Global Intravesical Bladder Cancer Therapeutics Market

Market Size in USD Million

USD

322.23 Million

USD

448.85 Million

2024

2032

USD

322.23 Million

USD

448.85 Million

2024

2032

| 2025 - 2032 | |

| USD 322.23 Million | |

| USD 448.85 Million | |

| % | |

|

Intravesical Bladder Cancer Therapeutics Market Size

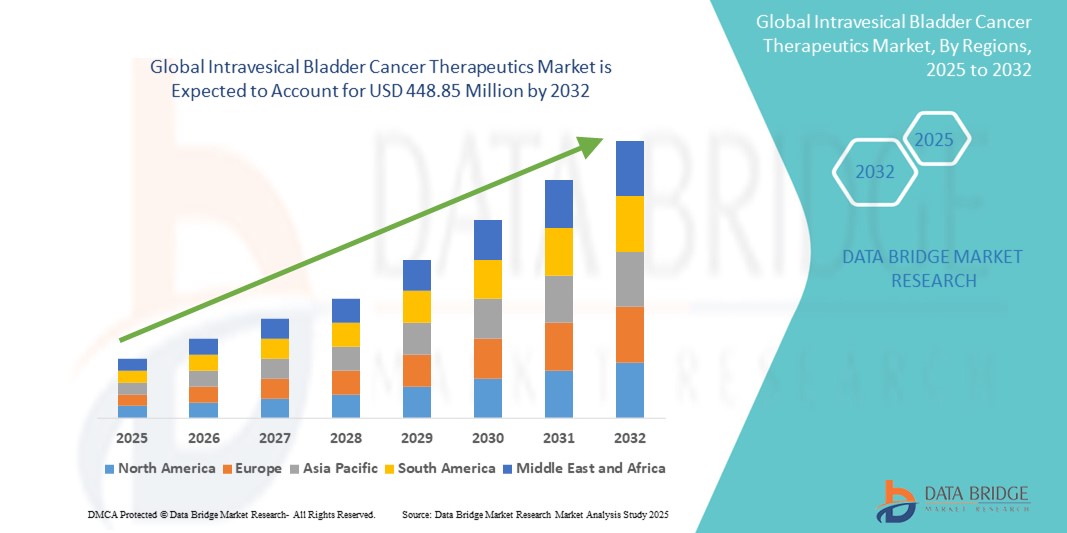

- The global intravesical bladder cancer therapeutics market size was valued at USD 322.23 million in 2024 and is expected to reach USD 448.85 million by 2032, at a CAGR of 4.23% during the forecast period

- The market growth is largely driven by increasing prevalence of bladder cancer particularly non-muscle invasive bladder cancer and the rising adoption of intravesical therapies such as BCG, chemotherapy, and novel gene-based treatments across developed and emerging regions

- Furthermore, advancements in targeted intravesical drug delivery systems, along with growing regulatory approvals of innovative immunotherapies and biologics, are expanding treatment options and improving patient outcomes. These converging trends are accelerating the demand for intravesical bladder cancer therapeutics, thereby significantly boosting the industry’s growth

Intravesical Bladder Cancer Therapeutics Market Analysis

- Intravesical bladder cancer therapeutics, involving the direct delivery of anti-cancer agents into the bladder, play a critical role in treating non-muscle invasive bladder cancer (NMIBC) due to their targeted action, minimal systemic toxicity, and ability to reduce tumor recurrence and progression

- The rising demand for intravesical therapies is primarily driven by the growing prevalence of bladder cancer globally, increased awareness of early-stage diagnosis, and continued clinical reliance on chemotherapy and immunotherapy, alongside the emergence of advanced treatment modalities such as gene therapy

- North America dominated the intravesical bladder cancer therapeutics market with the largest revenue share of 44.8% in 2024, supported by strong diagnostic infrastructure, favorable reimbursement policies, and widespread availability of intravesical agents, with the U.S. leading in the adoption of both traditional chemotherapy regimens and newer gene-based therapies

- Asia-Pacific is expected to be the fastest growing region in the intravesical bladder cancer therapeutics market during the forecast period due to rising healthcare investments, expanding cancer screening programs, and increasing access to urologic care across rapidly urbanizing nations

- The chemotherapy segment dominated the intravesical bladder cancer therapeutics market with a market share of 50.3% in 2024, driven by its cost-effectiveness, clinical efficacy in early-stage disease, and continued use of agents such as mitomycin C and gemcitabine as standard-of-care treatments

Report Scope and Intravesical Bladder Cancer Therapeutics Market Segmentation

|

Attributes |

Intravesical Bladder Cancer Therapeutics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Intravesical Bladder Cancer Therapeutics Market Trends

“Shift Toward Advanced Intravesical Immuno- and Gene Therapies”

- A significant and accelerating trend in the global intravesical bladder cancer therapeutics market is the transition toward advanced therapies such as gene therapy and biologic immunotherapies, aimed at treating BCG-unresponsive non-muscle invasive bladder cancer (NMIBC). This evolution is reshaping treatment protocols and expanding options beyond conventional chemotherapy and BCG

- For instance, Adstiladrin (nadofaragene firadenovec), a gene therapy approved in the U.S., delivers the IFN-α2b gene directly into the bladder lining, triggering a localized immune response. Similarly, Anktiva (nogapendekin alfa inbakicept), approved in 2024, works synergistically with BCG to stimulate IL-15-based immune activation

- These next-generation intravesical agents are designed to enhance treatment efficacy, minimize systemic exposure, and offer options for high-risk patients with limited response to traditional therapies. In addition, advancements in targeted delivery systems such as hydrogel formulations and sustained-release carriers enable prolonged drug exposure within the bladder, improving therapeutic outcomes

- The integration of such innovations is enabling personalized and precision-based treatment strategies, wherein clinicians tailor therapies based on patient responsiveness and molecular profiling. This approach is redefining standards of care, especially in regions with access to advanced oncology infrastructure

- Pharmaceutical innovators such as Ferring Pharmaceuticals, FerGene, and ImmunityBio are focusing R&D efforts on developing and commercializing new intravesical therapies with enhanced immunomodulatory potential. Their pipelines are driving market growth through a combination of robust clinical trial results and favorable regulatory progress

- The increasing demand for more effective and personalized intravesical bladder cancer treatments is creating new opportunities across both established and emerging markets, as stakeholders prioritize efficacy, bladder preservation, and patient quality of life in treatment selection

Intravesical Bladder Cancer Therapeutics Market Dynamics

Driver

“Rising Bladder Cancer Incidence and Demand for Bladder-Sparing Therapies”

- The rising global incidence of bladder cancer, particularly non-muscle invasive bladder cancer (NMIBC), is a key driver of the intravesical therapeutics market. NMIBC accounts for approximately 70–75% of initial diagnoses, and intravesical therapy remains the standard of care for bladder preservation and recurrence prevention

- For instance, the approval and adoption of novel treatments such as Adstiladrin and Anktiva in BCG-unresponsive cases signal a major shift in therapeutic approaches. These therapies provide alternatives to radical cystectomy, thereby addressing a long-standing clinical gap

- Governments and health systems are increasingly investing in early cancer detection and screening programs, leading to more NMIBC diagnoses at stages where intravesical therapy is most effective

- Moreover, the growing patient preference for bladder-sparing treatments and the availability of multiple intravesical options ranging from traditional BCG to advanced biologics are contributing to sustained market expansion

- Healthcare providers and urologists also benefit from improved treatment guidelines and emerging data that support the efficacy of these therapies, helping accelerate adoption across both high- and middle-income countries

Restraint/Challenge

“Treatment Limitations in BCG-Intolerant or Refractory Patients and Cost Barriers”

- A key challenge in the intravesical bladder cancer therapeutics market is the limited efficacy or tolerance of existing therapies, particularly BCG, in a significant subset of patients. Many patients either fail to respond to BCG or experience adverse events that lead to discontinuation, leaving them with limited non-surgical alternatives

- While new therapies such as gene and cytokine-based treatments offer hope, they also present cost and accessibility challenges. For instance, advanced biologics and gene therapies come with high price tags and complex delivery logistics, which can limit uptake in lower-income or under-resourced healthcare systems

- Moreover, despite improvements in intravesical drug delivery, there is still a lack of long-term efficacy data for many of the emerging treatments, which may delay wider adoption by clinicians and payers

- Regulatory complexity and the need for specialized infrastructure (such as, cold-chain storage for biologics, trained personnel for intravesical instillation) further complicate market penetration in certain regions

- Overcoming these challenges will require strategic investments in healthcare infrastructure, broader access programs, continued clinical trial support, and pricing strategies that improve affordability while maintaining innovation incentives

Intravesical Bladder Cancer Therapeutics Market Scope

The market is segmented on the basis of cancer type, therapy type, and end user.

- By Cancer Type

On the basis of cancer type, the intravesical bladder cancer therapeutics market is segmented into non-muscle invasive bladder cancer (NMIBC), muscle-invasive bladder cancer (MIBC), and metastatic bladder cancer. The NMIBC segment dominated the market with the largest revenue share of 64.3% in 2024, owing to the high prevalence of early-stage bladder cancer cases and the wide adoption of intravesical therapies such as BCG and mitomycin C for localized treatment. NMIBC is commonly diagnosed at an early stage and is highly treatable through bladder-preserving therapeutic approaches, making it the primary focus of intravesical treatment regimens.

The metastatic bladder cancer segment is expected to witness the fastest growth rate of 7.8% CAGR from 2025 to 2032, driven by increasing diagnosis rates and advances in systemic and adjunctive intravesical therapies that aim to reduce progression from early-stage disease. Emerging treatment protocols now consider hybrid approaches combining intravesical and systemic therapies, which is expanding clinical attention to this patient population.

- By Therapy Type

On the basis of therapy type, the intravesical bladder cancer therapeutics market is segmented into chemotherapy, immunotherapy, gene therapy, targeted therapy, and others. The chemotherapy segment held the largest market revenue share of 50.3% in 2024, primarily due to the widespread use of agents such as mitomycin C and gemcitabine in first-line intravesical treatment. Chemotherapy is often chosen for its cost-effectiveness, established efficacy in reducing recurrence, and compatibility with existing treatment protocols in hospitals and outpatient clinics.

The gene therapy segment is projected to grow at the fastest CAGR of 10.3% from 2025 to 2032, driven by the commercial introduction and clinical adoption of gene-based treatments such as Adstiladrin, particularly for BCG-unresponsive NMIBC. Gene therapies offer targeted immune stimulation and durable responses, and their FDA approvals have spurred ongoing innovation and investments in this space.

- By End User

On the basis of end user, the intravesical bladder cancer therapeutics market is segmented into hospitals, ambulatory surgical centers (ASCs), specialty clinics, and research & academic institutes. The hospital segment dominated the market with the largest revenue share of 55.4% in 2024, attributed to the availability of specialized oncology departments, access to intravesical instillation infrastructure, and presence of skilled healthcare professionals for therapy administration and monitoring. Hospitals remain the preferred setting for initial diagnosis, high-risk case management, and administration of novel therapies such as BCG and gene therapy.

The ambulatory surgical centers segment is anticipated to witness the fastest growth rate of 8.7% CAGR from 2025 to 2032, as outpatient settings become increasingly equipped to administer intravesical treatments. ASCs offer cost-effective, convenient, and patient-friendly options, especially for maintenance therapy and lower-risk NMIBC cases. Their growing adoption reflects the broader healthcare shift toward decentralized cancer treatment models

Intravesical Bladder Cancer Therapeutics Market Regional Analysis

- North America dominated the intravesical bladder cancer therapeutics market with the largest revenue share of 44.8% in 2024, supported by strong diagnostic infrastructure, favorable reimbursement policies, and widespread availability of intravesical agents

- Patients and healthcare providers in the region place strong emphasis on bladder-sparing approaches, supported by the availability of advanced urologic care, access to intravesical delivery systems, and inclusion of cutting-edge therapies in clinical guidelines

- This leadership position is further reinforced by favorable reimbursement policies, well-established oncology networks, and ongoing clinical research and FDA approvals, making North America a key driver in the adoption and commercialization of intravesical bladder cancer therapies for both primary and recurrent NMIBC cases

U.S. Intravesical Bladder Cancer Therapeutics Market Insight

The U.S. intravesical bladder cancer therapeutics market captured the largest revenue share of 79% in 2024 within North America, driven by the high incidence of non-muscle invasive bladder cancer (NMIBC) and strong uptake of advanced therapies. Increasing availability of treatments such as Adstiladrin and Anktiva, combined with a well-developed healthcare infrastructure and favorable reimbursement policies, supports widespread use of intravesical therapies. Furthermore, the presence of leading clinical research institutions and regulatory advancements continue to foster innovation and accelerate market growth.

Europe Intravesical Bladder Cancer Therapeutics Market Insight

The Europe intravesical bladder cancer therapeutics market is projected to expand at a substantial CAGR throughout the forecast period, supported by national screening programs, aging populations, and a growing preference for bladder-sparing treatments. Rising awareness of NMIBC and increased access to intravesical immunotherapies, such as BCG and mitomycin C, are fueling adoption. Countries across Western and Central Europe are witnessing increased demand for localized, minimally invasive cancer treatment, making intravesical therapy a frontline option in early-stage cases.

U.K. Intravesical Bladder Cancer Therapeutics Market Insight

The U.K. intravesical bladder cancer therapeutics market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by a robust public health infrastructure and national guidelines promoting bladder-preserving treatments. The U.K. continues to invest in early detection and access to innovative therapies, including BCG alternatives and clinical trials for novel intravesical agents. The National Health Service (NHS) plays a key role in facilitating treatment accessibility across hospitals and urology centers.

Germany Intravesical Bladder Cancer Therapeutics Market Insight

The Germany intravesical bladder cancer therapeutics market is expected to expand at a considerable CAGR during the forecast period, supported by strong oncology expertise, a focus on technological advancement, and widespread clinical adoption of intravesical chemotherapy and immunotherapy. Germany’s precision-driven healthcare system encourages adoption of both established and novel bladder-sparing treatments, particularly for high-risk NMIBC patients, aligning with clinical research trends and patient-centric care models.

Asia-Pacific Intravesical Bladder Cancer Therapeutics Market Insight

The Asia-Pacific intravesical bladder cancer therapeutics market is poised to grow at the fastest CAGR of 8.6% from 2025 to 2032, driven by increasing cancer incidence, healthcare modernization, and expanding access to urologic care in countries such as China, Japan, and India. Government-led cancer control initiatives and rising awareness are promoting early diagnosis and intervention. The region is also experiencing growing interest in cost-effective intravesical solutions, making bladder-preserving therapies more accessible to a broader population.

Japan Intravesical Bladder Cancer Therapeutics Market Insight

The Japan intravesical bladder cancer therapeutics market is gaining momentum due to a high rate of bladder cancer diagnoses and a strong focus on innovation in localized cancer therapies. Japan’s aging population and emphasis on minimally invasive treatment options are fueling demand for intravesical immunotherapy and chemotherapy. In addition, collaboration between government agencies and pharmaceutical firms is promoting the development of next-generation therapies and clinical trials across major cancer centers.

India Intravesical Bladder Cancer Therapeutics Market Insight

The India intravesical bladder cancer therapeutics market accounted for the largest market revenue share in Asia Pacific in 2024, supported by increasing cancer screening rates, growing investments in healthcare infrastructure, and the emergence of local pharmaceutical manufacturers. India is witnessing rising demand for bladder-preserving therapies across both public and private hospitals. The growing availability of affordable intravesical agents and efforts to improve urologic oncology access in urban and semi-urban regions are driving rapid market expansion.

Intravesical Bladder Cancer Therapeutics Market Share

The intravesical bladder cancer therapeutics industry is primarily led by well-established companies, including:

- Ferring Pharmaceuticals (Switzerland)

- ImmunityBio, Inc. (U.S.)

- CG Oncology, Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- AstraZeneca (U.K.)

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Roche Holding AG (Switzerland)

- Lilly (U.S.)

- Qilu Pharmaceutical Co., Ltd. (China)

- Dr. Reddy’s Laboratories Ltd. (India)

- Endo International plc (Ireland)

- Zydus Lifesciences Limited (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Aurobindo Pharma Limited (India)

- Hikma Pharmaceuticals PLC (U.K.)

- Seagen Inc. (U.S.)

- Asieris Pharmaceuticals (China)

- Takeda Pharmaceutical Company Limited (Japan)

What are the Recent Developments in Global Intravesical Bladder Cancer Therapeutics Market?

- In April 2024, Ferring Pharmaceuticals and its U.S.-based subsidiary FerGene advanced commercialization efforts for Adstiladrin (nadofaragene firadenovec), a gene therapy approved by the FDA for BCG-unresponsive non-muscle invasive bladder cancer (NMIBC). The therapy delivers the interferon alfa-2b gene directly into the bladder lining, offering a novel mechanism for immune activation. This milestone signifies a transformative step in bladder cancer care, providing an effective bladder-preserving alternative for high-risk patients lacking options beyond radical cystectomy

- In March 2024, ImmunityBio, Inc. received FDA approval for Anktiva (nogapendekin alfa inbakicept), an IL-15 superagonist used in combination with BCG for patients with BCG-unresponsive NMIBC. This approval marked the second immunotherapy-based alternative to BCG in this niche, targeting immune stimulation pathways to boost the body’s ability to clear cancer cells intravesically. The launch reflects growing regulatory momentum and clinical demand for novel immunotherapies in urologic oncology

- In February 2024, CG Oncology initiated Phase 3 clinical trials for CG0070, an oncolytic immunotherapy designed to selectively replicate in and kill bladder cancer cells while stimulating anti-tumor immune responses. The trial targets patients with high-risk NMIBC unresponsive to BCG, reinforcing the company’s focus on developing intravesical oncolytic viral therapies. This highlights the pipeline expansion and competitive innovation landscape within bladder-sparing treatments

- In January 2024, The U.S. National Cancer Institute (NCI) partnered with multiple academic centers to launch a multicenter clinical program evaluating combination intravesical regimens involving gene therapy and immune checkpoint inhibitors for NMIBC. The initiative reflects a broader shift toward synergistic therapies aiming to enhance efficacy while minimizing systemic exposure, furthering precision oncology within the bladder cancer therapeutics space

- In December 2023, Qilu Pharmaceutical (China) announced early-phase clinical results for its proprietary intravesical chemotherapy combination for intermediate-risk NMIBC patients. With promising outcomes in recurrence reduction and bladder preservation, the company is preparing for international regulatory submissions, signaling the global expansion of innovation beyond Western markets and increasing therapeutic accessibility in Asia-Pacific regions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.