Global Kyphosis Treatment Market

Market Size in USD Billion

USD

1.37 Billion

USD

2.12 Billion

2024

2032

USD

1.37 Billion

USD

2.12 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.37 Billion | |

| USD 2.12 Billion | |

| % | |

|

Kyphosis Treatment Market Size

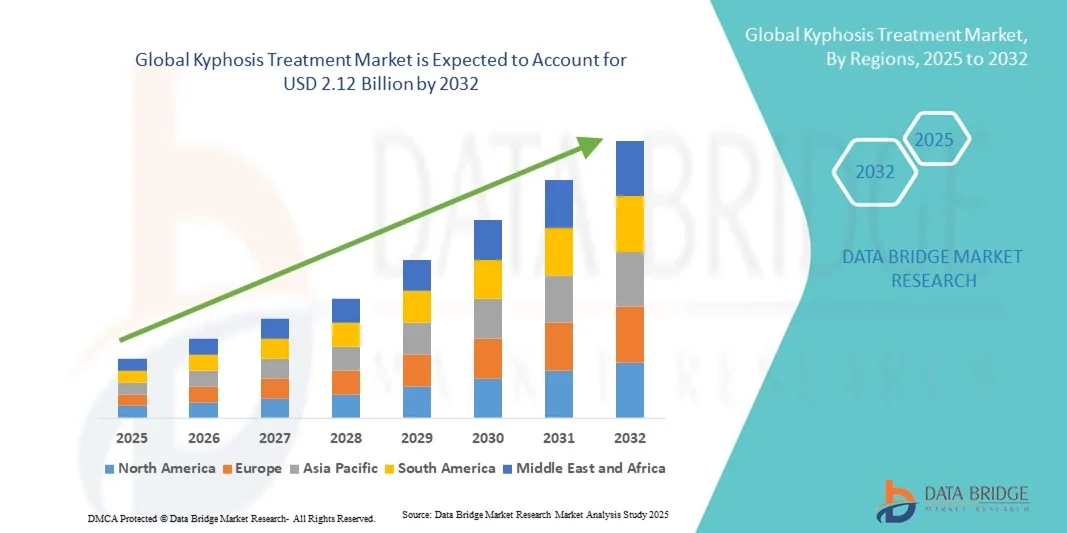

- The global kyphosis treatment market size was valued at USD 1.37 billion in 2024 and is expected to reach USD 2.12 billion by 2032, at a CAGR of 5.60% during the forecast period

- The market growth is largely fueled by the increasing prevalence of spinal deformities, aging populations, and advancements in orthopedic and minimally invasive surgical technologies, driving higher adoption of kyphosis correction treatments

- Furthermore, rising awareness among patients and healthcare providers about early diagnosis, effective treatment options, and rehabilitation programs is encouraging timely interventions. These converging factors are accelerating the uptake of kyphosis treatment solutions, thereby significantly boosting the industry's growth

Kyphosis Treatment Market Analysis

- Kyphosis treatments, encompassing surgical interventions, bracing, and physiotherapy, are increasingly vital in managing spinal deformities and improving patient quality of life, driven by growing awareness of spinal health and advancements in minimally invasive procedures

- The escalating demand for kyphosis treatment is primarily fueled by the rising prevalence of spinal disorders, an aging population, and increasing awareness among healthcare providers and patients about early diagnosis and corrective interventions

- North America dominated the kyphosis treatment market with the largest revenue share of 39.4% in 2024, characterized by advanced healthcare infrastructure, high adoption of minimally invasive surgical technologies, and strong presence of leading orthopedic device manufacturers, with the U.S. experiencing substantial growth in kyphosis surgeries and corrective procedures, driven by innovations in spinal implants and navigation-assisted surgeries

- Asia-Pacific is expected to be the fastest-growing region in the kyphosis treatment market during the forecast period due to rising geriatric populations, improving healthcare access, and increasing investments in orthopedic healthcare facilities

- Surgery segment dominated the kyphosis treatment market with a market share of 47% in 2024, driven by its proven efficacy in correcting severe spinal curvature and improving long-term patient outcomes

Report Scope and Kyphosis Treatment Market Segmentation

|

Attributes |

Kyphosis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Kyphosis Treatment Market Trends

Minimally Invasive and Robotic-Assisted Surgical Adoption

- A significant and accelerating trend in the global kyphosis treatment market is the increasing adoption of minimally invasive and robotic-assisted spinal surgeries, which offer reduced recovery times, lower complication rates, and enhanced surgical precision

- For instance, robotic systems such as Mazor X and ROSA Spine assist surgeons in precise implant placement and real-time navigation, improving outcomes in complex kyphosis correction procedures

- Integration of advanced imaging technologies, intraoperative navigation, and AI-based surgical planning allows for highly personalized treatment strategies, enabling surgeons to anticipate risks and optimize correction angles for each patient

- The combination of robotic-assisted procedures and minimally invasive approaches is reshaping patient expectations, emphasizing shorter hospital stays, reduced postoperative pain, and faster rehabilitation

- Companies such as Medtronic and Globus Medical are developing AI-enabled surgical systems and personalized implant solutions to support precision-driven kyphosis correction surgeries

- The demand for technologically advanced, patient-centric treatment solutions is growing rapidly across both pediatric and adult populations, as patients and healthcare providers increasingly prioritize safety, efficiency, and improved functional outcomes

Kyphosis Treatment Market Dynamics

Driver

Increasing Prevalence of Spinal Disorders and Awareness of Early Intervention

- The rising prevalence of kyphosis, scoliosis, and other spinal deformities, combined with growing awareness of early diagnosis and treatment options, is a significant driver for market growth

- For instance, in March 2024, Medtronic launched an advanced spinal navigation system aimed at improving surgical outcomes for complex spinal deformities, highlighting industry efforts to drive adoption

- As patients and clinicians become more aware of the benefits of timely intervention, treatments such as corrective surgery, bracing, and physiotherapy are increasingly preferred over delayed or conservative approaches, ensuring better long-term outcomes

- Technological advancements in surgical instrumentation, navigation, and imaging systems are making complex kyphosis corrections safer and more effective, fueling broader adoption in hospitals and specialty orthopedic centers

- The growing geriatric population and pediatric patients with congenital spinal deformities are further increasing demand for effective kyphosis treatment solutions globally

Restraint/Challenge

High Treatment Costs and Limited Access in Emerging Region

- The high cost of advanced surgical procedures, implants, and postoperative rehabilitation presents a significant challenge to widespread adoption, particularly in developing countries and regions with limited healthcare infrastructure

- For instance, robotic-assisted surgeries and custom spinal implants can be prohibitively expensive, limiting accessibility for price-sensitive patients or hospitals with budget constraints

- Limited availability of trained spinal surgeons and specialized healthcare facilities in emerging regions further restricts market penetration, creating disparities in treatment access

- In addition, concerns about postoperative complications, lengthy rehabilitation, and patient compliance with physiotherapy or bracing regimens can affect treatment outcomes and adoption rates

- Overcoming these challenges through cost-effective treatment options, expansion of surgical training programs, and improvements in healthcare infrastructure will be vital for sustained market growth in the global kyphosis treatment industry

- Regulatory variations and stringent approval processes for new surgical devices and implants in different regions can delay product launches, affecting market expansion

Kyphosis Treatment Market Scope

The market is segmented on the basis of type, diagnostic test, treatment, and end user.

- By Type

On the basis of type, the kyphosis treatment market is segmented into postural kyphosis, Scheuermann's kyphosis, and congenital kyphosis. The Scheuermann's kyphosis segment dominated the market with the largest revenue share in 2024, driven by its higher prevalence among adolescents and the growing demand for early-stage corrective treatments. Patients diagnosed with Scheuermann's kyphosis often require surgical or bracing interventions depending on severity, which has led to increased adoption of specialized spinal implants and physiotherapy programs. Advanced imaging and personalized treatment planning further support better outcomes, boosting the segment's market contribution. Healthcare providers are increasingly focusing on comprehensive management of this condition, including post-surgery rehabilitation and long-term monitoring, which enhances patient satisfaction and reinforces market growth. The availability of established surgical techniques and braces tailored for Scheuermann's kyphosis also supports robust demand.

The postural kyphosis segment is anticipated to witness the fastest growth from 2025 to 2032 due to rising awareness about early detection and non-surgical corrective measures, such as posture training and physical therapy. Growing adoption of preventive care programs in schools and clinics is driving increased diagnosis and management of mild postural kyphosis. Non-invasive treatments are favored by both patients and healthcare providers for their cost-effectiveness and minimal risk, which is contributing to faster market expansion. Digital physiotherapy platforms and wearable posture-correcting devices are further accelerating adoption. The segment also benefits from increasing health consciousness and emphasis on ergonomic interventions in workplaces and academic settings.

- By Diagnostic Test

On the basis of diagnostic tests, the kyphosis treatment market is segmented into imaging, biopsy, and others. The imaging segment dominated the market in 2024 due to its critical role in accurately diagnosing kyphosis severity, identifying vertebral anomalies, and planning corrective interventions. Advanced imaging modalities such as X-ray, MRI, and CT scans provide detailed insights into spinal alignment and curvature, enabling precise surgical or bracing strategies. The segment’s growth is further supported by technological advancements in imaging equipment, which allow faster, more detailed, and less invasive assessments. Hospitals and specialty orthopedic centers increasingly rely on imaging for pre-operative planning and long-term monitoring, which strengthens the segment's market dominance. In addition, insurance coverage and standard diagnostic protocols favor imaging over other diagnostic tests, increasing adoption.

The others segment, including genetic testing and lab-based assessments, is expected to witness the fastest growth from 2025 to 2032, due to increasing focus on personalized treatment planning and early identification of congenital spinal deformities. Technological advancements in molecular diagnostics and predictive tools are enabling early intervention strategies for high-risk patients. Integration of AI and digital platforms in diagnostic workflows supports more accurate and efficient assessment, fueling adoption. Growing awareness among pediatricians and orthopedists about genetic predispositions to spinal deformities is also driving market growth. Moreover, early-stage detection through innovative diagnostic methods reduces the need for invasive surgeries, making this segment attractive for both patients and healthcare providers.

- By Treatment

On the basis of treatment, the kyphosis treatment market is segmented into medications, surgery, and bracing. The surgery segment dominated the market with the largest share of 47% in 2024 due to its efficacy in correcting severe spinal deformities and improving long-term functional outcomes. Advanced surgical techniques, including minimally invasive and robotic-assisted procedures, provide higher precision and lower complication rates, driving adoption in hospitals and specialty centers. Postoperative care and rehabilitation programs further enhance treatment success, boosting the segment’s revenue. Surgeons increasingly rely on computer-assisted navigation and patient-specific implants, which improves outcomes and reinforces the preference for surgical interventions. Complex cases such as congenital or Scheuermann’s kyphosis often necessitate surgical correction, contributing to strong market dominance.

The bracing segment is anticipated to witness the fastest growth from 2025 to 2032 due to its non-invasive nature, cost-effectiveness, and increasing acceptance among adolescents with mild-to-moderate kyphosis. The rising prevalence of postural kyphosis and the adoption of corrective braces in schools and outpatient clinics are driving market expansion. Advances in ergonomic and customizable braces, coupled with wearable monitoring systems, enhance patient compliance and outcomes. Growing awareness among parents and healthcare providers about early-stage intervention further fuels demand. In addition, bracing solutions are increasingly integrated with digital monitoring platforms to track patient progress, making this segment highly attractive for future growth.

- By End User

On the basis of end users, the kyphosis treatment market is segmented into hospitals, clinics, ambulatory surgical centers, and others. The hospital segment dominated the market in 2024 due to the availability of advanced surgical facilities, experienced spinal surgeons, and comprehensive post-operative care programs. Hospitals serve as the primary choice for both surgical and complex non-surgical kyphosis treatments, accommodating inpatient monitoring and multidisciplinary care. Access to advanced diagnostic imaging and specialized rehabilitation units further strengthens the segment’s market share. The high volume of patient inflow and the presence of technologically advanced spinal care infrastructure ensure sustained dominance in the market.

The ambulatory surgical centers segment is expected to witness the fastest growth from 2025 to 2032 due to the rising preference for outpatient procedures, shorter hospital stays, and cost-effective treatment options. Minimally invasive surgical approaches and enhanced recovery protocols allow many kyphosis corrections to be performed in these centers. Patients increasingly favor ambulatory centers for their convenience, reduced infection risks, and quicker return to daily activities. Expansion of these centers in urban and suburban areas, coupled with investments in specialized spinal care equipment, supports rapid adoption. The trend toward outpatient care and early intervention programs makes this segment a high-growth opportunity in the kyphosis treatment market.

Kyphosis Treatment Market Regional Analysis

- North America dominated the kyphosis treatment market with the largest revenue share of 39.4% in 2024, characterized by advanced healthcare infrastructure, high adoption of minimally invasive surgical technologies, and strong presence of leading orthopedic device

- Patients and healthcare providers in the region prioritize access to state-of-the-art diagnostic tools, advanced implants, and comprehensive post-operative care, contributing to strong demand for both surgical and non-surgical kyphosis treatments

- This widespread adoption is further supported by high healthcare spending, a well-established network of specialty orthopedic centers, and the presence of key industry players such as Medtronic and Globus Medical, establishing North America as a leading market for kyphosis management solutions

U.S. Kyphosis Treatment Market Insight

The U.S. kyphosis treatment market captured the largest revenue share of 42% in 2024 within North America, fueled by advanced healthcare infrastructure and high adoption of minimally invasive and robotic-assisted spinal surgeries. Patients and clinicians increasingly prioritize early diagnosis and corrective interventions to improve long-term spinal health. The growing preference for technologically advanced surgical solutions, coupled with comprehensive rehabilitation programs, further propels the market. Moreover, the presence of leading spinal care device manufacturers such as Medtronic and Globus Medical, along with rising awareness of spinal deformities, is significantly contributing to market expansion.

Europe Kyphosis Treatment Market Insight

The Europe kyphosis treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence of spinal deformities, high-quality healthcare facilities, and rising awareness about early-stage treatment. Urbanization and the rising demand for specialized orthopedic care are fostering the adoption of surgical and non-surgical interventions. European patients are increasingly opting for minimally invasive surgeries, bracing, and physiotherapy programs to improve quality of life. The region is witnessing notable growth across hospitals, clinics, and specialty centers, with treatments being incorporated into both new healthcare initiatives and rehabilitation programs.

U.K. Kyphosis Treatment Market Insight

The U.K. kyphosis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of spinal health, demand for advanced corrective procedures, and early intervention programs. Concerns regarding spinal deformities among adolescents and adults are encouraging timely diagnosis and treatment. The U.K.’s strong healthcare infrastructure, robust insurance coverage, and increasing adoption of minimally invasive and robotic-assisted surgeries are expected to continue stimulating market growth. In addition, educational campaigns and preventive screening programs are enhancing early detection and non-surgical treatment adoption.

Germany Kyphosis Treatment Market Insight

The Germany kyphosis treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of spinal deformities and demand for technologically advanced corrective solutions. Germany’s well-developed healthcare system and emphasis on innovation and precision surgery promote the adoption of surgical and non-surgical interventions. Advanced imaging technologies, spinal implants, and rehabilitation programs are driving patient preference for hospitals and specialty centers. Integration of robotic-assisted surgeries and patient-specific treatment plans aligns with local expectations for safe, effective, and sustainable care.

Asia-Pacific Kyphosis Treatment Market Insight

The Asia-Pacific kyphosis treatment market is poised to grow at the fastest CAGR of 23% during the forecast period of 2025 to 2032, driven by increasing prevalence of spinal deformities, rising geriatric population, and improving healthcare infrastructure in countries such as China, Japan, and India. Growing awareness of early diagnosis, coupled with government initiatives promoting healthcare accessibility, is driving adoption of both surgical and non-surgical interventions. Technological advancements and expansion of specialty spinal centers are making treatments more accessible and affordable, further boosting market growth.

Japan Kyphosis Treatment Market Insight

The Japan kyphosis treatment market is gaining momentum due to the country’s aging population, high healthcare standards, and demand for advanced spinal care solutions. Adoption of minimally invasive and robotic-assisted surgeries is increasing in hospitals and specialty centers. Japan’s focus on precision healthcare and post-operative rehabilitation programs is enhancing patient outcomes. The integration of digital physiotherapy, imaging technologies, and AI-assisted surgical planning is further driving growth. In addition, preventive care and early-stage intervention programs for adolescents are supporting rising demand in the country.

India Kyphosis Treatment Market Insight

The India kyphosis treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rising prevalence of spinal deformities, expanding healthcare infrastructure, and increasing awareness about early intervention. India’s growing middle class, improving access to orthopedic care, and rising adoption of minimally invasive surgeries and bracing solutions are key factors propelling the market. Government initiatives to strengthen healthcare facilities, coupled with the availability of affordable treatment options, are accelerating adoption in hospitals, clinics, and specialty centers across urban and semi-urban regions.

Kyphosis Treatment Market Share

The Kyphosis Treatment industry is primarily led by well-established companies, including:

- Amneal Pharmaceuticals LLC (U.S.)

- Zimmer Biomet (U.S.)

- Aurobindo Pharma Limited (India)

- Teva Pharmaceuticals Inc. (U.S.)

- B. Braun SE (Germany)

- Integra LifeSciences Corporation (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Medtronic (Ireland)

- MicroPort Scientific Corporation (China)

- NuVasive, Inc. (U.S.)

- Orthofix Medical Inc. (U.S.)

- Perrigo Company plc (Ireland)

- Stryker (U.S.)

- ScoliCare (Australia)

- Hanger Clinic (U.S.)

- Rothman Orthopaedic Institute (U.S.)

- Ortho Sport & Spine Physicians (U.S.)

- Boston Scientific Corporation (U.S.)

What are the Recent Developments in Global Kyphosis Treatment Market?

- In November 2025, advancements in biomaterials led to the development of biocompatible coatings that can be applied alongside drugs such as strontium ranelate or simvastatin. These coatings support implant osteointegration in osteoporotic patients, improving the effectiveness of kyphosis surgeries

- In August 2025, personalized treatment strategies incorporating 3D printing were introduced for kyphosis patients. This approach allows for the creation of customized implants and braces tailored to the individual's specific spinal anatomy, improving treatment efficacy

- In April 2025, doctors at Jupiter Hospital in Pune, India, successfully performed a groundbreaking full endoscopic internal gibbectomy on a 12-year-old boy suffering from congenital thoracic kyphosis. This rare spinal condition, caused by the fusion of two thoracic vertebrae, led to a bony hump pressing on the spinal cord, impairing mobility and bladder control

- In October 2024, a novel minimally invasive surgical technique known as Biportal Endoscopic Lumbar Ponte Osteotomy (BELPO) was introduced for correcting rigid post-traumatic kyphosis at the L2–3 level. This procedure utilizes dual endoscopic portals to perform osteotomy and decompression, offering significant advantages for frail, osteoporotic patients

- In August 2022, the U.S. Food and Drug Administration (FDA) granted 510(k) clearance for Surgalign's Cortera spinal fixation system. This system offers both open and minimally invasive modules and integrates with Surgalign’s Holo Portal surgical system, enhancing precision in spinal surgeries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.