Global Neutropenia Market

Market Size in USD Billion

USD

16.35 Billion

USD

25.09 Billion

2025

2033

USD

16.35 Billion

USD

25.09 Billion

2025

2033

| 2026 - 2033 | |

| USD 16.35 Billion | |

| USD 25.09 Billion | |

| % | |

|

Neutropenia Market Size

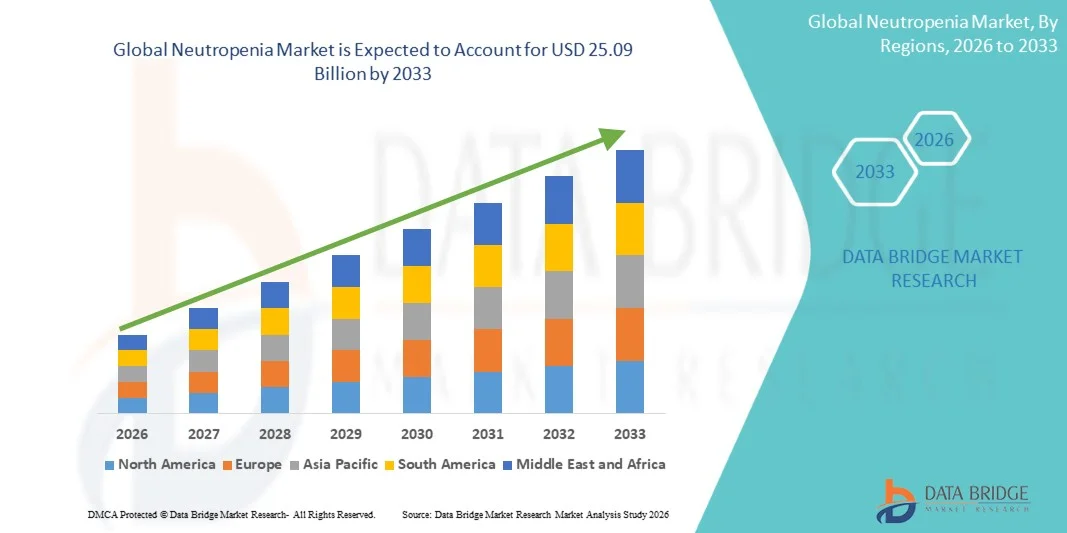

- The global neutropenia market size was valued at USD 16.35 billion in 2025 and is expected to reach USD 25.09 billion by 2033, at a CAGR of 5.50% during the forecast period

- The market growth is primarily driven by increasing prevalence of neutropenia-inducing conditions, such as chemotherapy-related neutropenia, congenital disorders, and autoimmune diseases, combined with rising awareness and early diagnosis efforts among healthcare providers

- Furthermore, advancements in biologic therapies, granulocyte colony-stimulating factors (G-CSFs), and supportive care treatments, along with growing demand for patient-specific and hospital-based management solutions, are positioning neutropenia therapeutics as a critical component of modern hematology care. These converging factors are accelerating the adoption of effective neutropenia treatments, thereby significantly boosting the industry's growth

Neutropenia Market Analysis

- Neutropenia, characterized by abnormally low neutrophil counts, is increasingly recognized as a critical hematological condition due to its association with heightened infection risk, chemotherapy complications, and prolonged hospitalizations in both adult and pediatric patients.

- The escalating demand for neutropenia management is primarily fueled by the rising prevalence of chemotherapy-induced and congenital neutropenia, growing awareness among healthcare providers, and increasing adoption of advanced therapeutic interventions

- North America dominated the neutropenia market with the largest revenue share of 42.5% in 2025, supported by advanced healthcare infrastructure, high adoption of colony-stimulating factor therapies, strong presence of key pharmaceutical players, and extensive clinical awareness programs

- Asia-Pacific is expected to be the fastest-growing region in the neutropenia market during the forecast period due to rising cancer prevalence, expanding healthcare access, and increasing adoption of supportive therapies such as antibiotic therapy and granulocyte transfusions

- Congenital neutropenia segment dominated the market with a share of 38.7% in 2025, driven by early diagnosis, genetic testing availability, and targeted treatment options

Report Scope and Neutropenia Market Segmentation

|

Attributes |

Neutropenia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Neutropenia Market Trends

“Advancements in Biologic and Colony-Stimulating Factor Therapies”

- A significant and accelerating trend in the global neutropenia market is the development and adoption of advanced biologic therapies, particularly colony-stimulating factors (G-CSFs), which enhance neutrophil production and reduce infection risks

- For instance, filgrastim biosimilars now allow hospitals and clinics to provide more cost-effective therapy options while maintaining efficacy, improving patient access to critical treatments

- These therapies are being optimized for personalized regimens based on patient-specific risk profiles, enabling more targeted treatment plans and better outcomes. For instance, pegfilgrastim formulations with extended half-lives allow fewer injections while maintaining therapeutic efficacy

- The integration of biologics with supportive care protocols, such as antibiotic prophylaxis and hospitalization monitoring, facilitates a comprehensive approach to neutropenia management, improving overall patient quality of life

- This trend towards precision medicine and biologic optimization is reshaping expectations for neutropenia care. Consequently, companies such as Amgen and Teva are developing next-generation G-CSF therapies with improved dosing convenience and safety profiles

- The demand for advanced, patient-tailored neutropenia treatments is growing rapidly across both oncology and hematology segments, as healthcare providers prioritize reducing infection-related complications and hospital stays

- Increasing collaboration between pharmaceutical companies and hospitals for clinical trials and early-access programs is further accelerating innovation in neutropenia therapies

Neutropenia Market Dynamics

Driver

“Increasing Prevalence of Chemotherapy-Induced and Congenital Neutropenia”

- The rising incidence of chemotherapy-induced neutropenia among cancer patients, combined with growing detection of congenital and autoimmune neutropenia disorders, is a significant driver for increased demand for neutropenia therapies

- For instance, in March 2025, Amgen expanded access programs for pegfilgrastim in outpatient oncology clinics, aiming to reduce infection-related complications during chemotherapy cycles

- As healthcare providers become more aware of infection risks and treatment protocols, neutropenia therapies such as G-CSFs, antibiotic prophylaxis, and granulocyte transfusions are increasingly integrated into standard care

- Furthermore, the growing oncology patient population and rising cancer incidence worldwide are making neutropenia management an essential part of modern treatment protocols, particularly in developed and emerging regions

- The convenience of outpatient administration, improved adherence with extended dosing schedules, and availability of patient-friendly formulations are key factors propelling the adoption of neutropenia therapies in both hospital and home-care settings

- The trend towards accessible and effective neutropenia management programs, supported by innovations in biologics and patient monitoring, further contributes to market growth

- Increasing governmental initiatives and healthcare reimbursement programs targeting supportive care for oncology patients are driving broader adoption of neutropenia therapies

- Rising awareness campaigns and educational programs among oncologists and hematologists regarding infection risk reduction strategies are encouraging early intervention and treatment uptake

Restraint/Challenge

“High Treatment Costs and Limited Access in Emerging Markets”

- Concerns surrounding the high cost of biologic therapies, including G-CSFs and granulocyte transfusions, pose a significant challenge to broader market penetration, particularly in price-sensitive regions

- For instance, filgrastim therapy may remain inaccessible to some patients in developing countries due to reimbursement limitations and high out-of-pocket costs

- Ensuring equitable access through biosimilars, patient assistance programs, and insurance coverage is crucial for expanding adoption, particularly for chronic or high-risk neutropenia patients. For instance, Teva’s biosimilar G-CSF programs aim to address affordability issues while maintaining clinical efficacy

- In addition, the complexity of treatment protocols, including proper dosing, monitoring, and administration routes, can create barriers for both healthcare providers and patients, slowing widespread uptake

- While overall awareness and availability are improving, the perceived high cost of therapy and logistical challenges in treatment delivery can hinder adoption, especially in rural or under-resourced areas

- Overcoming these challenges through cost-reduction strategies, expanded biosimilar adoption, and healthcare provider training will be vital for sustained market growth

- Regulatory approvals and variations in clinical guidelines across regions may delay product launches and limit market expansion for new therapies

- Limited infrastructure for home-based administration of injectable therapies, especially in emerging economies, can restrict patient access and treatment continuity

Neutropenia Market Scope

The market is segmented on the basis of type, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the neutropenia market is segmented into congenital neutropenia, idiopathic neutropenia, cyclic neutropenia, autoimmune neutropenia, and others. The congenital neutropenia segment dominated the market with the largest market revenue share of 38.7% in 2025, driven by the early diagnosis through genetic testing and awareness of long-term infection risks in pediatric and adult patients. Hospitals and specialty clinics often prioritize treatment plans for congenital neutropenia using colony-stimulating factors to prevent severe infections. The segment’s dominance is also supported by ongoing research and clinical trials focused on novel therapies, improving patient outcomes. Availability of patient support programs and early intervention strategies further boosts adoption. In addition, congenital neutropenia patients typically require continuous monitoring and supportive care, reinforcing the demand for established treatment protocols. The segment also benefits from high adoption in developed regions with advanced healthcare infrastructure.

The autoimmune neutropenia segment is anticipated to witness the fastest growth rate of 20.5% from 2026 to 2033, fueled by increasing diagnosis of immune-mediated neutropenia in adults and children. Rising awareness among hematologists and general practitioners regarding autoimmune causes of neutropenia is driving early treatment adoption. Novel immunomodulatory therapies and improved supportive care are expanding treatment options for this segment. Autoimmune neutropenia often requires personalized treatment plans, increasing demand for specialized therapies and monitoring services. The prevalence of autoimmune conditions globally, along with improved laboratory diagnostic capabilities, supports market expansion. Growing research initiatives and emerging biologics targeting autoimmune mechanisms are expected to accelerate growth in this subsegment.

- By Treatment

On the basis of treatment, the neutropenia market is segmented into antibiotic therapy, colony-stimulating factor therapy, granulocyte transfusion, splenectomy procedure, and others. Colony-stimulating factor therapy dominated the market with the largest market revenue share of 44.1% in 2025, driven by its proven efficacy in stimulating neutrophil production and reducing infection-related complications in chemotherapy-induced and congenital neutropenia. Hospitals and outpatient clinics rely on these therapies to minimize hospitalization and improve patient recovery. The segment’s dominance is further strengthened by the availability of biosimilars, which reduce costs and increase patient access. Extended-release and pegylated formulations allow fewer injections and improve patient compliance. Pharmaceutical companies actively invest in new G-CSF formulations, enhancing safety and convenience. Furthermore, clinician familiarity and well-established clinical guidelines reinforce its leading market position.

Granulocyte transfusion therapy is expected to witness the fastest CAGR from 2026 to 2033, driven by its critical role in treating severe, life-threatening neutropenia cases resistant to standard therapy. The therapy is increasingly adopted in oncology and hematology centers for immunocompromised patients. Technological improvements in collection, storage, and transfusion processes are enhancing treatment safety and effectiveness. Granulocyte transfusions are particularly important in acute infections where rapid neutrophil recovery is required. Growing awareness among clinicians and patients about advanced supportive care options supports market expansion. Strategic collaborations between transfusion centers and hospitals further drive adoption.

- By Route of Administration

On the basis of route of administration, the neutropenia market is segmented into oral and injectable. Injectable administration dominated the market with the largest revenue share of 67.3% in 2025, primarily due to the widespread use of injectable colony-stimulating factors and granulocyte transfusions. Injectable therapies ensure rapid bioavailability, precise dosing, and better clinical outcomes, especially in hospital and oncology settings. Many outpatient and specialty care clinics prefer injectable formats for accurate monitoring and treatment adjustments. Injectable administration is also favored for severe neutropenia requiring immediate neutrophil recovery. Advances in injection devices and pre-filled syringes are improving patient convenience and adherence. Hospitals and specialty centers remain key adopters of injectable therapies due to reliability and clinical guidelines supporting parenteral administration.

Oral administration is anticipated to witness the fastest growth rate of 18.8% from 2026 to 2033, driven by development of patient-friendly oral therapies such as oral antibiotics and novel small-molecule immunomodulators. Oral formulations enhance convenience for homecare and outpatient settings, reducing hospital visits. Increased adoption in emerging markets with limited injectable infrastructure supports growth. Oral therapies are particularly attractive for mild to moderate neutropenia or long-term management. Ongoing research and clinical trials for orally-administered agents are expected to expand availability. The ease of self-administration and improved patient compliance further accelerates growth in this subsegment.

- By End-Users

On the basis of end-users, the neutropenia market is segmented into hospitals, homecare, specialty centers, and others. Hospitals dominated the market with the largest revenue share of 55.4% in 2025, driven by the concentration of oncology, hematology, and immunology services in inpatient and outpatient hospital settings. Hospitals provide advanced diagnostics, injectable therapies, and monitoring facilities that are critical for effective neutropenia management. The segment benefits from strong clinician familiarity with G-CSF therapies and supportive care protocols. Hospitals are also central to clinical trials and early access programs, which reinforce adoption of advanced therapies. Rising cancer prevalence and complex neutropenia cases requiring hospitalization further support dominance. Strategic partnerships with pharmaceutical companies and government healthcare initiatives enhance treatment accessibility within hospital settings.

Homecare is expected to witness the fastest growth rate of 21.2% from 2026 to 2033, fueled by increasing adoption of home-based injectable therapy and telemedicine monitoring solutions. Homecare allows patients to receive G-CSF injections and supportive care without frequent hospital visits. The trend is supported by convenience, patient comfort, and cost reduction in healthcare delivery. Remote patient monitoring devices enable real-time neutrophil count tracking and timely interventions. Growth is particularly strong in regions with expanding outpatient care infrastructure. Collaborations between hospitals, homecare providers, and pharmaceutical companies are driving adoption of homecare services.

- By Distribution Channel

On the basis of distribution channel, the neutropenia market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. Hospital pharmacies dominated the market with the largest revenue share of 61.7% in 2025, due to the direct availability of injectable therapies, G-CSFs, and granulocyte transfusions at hospitals and specialty care centers. Hospital pharmacies ensure compliance with clinical guidelines, proper storage, and timely administration of critical therapies. The segment benefits from strong relationships between clinicians and pharmacy services, facilitating seamless patient care. High adoption of hospital pharmacies in developed regions further strengthens market dominance. Hospital pharmacies also provide access to clinical trials and biosimilars, enhancing patient affordability. Continuous collaboration with healthcare providers ensures treatment adherence and optimal outcomes.

Online pharmacies are expected to witness the fastest growth rate of 19.4% from 2026 to 2033, driven by increasing e-pharmacy adoption, expanding homecare services, and rising patient preference for convenient delivery of medications. Online channels allow patients to access oral therapies and supportive care products from home. Regulatory approval of telemedicine prescriptions and digital healthcare platforms supports growth. Online pharmacies also provide opportunities for patient education, reminders, and subscription services. Growing internet penetration and smartphone usage facilitate wider reach. Partnerships with pharmaceutical companies for direct-to-patient delivery further accelerate adoption.

Neutropenia Market Regional Analysis

- North America dominated the neutropenia market with the largest revenue share of 42.5% in 2025, supported by advanced healthcare infrastructure, high adoption of colony-stimulating factor therapies, strong presence of key pharmaceutical players, and extensive clinical awareness programs

- Patients and healthcare providers in the region highly value access to advanced colony-stimulating factor therapies, granulocyte transfusions, and comprehensive monitoring programs that reduce infection risks and hospitalization duration

- This widespread adoption is further supported by well-established clinical guidelines, early diagnosis programs, increasing government and insurance support, and the presence of key pharmaceutical players, establishing North America as a leading market for both hospital and outpatient neutropenia management

U.S. Neutropenia Market Insight

The U.S. neutropenia market captured the largest revenue share of 79% in 2025 within North America, fueled by the high prevalence of chemotherapy-induced neutropenia and advanced healthcare infrastructure. Patients and healthcare providers increasingly prioritize effective neutropenia management through colony-stimulating factor therapies, antibiotic prophylaxis, and supportive care protocols. The growing preference for outpatient and home-based administration, alongside robust adoption of patient monitoring programs, further propels the market. Moreover, increasing clinical awareness of infection risk reduction and early intervention strategies is significantly contributing to market expansion. Strong reimbursement policies, advanced hospital networks, and the presence of leading pharmaceutical companies also support adoption across both adult and pediatric patient populations.

Europe Neutropenia Market Insight

The Europe neutropenia market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising cancer incidence and the growing demand for supportive care therapies. Stringent clinical guidelines and well-established hematology and oncology care infrastructure are fostering the adoption of colony-stimulating factor therapies and granulocyte transfusions. European healthcare providers are increasingly emphasizing early detection and treatment of neutropenia to reduce infection-related complications. The market is experiencing significant growth across hospital and specialty care settings, with neutropenia therapies being incorporated into standard care protocols for both adult and pediatric patients. Increasing government initiatives and healthcare reimbursement programs are further boosting the market.

U.K. Neutropenia Market Insight

The U.K. neutropenia market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of chemotherapy-induced and autoimmune neutropenia. Concerns regarding infection risks and patient safety are encouraging healthcare providers to adopt advanced therapies such as G-CSFs and granulocyte transfusions. In addition, the U.K.’s well-developed hospital infrastructure, strong clinical research initiatives, and growing adoption of home-based treatment programs are expected to stimulate market growth. Increasing patient access to biosimilars and patient support programs is also contributing to adoption. Rising cancer prevalence and a focus on preventive supportive care further drive the market.

Germany Neutropenia Market Insight

The Germany neutropenia market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of neutropenia management and the adoption of advanced supportive therapies. Germany’s emphasis on healthcare innovation, well-established hospital systems, and focus on patient safety promotes the adoption of injectable therapies and outpatient monitoring programs. Integration of neutropenia management into comprehensive cancer care protocols is becoming increasingly prevalent. Strong research programs, clinical trials, and collaborations with pharmaceutical companies reinforce market growth. The German market also places a strong emphasis on personalized treatment strategies and patient-centric care models.

Asia-Pacific Neutropenia Market Insight

The Asia-Pacific neutropenia market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by increasing cancer prevalence, rising healthcare expenditure, and expanding access to advanced supportive care therapies in countries such as China, Japan, and India. The region’s growing adoption of outpatient and home-based neutropenia management, supported by telemedicine-enabled patient monitoring, is driving market expansion. Furthermore, increasing awareness among healthcare providers regarding infection risk reduction and the availability of cost-effective biosimilars are enhancing accessibility. Government healthcare initiatives, digital health programs, and expanding oncology infrastructure are further supporting market growth.

Japan Neutropenia Market Insight

The Japan neutropenia market is gaining momentum due to the country’s advanced healthcare system, high cancer prevalence, and growing demand for patient-friendly treatment options. Japanese hospitals and specialty centers emphasize injectable colony-stimulating factors and home-based monitoring solutions to reduce infection-related complications. The integration of neutropenia therapies with comprehensive cancer care programs is fueling growth. In addition, Japan’s aging population is likely to drive demand for convenient and effective neutropenia management solutions in both residential and clinical settings. Ongoing clinical trials and strong government support for advanced therapies further enhance market expansion.

India Neutropenia Market Insight

The India neutropenia market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s rising cancer incidence, expanding hospital infrastructure, and increasing awareness of supportive care therapies. Injectable colony-stimulating factor therapies and homecare-based treatment programs are becoming more widely adopted across urban hospitals and specialty centers. Government initiatives promoting cancer care and digital health monitoring are key factors propelling market growth. In addition, the availability of affordable biosimilars and growing domestic pharmaceutical manufacturing capabilities support wider access. Rising adoption of outpatient therapy, telemedicine, and patient education programs further drives the market in India.

Neutropenia Market Share

The Neutropenia industry is primarily led by well-established companies, including:

- Amgen Inc. (U.S.)

- Sandoz Inc. (U.S.)

- Coherus BioSciences, Inc. (U.S.)

- Biocon Biologics Ltd. (India)

- Pfizer Inc. (U.S.)

- Evive Biotech (U.S.)

- G1 Therapeutics, Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Spectrum Pharmaceuticals, Inc. (U.S.)

- Baxter (U.S.)

- Sanofi (France)

- Novartis AG (Switzerland)

- GSK plc (U.K.)

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Kyowa Kirin Co., Ltd. (Japan)

- CSL Limited (Australia)

- Dr. Reddy’s Laboratories Ltd. (India)

- Astellas Pharma Inc. (Japan)

What are the Recent Developments in Global Neutropenia Market?

- In December 2025, the U.S. Food and Drug Administration (FDA) approved Armlupeg™ (pegfilgrastim‑unne), a biosimilar to Neulasta® (pegfilgrastim), to decrease the incidence of infection manifested by febrile neutropenia in patients receiving myelosuppressive chemotherapy, expanding accessible neutropenia supportive care options in the U.S. market

- In March 2025, the European Medicines Agency (EMA) granted marketing authorization for Ryzneuta, enabling its use across EU member states to reduce the duration and incidence of neutropenia and associated febrile neutropenia in adult cancer patients receiving cytotoxic chemotherapy, expanding global access to this supportive therapy

- In August 2024, Armlupeg (pegfilgrastim‑unne) received regulatory approval in Canada for reducing the risk of neutropenia‑related infection in chemotherapy patients, marking a key step for broader international rollout of this biosimilar supportive therapy

- In November 2023, the U.S. Food and Drug Administration (FDA) approved Ryzneuta (efbemalenograstim alfa‑vuxw) injection as a new long‑acting G‑CSF to prevent chemotherapy‑induced febrile neutropenia in adults with non‑myeloid malignancies, providing another prophylactic treatment option alongside pegfilgrastim and enhancing patient care protocols

- In May 2023, China’s National Medical Products Administration approved efbemalenograstim alfa (Ryzneuta), a novel long‑acting granulocyte colony‑stimulating factor (G‑CSF), to reduce the incidence of infection manifested by febrile neutropenia in adult patients receiving myelosuppressive chemotherapy, marking a significant expansion in supportive care therapy options in Asia

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.