Global Neonatal Jaundice Management Market

Market Size in USD Million

USD

425.85 Million

USD

715.43 Million

2024

2032

USD

425.85 Million

USD

715.43 Million

2024

2032

| 2025 - 2032 | |

| USD 425.85 Million | |

| USD 715.43 Million | |

| % | |

|

Neonatal Jaundice Management Market Size

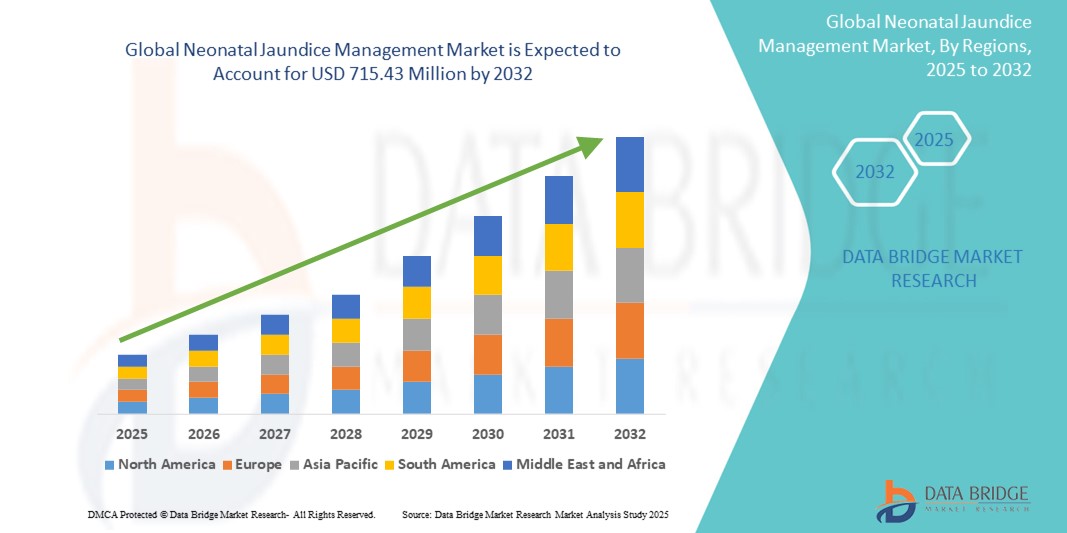

- The global neonatal jaundice management market size was valued at USD 425.85 million in 2024 and is expected to reach USD 715.43 million by 2032, at a CAGR of 6.70% during the forecast period

- The market growth is primarily driven by the increasing prevalence of neonatal jaundice worldwide, coupled with a rising awareness among healthcare providers and parents about early diagnosis and effective treatment solutions

- In addition, advancements in phototherapy technologies, enhanced diagnostic tools, and government initiatives focused on neonatal care are contributing to the wider adoption of jaundice management systems in hospitals and homecare settings

Neonatal Jaundice Management Market Analysis

- Neonatal jaundice management, encompassing phototherapy devices and diagnostic tools, is a critical component of neonatal care aimed at reducing elevated bilirubin levels in newborns to prevent severe complications such as kernicterus and neurological damage

- The rising demand for neonatal jaundice management solutions is driven by increasing birth rates, heightened awareness of early jaundice detection, and the growing prevalence of neonatal hyperbilirubinemia, especially in developing regions with limited access to advanced care

- North America dominated the neonatal jaundice management market with the largest revenue share of 39.5% in 2024, attributed to strong healthcare infrastructure, favorable reimbursement policies, and the early adoption of innovative phototherapy technologies in neonatal intensive care units (NICUs), particularly in the U.S.

- Asia-Pacific is projected to witness the fastest growth in the the neonatal jaundice management market, during the forecast period, supported by government investments in maternal and child healthcare, rising healthcare expenditures, and increasing access to affordable phototherapy devices in countries such as India and China

- Treatment segment dominated the neonatal jaundice management market with a market share of 64.8% in 2024, driven by its critical role in reducing bilirubin levels through phototherapy and exchange transfusion, which are essential for preventing severe complications

Report Scope and Neonatal Jaundice Management Market Segmentation

|

Attributes |

Neonatal Jaundice Management Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Neonatal Jaundice Management Market Trends

“Technological Advancements in Phototherapy and Diagnostic Solutions”

- A significant and advancing trend in the global neonatal jaundice management market is the integration of cutting-edge technologies in phototherapy and diagnostic devices, enhancing treatment outcomes and enabling early, non-invasive detection of hyperbilirubinemia

- For instance, GE Healthcare’s BiliSoft LED phototherapy system delivers high-intensity treatment with minimal heat generation, ensuring safer and more effective therapy for newborns. Similarly, the Dräger JM-105 bilirubinometer provides instant, non-invasive bilirubin level readings, supporting early diagnosis without repeated blood sampling

- These innovations are improving clinical efficiency while reducing discomfort and hospitalization time, particularly in NICUs and home care settings

- Compact and portable phototherapy devices are being adopted across low-resource settings, expanding access to jaundice care in rural and underserved regions

- This trend toward smarter, more accessible jaundice management solutions is transforming neonatal care, especially in countries with growing investments in maternal and child health programs

- As demand grows for safe, cost-effective, and technologically advanced treatment, companies are developing user-friendly, portable devices to meet the needs of both hospitals and home users globally

Neonatal Jaundice Management Market Dynamics

Driver

“Rising Prevalence of Neonatal Hyperbilirubinemia and Focus on Early Intervention”

- The growing incidence of neonatal jaundice, particularly among premature and low birth weight infants, is a major factor driving the demand for effective jaundice management solutions

- For instance, the World Health Organization (WHO) estimates that over 60% of term and 80% of preterm infants develop jaundice in the first week of life, necessitating timely diagnosis and treatment

- Rising awareness among parents and healthcare providers, coupled with national programs promoting neonatal screening, is boosting the uptake of diagnostic and phototherapy solutions

- Hospitals and healthcare facilities are increasingly equipping NICUs with advanced treatment technologies to ensure safe and prompt management of jaundice, improving neonatal survival and reducing complications

- In addition, the adoption of home-based phototherapy units and telemedicine follow-ups is enhancing access to care, especially in remote and underserved regions

Restraint/Challenge

“Limited Access in Low-Income Regions and High Equipment Costs”

- Limited access to neonatal care infrastructure in low- and middle-income countries poses a key challenge for the widespread adoption of jaundice management solutions

- For instance, many rural clinics lack reliable electricity, trained healthcare staff, and essential medical devices, resulting in delayed or inadequate treatment of neonatal jaundice

- Furthermore, the high cost of advanced phototherapy equipment and bilirubin monitoring systems, such as LED-based units, remains a barrier for smaller hospitals and public health facilities with constrained budgets

- Although cost-effective models are emerging, affordability and long-term maintenance remain concerns that hinder broader implementation in resource-poor settings

- Addressing these challenges through international health collaborations, subsidies, and the development of low-cost, durable technologies is essential to expanding access and improving neonatal outcomes worldwide

Neonatal Jaundice Management Market Scope

The market is segmented on the basis of management, type, technology, end user, and distribution channel.

- By Management

On the basis of management, the neonatal jaundice management market is segmented into diagnosis and treatment. The treatment segment dominated the market with the largest market revenue share of 64.8% in 2024, driven by the widespread use of phototherapy as the primary intervention to reduce elevated bilirubin levels in newborns. The increasing adoption of LED phototherapy units in hospitals and home care settings further strengthens the dominance of this segment.

The diagnosis segment is expected to witness the fastest CAGR from 2025 to 2032, supported by advancements in non-invasive bilirubin monitoring technologies such as transcutaneous bilirubinometers, which reduce the need for blood draws and enable early detection in both clinical and home environments.

- By Type

On the basis of type, the market is segmented into primary care and secondary care. The secondary care segment held the largest market share of 58.6% in 2024, owing to the concentration of advanced treatment and monitoring systems in specialized hospital units and NICUs. These settings are better equipped to manage moderate to severe jaundice cases using phototherapy and exchange transfusion.

The primary care segment is expected to witness the fastest CAGR from 2025 to 2032, as rural health clinics and local health centers expand their neonatal screening capabilities, supported by government health initiatives and mobile healthcare services.

- By Technology

On the basis of technology, the market is segmented into light-emitting diode (LED) light sources, fluorescent, halogen, and fiberoptic.The LED light sources segment dominated the market with a 51.8% share in 2024, attributed to their superior clinical efficacy, energy efficiency, longer operational life, and minimal heat emission, making them safer for newborns.

The fiberoptic segment is expected to witness the fastest CAGR from 2025 to 2032, driven by its application in portable and wearable phototherapy devices that allow treatment without separating the infant from the mother, enhancing maternal-infant bonding during therapy.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, ambulatory surgical centers, home users, and others. The hospital segment was the dominant end user in 2024, accounting for 60.2% of the market, owing to the widespread availability of NICUs and trained healthcare professionals, along with access to comprehensive diagnostic and treatment infrastructure.

The home users segment is expected to witness the fastest CAGR from 2025 to 2032, due to the increasing availability of compact and user-friendly phototherapy units, which enable early-stage jaundice management at home under medical supervision.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and third-party distribution. The direct tender segment accounted for the highest market share of 45.9% in 2024, largely driven by bulk purchasing by public hospitals, government health agencies, and large private healthcare institutions through tender-based procurement models.

The retail sales segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the increasing availability of home-use diagnostic and treatment devices through e-commerce platforms and medical supply stores, catering to both healthcare providers and individual consumers.

Neonatal Jaundice Management Market Regional Analysis

- North America dominated the neonatal jaundice management market with the largest revenue share of 39.5% in 2024, attributed to strong healthcare infrastructure, favorable reimbursement policies, and the early adoption of innovative phototherapy technologies in neonatal intensive care units (NICUs), particularly in the U.S.

- Healthcare providers in the region emphasize early intervention and non-invasive monitoring, utilizing modern devices that enhance neonatal outcomes while reducing hospitalization times

- This widespread adoption is further supported by favorable reimbursement policies, high healthcare expenditure, and ongoing investments in neonatal and maternal care programs, positioning the region as a leader in technological adoption and quality standards in neonatal jaundice management

U.S. Neonatal Jaundice Management Market Insight

The U.S. neonatal jaundice management market captured the largest revenue share of 79.5% in North America in 2024, driven by its advanced healthcare infrastructure and strong emphasis on early neonatal screening and intervention. Hospitals across the U.S. widely implement LED phototherapy systems and non-invasive bilirubin meters, ensuring high standards in neonatal care. The presence of major medical device manufacturers and favorable reimbursement frameworks further strengthen the market, while growing awareness among parents and pediatricians continues to support early diagnosis and effective treatment.

Europe Neonatal Jaundice Management Market Insight

The Europe neonatal jaundice management market is projected to expand at a steady CAGR throughout the forecast period, fueled by increasing government initiatives focused on maternal and infant health. Rising investments in neonatal intensive care units and the adoption of advanced phototherapy technologies are key contributors. The region’s regulatory emphasis on quality and safety, along with strong public health systems, supports widespread deployment of modern jaundice treatment solutions across both urban hospitals and regional care centers.

U.K. Neonatal Jaundice Management Market Insight

The U.K. neonatal jaundice management market is anticipated to grow at a notable CAGR during the forecast period, supported by a strong public healthcare system and rising demand for early neonatal interventions. The National Health Service (NHS) emphasizes routine screening for jaundice, and hospitals are increasingly adopting advanced phototherapy units and non-invasive diagnostic devices. Public health campaigns and training programs for healthcare providers also contribute to enhanced care outcomes for newborns affected by jaundice.

Germany Neonatal Jaundice Management Market Insight

The Germany neonatal jaundice management market is expected to expand at a significant CAGR, propelled by the country’s focus on high-quality neonatal care and continuous investment in healthcare technology. German hospitals are early adopters of LED phototherapy systems and portable bilirubinometers, ensuring comprehensive care even in decentralized healthcare settings. Strong demand for clinically validated, eco-friendly, and efficient devices aligns with the country’s commitment to sustainability and technological precision in the medical field.

Asia-Pacific Neonatal Jaundice Management Market Insight

The Asia-Pacific neonatal jaundice management market is projected to grow at the fastest CAGR of 23.1% from 2025 to 2032, driven by high birth rates, expanding healthcare access, and increasing investments in maternal and child health across countries such as India, China, and Indonesia. Government-backed programs promoting neonatal screening and care are fostering demand for affordable phototherapy and diagnostic equipment. Local manufacturing capabilities are also improving the availability of cost-effective, portable solutions, enabling broader adoption in rural and underserved regions.

Japan Neonatal Jaundice Management Market Insight

The Japan neonatal jaundice management market is advancing steadily due to the country’s cutting-edge healthcare infrastructure and technological innovation. Japanese hospitals utilize high-precision phototherapy and bilirubin monitoring devices, ensuring timely and effective treatment. The aging population's concern for neonatal health, along with policy-driven hospital modernization, supports continuous investment in neonatal care equipment, especially those that offer minimal invasiveness and high treatment efficiency.

India Neonatal Jaundice Management Market Insight

The India neonatal jaundice management market held the largest revenue share in Asia-Pacific in 2024, attributed to its large neonatal population, improving healthcare infrastructure, and rising awareness of early neonatal care. Initiatives such as the National Health Mission and growing private healthcare investments are increasing access to affordable phototherapy and diagnostic devices. The presence of domestic manufacturers and public-private partnerships is also boosting market expansion, particularly in tier 2 and rural regions.

Neonatal Jaundice Management Market Share

The neonatal jaundice management industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Natus Medical Incorporated (U.S.)

- Draegerwerk AG & Co. KGaA (Germany)

- Koninklijke Philips N.V., (Netherlands)

- Atom Medical Corp. (Japan)

- AVI Healthcare Pvt. Ltd. (India)

- Weyer GmbH (Germany)

- Phoenix Medical Systems Pvt. Ltd. (India)

- Nice Neotech Medical Systems Pvt. Ltd. (India)

- Fanem Ltda. (Brazil)

- MTTS (Vietnam)

- Zhengzhou Dison Instrument and Meter Co., Ltd. (China)

- David Medical Device Co., Ltd. (China)

- Kay & Company (India)

- Ameda Inc. (U.S.)

- Signify Holding (Netherlands)

- Ibis Medical Equipment & Systems Pvt. Ltd. (India)

- Novos Medical Systems (India)

- Heal Force Bio-Meditech Holdings Limited (China)

- Shvabe JSC (Russia)

What are the Recent Developments in Global Neonatal Jaundice Management Market?

- In March 2024, GE HealthCare announced the global expansion of its BiliSoft 3.0 Phototherapy System, an advanced LED-based solution designed to offer effective treatment for neonatal jaundice while maximizing infant comfort and caregiver convenience. The system includes enhanced portability and reduced light scatter, making it more efficient in both hospital and home settings. This launch demonstrates GE HealthCare’s ongoing commitment to improving neonatal outcomes through innovative, non-invasive therapeutic solutions

- In February 2024, Draegerwerk AG & Co. KGaA introduced a next-generation transcutaneous bilirubin meter, JM-300, aimed at delivering fast, accurate, and non-invasive bilirubin assessments. The device is designed for point-of-care use in hospitals and clinics, supporting early diagnosis and reducing the need for invasive blood sampling. This advancement reflects Draeger’s strategic focus on enhancing diagnostic precision in neonatal care through smart, patient-friendly technologies

- In January 2024, Philips Healthcare partnered with a regional government health initiative in Southeast Asia to pilot its Mother & Baby Care Program, incorporating smart neonatal jaundice screening tools in rural healthcare centers. The initiative aims to expand access to early detection and timely treatment in low-resource settings. By integrating portable bilirubin meters and LED phototherapy devices, Philips is addressing regional disparities in neonatal healthcare access

- In December 2023, Natus Medical Incorporated expanded its product line by launching neoBLUE compact, a cost-effective and space-saving phototherapy device tailored for both hospital and home use. With LED technology that delivers consistent irradiance, the device meets global treatment standards while addressing the growing demand for affordable neonatal care solutions in emerging markets

- In November 2023, Nice Neotech Medical Systems Pvt. Ltd., a key player in India’s neonatal equipment market, unveiled a new portable Dual Surface LED Phototherapy System. The device is designed to provide intensive treatment in NICUs and rural clinics, enabling quicker bilirubin breakdown from both sides of the infant’s body. This development underscores the company’s focus on innovation tailored to regional needs and the ongoing expansion of neonatal care in developing countries.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATION

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 KEY TAKEAWAYS

2.2 MARKETS COVERED

2.3 GEOGRAPHICAL SCOPE

2.4 ARRIVING AT THE GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET SIZE

2.4.1 VENDOR POSITIONING GRID

2.4.2 MANAGEMENT LIFE LINE CURVE

2.4.3 TRIPOD DATA VALIDATION MODEL

2.4.4 MARKET GUIDE

2.4.5 MULTIVARIATE MODELLING

2.4.6 TOP TO BOTTOM ANALYSIS

2.4.7 CHALLENGE MATRIX

2.4.8 APPLICATION COVERAGE GRID

2.4.9 STANDARDS OF MEASUREMENT

2.4.10 VENDOR SHARE ANALYSIS

2.4.11 DATA POINTS FROM KEY PRIMARY INTERVIEWS

2.4.12 DATA POINTS FROM KEY SECONDARY DATABASES

2.5 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET: RESEARCH SNAPSHOT

2.6 ASSUMPTIONS

3 MARKET OVERVIEW

3.1 DRIVERS

3.1.1 RISING PATIENT POPULATION SUFFERING FROM NEONATAL JAUNDICE

3.1.2 LARGE NUMBER OF RISK FACTORS

3.1.3 RISING NUMBER OF NEW-BORN INFANTS

3.1.4 INCREASE IN PRETERM BIRTH

3.1.5 AWARENESS ABOUT NEONATAL JAUNDICE AMONG THE POPULATION

3.2 RESTRAINTS

3.2.1 SIDE-EFFECTS RELATED TO PHOTOTHERAPY

3.2.2 PRODUCT RECALLS

3.2.3 LIMITED ADOPTION OF NEONATAL JAUNDICE MANAGEMENT

3.3 OPPORTUNITIES

3.3.1 INCREASING HEALTHCARE EXPENDITURE

3.3.2 TECHNOLOGICAL ADVANCEMENT IN DIAGNOSIS AND TREATMENT

3.3.3 INCREASING DISPOSABLE INCOME

3.3.4 INCREASE IN AGREEMENTS AND ACQUISITIONS

3.4 CHALLENGES

3.4.1 COMPLICATIONS RELATED TO NEONATAL JAUNDICE

3.4.2 LACK OF SKILLED PROFESSIONALS

3.4.3 DIAGNOSIS OF NEONATAL JAUNDICE

4 EXECUTIVE SUMMARY

5 PREMIUM INSIGHTS

6 INDUSTRY INSIGHTS

7 REGULATORY FRAMWORK

8 IMPACT OF COVID-19 PANDEMIC ON THE MARKET

8.1 PRICE IMPACT

8.2 IMPACT ON DEMAND

8.3 IMPACT ON SUPPLY CHAIN

8.4 STRATEGIC DECISION FOR MANUFACTURER/SERVICE PROVIDER

8.5 CONCLUSION

9 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET, BY MANAGEMENT

9.1 OVERVIEW

9.2 DIAGNOSIS

9.2.1 TRANSCUTANEOUS BILIRUBINOMETER (TCB)

9.2.2 TOTAL SERUM BILIRUBIN (TSB)

9.2.3 VISUAL ASSESSMENT

9.3 TREATMENT

9.3.1 PHOTOTHERAPY

9.3.1.1. LED PHOTOTHERAPY

9.3.1.2. FIBREOPTIC PHOTOTHERAPY

9.3.1.3. CONVENTIONAL PHOTOTHERAPY

9.3.1.3.1. CONVENTIONAL PHOTOTHERAPY WITH COMPACT FLUORESCENT LAMP

9.3.1.3.2. CONVENTIONAL PHOTOTHERAPY WITH FLUORESCENT LAMP

9.3.1.3.2.1 FULL-BODY PHOTOTHERAPY

9.3.1.3.2.2 PARTIAL-BODY PHOTOTHERAPY

9.3.1.3.3. EXCHANGE TRANSFUSION

9.3.1.3.4. INTRAVENOUS IMMUNOGLOBULIN

9.3.1.3.5. OTHERS

10 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET, BY TYPE

10.1 OVERVIEW

10.2 PRIMARY CARE

10.3 SEODNARY CARE

11 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET, BY TECHNOLOGY

11.1 OVERVIEW

11.2 FLUORESCENT

11.3 HALOGEN

11.4 FIBEROPTIC

11.5 LIGHT-EMITTING DIODE LIGHT SOURCES

11.6 OTHERS

12 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET, BY END USER

12.1 OVERVIEW

12.2 HOSPITALS

12.3 CLINICS

12.4 AMBULATORY SURGICAL CENTERS

12.5 HOME USERS

12.6 OTHERS

13 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET, BY DISTRIBUTION CHANNEL

13.1 OVERVIEW

13.2 DIRECT TENDERS

13.3 RETAIL SALES

13.4 THIRD PARTY DISTRIBUTION

14 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET, BY COUNTRY

14.1 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET (ALL SEGMENTATION PROVIDED ABOVE IS REPRESENTED IN THIS CHAPTER BY COUNTRY)

14.1.1 NORTH AMERICA

14.1.1.1. U.S.

14.1.1.2. CANADA

14.1.1.3. MEXICO

14.1.2 EUROPE

14.1.2.1. GERMANY

14.1.2.2. U.K.

14.1.2.3. FRANCE

14.1.2.4. ITALY

14.1.2.5. SPAIN

14.1.2.6. NETHERLANDS

14.1.2.7. RUSSIA

14.1.2.8. SWITZERLAND

14.1.2.9. TURKEY

14.1.2.10. REST OF EUROPE

14.1.3 ASIA-PACIFIC

14.1.3.1. CHINA

14.1.3.2. JAPAN

14.1.3.3. INDIA

14.1.3.4. AUSTRALIA

14.1.3.5. SOUTH KOREA

14.1.3.6. SINGAPORE

14.1.3.7. MALAYSIA

14.1.3.8. THAILAND

14.1.3.9. INDONESIA

14.1.3.10. PHILIPPINES

14.1.3.11. REST OF ASIA-PACIFIC

14.1.4 SOUTH AMERICA

14.1.4.1. BRAZIL

14.1.4.2. ARGENTINA

14.1.4.3. REST OF SOUTH AMERICA

14.1.5 MIDDLE EAST AND AFRICA

14.1.5.1. SOUTH AFRICA

14.1.5.2. SAUDI ARABIA

14.1.5.3. UAE

14.1.5.4. EGYPT

14.1.5.5. ISRAEL

14.1.5.6. REST OF MIDDLE EAST AND AFRICA

14.1.6 KEY PRIMARY INSIGHTS: BY MAJOR COUNTRIES

15 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET, COMPANY LANDSCAPE

15.1 COMPANY SHARE ANALYSIS: GLOBAL

15.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

15.3 COMPANY SHARE ANALYSIS: EUROPE

15.4 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

15.5 MERGERS & ACQUISITIONS

15.6 NEW PRODUCT DEVELOPMENT & APPROVALS

15.7 EXPANSIONS

15.8 REGULATORY CHANGES

15.9 PARTNERSHIP AND OTHER STRATEGIC DEVELOPMENTS

16 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET, SWOT AND DBR ANALYSIS

17 GLOBAL NEONATAL JAUNDICE MANAGEMENT MARKET, COMPANY PROFILE

17.1 DRÄGERWERK AG & CO. KGAA,

17.1.1 COMPANY OVERVIEW

17.1.2 REVENUE ANALYSIS

17.1.3 GEOGRAPHIC PRESENCE

17.1.4 PRODUCT PORTFOLIO

17.1.5 RECENT DEVELOPMENTS

17.2 ATOM MEDICAL CORP

17.2.1 COMPANY OVERVIEW

17.2.2 REVENUE ANALYSIS

17.2.3 GEOGRAPHIC PRESENCE

17.2.4 PRODUCT PORTFOLIO

17.2.5 RECENT DEVELOPMENTS

17.3 MTTS

17.3.1 COMPANY OVERVIEW

17.3.2 REVENUE ANALYSIS

17.3.3 GEOGRAPHIC PRESENCE

17.3.4 PRODUCT PORTFOLIO

17.3.5 RECENT DEVELOPMENTS

17.4 PHOENIX MEDICAL SYSTEMS PVT. LTD

17.4.1 COMPANY OVERVIEW

17.4.2 REVENUE ANALYSIS

17.4.3 GEOGRAPHIC PRESENCE

17.4.4 PRODUCT PORTFOLIO

17.4.5 RECENT DEVELOPMENTS

17.5 AVIHEALTHCARE

17.5.1 COMPANY OVERVIEW

17.5.2 REVENUE ANALYSIS

17.5.3 GEOGRAPHIC PRESENCE

17.5.4 PRODUCT PORTFOLIO

17.5.5 RECENT DEVELOPMENTS

17.6 IBIS MEDICAL

17.6.1 COMPANY OVERVIEW

17.6.2 REVENUE ANALYSIS

17.6.3 GEOGRAPHIC PRESENCE

17.6.4 PRODUCT PORTFOLIO

17.6.5 RECENT DEVELOPMENTS

17.7 NATUS MEDICAL INCORPORATED

17.7.1 COMPANY OVERVIEW

17.7.2 REVENUE ANALYSIS

17.7.3 GEOGRAPHIC PRESENCE

17.7.4 PRODUCT PORTFOLIO

17.7.5 RECENT DEVELOPMENTS

17.8 NINGBO DAVID MEDICAL DEVICE CO., LTD

17.8.1 COMPANY OVERVIEW

17.8.2 REVENUE ANALYSIS

17.8.3 GEOGRAPHIC PRESENCE

17.8.4 PRODUCT PORTFOLIO

17.8.5 RECENT DEVELOPMENTS

17.9 WEYER GMBH

17.9.1 COMPANY OVERVIEW

17.9.2 REVENUE ANALYSIS

17.9.3 GEOGRAPHIC PRESENCE

17.9.4 PRODUCT PORTFOLIO

17.9.5 RECENT DEVELOPMENTS

17.1 SOLARC SYSTEMS INC.,

17.10.1 COMPANY OVERVIEW

17.10.2 REVENUE ANALYSIS

17.10.3 GEOGRAPHIC PRESENCE

17.10.4 PRODUCT PORTFOLIO

17.10.5 RECENT DEVELOPMENTS

17.11 GE HEALTHCARE

17.11.1 COMPANY OVERVIEW

17.11.2 REVENUE ANALYSIS

17.11.3 GEOGRAPHIC PRESENCE

17.11.4 PRODUCT PORTFOLIO

17.11.5 RECENT DEVELOPMENTS

17.12 PHILIPS LIGHTING HOLDING B.V.

17.12.1 COMPANY OVERVIEW

17.12.2 REVENUE ANALYSIS

17.12.3 GEOGRAPHIC PRESENCE

17.12.4 PRODUCT PORTFOLIO

17.12.5 RECENT DEVELOPMENTS

17.13 IHR. LTD.

17.13.1 COMPANY OVERVIEW

17.13.2 REVENUE ANALYSIS

17.13.3 GEOGRAPHIC PRESENCE

17.13.4 PRODUCT PORTFOLIO

17.13.5 RECENT DEVELOPMENTS

17.14 ZHENGZHOU DISON INSTRUMENT AND METER CO., LTD

17.14.1 COMPANY OVERVIEW

17.14.2 REVENUE ANALYSIS

17.14.3 GEOGRAPHIC PRESENCE

17.14.4 PRODUCT PORTFOLIO

17.14.5 RECENT DEVELOPMENTS

17.15 HERBERT WALDMANN GMBH & CO. KG

17.15.1 COMPANY OVERVIEW

17.15.2 REVENUE ANALYSIS

17.15.3 GEOGRAPHIC PRESENCE

17.15.4 PRODUCT PORTFOLIO

17.15.5 RECENT DEVELOPMENTS

17.16 NICE NEOTECH MEDICAL SYSTEMS PVT. LTD.

17.16.1 COMPANY OVERVIEW

17.16.2 REVENUE ANALYSIS

17.16.3 GEOGRAPHIC PRESENCE

17.16.4 PRODUCT PORTFOLIO

17.16.5 RECENT DEVELOPMENTS

17.17 GINEVRI SRL

17.17.1 COMPANY OVERVIEW

17.17.2 REVENUE ANALYSIS

17.17.3 GEOGRAPHIC PRESENCE

17.17.4 PRODUCT PORTFOLIO

17.17.5 RECENT DEVELOPMENTS

17.18 NEOLIGHT LLC

17.18.1 COMPANY OVERVIEW

17.18.2 REVENUE ANALYSIS

17.18.3 GEOGRAPHIC PRESENCE

17.18.4 PRODUCT PORTFOLIO

17.18.5 RECENT DEVELOPMENTS

17.19 S S TECHNOMED (P) LTD

17.19.1 COMPANY OVERVIEW

17.19.2 REVENUE ANALYSIS

17.19.3 GEOGRAPHIC PRESENCE

17.19.4 PRODUCT PORTFOLIO

17.19.5 RECENT DEVELOPMENTS

17.2 SHVABE‑ZURICH GMBH

17.20.1 COMPANY OVERVIEW

17.20.2 REVENUE ANALYSIS

17.20.3 GEOGRAPHIC PRESENCE

17.20.4 PRODUCT PORTFOLIO

17.20.5 RECENT DEVELOPMENTS

NOTE: THE COMPANIES PROFILED IS NOT EXHAUSTIVE LIST AND IS AS PER OUR PREVIOUS CLIENT REQUIREMENT. WE PROFILE MORE THAN 100 COMPANIES IN OUR STUDY AND HENCE THE LIST OF COMPANIES CAN BE MODIFIED OR REPLACED ON REQUEST RELATED REPORTS

18 CONCLUSION

19 QUESTIONNAIRE

20 ABOUT DATA BRIDGE MARKET RESEARCH

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.