Global Medical Device Interface Market

Market Size in USD Billion

USD

732.37 Billion

USD

1,712.27 Billion

2024

2032

USD

732.37 Billion

USD

1,712.27 Billion

2024

2032

| 2025 - 2032 | |

| USD 732.37 Billion | |

| USD 1,712.27 Billion | |

| % | |

|

Medical Device Interface Market Size

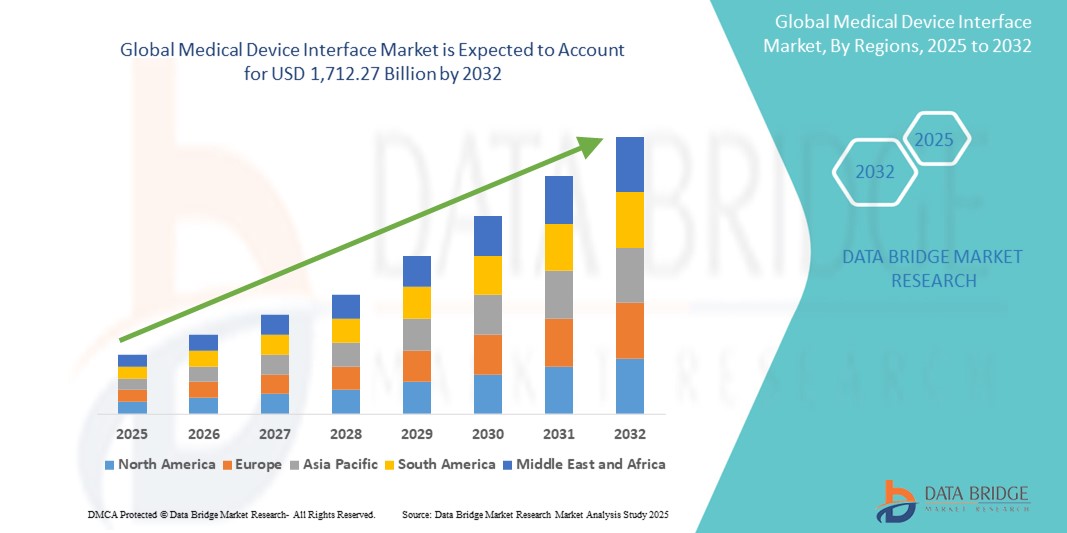

- The global medical device interface market size was valued at USD 732.37 billion in 2024 and is expected to reach USD 1,712.27 billion by 2032, at a CAGR of 11.20% during the forecast period

- The market growth is largely driven by the increasing integration of medical devices with healthcare IT systems and the rising demand for real-time patient monitoring and data sharing across healthcare settings

- Furthermore, the growing need for interoperable systems, improved patient outcomes, and streamlined clinical workflows is positioning medical device interfaces as a critical component in modern healthcare infrastructure. These converging factors are accelerating the adoption of medical device interface solutions, thereby significantly boosting the industry’s growth

Medical Device Interface Market Analysis

- Medical device interfaces, enabling seamless data exchange between medical devices and healthcare information systems, are becoming increasingly essential for modern clinical environments due to their role in enhancing patient monitoring, improving workflow efficiency, and supporting real-time data-driven decision-making

- The escalating demand for medical device interfaces is primarily fueled by the rapid digitization of healthcare, rising need for interoperable systems, and the increasing prevalence of chronic diseases that require continuous patient monitoring and data integration

- North America dominated the medical device interface market with the largest revenue share of 42% in 2024, supported by robust healthcare infrastructure, widespread adoption of electronic health records (EHRs), and the presence of major health tech firms and device manufacturers focused on innovation and regulatory compliance

- Asia-Pacific is expected to be the fastest growing region in the medical device interface market during the forecast period due to expanding healthcare access, rising investments in healthcare IT, and government initiatives to modernize hospital infrastructure

- The software interface segment dominated the medical device interface market with a market share of 45.3% in 2024, driven by the need for secure, scalable, and customizable integration solutions that can effectively manage and transmit complex medical data across diverse clinical platforms

Report Scope and Medical Device Interface Market Segmentation

|

Attributes |

Medical Device Interface Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Medical Device Interface Market Trends

“Rising Integration with EHR Systems and Real-Time Data Analytics”

- A significant and accelerating trend in the global medical device interface market is the growing integration of interfaces with electronic health record (EHR) systems and advanced real-time analytics platforms, enhancing clinical decision-making and patient monitoring

- For instance, companies such as capsule technologies offer interfaces that connect a wide range of bedside devices directly to hospital EHRs, streamlining data capture and reducing manual input errors. Similarly, Mindray integrates real-time patient data into central monitoring systems to support fast, informed medical responses

- These interfaces enable healthcare providers to automatically collect, analyze, and document patient data from devices such as infusion pumps, ventilators, and monitors, improving workflow efficiency and care accuracy. Real-time data analytics can detect anomalies in patient vitals and alert clinicians to potential emergencies, supporting proactive intervention

- In addition, interoperability with cloud-based platforms is enabling remote access and collaboration between departments and care teams, fostering a more connected and responsive healthcare environment. Through a single dashboard, clinicians can monitor patient vitals, track equipment usage, and manage care protocols

- This trend toward interoperable, intelligent medical device interfaces is transforming healthcare delivery, particularly in high-acuity settings such as intensive care units. As a result, leading players such as GE HealthCare and Philips are investing in integrated platforms that unify data flows across devices and systems

- The rising demand for seamless data management and improved patient safety is fueling interface adoption across hospitals, outpatient facilities, and home care settings, making it a cornerstone of digital healthcare transformation

Medical Device Interface Market Dynamics

Driver

“Surging Demand for Connected Care and Streamlined Clinical Workflows”

- The increasing need for efficient clinical workflows and the demand for integrated, connected care delivery are key drivers of growth in the medical device interface market

- For instance, in February 2024, Masimo Corporation launched enhancements to its connectivity platform, including seamless device integration with hospital IT systems, reinforcing the shift toward data-driven healthcare

- As the healthcare industry emphasizes interoperability and automation, medical device interfaces help reduce clinician workload by automating data entry and enabling centralized monitoring of multiple devices

- The rising burden of chronic diseases and the expansion of remote patient monitoring (RPM) further enhance the value proposition of interfaces, allowing continuous tracking of patient vitals and supporting timely medical interventions

- Moreover, regulatory frameworks promoting the use of EHRs and medical device integration in developed markets are pushing healthcare facilities to adopt robust interface solutions that ensure compliance and improve care coordination

- The growing availability of plug-and-play interfaces and scalable software platforms is also contributing to market expansion, particularly in small- to mid-sized healthcare institutions

Restraint/Challenge

“Complex Integration Requirements and Data Security Concerns”

- The integration of diverse medical devices from multiple manufacturers, each using different communication protocols, presents a significant challenge to seamless data exchange. This complexity can slow implementation and require extensive customization

- For instance, legacy systems in many hospitals lack standardization, making interface deployment labor-intensive and costly, especially in low-resource settings. Compatibility issues between proprietary platforms can further hinder the establishment of fully integrated environments

- Data privacy and cybersecurity are also major concerns, as interfaces transmit sensitive patient health data over networks that may be vulnerable to cyber threats. Healthcare organizations must comply with regulations such as HIPAA and GDPR, adding further pressure to ensure secure infrastructure

- High-profile breaches and concerns over ransomware attacks in hospital systems have prompted increased scrutiny over data protection measures in medical device communications

- Overcoming these challenges requires adoption of standardized communication protocols, robust cybersecurity frameworks, and vendor collaboration to ensure interoperability. Companies such as Cerner and Capsule Technologies are investing in secure, standards-based interface development to address these critical concerns and build trust in digital health infrastructure

Medical Device Interface Market Scope

The market is segmented on the basis of type, technology, and end-use

- By Type

On the basis of type, the medical device interface market is segmented into hardware and software. The software segment dominated the market with the largest market revenue share of 45.3% in 2024, driven by the increasing need for interoperable solutions that can facilitate seamless data exchange between medical devices and hospital information systems. Software interfaces offer scalable integration across various devices and are crucial for real-time monitoring, decision support, and centralized data collection. Their flexibility, customization capabilities, and ease of deployment in cloud-based and on-premise environments have made them a preferred solution across hospitals and outpatient settings.

The hardware segment is anticipated to witness steady growth from 2025 to 2032, supported by the demand for physical connectors, adapters, and gateways that bridge communication between non-digital medical devices and IT systems. As hospitals continue to modernize legacy equipment, hardware interfaces serve as vital components enabling digital transformation without the need to replace entire systems.

- By Technology

On the basis of technology, the medical device interface market is segmented into wireless, wired, and hybrid. The wireless segment held the largest market revenue share in 2024, attributed to the growing adoption of wireless technologies such as Wi-Fi, Bluetooth, and Zigbee in hospital and home care settings. Wireless interfaces reduce cable clutter, enhance mobility, and enable real-time data transmission across departments or remote locations. Their deployment in remote patient monitoring and mobile health units is a key factor contributing to their dominance.

The hybrid segment is expected to witness the fastest CAGR from 2025 to 2032, as healthcare providers seek solutions that combine the reliability of wired communication with the flexibility of wireless connectivity. Hybrid systems are increasingly used in critical care units where high reliability and continuous data flow are essential, while still supporting mobility and scalability

- By End Use

On the basis of end-use, the medical device interface market is segmented into hospitals, home care, diagnostic and imaging centers, ambulatory care centers, and others. The hospitals segment dominated the market in 2024 with the largest revenue share, owing to the high volume of connected devices, extensive infrastructure for IT integration, and strong emphasis on patient safety and workflow optimization. Hospitals require comprehensive interface solutions to manage large-scale device integration across multiple departments.

The home care segment is projected to grow at the fastest rate during the forecast period, fueled by the increasing shift towards remote patient monitoring, aging populations, and cost-effective care delivery outside traditional hospital environments. Medical device interfaces in home settings support continuous monitoring, improve patient engagement, and help reduce hospital readmissions.

Medical Device Interface Market Regional Analysis

- North America dominated the medical device interface market with the largest revenue share of 42% in 2024, supported by robust healthcare infrastructure, widespread adoption of electronic health records (EHRs), and the presence of major health tech firms and device manufacturers focused on innovation and regulatory compliance

- Healthcare providers in the region prioritize advanced connectivity solutions that improve workflow efficiency, enable real-time patient monitoring, and ensure compliance with stringent data security regulations such as HIPAA

- This broad adoption is further supported by the presence of leading interface solution providers, high healthcare expenditure, and continuous technological advancements, positioning medical device interfaces as critical components in both acute care hospitals and outpatient care facilities across the U.S. and Canada

U.S. Medical Device Interface Market Insight

The U.S. medical device interface market captured the largest revenue share of 79.3% in North America in 2024, driven by the widespread deployment of electronic health records (EHRs), a strong focus on health IT innovation, and the presence of leading interface technology providers. Hospitals and health systems are prioritizing real-time data integration and seamless connectivity between devices to support clinical efficiency and patient safety. Government incentives promoting interoperability and data exchange, coupled with the increasing demand for remote monitoring and home-based care, are propelling market growth in the U.S.

Europe Medical Device Interface Market Insight

The Europe medical device interface market is projected to grow at a substantial CAGR during the forecast period, supported by strict regulatory mandates for patient data security and medical device interoperability. The region’s emphasis on modernizing healthcare infrastructure and advancing digital health is accelerating the adoption of interface systems in both public and private healthcare institutions. The ongoing shift toward value-based care and population health management is further enhancing demand for interfaces that streamline data sharing across care settings.

U.K. Medical Device Interface Market Insight

The U.K. medical device interface market is expected to grow at a noteworthy CAGR, fueled by the country’s strong focus on digital transformation within the National Health Service (NHS). Government initiatives aimed at boosting interoperability between medical devices and hospital information systems are encouraging adoption. The increasing need for integrated care pathways and telehealth expansion is also prompting healthcare facilities to invest in interface technologies that enable efficient, secure data transmission.

Germany Medical Device Interface Market Insight

The Germany medical device interface market is anticipated to expand significantly during the forecast period, driven by the country’s advanced healthcare infrastructure and commitment to health technology innovation. Strong regulatory frameworks supporting digital health adoption, coupled with robust demand for interoperable medical systems, are promoting the use of interface solutions. The integration of medical devices with hospital IT networks and centralized data systems is becoming more prevalent across hospitals and clinics.

Asia-Pacific Medical Device Interface Market Insight

The Asia-Pacific medical device interface market is expected to grow at the fastest CAGR during the forecast period from 2025 to 2032, driven by rising healthcare investments, increasing digitization, and a growing population burdened by chronic diseases. Countries such as China, Japan, and India are actively adopting smart healthcare technologies and expanding their health IT infrastructure, thereby fueling interface adoption. Government-backed initiatives to improve healthcare delivery and modernize hospital systems are key growth accelerators in the region.

Japan Medical Device Interface Market Insight

The Japan medical device interface market is gaining momentum due to the country’s strong technological infrastructure, aging population, and emphasis on healthcare automation. The integration of medical devices with centralized monitoring systems and EHR platforms is becoming increasingly common in hospitals and eldercare facilities. Japan’s push toward smart hospitals and digital transformation in healthcare is expected to further drive market expansion.

India Medical Device Interface Market Insight

The India medical device interface market accounted for the largest revenue share in Asia-Pacific in 2024, fueled by rapid healthcare infrastructure development, growing demand for health data digitization, and government-led digital health programs. As hospitals and diagnostic centers upgrade their systems to improve patient care and operational efficiency, the adoption of interface solutions is accelerating. The presence of both global and local vendors offering cost-effective technologies further strengthens the market outlook in India.

Medical Device Interface Market Share

The medical device interface industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Masimo (U.S.)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Drägerwerk AG & Co. KGaA (Germany)

- ICU Medical, Inc. (U.S.)

- Hill-Rom Holdings, Inc. (U.S.)

- Smiths Group plc (U.S.)

- NIHON KOHDEN CORPORATION (Japan)

- Spacelabs Healthcare (U.S.)

- Medtronic (Ireland)

- Stryker (U.S.)

- Fresenius Medical Care AG (Germany)

- Siemens Healthineers AG (Germany)

- Baxter (U.S.)

- Honeywell International Inc. (U.S.)

- Biotronik SE & Co. KG (Germany)

- B. Braun SE (Germany)

What are the Recent Developments in Global Medical Device Interface Market?

- In April 2023, Capsule Technologies, a subsidiary of Philips and a leader in medical device connectivity, launched an enhanced version of its Capsule Medical Device Information Platform (MDIP). The upgrade offers improved real-time data integration and analytics capabilities, aimed at streamlining clinical workflows and enabling predictive insights for healthcare providers. This advancement reinforces Capsule’s commitment to advancing interoperability and care efficiency through robust interface solutions

- In March 2023, Masimo Corporation introduced expanded connectivity features in its Hospital Automation platform, allowing for seamless integration between patient monitoring systems and hospital IT infrastructure. This development enhances patient safety by reducing manual data entry errors and supporting continuous, centralized monitoring. The upgrade demonstrates Masimo's strategic focus on enabling intelligent, connected care environments across acute and non-acute settings

- In March 2023, Cerner Corporation (now part of Oracle Health) partnered with multiple U.S. hospital networks to deploy its latest interface solutions that ensure bi-directional data flow between EHR systems and bedside medical devices. This initiative enhances clinical decision-making by enabling real-time visibility of patient data and supports compliance with evolving healthcare data standards. The partnership highlights Cerner’s leadership in fostering seamless integration across digital health platforms

- In February 2023, Mindray Medical International Limited announced the integration of its BeneVision monitoring systems with third-party medical device interfaces to enhance interoperability in ICUs. This initiative aims to reduce alarm fatigue, optimize patient monitoring, and ensure compatibility with various clinical systems, further positioning Mindray as a key innovator in the critical care interface space

- In January 2023, GE HealthCare introduced its new Edison Digital Health Platform, a next-generation interface architecture designed to unify data from multiple medical devices and applications. The platform empowers clinicians with real-time insights and supports advanced analytics for diagnostic and therapeutic decisions. This development reflects GE HealthCare’s continued investment in digital transformation and clinical data integration.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.