Global Intravenous Iron Market

Market Size in USD Billion

USD

3.38 Billion

USD

6.73 Billion

2025

2033

USD

3.38 Billion

USD

6.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.38 Billion | |

| USD 6.73 Billion | |

| % | |

|

What is the Intravenous Iron Market Size and Growth Rate?

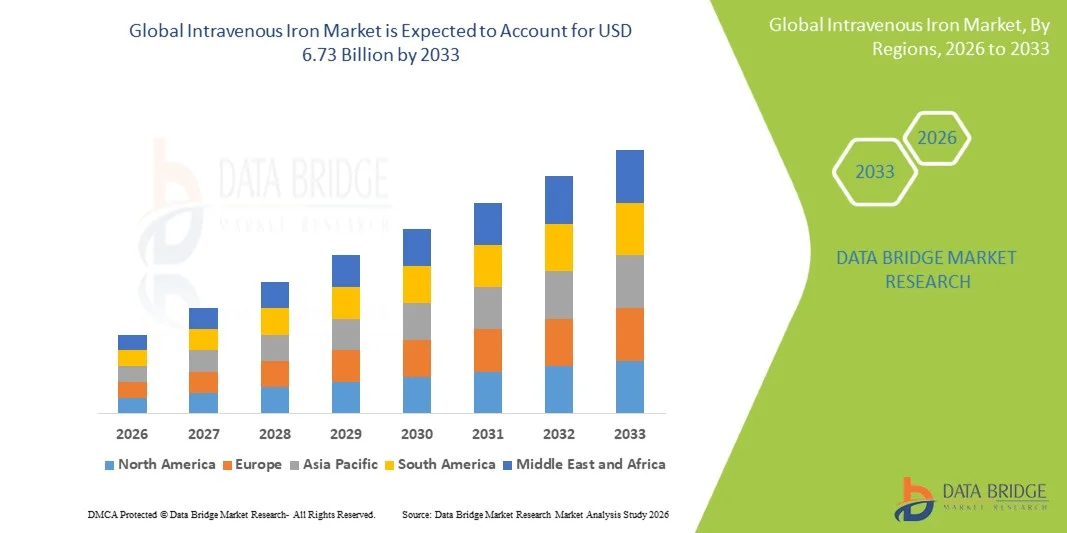

- As per Data Bridge Market Research Analysis the global Intravenous Iron Market size was valued at USD 3.38 billion in 2025 and is expected to reach USD 6.73 billion by 2033, at a CAGR of 9.00% during the forecast period

- The market growth is primarily driven by the increasing prevalence of iron deficiency anemia (IDA), chronic kidney disease (CKD), and inflammatory bowel disease (IBD), along with rising hospital-based demand for rapid iron replenishment therapies

- Furthermore, advancements in safer and more stable IV iron formulations, coupled with growing adoption of outpatient infusion services and improved reimbursement frameworks in developed healthcare systems, are establishing IV iron therapy as a preferred treatment option, thereby significantly boosting industry growth

Market Size & Forecast

- Global Market Value (2025):USD 3.38 billion

- Expected Market Value (2033):USD 6.73 billion

- Forecast CAGR (2026–2033): 9.00

Intravenous Iron Market Analysis

- Intravenous iron therapy, delivering iron directly into the bloodstream for rapid correction of iron deficiency anemia (IDA), has become a critical treatment option in hospitals and specialty care settings due to its high efficacy, faster iron replenishment compared to oral supplements, and suitability for patients with chronic kidney disease (CKD), inflammatory bowel disease (IBD), and oncology-related anemia

- The growing demand for intravenous iron is primarily driven by the increasing global prevalence of iron deficiency anemia, rising burden of chronic diseases, expanding dialysis population, and higher clinical preference for IV formulations in patients who do not respond adequately to oral iron therapy

- North America dominated the intravenous iron market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, strong anemia screening practices, high adoption of novel IV iron formulations, and extensive use in nephrology and hospital infusion centers, particularly in the U.S.

- Asia-Pacific is expected to be the fastest growing region in the intravenous iron market during the forecast period due to rising prevalence of anemia, increasing healthcare expenditure, improving diagnostic rates, expanding hospital infrastructure, and growing awareness of advanced iron therapies in emerging economies such as India and China

- Ferric carboxymaltose segment dominated the intravenous iron market with a significant market share of 42.8% in 2025, driven by its ability to deliver high-dose iron in fewer infusions, improved safety profile compared to older formulations, and widespread clinical adoption across hospital and outpatient care settings

Report Scope and Intravenous Iron Market Segmentation

|

Attributes |

Intravenous Iron Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

|

What is the Key Trend in the Intravenous Iron Market?

“Shift Toward Advanced Formulations and High-Dose Infusion Therapies”

- A significant and accelerating trend in the global intravenous iron market is the increasing adoption of next-generation IV iron formulations and high-dose single-infusion therapies, improving treatment efficiency and patient compliance in both hospital and outpatient settings

- For instance, ferric carboxymaltose is widely used across hospitals and infusion centers due to its ability to deliver larger iron doses in fewer visits, reducing overall treatment burden for patients with iron deficiency anemia (IDA)

- Advances in IV iron therapies are enabling improved safety profiles, reduced risk of hypersensitivity reactions, and better tolerability, with newer formulations designed to minimize free iron release and oxidative stress during administration

- Furthermore, the expansion of outpatient infusion centers and day-care treatment facilities is supporting faster adoption of IV iron therapies outside traditional hospital environments, improving accessibility for chronic anemia patients

- The growing use of IV iron in oncology and cardiology supportive care is expanding its clinical application beyond nephrology, as anemia management becomes a critical component of broader chronic disease treatment pathways

- Increasing clinical preference for combination therapy approaches, where IV iron is used alongside erythropoiesis-stimulating agents (ESAs), is further enhancing treatment effectiveness in complex anemia cases

Intravenous Iron Market Dynamics

Driver

“Rising Prevalence of Iron Deficiency Anemia and Chronic Disease Burden”

- The increasing global prevalence of iron deficiency anemia (IDA), chronic kidney disease (CKD), and inflammatory bowel disease (IBD) is a major driver fueling demand for intravenous iron therapies across healthcare systems

- For instance, in April 2025, healthcare providers in several regions expanded anemia management programs to improve early diagnosis and treatment of iron deficiency in high-risk populations such as dialysis and cancer patients

- As the burden of chronic diseases continues to rise, intravenous iron is increasingly preferred over oral iron due to its faster action, higher efficacy, and better outcomes in patients with absorption impairments

- Furthermore, growing awareness among physicians regarding the limitations of oral iron therapy, especially in moderate to severe anemia cases, is driving higher adoption of IV iron formulations in hospital settings

- Expanding geriatric population worldwide is significantly contributing to higher anemia incidence, further increasing the clinical need for intravenous iron interventions

- Rising investment in hospital infrastructure and infusion care services is also improving patient access to IV iron therapy, supporting sustained market growth globally

Restraint/Challenge

“Safety Concerns and High Treatment Costs Limiting Widespread Adoption”

- Concerns related to potential adverse effects such as hypersensitivity reactions, iron overload, and infusion-related complications pose a significant challenge to broader adoption of intravenous iron therapies

- For instance, reported safety warnings associated with older IV iron formulations have led to cautious prescribing practices among clinicians in certain healthcare settings

- Addressing these safety concerns through improved formulation stability, controlled dosing protocols, and enhanced patient monitoring is essential to strengthen physician and patient confidence

- Furthermore, the relatively high cost of intravenous iron treatments compared to oral iron supplements remains a barrier in cost-sensitive healthcare systems, particularly in developing regions

- Limited availability of infusion facilities in rural and underserved areas restricts timely access to IV iron therapy, especially in emerging economies

- Overcoming these challenges through cost optimization, wider insurance coverage, expansion of infusion infrastructure, and continued development of safer IV iron options will be crucial for sustained market expansion

Intravenous Iron Market Scope

The market is segmented on the basis of application, product, end-users, and distribution channel.

- By Application

On the basis of application, the intravenous iron market is segmented into gastroenterology, gynaecology, nephrology, oncology, cardiology, hematology, surgeries, and others. The nephrology segment dominated the market with the largest revenue share of 34.8% in 2025, driven by the high prevalence of chronic kidney disease (CKD) and the widespread use of dialysis, where intravenous iron is routinely administered to manage iron deficiency anemia. Patients undergoing hemodialysis require frequent iron supplementation due to blood loss and impaired erythropoiesis, making IV iron a standard component of renal care protocols. Strong clinical guidelines recommending IV iron therapy in CKD patients further support its dominance. In addition, established hospital infrastructure and reimbursement coverage for renal treatments contribute to consistent demand in this segment. The oncology and gastroenterology segments also significantly contribute due to anemia associated with cancer therapies and malabsorption disorders.

The oncology segment is expected to witness the fastest growth rate of 20.6% from 2026 to 2033, fueled by rising global cancer incidence and increasing use of chemotherapy and radiotherapy, which often lead to treatment-induced anemia. Intravenous iron is increasingly used as supportive care in cancer patients to improve hemoglobin levels and reduce fatigue without relying solely on blood transfusions. For instance, cancer care centers are increasingly integrating IV iron into anemia management protocols to improve patient outcomes and treatment tolerance. Growing awareness among oncologists regarding iron deficiency correction in cancer-related anemia is further accelerating adoption. Expanding oncology treatment infrastructure in emerging markets and rising demand for supportive care therapies are key growth drivers.

- By Product

On the basis of product, the intravenous iron market is segmented into iron dextran, ferric gluconate, iron sucrose, ferric carboxymaltose, and others. The ferric carboxymaltose segment dominated the market with the largest revenue share of 42.8% in 2025, driven by its ability to deliver high-dose iron in a single or limited number of infusions, significantly improving patient convenience and compliance. It has a strong safety profile with lower risk of hypersensitivity reactions compared to older formulations, making it widely preferred in hospitals and outpatient infusion centers. Its broad clinical applicability across nephrology, oncology, and gastroenterology further strengthens its dominance. In addition, strong adoption in developed healthcare systems and inclusion in treatment guidelines support its leading position. Healthcare providers also prefer it due to reduced treatment time and lower overall hospitalization burden.

The iron sucrose segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its long-standing clinical acceptance, cost-effectiveness, and widespread use in dialysis centers. It is particularly favored in developing regions where affordability and availability are key decision factors. For instance, iron sucrose remains a standard IV iron option in many public healthcare systems due to its established safety record and predictable dosing profile. Its frequent use in CKD-related anemia management supports consistent demand growth. Increasing dialysis patient population and expansion of nephrology services in emerging economies are further boosting its adoption.

- By End-Users

On the basis of end-users, the intravenous iron market is segmented into hospitals, homecare, specialty centres, and others. The hospitals segment dominated the market with the largest revenue share of 58.3% in 2025, driven by the high volume of inpatient treatments, presence of advanced infusion infrastructure, and availability of trained healthcare professionals. Hospitals remain the primary setting for IV iron administration due to the need for monitoring during infusion, especially in high-risk patients. Strong patient inflow for CKD, oncology, and surgical anemia management further strengthens hospital dominance. In addition, favorable reimbursement structures and established treatment protocols contribute to high utilization. Integration of IV iron therapy into routine hospital-based anemia management programs ensures sustained demand.

The specialty centres segment is expected to witness the fastest growth rate of 19.4% from 2026 to 2033, driven by the rising shift toward outpatient care and dedicated infusion clinics. These centres offer faster service, reduced waiting times, and more patient-centric treatment environments compared to traditional hospitals. For instance, standalone infusion clinics are increasingly being used for chronic anemia management, improving accessibility and convenience for patients. The growing burden of long-term conditions such as CKD and IBD is driving repeat visits to specialty centres. Expansion of private healthcare infrastructure and increasing investment in ambulatory care services are further accelerating growth.

- By Distribution Channel

On the basis of distribution channel, the intravenous iron market is segmented into hospital pharmacy, online pharmacy, retail pharmacy, and others. The hospital pharmacy segment dominated the market with the largest revenue share of 64.1% in 2025, driven by the direct administration of IV iron within hospital settings and strong procurement systems integrated with inpatient treatment workflows. Hospital pharmacies ensure controlled supply, proper storage, and immediate availability of intravenous formulations required for emergency and scheduled infusions. The dominance is further supported by centralized purchasing policies and bulk procurement for large patient volumes. In addition, strict regulatory handling requirements for IV iron formulations reinforce hospital pharmacy control. High dependence on institutional treatment pathways ensures continued dominance of this segment.

The online pharmacy segment is expected to witness the fastest CAGR of 18.7% from 2026 to 2033, driven by the digitalization of healthcare procurement systems and increasing adoption of e-health platforms. Although IV iron is primarily administered in clinical settings, online platforms are increasingly used for procurement by healthcare providers and specialty clinics. For instance, hospitals and infusion centres are leveraging digital supply chains to streamline ordering and reduce procurement delays. Rising penetration of healthcare e-commerce platforms in emerging markets is further supporting growth. The shift toward efficient, technology-enabled medical supply distribution is expected to accelerate adoption in this segment.

Intravenous Iron Market Regional Analysis

- North America dominated the intravenous iron market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, strong anemia screening practices, high adoption of novel IV iron formulations, and extensive use in nephrology and hospital infusion centers, particularly in the U.S.

- Healthcare providers in the region highly value the clinical efficacy, rapid hemoglobin improvement, and improved safety profiles offered by modern IV iron formulations, particularly in dialysis, oncology, and gastroenterology patients requiring fast iron replenishment

- This widespread adoption is further supported by advanced healthcare infrastructure, high healthcare expenditure, strong reimbursement coverage, and early uptake of next-generation IV iron products, establishing intravenous iron as a standard treatment option in both inpatient and outpatient care environments

U.S. Intravenous Iron Market Insight

The U.S. intravenous iron market captured the largest revenue share of 81% in North America in 2025, driven by the high burden of chronic kidney disease, iron deficiency anemia, and strong utilization of hospital-based infusion therapies. The country benefits from advanced healthcare infrastructure and rapid adoption of innovative IV iron formulations in nephrology, oncology, and gastroenterology care. Patients and providers increasingly prefer intravenous iron due to its faster hemoglobin correction and better efficacy compared to oral supplements. Strong reimbursement policies and insurance coverage further support widespread adoption across hospitals and specialty clinics. In addition, increasing use of outpatient infusion centers is improving accessibility and treatment convenience.

Europe Intravenous Iron Market Insight

The Europe intravenous iron market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by increasing awareness of iron deficiency management and strong adherence to clinical treatment guidelines for anemia in CKD and IBD patients. The rising burden of chronic diseases, along with a well-established public healthcare system, is fostering consistent demand for IV iron therapies. European healthcare providers increasingly prefer intravenous formulations due to their effectiveness in patients with poor oral iron absorption. In addition, supportive reimbursement frameworks and structured hospital protocols are encouraging broader adoption. Growth is also supported by increasing use in outpatient infusion centers and hospital day-care settings across major European countries.

U.K. Intravenous Iron Market Insight

The U.K. intravenous iron market is anticipated to grow at a notable CAGR during the forecast period, driven by rising cases of iron deficiency anemia and increasing hospital admissions related to chronic kidney disease and cancer-related anemia. The National Health Service (NHS) plays a key role in supporting standardized IV iron therapy protocols across hospitals and specialist clinics. Growing clinical preference for fast-acting anemia correction therapies is further boosting demand. In addition, increased awareness among physicians regarding the limitations of oral iron therapy is accelerating IV iron adoption. Expansion of outpatient infusion services is also contributing to market growth in the country.

Germany Intravenous Iron Market Insight

The Germany intravenous iron market is expected to expand at a considerable CAGR during the forecast period, fueled by a strong focus on advanced medical treatments and high-quality healthcare infrastructure. Germany’s large CKD and elderly patient population significantly contributes to sustained demand for IV iron therapies. Hospitals and specialty clinics widely adopt intravenous formulations due to their high efficacy and improved safety profiles. Furthermore, strong emphasis on evidence-based treatment practices supports the integration of IV iron into standard care pathways. Increasing investments in hospital modernization and outpatient infusion services are also enhancing market penetration.

Asia-Pacific Intravenous Iron Market Insight

The Asia-Pacific intravenous iron market is poised to grow at the fastest CAGR of 21.3% during the forecast period of 2026 to 2033, driven by the rising prevalence of iron deficiency anemia, increasing healthcare expenditure, and expanding access to advanced treatment options in countries such as China, India, and Japan. The region’s large population base and growing burden of chronic diseases are significantly boosting demand for IV iron therapies. Government initiatives aimed at improving healthcare infrastructure and anemia control programs are further supporting market expansion. In addition, increasing awareness among healthcare professionals and patients regarding the benefits of intravenous iron over oral supplementation is accelerating adoption. The growing availability of affordable IV iron formulations is also widening market access across emerging economies.

Japan Intravenous Iron Market Insight

The Japan intravenous iron market is gaining momentum due to its aging population, high prevalence of chronic kidney disease, and advanced healthcare system emphasizing efficient anemia management. Hospitals widely utilize IV iron therapies for elderly patients who require rapid and effective iron correction. The country’s strong focus on technological advancement in healthcare supports the adoption of safer and more efficient intravenous formulations. Integration of IV iron therapy into dialysis and oncology care protocols further strengthens demand. In addition, Japan’s well-organized hospital infrastructure and high treatment standards ensure consistent utilization across specialty care settings.

India Intravenous Iron Market Insight

The India intravenous iron market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the high burden of iron deficiency anemia, large patient population, and increasing awareness of advanced anemia treatments. Rapid urbanization and improving access to healthcare services are driving greater adoption of IV iron therapies in both public and private hospitals. Government-led anemia control initiatives and maternal health programs are also supporting demand. In addition, the growing availability of cost-effective IV iron formulations is making treatment more accessible. Expansion of hospital infrastructure and rising investments in specialty care centers are further propelling market growth in the country.

Which are the Top Companies in Intravenous Iron Market?

The Intravenous Iron industry is primarily led by well-established companies, including:

- Vifor Pharma Ltd. (Switzerland)

- Pharmacosmos A/S (Denmark)

- Fresenius Kabi AG (Germany)

- Sanofi (France)

- CSL Vifor (Switzerland)

- American Regent, Inc. (U.S.)

- AMAG Pharmaceuticals, Inc. (U.S.)

- Daiichi Sankyo Company, Limited (Japan)

- AbbVie Inc. (U.S.)

- Shield Therapeutics plc (U.K.)

- Rockwell Medical, Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Hikma Pharmaceuticals PLC (U.K.)

- Zydus Lifesciences Limited (India)

- Aurobindo Pharma Limited (India)

- B. Braun SE (Germany)

What are the Recent Developments in Global Intravenous Iron Market?

- In August 2025, Amphastar Pharmaceuticals received FDA approval for Iron Sucrose Injection (USP), a generic IV iron therapy for treating iron deficiency anemia in chronic kidney disease patients. The approval strengthens access to affordable IV iron options in the U.S. market and expands competition in the iron sucrose segment. This launch is expected to improve treatment accessibility in dialysis and hospital settings

- In August 2025, Viatris announced FDA approval for the first generic Iron Sucrose Injection in the U.S., marking a major milestone in expanding low-cost intravenous iron therapies. The product is a generic version of Venofer and is indicated for iron deficiency anemia in CKD patients. This development is expected to significantly increase market penetration of IV iron in public healthcare systems

- In October 2024, CSL Vifor received European Medicines Agency (EMA) approval for expanded use of Ferinject (ferric carboxymaltose), extending its indication to include treatment of iron deficiency in symptomatic chronic heart failure patients with reduced ejection fraction. This expansion significantly increases the eligible patient population across Europe and strengthens IV iron adoption in cardiology care pathways. The approval reinforces Ferinject’s position as a leading IV iron therapy in hospital settings

- In March 2024, Pharmacosmos announced positive clinical results from the FERWALK trial evaluating ferric derisomaltose in heart failure patients with iron deficiency, showing significant improvement in exercise capacity and quality-of-life scores. The study supports broader use of high-dose IV iron therapy beyond traditional anemia indications. This development strengthens the clinical evidence base for single-infusion iron therapies in cardiology applications

- In June 2023, Injectafer (ferric carboxymaltose) received U.S. FDA approval for use in patients with heart failure and iron deficiency, expanding its therapeutic application beyond traditional anemia indications. This label extension supports broader clinical use in cardiology care, especially for improving exercise capacity in affected patients. It further strengthens ferric carboxymaltose as a key IV iron therapy in advanced treatment settings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.