestinal disorders.

The online pharmacy segment is expected to grow at the fastest rate from 2025 to 2032, driven by the increasing penetration of e-commerce and rising patient preference for home delivery. Online pharmacies improve accessibility, particularly for chronic patients who require long-term medication supply. They also offer cost-effective alternatives to traditional pharmacy channels. Integration with telemedicine platforms enhances prescription fulfillment and patient convenience. Growing digital literacy and internet penetration in emerging economies are supporting rapid adoption. Furthermore, regulatory approvals for online drug sales in various countries are enabling market expansion for this channel.

Intestinal Pseudo Obstruction Treatment Market Regional Analysis

- North America dominated the intestinal pseudo obstruction treatment market with the largest revenue share of 40.3% in 2024, supported by robust healthcare infrastructure, specialized gastroenterology centers, early diagnosis rates, and active R&D initiatives by leading pharmaceutical and medical device companies

- Patients and healthcare providers in the region highly value access to accurate diagnostics, comprehensive treatment options including medications and surgical interventions, and continuous monitoring for both acute and chronic cases

- This widespread adoption is further supported by high healthcare expenditure, strong R&D presence of pharmaceutical companies, and early adoption of innovative therapies, establishing North America as the leading region for managing intestinal pseudo obstruction effectively

U.S. Intestinal Pseudo Obstruction Treatment Market Insight

The U.S. intestinal pseudo obstruction treatment market captured the largest revenue share of 82% in 2024 within North America, fueled by advanced healthcare infrastructure and high awareness of gastrointestinal motility disorders. Patients and clinicians increasingly prioritize early diagnosis, comprehensive symptom management, and access to multidisciplinary treatment approaches. The growing adoption of innovative therapies, including prokinetic medications and minimally invasive surgical interventions, further propels market growth. Moreover, the availability of specialized gastroenterology centers and well-established hospital networks ensures timely and effective management of both acute and chronic cases. The U.S. market also benefits from active R&D investments and clinical trials focused on rare gastrointestinal disorders.

Europe Intestinal Pseudo Obstruction Treatment Market Insight

The Europe intestinal pseudo obstruction treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of rare gastrointestinal motility disorders and the need for effective management of chronic intestinal pseudo obstruction. Rising healthcare expenditure, urbanization, and access to advanced diagnostics such as imaging and manometry are fostering market adoption. European patients are also drawn to comprehensive treatment plans combining medication, dietary interventions, and decompression therapies. The region is witnessing growth across both hospital and clinic settings, with treatments being incorporated into new healthcare protocols and specialty centers.

U.K. Intestinal Pseudo Obstruction Treatment Market Insight

The U.K. intestinal pseudo obstruction treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising incidence and diagnosis of chronic intestinal pseudo obstruction and increased patient awareness. In addition, concerns regarding severe gastrointestinal complications are encouraging both patients and healthcare providers to adopt early intervention and specialized treatment approaches. The U.K.’s strong healthcare infrastructure, widespread availability of advanced diagnostics, and efficient pharmacy networks are expected to continue stimulating market growth. Growing focus on rare disease management and increasing clinical research activities further reinforce expansion.

Germany Intestinal Pseudo Obstruction Treatment Market Insight

The Germany intestinal pseudo obstruction treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of gastrointestinal motility disorders and the growing demand for advanced therapies. Germany’s well-developed healthcare infrastructure, emphasis on clinical innovation, and high-quality specialty care centers promote the adoption of medication, surgical, and dietary interventions. Integration of comprehensive management programs with hospital and outpatient services is becoming increasingly prevalent, ensuring effective treatment. Moreover, patient preference for early intervention and evidence-based care aligns with local medical practices, supporting sustained growth.

Asia-Pacific Intestinal Pseudo Obstruction Treatment Market Insight

The Asia-Pacific intestinal pseudo obstruction treatment market is poised to grow at the fastest CAGR from 2025 to 2032, driven by rising diagnosis rates, improving healthcare access, and increasing investments in specialized gastroenterology care in countries such as China, Japan, and India. Growing awareness of rare gastrointestinal disorders and government initiatives promoting digital health solutions are accelerating treatment adoption. Furthermore, the expansion of hospital infrastructure and availability of both medications and minimally invasive therapies are increasing accessibility. Economic growth, urbanization, and rising disposable incomes are enabling patients to seek advanced treatment options across the region.

Japan Intestinal Pseudo Obstruction Treatment Market Insight

The Japan intestinal pseudo obstruction treatment market is gaining momentum due to the country’s advanced healthcare system, high awareness of gastrointestinal motility disorders, and demand for convenience in patient care. Japanese patients increasingly prefer integrated management approaches combining medications, diet, and monitoring technologies. Hospitals and specialty centers are actively adopting advanced diagnostic tools such as manometry and imaging tests to improve patient outcomes. Moreover, Japan’s aging population is such asly to spur demand for effective, easy-to-administer treatment options for chronic intestinal pseudo obstruction in both residential and clinical settings.

India Intestinal Pseudo Obstruction Treatment Market Insight

The India intestinal pseudo obstruction treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to improving healthcare infrastructure, growing awareness of gastrointestinal disorders, and rising patient demand for specialized care. India represents one of the fastest-growing markets for intestinal pseudo obstruction treatments, with both medications and supportive therapies being increasingly adopted in hospitals and clinics. The push towards digital health solutions, telemedicine, and expanded access to specialty gastroenterology care are key factors propelling market growth. Availability of affordable treatment options and expansion of hospital networks further support adoption in residential and commercial healthcare settings.

Intestinal Pseudo Obstruction Treatment Market Share

The intestinal pseudo obstruction treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- Cipla Ltd. (India)

- GSK plc (U.K.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Lilly USA, LLC. (U.S.)

- AstraZeneca (U.K.)

- Johnson & Johnson and its affiliates (U.S.)

- Sanofi (France)

- Bayer AG (Germany)

- Sun Pharmaceutical Industries Ltd. (India)

- Melinta Therapeutics LLC (U.S.)

- Basilea Pharmaceutica Ltd. (Switzerland)

- Tetraphase Pharmaceuticals (U.S.)

- Paratek Pharmaceuticals, Inc. (U.S.)

- AbbVie (U.S.)

What are the Recent Developments in Global Intestinal Pseudo Obstruction Treatment Market?

- In October 2025, the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK) outlined comprehensive treatment strategies for chronic intestinal pseudo-obstruction. These strategies include nutritional support to prevent malnutrition, medications to manage symptoms, decompression techniques to relieve bowel distention, and, in some cases, surgical interventions to address underlying causes

- In September 2025, Penn Medicine reported that neostigmine is being utilized to treat large bowel pseudo-obstruction, also known as Ogilvie syndrome. The medication has been found effective in stimulating colonic motility, offering a non-invasive treatment option for patients with this condition

- In July 2025, OPKO Health and Entera Bio announced a collaboration to develop an oral GLP-2 analog tablet for the treatment of Short Bowel Syndrome, a condition related to intestinal motility disorders. Their research focuses on creating a first-in-class oral medication that could offer a more convenient alternative to current injectable therapies, potentially improving patient adherence and quality of life

- In July 2025, a study published in Neurology highlighted the need for optimized immunosuppressive treatments for autoimmune-related chronic intestinal pseudo-obstruction (CIPO). The research emphasized that while corticosteroids and immunosuppressive agents are commonly used, their efficacy varies, and more targeted therapies are necessary. The study called for clinical trials to establish standardized treatment protocols for this subgroup of CIPO patients

- In February 2025, researchers introduced a self-contact electromechanical framework to study intestinal motility. This model integrates microstructural material properties with electrophysiological data to simulate peristaltic movements. The approach aims to enhance the understanding of intestinal dynamics and could inform future treatment strategies for motility disorders

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.