Global Isobutyryl Coa Dehydrogenase Deficiency Treatment Market

Market Size in USD Billion

USD

1.26 Billion

USD

1.91 Billion

2025

2033

USD

1.26 Billion

USD

1.91 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.26 Billion | |

| USD 1.91 Billion | |

| % | |

|

Isobutyryl-Coa Dehydrogenase Deficiency Treatment Market Size

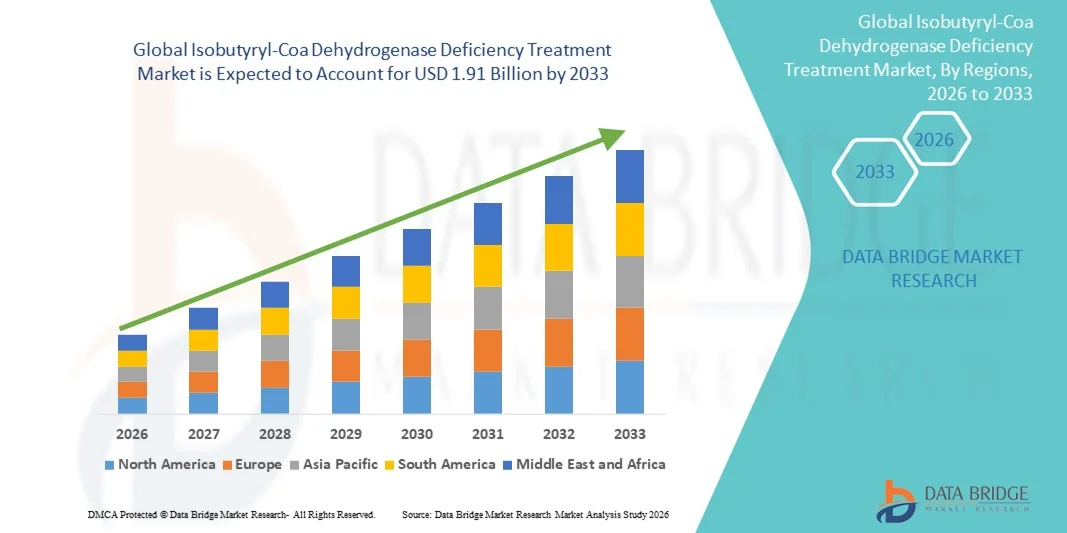

- The global Isobutyryl-Coa Dehydrogenase Deficiency Treatment market size was valued at USD 1.26 billion in 2025 and is expected to reach USD 1.91 billion by 2033, at a CAGR of 5.30% during the forecast period

- The market growth is primarily driven by the increasing awareness, early diagnosis, and advancements in targeted therapies for rare metabolic disorders, which are enabling more effective management of Isobutyryl-CoA Dehydrogenase Deficiency

- In addition, growing investment in research and development, rising healthcare expenditure, and the availability of innovative treatment options are facilitating better patient outcomes, thereby accelerating the adoption of specialized therapies and significantly contributing to the market’s expansion

Isobutyryl-Coa Dehydrogenase Deficiency Treatment Market Analysis

- Treatments for Isobutyryl-CoA Dehydrogenase Deficiency, including L-carnitine supplementation, low-valine food diet, and other supportive therapies, are increasingly vital for managing this rare metabolic disorder by preventing metabolic crises and improving patient quality of life

- The rising demand for effective and personalized treatment options is primarily driven by growing awareness of rare metabolic disorders, improved diagnostic capabilities, and increasing adoption of targeted therapies among healthcare providers

- North America dominated the Isobutyryl-CoA Dehydrogenase Deficiency treatment market with the largest revenue share of 42.5% in 2025, characterized by advanced healthcare infrastructure, early adoption of innovative therapies, and strong presence of key pharmaceutical and biotech players, particularly in the U.S., where specialized metabolic clinics and research initiatives are enhancing treatment access

- Asia-Pacific is expected to be the fastest growing region in the Isobutyryl-CoA Dehydrogenase Deficiency treatment market during the forecast period due to increasing healthcare awareness, rising newborn screening programs, growing investments in rare disease management, and expanding healthcare infrastructure in countries such as China and India

- L-carnitine segment dominated the market with a share of 47.7% in 2025, driven by its established efficacy in improving metabolic outcomes and widespread clinical adoption as a first-line therapy for managing Isobutyryl-CoA Dehydrogenase Deficiency

Report Scope and Isobutyryl-Coa Dehydrogenase Deficiency Treatment Market Segmentation

|

Attributes |

Isobutyryl-Coa Dehydrogenase Deficiency Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Isobutyryl-Coa Dehydrogenase Deficiency Treatment Market Trends

Advancements in Targeted Therapies and Personalized Treatment

- A significant and accelerating trend in the global Isobutyryl-CoA Dehydrogenase Deficiency treatment market is the development of targeted therapies and personalized treatment plans tailored to the metabolic needs of individual patients. This approach is significantly enhancing treatment efficacy and patient outcomes

- For instance, novel L-carnitine formulations and low-valine dietary supplements are being customized based on genetic profiling, allowing more precise metabolic control and reducing the risk of metabolic crises

- Advances in treatment monitoring, such as integration with wearable health devices and mobile health applications, enable real-time tracking of biochemical markers and patient compliance, supporting proactive interventions

- The combination of dietary management and pharmacological therapy in a patient-specific regimen facilitates improved metabolic stability, reduced hospitalization, and better quality of life for patients

- This trend toward personalized and technology-assisted care is reshaping patient expectations for rare metabolic disorder management, encouraging pharmaceutical companies to invest in innovative therapies

- The demand for therapies that are tailored to individual patient needs is growing rapidly across both pediatric and adult populations, as caregivers and clinicians increasingly prioritize efficacy and safety

- Increasing collaboration between biotech companies and research institutions is driving innovation in enzyme therapy and novel formulations, accelerating the development of more effective treatment options

- Rising adoption of telemedicine and remote patient monitoring in metabolic disorders is enhancing therapy adherence and enabling continuous guidance from specialists, expanding treatment reach

Isobutyryl-Coa Dehydrogenase Deficiency Treatment Market Dynamics

Driver

Rising Awareness, Early Diagnosis, and Expanded Screening Programs

- The increasing awareness of rare metabolic disorders, coupled with expanding newborn screening programs and improved diagnostic capabilities, is a significant driver for the heightened demand for Isobutyryl-CoA Dehydrogenase Deficiency treatments

- For instance, in 2025, several hospitals in North America and Asia-Pacific integrated newborn screening for rare metabolic disorders into routine healthcare check-ups, enabling early diagnosis and timely initiation of therapy

- Early detection allows clinicians to implement L-carnitine supplementation or low-valine diets promptly, preventing metabolic crises and long-term complications, thereby improving patient outcomes

- Furthermore, government initiatives and advocacy programs aimed at rare disease awareness are increasing patient identification rates and driving demand for specialized therapies

- Rising healthcare expenditure and increased insurance coverage for rare disease treatments are further propelling adoption of both dietary and pharmacological interventions. The combination of early diagnosis, awareness campaigns, and supportive healthcare policies is expanding patient access to effective treatment, accelerating market growth

- Advancements in diagnostic technologies, such as tandem mass spectrometry, are enabling faster and more accurate detection of metabolic abnormalities, supporting timely intervention and boosting treatment adoption

- Growing partnerships between pharmaceutical companies and rare disease foundations are improving patient outreach, education, and access to treatment programs, strengthening market growth

Restraint/Challenge

High Treatment Costs and Limited Access in Emerging Regions

- Concerns regarding the high cost of therapies and limited availability of specialized metabolic care in emerging regions pose a significant challenge to broader market penetration

- For instance, L-carnitine and low-valine dietary products can be prohibitively expensive in low- and middle-income countries, limiting accessibility for patients who require continuous treatment

- The need for lifelong dietary management and supplementation increases overall treatment expenses, creating financial burden for families and healthcare systems

- In addition, the shortage of trained metabolic specialists and limited infrastructure in some regions restricts diagnosis and treatment initiation, slowing market adoption

- While awareness and screening programs are expanding, gaps in healthcare delivery and affordability continue to hinder widespread access to effective therapies

- Overcoming these challenges through cost reduction strategies, government subsidies, and expansion of specialized metabolic care centers will be crucial for sustained market growth

- Variability in reimbursement policies and insurance coverage across regions can limit patient access to expensive treatments, creating uneven market growth

- Logistical challenges in distributing specialized dietary products and supplements to remote or underserved areas further constrain market penetration and consistent therapy adherence

Isobutyryl-Coa Dehydrogenase Deficiency Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, dosage, route of administration, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the market is segmented into L-carnitine, low-valine food diet, and others. The L-carnitine segment dominated the market with the largest revenue share of 47.7% in 2025, driven by its established efficacy in improving metabolic outcomes for Isobutyryl-CoA Dehydrogenase Deficiency patients. Clinicians often prioritize L-carnitine supplementation due to its direct role in restoring proper fatty acid metabolism and reducing the risk of metabolic crises. The market also sees strong demand for L-carnitine due to widespread clinical adoption, well-documented safety, and compatibility with both pediatric and adult treatment regimens. L-carnitine therapy is further favored as it can be combined with dietary management to improve long-term patient outcomes. Its proven effectiveness in improving biochemical markers and reducing hospitalizations enhances its adoption. The availability of various formulations, including tablets and oral solutions, also contributes to its dominant position.

The low-valine food diet segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing awareness of personalized nutrition and metabolic care. Specialized dietary plans help manage amino acid levels in patients and prevent metabolic complications, making them essential in combination therapies. Growing emphasis on home-based management and telemedicine support for dietary adherence further drives adoption. Advances in pre-packaged medical foods and easier access through online pharmacies are enhancing convenience. Increasing patient and caregiver education on dietary interventions is accelerating acceptance. Rising investment in R&D for more palatable and nutritionally balanced low-valine products is further supporting growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into newborn screening, laboratory tests, physical examination, and others. The newborn screening segment dominated the market in 2025 due to early detection advantages, enabling timely intervention and initiation of therapies such as L-carnitine supplementation and dietary management. Hospitals and clinics increasingly integrate newborn metabolic panels into routine check-ups to identify rare metabolic disorders promptly. Early diagnosis significantly reduces the risk of severe metabolic crises and associated complications. Screening programs also facilitate long-term monitoring and management plans for affected children. Government initiatives and rare disease advocacy are boosting adoption of newborn screening programs globally. High adoption in North America and Europe further reinforces its market dominance.

The laboratory tests segment is expected to witness the fastest growth during the forecast period due to the rising availability of advanced diagnostic technologies such as tandem mass spectrometry and genetic testing. Laboratory tests provide accurate identification of metabolic enzyme deficiencies, guiding targeted treatment plans. Growth is further supported by increasing hospital-based diagnostics and specialized metabolic clinics. Continuous advancements in testing speed and sensitivity are expanding adoption. Emerging markets are increasingly investing in laboratory infrastructure for rare disease detection. Increasing insurance coverage for diagnostic procedures is also enhancing market penetration.

- By Dosage

On the basis of dosage, the market is segmented into tablet, injection, and others. The tablet segment dominated the market with the largest revenue share in 2025 due to ease of administration, patient compliance, and widespread use of oral L-carnitine formulations. Tablets offer convenience for both pediatric and adult patients, allowing home-based long-term treatment. The segment benefits from established clinical protocols and availability across retail and hospital pharmacies. Tablets are often preferred due to stability, accurate dosing, and affordability compared to injectable forms. They are compatible with daily dietary regimens and telemedicine monitoring programs. Strong manufacturing and supply chains ensure consistent availability, reinforcing dominance.

The injection segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its use in acute cases requiring rapid therapeutic intervention. Injectable L-carnitine provides immediate metabolic support during crises or hospitalization. Increasing adoption in specialized metabolic clinics and hospitals supports growth. Injectable formulations are particularly important for newborns and severely affected patients who cannot tolerate oral forms. Development of safer, ready-to-use injection solutions enhances convenience for healthcare providers. Growing awareness among clinicians regarding prompt intervention is accelerating adoption.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, intravenous, and others. The oral segment dominated in 2025 due to patient preference, ease of administration, and suitability for long-term home therapy. Oral formulations allow convenient integration with dietary management, enhancing adherence and metabolic control. Tablets and liquid oral forms cater to different age groups, improving compliance across patient populations. The segment benefits from widespread availability through hospital, retail, and online pharmacies. Long-term safety profile and stability of oral formulations also support dominance. Increasing awareness among caregivers and patients about oral therapy advantages drives adoption.

The intravenous segment is expected to witness the fastest growth from 2026 to 2033 due to its critical role in emergency metabolic management and hospitalized patient care. IV administration ensures rapid bioavailability for immediate therapeutic effects. Adoption is increasing in specialized metabolic wards and intensive care settings. Technological improvements in infusion devices and formulations support safety and ease of use. Growing clinician preference for IV therapy in acute scenarios accelerates uptake. Expansion of hospital infrastructure in emerging markets further drives growth.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, and others. The hospital segment dominated the market in 2025 due to the availability of specialized metabolic care units, trained staff, and access to both diagnostic and therapeutic resources. Hospitals provide comprehensive management including emergency care, dietary counseling, and therapy monitoring. High adoption in developed regions supports market dominance. Hospitals often serve as centers for newborn screening, ongoing monitoring, and patient education. Integrated healthcare services within hospitals ensure continuity of care. The ability to manage acute metabolic crises in hospitals further strengthens the segment.

The clinic segment is expected to witness the fastest growth during the forecast period due to the expansion of specialized metabolic and pediatric clinics offering outpatient care. Clinics provide accessible treatment monitoring, dietary guidance, and routine follow-ups. Growth is fueled by telemedicine integration and home-based support programs. Clinics improve adherence through personalized care and frequent check-ins. Expansion in urban and semi-urban areas is increasing market penetration. Rising partnerships with hospitals and rare disease foundations also accelerate clinic-based adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated in 2025 due to direct availability of prescribed therapies, including L-carnitine and low-valine dietary products, for inpatients and outpatients. Hospital pharmacies ensure compliance with treatment protocols and provide patient counseling. The segment benefits from strong clinician influence and established supply chains. Hospitals often dispense therapies during critical interventions or follow-up visits. Integration with hospital management systems enhances adherence tracking. High trust in hospital pharmacies supports dominant revenue share.

The online pharmacy segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing e-commerce adoption, ease of home delivery, and growing awareness among caregivers. Online channels improve access to specialized dietary products and therapies in remote regions. Rising digital literacy and telemedicine integration are further accelerating adoption. Online pharmacies offer subscription-based and customizable delivery options, enhancing convenience. Cost-effectiveness and comparison options encourage wider usage. Expansion of online healthcare platforms in emerging markets also supports growth.

Isobutyryl-Coa Dehydrogenase Deficiency Treatment Market Regional Analysis

- North America dominated the Isobutyryl-CoA Dehydrogenase Deficiency treatment market with the largest revenue share of 42.5% in 2025, characterized by advanced healthcare infrastructure, early adoption of innovative therapies, and strong presence of key pharmaceutical and biotech players

- Patients and caregivers in the region highly value timely diagnosis, access to specialized metabolic clinics, and availability of therapies such as L-carnitine and low-valine dietary management, which help prevent metabolic crises and improve long-term outcomes

- This widespread adoption is further supported by strong government initiatives for rare disease awareness, high healthcare expenditure, insurance coverage for rare disease treatments, and a robust presence of pharmaceutical and biotech companies, establishing North America as the key market for Isobutyryl-CoA Dehydrogenase Deficiency management

U.S. Isobutyryl-Coa Dehydrogenase Deficiency Treatment Market Insight

The U.S. market captured the largest revenue share of 80% in 2025 within North America, fueled by advanced healthcare infrastructure and widespread newborn screening programs for rare metabolic disorders. Patients and caregivers increasingly prioritize early diagnosis and timely intervention through therapies such as L-carnitine supplementation and low-valine dietary management. The growing adoption of specialized metabolic clinics, telemedicine for dietary and therapy monitoring, and comprehensive rare disease support programs further propels the market. In addition, robust insurance coverage and strong presence of pharmaceutical and biotech companies are significantly contributing to market growth. The increasing awareness campaigns and government initiatives for rare disease management are further accelerating patient identification and treatment initiation.

Europe Isobutyryl-CoA Dehydrogenase Deficiency Treatment Market Insight

The Europe market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by government-funded newborn screening programs and initiatives for rare disease awareness. Rising urbanization, increased healthcare expenditure, and the growing need for specialized care are fostering the adoption of therapies for Isobutyryl-CoA Dehydrogenase Deficiency. European patients and caregivers are increasingly drawn to integrated treatment approaches combining dietary management and L-carnitine supplementation. The region is witnessing growth across both pediatric and adult populations, with treatments being incorporated into hospitals and metabolic care centers. Strong healthcare infrastructure and active participation of pharmaceutical players in research and development also support market expansion.

U.K. Isobutyryl-CoA Dehydrogenase Deficiency Treatment Market Insight

The U.K. market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increased awareness of rare metabolic disorders and advancements in diagnostic and treatment facilities. Early diagnosis through newborn screening and laboratory testing is boosting timely intervention, reducing metabolic complications. The growing emphasis on personalized care and patient support programs encourages wider adoption of therapies. In addition, rising healthcare expenditure, strong insurance coverage, and telemedicine adoption are expected to stimulate market growth. The presence of specialized metabolic clinics and active involvement of rare disease foundations also contribute to the market’s expansion.

Germany Isobutyryl-CoA Dehydrogenase Deficiency Treatment Market Insight

The Germany market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of rare metabolic disorders and the demand for advanced, technology-assisted treatment solutions. Germany’s well-developed healthcare infrastructure, emphasis on innovation, and strong R&D ecosystem promote adoption of L-carnitine therapy and low-valine dietary management. Integration of treatment protocols with newborn screening programs and hospital-based metabolic care centers is becoming increasingly prevalent. Patients and caregivers prefer structured clinical support to ensure compliance and improved outcomes. Government initiatives and insurance coverage for rare disease therapies are further accelerating growth.

Asia-Pacific Isobutyryl-CoA Dehydrogenase Deficiency Treatment Market Insight

The Asia-Pacific market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing awareness of rare metabolic disorders, expansion of newborn screening programs, and rising healthcare expenditure in countries such as China, Japan, and India. Growing inclination towards early diagnosis and timely intervention is fueling adoption of therapies. Government initiatives promoting rare disease management and telemedicine support are enhancing treatment reach. The region’s expanding healthcare infrastructure and presence of specialized metabolic clinics are improving access to therapies. In addition, increasing public and private investment in rare disease research and patient education is further propelling market growth.

Japan Isobutyryl-CoA Dehydrogenase Deficiency Treatment Market Insight

The Japan market is gaining momentum due to the country’s emphasis on preventive healthcare, advanced diagnostic facilities, and high public awareness of rare metabolic disorders. Adoption of newborn screening programs and specialized metabolic clinics supports early intervention through L-carnitine and dietary therapies. The growing elderly population and pediatric patient base are driving demand for effective, easy-to-administer treatment options. Integration of digital monitoring tools and telemedicine for patient compliance is fueling growth. Japan’s technologically advanced healthcare ecosystem and supportive government policies further enhance market expansion.

India Isobutyryl-CoA Dehydrogenase Deficiency Treatment Market Insight

The India market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to increasing awareness of rare diseases, expanding healthcare infrastructure, and rising adoption of newborn screening programs. Patients and caregivers are increasingly seeking accessible and affordable treatments, including L-carnitine supplementation and low-valine dietary management. The push towards telemedicine support and specialized metabolic clinics improves therapy adherence and long-term outcomes. Rising healthcare expenditure, government initiatives for rare disease management, and growing public awareness are key factors propelling market growth. The presence of domestic pharmaceutical companies and online pharmacy distribution channels also enhances market accessibility and penetration.

Isobutyryl-Coa Dehydrogenase Deficiency Treatment Market Share

The Isobutyryl-Coa Dehydrogenase Deficiency Treatment industry is primarily led by well-established companies, including:

- Lonza (Switzerland)

- Merck Sharp & Dohme Corp. (U.S.)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Sanofi (France)

- Johnson & Johnson Services, Inc. (U.S.)

- GSK plc (U.K.)

- AstraZeneca (U.K.)

- Bristol-Myers Squibb Company (U.S.)

- Eli Lilly and Company (U.S.)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Gilead Sciences, Inc. (U.S.)

- Novo Nordisk A/S (Denmark)

- Biogen Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Celgene Corporation (U.S.)

What are the Recent Developments in Global Isobutyryl-Coa Dehydrogenase Deficiency Treatment Market?

- In April 2025, a study published in Frontiers in Genetics reported seven new variants of the ACAD8 gene associated with IBDD expanding the known genetic mutation spectrum and demonstrating significant phenotypic variability, including cases where patients remained asymptomatic for years but some developed neurological symptoms such as febrile seizures

- In April 2025, researchers published a study identifying seven novel variants in ACAD8 (the gene underlying IBDD) among individuals flagged by newborn screening; the study documented long-term follow-up, noting that while most remained clinically normal, some developed neurological symptoms such as febrile seizures highlighting the need for long-term monitoring and individualized management

- In September 2024, a global retrospective analysis (published via Minerva Pediatrics) described two additional ACAD8 mutations (c.1166G>A and c.986C>T), reinforcing the genetic heterogeneity of IBDD and providing new data on genotype‑phenotype correlations to assist diagnosis and future patient management

- In January 2022, a large screening of nearly 303,000 newborns in Ningbo, China identified 27 re‑screened positive cases for IBDD; subsequent genetic testing confirmed multiple known and novel ACAD8 mutation combinations expanding the mutation spectrum and improving diagnostic sensitivity for early detection

- In December 2021, a major study on a cohort of 40 Chinese IBDD patients was published in Orphanet Journal of Rare Diseases, detailing genotype, long-term prognosis and the ACAD8 variant spectrum. It confirmed that many diagnosed via newborn screening remain clinically benign, but underlined that long-term follow-up is needed shaping clinical management guidelines and awareness for IBDD

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.