Global Nasal Polyposis Drugs Market

Market Size in USD Billion

CAGR :

%

USD

3.28 Billion

USD

5.07 Billion

2025

2033

USD

3.28 Billion

USD

5.07 Billion

2025

2033

| 2026 –2033 | |

| USD 3.28 Billion | |

| USD 5.07 Billion | |

| % | |

|

Nasal Polyposis Drugs Market Size

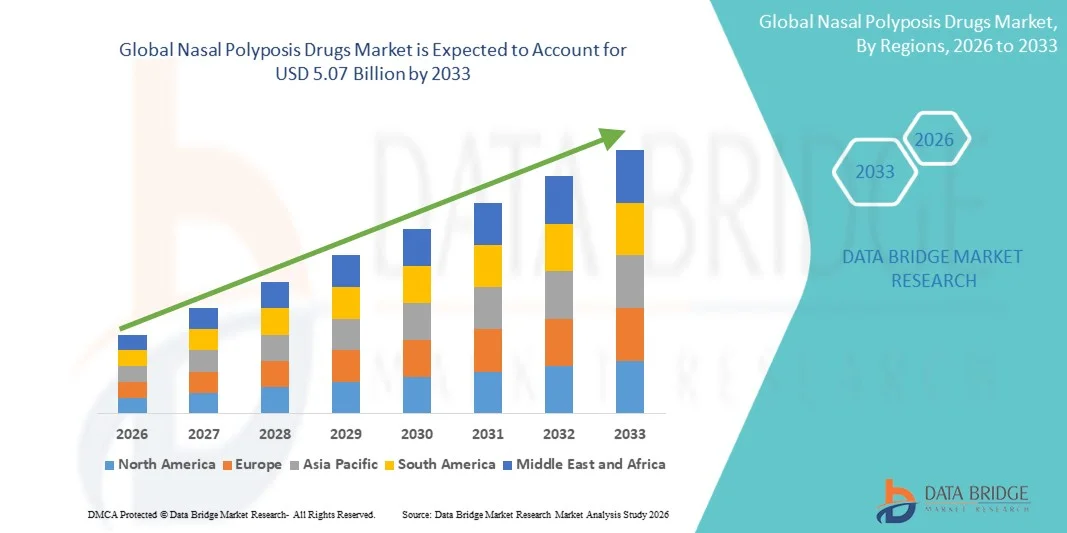

- The global nasal polyposis drugs market size was valued at USD 3.28 billion in 2025 and is expected to reach USD 5.07 billion by 2033, at a CAGR of 5.60% during the forecast period

- The market growth is primarily driven by increasing prevalence of chronic rhinosinusitis with nasal polyps (CRSwNP), rising awareness about effective treatment options, and the expansion of biologic and corticosteroid therapies

- Additionally, growing patient preference for non-surgical, minimally invasive therapies and increasing healthcare accessibility worldwide are positioning nasal polyposis drugs as essential in managing chronic sinus conditions. These factors are collectively accelerating market expansion and driving sustained growth in the sector

Nasal Polyposis Drugs Market Analysis

- Nasal polyposis drugs, including nasal corticosteroids, oral and injectable corticosteroids, Dupixent, and other emerging therapies, are increasingly critical in managing chronic rhinosinusitis with nasal polyps (CRSwNP) due to their effectiveness in reducing inflammation, improving nasal airflow, and minimizing the need for surgical interventions

- The rising demand for nasal polyposis drugs is primarily fueled by the growing prevalence of CRSwNP, increasing awareness of non-surgical treatment options, and expanding availability of targeted therapies such as biologics and corticosteroids that provide better disease control

- North America dominated the nasal polyposis drugs market with the largest revenue share of 38.7% in 2025, supported by high patient awareness, advanced healthcare infrastructure, and early adoption of therapies such as Dupixent. The U.S. market witnessed significant growth in prescription volumes for novel corticosteroids and biologics, driven by clinical guidelines emphasizing early intervention

- Asia-Pacific is expected to be the fastest growing region in the nasal polyposis drugs market during the forecast period due to increasing healthcare accessibility, rising prevalence of CRSwNP, and growing adoption of advanced therapies in urban healthcare facilities

- Nasal corticosteroids segment dominated the nasal polyposis drugs market with a market share of 41.3% in 2025, driven by their efficacy, ease of administration, and widespread recommendation as the first-line therapy for patients with mild to moderate CRSwNP

Report Scope and Nasal Polyposis Drugs Market Segmentation

|

Attributes |

Nasal Polyposis Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Nasal Polyposis Drugs Market Trends

“Emergence of Biologics and Targeted Therapies”

- A significant and accelerating trend in the global nasal polyposis drugs market is the growing adoption of biologic therapies such as Dupixent, which provide targeted treatment for severe CRSwNP cases and reduce the need for repeated surgical interventions

- For instance, Dupixent has shown efficacy in reducing polyp size and improving nasal airflow in patients unresponsive to standard corticosteroid therapy, establishing biologics as a preferred option for severe cases

- Advanced formulations of nasal corticosteroids are also being developed to enhance delivery efficiency and patient compliance, minimizing systemic exposure while maximizing local efficacy

- Biologics and optimized corticosteroid therapies are increasingly integrated into treatment protocols alongside conventional care, allowing physicians to tailor interventions based on disease severity and patient response

- This trend towards precision medicine and targeted drug delivery is reshaping patient expectations and treatment paradigms, encouraging pharmaceutical companies to innovate in formulation, dosing, and combination therapies

- The demand for effective, minimally invasive, and personalized nasal polyposis treatments is growing rapidly across both developed and emerging markets, as patients seek long-term disease control with fewer adverse effects

- Increasing investment in R&D for novel therapies, including small molecules and next-generation biologics, is expected to drive further innovation and expand treatment options for CRSwNP patients

Nasal Polyposis Drugs Market Dynamics

Driver

“Increasing Prevalence of CRSwNP and Rising Patient Awareness”

- The rising prevalence of chronic rhinosinusitis with nasal polyps (CRSwNP), coupled with growing awareness of available treatment options, is a major driver for the increasing demand for nasal polyposis drugs

- For instance, a study in the U.S. highlighted that 4% of the adult population suffers from CRSwNP, fueling prescriptions for corticosteroids and biologics as first-line and advanced therapies

- Expanding patient education initiatives and advocacy programs are improving awareness about non-surgical treatment alternatives, encouraging early intervention and adherence to prescribed therapies

- Healthcare providers are increasingly recommending combination therapy approaches, such as biologics with nasal corticosteroids, to improve patient outcomes and reduce recurrence rates

- Rising insurance coverage and reimbursement for advanced therapies in developed markets are further facilitating patient access to these drugs, driving adoption

- The growing focus on disease management, quality of life improvements, and prevention of surgical interventions is propelling sustained market growth globally

- For instance, increasing partnerships between pharmaceutical companies and hospitals are expanding patient access programs, promoting adoption of advanced therapies in underserved areas

- Advancements in telemedicine and digital health platforms are enabling remote diagnosis, monitoring, and prescription of nasal polyposis drugs, increasing patient convenience and treatment adherence

Restraint/Challenge

“High Cost of Biologics and Limited Access in Emerging Markets”

- The high cost of biologic therapies and certain advanced corticosteroid formulations poses a significant challenge to wider adoption of nasal polyposis drugs, particularly in price-sensitive regions

- For instance, Dupixent therapy can cost several thousand dollars annually, limiting accessibility for patients without comprehensive insurance coverage

- Regulatory hurdles and complex approval processes for novel biologics can delay market entry in some countries, constraining growth opportunities

- In emerging markets, limited healthcare infrastructure and inadequate distribution networks restrict patient access to advanced therapies, even where demand is rising

- Additionally, the need for regular monitoring, follow-up visits, and physician-administered injections for certain therapies can be a barrier for patient adherence and convenience

- Overcoming these challenges through cost-reduction strategies, expanded reimbursement, and localized distribution programs will be critical for expanding the market in underserved regions

- For instance, patient assistance programs and subsidy schemes introduced by pharmaceutical companies can help reduce the financial burden and improve therapy adoption in low-income areas

- Limited awareness among general practitioners about the latest biologic therapies can delay referrals to specialists, impacting timely treatment initiation and overall market growth

Nasal Polyposis Drugs Market Scope

The market is segmented on the basis of drugs, route of administration, end-users, and distribution channel.

- By Drugs

On the basis of drugs, the nasal polyposis drugs market is segmented into nasal corticosteroids, oral and injectable corticosteroids, Dupixent, and others. The nasal corticosteroids segment dominated the market with the largest revenue share of 41.3% in 2025, driven by their first-line recommendation for CRSwNP management, ease of self-administration, and strong efficacy in reducing inflammation and polyp size. Physicians often prefer nasal corticosteroids for mild to moderate cases due to their safety profile and minimal systemic side effects. The segment also benefits from patient familiarity and the availability of multiple brands and formulations across key markets. Their integration into standard treatment guidelines further reinforces their market dominance. Strong consumer awareness and accessibility through various pharmacies contribute to consistent adoption and revenue generation.

The Dupixent segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing prescriptions for severe CRSwNP cases unresponsive to corticosteroids. Dupixent, a targeted biologic therapy, offers improved patient outcomes and reduced recurrence rates, making it highly attractive for specialists. Growing clinical evidence, patient support programs, and expanding insurance coverage are accelerating adoption. Physicians increasingly recommend Dupixent as a preferred advanced therapy, while awareness campaigns highlight its benefits for long-term disease control. Biologics such as Dupixent are also driving innovation in personalized treatment approaches, contributing to rapid market expansion.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, nasal, and others. The nasal route dominated the market with the largest revenue share in 2025 due to its direct delivery to the target site, high efficacy in controlling polyp growth, and convenience for patients in self-administering therapy at home. Nasal sprays are widely prescribed and form a cornerstone of CRSwNP management, offering rapid relief and minimal systemic exposure. Their dominance is supported by guideline recommendations and strong physician familiarity. Patients also prefer nasal administration for comfort and ease of use over oral or injectable options. The availability of combination sprays with optimized dosing further reinforces their market leadership.

The parenteral route is expected to witness the fastest growth from 2026 to 2033, driven by the expanding use of biologics and injectable corticosteroids for severe or refractory cases. Parenteral administration allows precise dosing, improved systemic bioavailability, and longer-lasting effects, making it ideal for advanced therapies. Increasing adoption in hospitals and specialty clinics, along with patient education on injection techniques, is boosting uptake. This segment benefits from rising physician confidence in biologic therapies and improved access programs for patients in need of advanced treatment.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospital segment dominated the market with the largest revenue share of 39.5% in 2025, driven by inpatient treatment for severe CRSwNP cases, administration of advanced biologics, and management of comorbid conditions. Hospitals provide access to specialist care, diagnostic testing, and monitoring that ensure effective treatment outcomes. The concentration of ENT specialists and access to advanced therapies in hospital settings reinforces this dominance. Institutional treatment protocols and insurance coverage also favor hospital-based prescriptions. The segment remains strong due to ongoing investments in hospital infrastructure and patient education programs.

The homecare segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising patient preference for self-administered therapies such as nasal corticosteroids and home-use biologic injections. Convenience, reduced hospital visits, and increased awareness about at-home care solutions are driving adoption. Remote patient monitoring and telehealth guidance further support homecare growth. The segment is also expanding due to improved distribution of nasal sprays and support services for at-home biologic administration.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The retail pharmacy segment dominated the market with the largest revenue share of 45.2% in 2025, driven by widespread accessibility, convenience, and immediate availability of nasal corticosteroids and oral medications. Patients commonly rely on retail pharmacies for OTC and prescription therapies, supported by pharmacist guidance and brand recognition. Strong distribution networks, promotional campaigns, and loyalty programs contribute to high retail adoption. The presence of multiple branded formulations and generic alternatives further strengthens this segment.

The online pharmacy segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing e-commerce adoption, patient preference for home delivery, and the convenience of subscription-based refills. Online pharmacies provide access to both prescription and advanced therapies, including biologics, expanding reach to remote areas. Growing digital health literacy, telemedicine integration, and secure online payment platforms are accelerating this trend. Online channels also facilitate discreet purchase and timely medication adherence, boosting market growth.

Nasal Polyposis Drugs Market Regional Analysis

- North America dominated the nasal polyposis drugs market with the largest revenue share of 38.7% in 2025, supported by high patient awareness, advanced healthcare infrastructure, and early adoption of therapies such as Dupixent

- Patients and healthcare providers in the region highly value the effectiveness, targeted treatment options, and improved quality of life offered by advanced therapies such as Dupixent and optimized nasal corticosteroids

- This widespread adoption is further supported by strong insurance coverage, high patient awareness, early adoption of innovative therapies, and easy access to hospitals and specialty clinics, establishing nasal polyposis drugs as a key solution for managing chronic sinus conditions in both mild and severe cases

U.S. Nasal Polyposis Drugs Market Insight

The U.S. nasal polyposis drugs market captured the largest revenue share of 82% in 2025 within North America, fueled by the high prevalence of chronic rhinosinusitis with nasal polyps (CRSwNP) and widespread adoption of advanced therapies such as nasal corticosteroids and Dupixent. Patients increasingly prioritize effective, non-surgical treatment options to manage inflammation, improve nasal airflow, and reduce polyp recurrence. The growing awareness of targeted biologic therapies, combined with robust insurance coverage and strong healthcare infrastructure, further propels market growth. Moreover, the integration of specialty care programs and patient support services is significantly enhancing access and adherence to prescribed therapies.

Europe Nasal Polyposis Drugs Market Insight

The Europe nasal polyposis drugs market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence of CRSwNP and rising demand for effective, guideline-recommended therapies. Growing urbanization, increasing healthcare expenditure, and awareness campaigns are fostering the adoption of corticosteroids and biologics. European patients are also drawn to treatments that improve quality of life and reduce surgical interventions. The region is experiencing significant growth across hospitals, specialty clinics, and homecare settings, with therapies being integrated into both new treatment protocols and updated clinical guidelines.

U.K. Nasal Polyposis Drugs Market Insight

The U.K. nasal polyposis drugs market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising patient awareness and preference for minimally invasive, effective treatment options. Additionally, increasing prevalence of CRSwNP and concerns regarding disease progression are encouraging both patients and healthcare providers to adopt advanced therapies, including biologics. The U.K.’s well-established healthcare infrastructure and strong insurance coverage, alongside growing digital health adoption and online pharmacy channels, are expected to continue stimulating market growth.

Germany Nasal Polyposis Drugs Market Insight

The Germany nasal polyposis drugs market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of chronic sinus conditions and the demand for advanced, targeted therapies. Germany’s robust healthcare infrastructure, emphasis on innovation, and high patient compliance promote the adoption of biologics and optimized corticosteroid treatments, particularly in hospital and specialty clinic settings. The integration of patient support programs and telehealth services is also becoming increasingly prevalent, with a strong preference for treatments that reduce recurrence and improve long-term outcomes.

Asia-Pacific Nasal Polyposis Drugs Market Insight

The Asia-Pacific nasal polyposis drugs market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by increasing urbanization, rising disposable incomes, and technological advancements in countries such as China, Japan, and India. The region’s growing awareness of CRSwNP treatment options, supported by government healthcare initiatives and expanding access to biologics, is driving adoption. Furthermore, local pharmaceutical manufacturing and distribution networks are improving affordability and accessibility of nasal polyposis drugs, enabling broader patient reach.

Japan Nasal Polyposis Drugs Market Insight

The Japan nasal polyposis drugs market is gaining momentum due to the country’s high prevalence of CRSwNP, strong healthcare infrastructure, and emphasis on early intervention. Japanese patients increasingly prefer effective, non-surgical therapies such as nasal corticosteroids and biologics, supported by specialist care programs. The integration of nasal polyposis drugs into digital health platforms and homecare initiatives is fueling growth. Moreover, Japan’s aging population is likely to spur demand for easier-to-use, safe, and effective treatment options in both residential and clinical settings.

India Nasal Polyposis Drugs Market Insight

The India nasal polyposis drugs market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to increasing prevalence of CRSwNP, rising healthcare awareness, and expanding middle-class population. India is emerging as a significant market for both corticosteroid therapies and biologics, driven by affordability, accessibility, and growing adoption in hospitals, specialty clinics, and homecare settings. Government initiatives promoting healthcare infrastructure and telemedicine, alongside strong domestic pharmaceutical manufacturing, are key factors propelling market growth in India.

Nasal Polyposis Drugs Market Share

The Nasal Polyposis Drugs industry is primarily led by well-established companies, including:

- Sanofi (France)

- GSK plc (U.K.)

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Amgen Inc. (U.S.)

- AstraZeneca (U.K.)

- OptiNose US, Inc. (U.S.)

- Intersect ENT, Inc. (U.S.)

- Teva Pharmaceuticals (Israel)

- F. Hoffmann‑La Roche Ltd. (Switzerland)

- Merck & Co., Inc. (U.S.)

- Keymed Biosciences, Inc. (U.S.)

- Biohaven Pharmaceuticals, Inc. (U.S.)

- Guangdong Hengrui Pharmaceutical Co., Ltd. (China)

- Upstream Bio, Inc. (U.S.)

- Sunshine Guojian Pharmaceutical Co., Ltd. (China)

- Genrix Biotherapeutics (China)

- Chia Tai Tianqing Pharmaceutical Group Co., Ltd. (China)

What are the Recent Developments in Global Nasal Polyposis Drugs Market?

- In October 2025, the U.S. FDA approved TEZSPIRE® (tezepelumab‑ekko) as a new biologic therapy for chronic rhinosinusitis with nasal polyps (CRSwNP) offering a novel mechanism of action by targeting thymic stromal lymphopoietin (TSLP) to significantly reduce polyp severity and decrease surgery/steroid requirements, marking a major advancement beyond existing treatments

- In June 2025, Dupixent® (dupilumab) demonstrated superiority over Xolair® (omalizumab) in a first‑ever head‑to‑head Phase 4 trial for CRSwNP with coexisting asthma, showing better outcomes on nasal polyp size, sense of smell, and asthma control, which could influence prescribing choices for biologics in complex cases

- In January 2025, GSK’s Nucala® (mepolizumab) received regulatory approval in China for the treatment of adults with CRSwNP, providing a new biologic option in one of the world’s largest markets and expanding treatment access beyond Western regions

- In September 2024, the U.S. FDA expanded approval for Dupixent® to include treatment of adolescents (ages 12–17) with inadequately controlled chronic rhinosinusitis with nasal polyps, making a leading biologic available to younger patients and broadening the addressable patient base

- In July 2021 (relevant baseline for market evolution), the FDA first approved Nucala (mepolizumab) for chronic rhinosinusitis with nasal polyps in adults, establishing the first IL‑5 targeted biologic for nasal polyps and laying groundwork for subsequent biologic competition and treatment diversification

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.