Global Lymphedema Tarda Treatment Market

Market Size in USD Million

USD

13.53 Million

USD

26.09 Million

2025

2033

USD

13.53 Million

USD

26.09 Million

2025

2033

| 2026 - 2033 | |

| USD 13.53 Million | |

| USD 26.09 Million | |

| % | |

|

Lymphedema Tarda Treatment Market Size

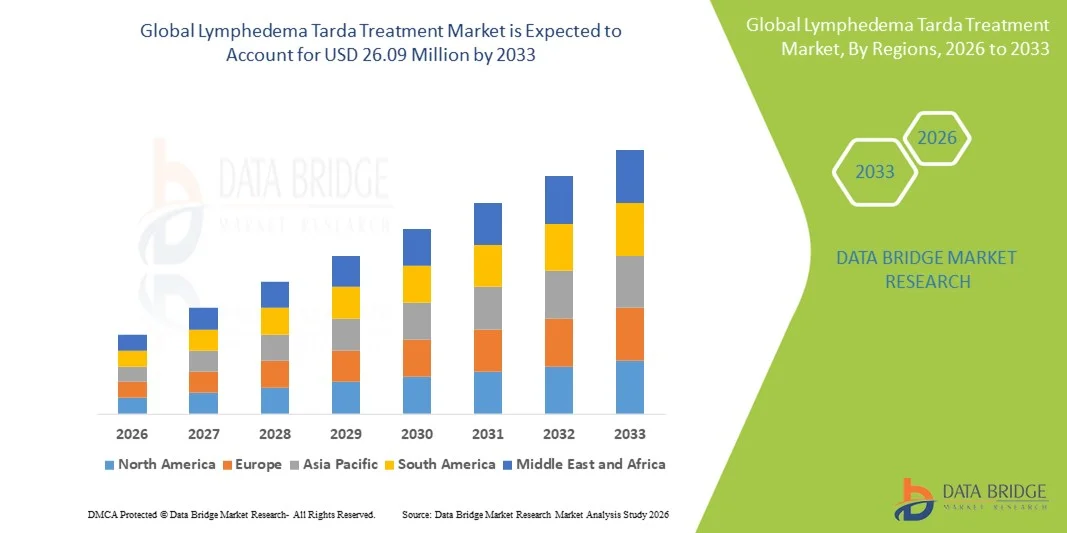

- The global lymphedema tarda treatment market size was valued at USD 13.53 million in 2025 and is expected to reach USD 26.09 million by 2033, at a CAGR of 8.55% during the forecast period

- The market growth is primarily driven by the rising prevalence of late-onset lymphatic dysfunction, coupled with improving diagnostic capabilities and broader clinical recognition of lymphedema tarda as a distinct patient segment. Increasing adoption of established therapies including compression solutions, decongestive therapies, and microsurgical interventions is also contributing to expanding demand

- In addition, growing patient awareness, expanding access to advanced treatment modalities, and rising investments in rehabilitation and home-based management tools are promoting stronger uptake of early and sustained care. These converging factors are accelerating the adoption of comprehensive lymphedema tarda treatment solutions, thereby significantly boosting the industry's overall growth

Lymphedema Tarda Treatment Market Analysis

- Lymphedema tarda, a late-onset lymphatic disorder occurring after the age of 35, is becoming an increasingly important focus within chronic lymphedema management, driven by the rising demand for effective long-term care solutions. Treatments such as compression therapy, manual lymphatic drainage, pneumatic compression devices, and microsurgical procedures are gaining prominence across hospitals, specialty clinics, and homecare settings as awareness and diagnosis continue to improve

- The growing demand for lymphedema tarda treatment is largely fueled by the rising prevalence of lymphatic diseases, increasing patient awareness, and the strong clinical preference for non-invasive and minimally invasive therapies, supported by expanding rehabilitation services. Conservative therapy remains widely adopted due to its effectiveness across all stages of the condition and its foundational role in comprehensive decongestive treatment

- North America dominated the lymphedema tarda treatment market with the largest revenue share of 42% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement support, and a growing number of specialized lymphedema treatment centers. The U.S. is experiencing substantial growth, driven by increased adoption of compression systems, pneumatic devices, and microsurgical interventions across both hospital and outpatient care settings

- Asia-Pacific is expected to be the fastest-growing region in the lymphedema tarda treatment market during the forecast period, supported by rising healthcare expenditure, expanding access to diagnostic and therapeutic services, and increasing awareness initiatives across developing economies

- Conservative therapy dominated the lymphedema tarda treatment market with a market share of 56.8% in 2025, driven by its position as the first-line standard of care, strong physician preference, and broad applicability across Stage I, Stage II, and Stage III cases

Report Scope and Lymphedema Tarda Treatment Market Segmentation

|

Attributes |

Lymphedema Tarda Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Lymphedema Tarda Treatment Market Trends

Rising Adoption of Advanced Compression and Microsurgical Techniques

- A significant and accelerating trend in the global lymphedema tarda treatment market is the increasing adoption of advanced compression systems and emerging microsurgical procedures, driven by growing clinical recognition of late-onset lymphatic dysfunction and the need for long-term management solutions

- For instance, devices such as the Flexitouch Plus (Tactile Medical) and Lympha Press systems offer programmable multi-chamber compression, improving patient adherence and outcomes through enhanced ease of use and targeted limb therapy. Similarly, lymphaticovenous anastomosis (LVA) and vascularized lymph node transfer (VLNT) are gaining attention as viable options for select patients

- Integration of innovative technologies enables features such as automated pressure adjustments, personalized therapy profiles, and intelligent monitoring of treatment sessions. For instance, several digital compression systems now utilize smart sensors to optimize pressure delivery and provide data-driven insights for clinicians. Furthermore, patient-facing mobile applications allow remote monitoring and support personalized treatment adjustments

- The seamless connection of advanced compression tools and digital monitoring platforms facilitates centralized control of patient therapy, enabling clinicians to track adherence, symptom progression, and therapeutic results through a single interface, promoting better long-term outcomes

- This trend toward more intelligent, data-enabled, and clinically integrated treatment systems is reshaping patient expectations for lymphatic care. Consequently, companies such as Bio Compression Systems are developing digitally enhanced compression solutions with improved automation, user-friendly interfaces, and remote connectivity features

- The demand for advanced compression and microsurgical treatment options is growing rapidly across hospitals, specialty clinics, and homecare settings, as patients increasingly prioritize effective, convenient, and clinically validated long-term management solutions

Lymphedema Tarda Treatment Market Dynamics

Driver

Increasing Disease Prevalence and Growing Demand for Non-Invasive Therapies

- The increasing prevalence of chronic lymphatic disorders and a rising number of patients presenting with late-onset lymphedema are significant drivers supporting the growing demand for effective treatment solutions

- For instance, in 2025, several clinical programs expanded access to comprehensive decongestive therapy and pneumatic compression in both hospital and homecare settings, encouraging broader adoption of evidence-based treatments and supporting market growth

- As patients become more aware of progressive lymphatic impairment and seek long-term management strategies, lymphedema tarda treatments offer advanced features such as staged therapy protocols, enhanced compression options, and improved symptom management, positioning them as compelling alternatives to untreated disease progression

- Furthermore, the growing emphasis on integrated chronic care pathways and the prioritization of non-invasive treatment options are making conservative and device-based therapies central components of lymphedema management, supported by expanding clinical education initiatives

- The convenience of home-based compression therapy, remote monitoring, and the ability to manage symptoms through wearable garments and programmable devices are key factors propelling adoption across both hospital and homecare environments. The trend toward digital health integration and patient-friendly therapy tools further contributes to market expansion

Restraint/Challenge

Skin Irritation Issues and Regulatory Compliance Hurdle

- Concerns surrounding skin irritation, dermatitis, and discomfort associated with prolonged compression use pose a significant challenge to broader treatment adherence, particularly among patients with sensitive skin or advanced disease stages

- For instance, reports of garment-related irritation or improper pressure settings have led some patients to hesitate in adopting long-term compression therapy, underscoring the need for improved material quality and better clinical guidance

- Addressing these comfort concerns through breathable fabrics, adjustable compression technologies, and patient education on proper usage is critical for improving adherence. Companies such as JOBST and Juzo emphasize skin-friendly materials and ergonomic garment design to support long-term wearability. In addition, navigating regulatory requirements for medical compression devices and microsurgical procedures can be complex and time-consuming for manufacturers

- While device approvals and surgical standardization are improving, the regulatory pathway for new pharmacologic or device-based therapies remains stringent, creating cost and timeline hurdles for market entrants

- The perceived complexity of treatment, ongoing maintenance needs, and potential discomfort can hinder widespread adoption, especially among older patients or those with limited access to specialized care centers

- Overcoming these challenges through improved material technologies, enhanced patient education, streamlined regulatory processes, and ongoing product innovation will be essential for sustaining long-term market growth

Lymphedema Tarda Treatment Market Scope

The market is segmented on the basis of disease, disease severity, treatment, end user, and distribution channel.

- By Disease

On the basis of disease, the global lymphedema tarda treatment market is segmented into primary lymphedema and secondary lymphedema. The secondary lymphedema segment dominated the market, driven by its significantly higher prevalence worldwide, largely linked to cancer treatments, trauma, and chronic venous disorders. Rising global cancer incidence and improved survivorship mean more patients develop late-onset lymphatic dysfunction requiring long-term therapy. Hospitals and oncology centers frequently diagnose secondary lymphedema, driving steady demand for compression garments, devices, and rehabilitation services. Healthcare guidelines prioritize managing secondary lymphedema early, further cementing its dominant share. Reimbursement structures for post-cancer lymphedema also support higher adoption of therapy products and systems.

The primary lymphedema segment is expected to witness the fastest growth during forecast period, fueled by better diagnostic imaging, improved genetic awareness, and expanded clinical evaluation of hereditary lymphatic disorders. As late-onset primary lymphedema becomes more frequently recognized, more patients are captured early in the treatment continuum. Increased research into congenital lymphatic abnormalities is driving therapeutic innovation, particularly around emerging drug mechanisms targeting lymphangiogenesis. Awareness initiatives by rare-disease groups are improving referral rates to specialists, enabling faster diagnosis. The segment also benefits from growing physician education and expanded availability of specialized physiotherapy programs.

- By Disease Severity

On the basis of disease severity, the market is segmented into Stage I, Stage II, and Stage III. The Stage II segment held the largest market revenue share, supported by strong diagnosis rates and the point at which most patients present with clinically visible swelling and soft-tissue changes. Stage II is widely recognized as the optimal treatment phase when conservative therapies and device-based interventions yield the most benefit, driving broad adoption. Compression therapy, manual lymphatic drainage, and complete decongestive therapy (CDT) are heavily utilized in this stage, contributing to recurring revenue demand. More facilities are equipped to manage Stage II patients, strengthening provider capacity. In addition, reimbursement for Stage II therapies is more accessible in many regions, further reinforcing segment dominance.

The Stage I segment is anticipated to witness the fastest growth rate during forecast period, driven by increasing emphasis on early detection in cancer survivors and high-risk patient groups. Rising use of imaging techniques such as lymphoscintigraphy and MRI lymphangiography is improving detection in early, reversible phases. The growing adoption of preventive interventions including early compression therapy supports rapid segment expansion. Patients are increasingly educated about early symptoms, boosting clinical visits and early treatment uptake. Remote physiotherapy programs and self-management tools are also driving early-stage engagement. As health systems shift toward value-based care, Stage I intervention is becoming a major focus area.

- By Treatment

On the basis of treatment, the market is segmented into conservative therapy, device-based therapy, surgical treatment, other therapies, and pharmacologic treatments. The conservative therapy segment dominated the market with a market share of 56.8%, supported by its status as the global standard of care for lymphedema tarda management. Complete decongestive therapy, manual lymphatic drainage, and compression garments remain the most widely prescribed interventions. These therapies are accessible, non-invasive, and easy to deploy across hospitals, outpatient rehabilitation settings, and homecare environments. Long-term management needs mean patients repeatedly purchase garments and accessories, driving sustainable revenue. Strong clinician preference and structured guidelines from lymphology associations reinforce the use of conservative approaches.

The device-based therapy segment is projected to grow the fastest during forecast period, driven by advancements in pneumatic compression pumps, smart wearable compression devices, and home-use digital systems. Increasing patient preference for automated, convenient, home-based solutions is accelerating adoption. New technologies offer personalized pressure settings and remote monitoring, improving adherence and clinical outcomes. The rise in chronic disease conditions and aging populations enhances the need for home-treatment alternatives. Expanding reimbursement for advanced compression devices in select markets further encourages adoption. Strong evidence showing improved lymphatic flow with intermittent pneumatic compression (IPC) is also supporting rapid market growth.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, homecare settings, and physiotherapy & rehabilitation centers. The hospitals segment dominated the market, as hospitals remain the primary point for diagnosis, staging, and multidisciplinary treatment planning for lymphedema tarda. Oncology departments, vascular units, and rehabilitation teams collaborate to deliver structured care pathways, ensuring steady patient inflow. Hospitals purchase large volumes of compression garments, devices, and surgical tools, giving them strong procurement power. They also perform advanced procedures such as lymphovenous anastomosis (LVA) and vascularized lymph node transfer, supporting higher therapy utilization. Long-term monitoring programs for cancer survivors further contribute to recurring demand. Hospitals benefit from strong reimbursement agreements that support broad treatment adoption.

The homecare settings segment is expected to witness the fastest growth during forecast period, driven by rising adoption of self-management strategies and home-use compression technology. Patients increasingly seek convenient, cost-effective options that allow consistent daily therapy without clinical visits. Portable pneumatic pumps, smart compression sleeves, and remote physiotherapy programs are transforming home-based care models. Aging populations and higher prevalence of chronic edema conditions are accelerating the shift toward home treatment. Telehealth integration is making patient monitoring and therapy guidance more accessible. These factors collectively contribute to rapid expansion of home-based lymphedema management.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital procurement, specialty distributors, medical supply stores, and direct-to-consumer. The hospital procurement segment held the largest market revenue share, underpinned by bulk purchasing of compression bandages, garments, treatment devices, and surgical supplies. Hospitals manage the highest patient volume and require continuous replenishment for outpatient and inpatient lymphedema programs. Cancer treatment centers, in particular, maintain standard inventory for managing post-operative or radiation-induced lymphedema. Strong supplier-hospital partnerships and negotiated long-term contracts stabilize procurement flows. Reimbursement alignment further ensures consistent adoption of hospital-based products.

The direct-to-consumer segment is set to witness the fastest growth during forecast period, driven by rising online sales of compression wear, home-use devices, and therapy accessories. Patients increasingly prefer buying directly from manufacturers for guaranteed product authenticity and faster delivery. Digital health platforms provide guidance on sizing and product selection, encouraging consumer confidence. Growth in self-management practices and telehealth-led follow-ups also boosts online purchasing behavior. Direct channels help manufacturers improve margins and expand patient reach, accelerating adoption. As awareness rises globally, more consumers are turning to D2C platforms for convenient, repeat procurement of essential supplies.

Lymphedema Tarda Treatment Market Regional Analysis

- North America dominated the lymphedema tarda treatment market with the largest revenue share of 42% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement support, and a growing number of specialized lymphedema treatment centers

- Patients in the region benefit from well-established lymphology programs, availability of certified lymphedema therapists, and broad adoption of compression garments, pneumatic devices, and surgical interventions across major hospitals and specialty centers

- This strong uptake is further supported by favorable reimbursement policies, high healthcare spending, and growing patient preference for early diagnosis and structured long-term management, positioning North America as a leading hub for both clinical care and innovation in lymphedema tarda treatment

U.S. Lymphedema Tarda Treatment Market Insight

The U.S. lymphedema tarda treatment market captured the largest revenue share within North America in 2025, driven by early diagnosis practices, strong specialist availability, and widespread adoption of advanced compression and device-based therapies. Patients increasingly seek structured treatment pathways, including complete decongestive therapy, pneumatic compression systems, and emerging microsurgical options. Growing awareness of lymphatic disorders across oncology, geriatrics, and primary care settings continues to accelerate demand for standardized care. The U.S. also benefits from strong reimbursement frameworks and well-established lymphedema management programs. Moreover, expanding integration of digital therapeutic tools and home-based management devices is significantly contributing to market growth.

Europe Lymphedema Tarda Treatment Market Insight

The Europe lymphedema tarda treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily supported by robust clinical guidelines, comprehensive lymphology networks, and strong hospital-based adoption of conservative therapies. The rise in chronic disease prevalence, aging populations, and demand for high-standard rehabilitative care is fostering the uptake of advanced compression garments and physiologic treatment modalities. European consumers are increasingly drawn to clinically validated therapies and structured long-term symptom management programs. The region is experiencing strong growth across hospitals, specialty clinics, and rehabilitation centers, with lymphedema services incorporated into both new and existing medical infrastructure.

U.K. Lymphedema Tarda Treatment Market Insight

The U.K. lymphedema tarda treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by expanding community-based lymphedema services and heightened focus on chronic disease management. Growing concerns regarding delayed lymphatic diagnosis and increasing cancer survivorship rates are encouraging both hospitals and specialty centers to adopt comprehensive treatment frameworks. The U.K.’s integration of digital health tools, along with strong NHS support for conservative therapy, is expected to further stimulate market adoption. Increasing patient access to compression garments, certified therapists, and home-based treatment solutions is also contributing to steady market expansion.

Germany Lymphedema Tarda Treatment Market Insight

The Germany lymphedema tarda treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by strong awareness of lymphatic health and demand for technologically advanced therapeutic solutions. Germany’s well-developed healthcare infrastructure and emphasis on evidence-based rehabilitation promote the adoption of high-quality compression garments, device-based therapy, and microsurgical interventions. The integration of lymphedema treatment with broader home-care and chronic disease programs is becoming increasingly prevalent. A strong preference for clinically validated, durable, and patient-friendly solutions aligns closely with local clinical practice and patient expectations.

Asia-Pacific Lymphedema Tarda Treatment Market Insight

The Asia-Pacific lymphedema tarda treatment market is poised to grow at the fastest CAGR during the forecast period, driven by rising healthcare investment, increasing awareness of lymphatic disorders, and expanding access to physiotherapy and rehabilitation services. Countries such as China, Japan, and India are seeing rapid growth in demand for compression therapy, device-based treatments, and specialized clinical services. The region’s growing burden of cancer and chronic diseases is further accelerating treatment adoption. Moreover, as APAC expands its manufacturing capabilities for compression products and home-care medical devices, treatment affordability and accessibility are improving across both urban and semi-urban areas.

Japan Lymphedema Tarda Treatment Market Insight

The Japan lymphedema tarda treatment market is gaining momentum due to the country’s advanced healthcare ecosystem, strong rehabilitation culture, and increasing focus on long-term chronic care. Japanese patients place significant emphasis on precision, comfort, and clinically validated treatment methods. Adoption of compression therapy, lymphatic drainage, and digital monitoring tools is rising alongside the expansion of smart medical devices. Moreover, Japan’s aging population is such asly to spur demand for easy-to-use, effective, and home-friendly lymphedema management solutions across both residential and clinical settings.

India Lymphedema Tarda Treatment Market Insight

The India lymphedema tarda treatment market accounted for the largest revenue share within Asia-Pacific in 2025, supported by the country's expanding healthcare infrastructure, rising awareness of lymphatic disorders, and growing investment in physiotherapy and rehabilitation services. India is emerging as a major market for compression garments and device-based therapies, with increasing adoption across hospitals, specialty clinics, and home-care settings. The nation’s push toward digital health, along with affordable treatment options and strong local manufacturing capabilities, is accelerating market penetration. In addition, the country’s large population and rising chronic disease incidence continue to support strong long-term market growth.

Lymphedema Tarda Treatment Market Share

The Lymphedema Tarda Treatment industry is primarily led by well-established companies, including:

- Tactile Medical (U.S.)

- BIO COMPRESSION SYSTEMS. (U.S.)

- Lympha Press (Israel)

- medi GmbH & Co. KG (Germany)

- SIGVARIS GROUP (Switzerland)

- Lohmann & Rauscher GmbH & Co. KG (Germany)

- Essity (Sweden)

- 3M (U.S.)

- ConvaTec (U.K.)

- Devon Medical Products (U.S.)

- Huntleigh Healthcare (Sweden)

- ThermoTek Inc. (U.S.)

- Koya Medical (U.S.)

- Smith & Nephew (U.K.)

- Paul Hartmann AG (Germany)

- ImpediMed Ltd. (Australia)

- BiaCare Medical LLC (U.S.)

- Compression Dynamics, LLC (U.S.)

- Sanyleg S.r.l. (Italy)

- Wright Therapy Products (Germany)

What are the Recent Developments in Global Lymphedema Tarda Treatment Market?

- In September 2025, AIROS Medical launched an expanded-size lineup of its truncal compression garments, introducing more inclusive sizing options for patients with larger body types or atypical swelling distributions. This enhancement aims to reduce disparities in lymphedema care accessibility by ensuring more patients can be properly fitted with medically necessary compression systems

- In April 2025, AIROS Medical received U.S. FDA 510(k) clearance for its AIROS 8P pneumatic compression device and advanced truncal garment system. The system is designed to treat edema in the legs, abdomen, hips, and lower trunk areas a critical step for patients with complicated lymphedema patterns such as those involving the pelvic region. The clearance broadened AIROS’s clinical portfolio and improved patient access to multi-zone compression therapy

- In February 2025, Tactile Medical expanded the commercial availability of Nimbl to include lower-extremity lymphedema (phlebolymphedema). This expansion marked the first time the device addressed both arm and leg lymphedema in a single platform, improving treatment coverage for a significantly larger patient base. The update also enabled clinicians to prescribe a unified device solution for complex multi-limb cases

- In October 2024, Tactile Medical launched its next-generation Nimbl pneumatic compression system for upper-extremity lymphedema. The new platform introduced enhanced portability, improved pressure-delivery algorithms, and quieter operation, making at-home therapy more accessible. This launch strengthened Tactile Medical’s presence in the non-invasive lymphedema management space and expanded advanced digital-connected therapy options for patients

- In September 2024, Tactile Medical’s Nimbl platform received PDAC coding approval (HCPCS E0651) from the U.S. Centers for Medicare & Medicaid Services (CMS). This approval allows the device to be billed and reimbursed under Medicare, significantly increasing affordability for patients and enabling broader adoption among healthcare providers. It represents one of the biggest reimbursement developments in recent years for lymphedema treatment technology

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.