Global Orphan Dermatology Disorders Drug Market

Market Size in USD Million

USD

138.60 Million

USD

308.20 Million

2025

2033

USD

138.60 Million

USD

308.20 Million

2025

2033

| 2026 - 2033 | |

| USD 138.60 Million | |

| USD 308.20 Million | |

| % | |

|

Orphan Dermatology Disorders Drug Market Size

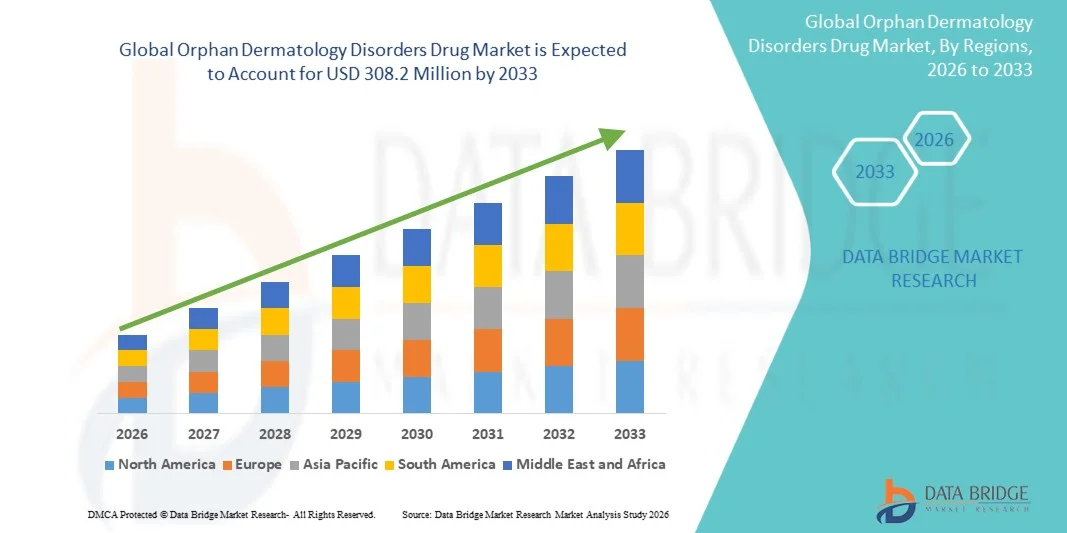

- The global orphan dermatology disorders drug market size was valued at USD 138.6 million in 2025 and is expected to reach USD 308.2 million by 2033, at a CAGR of 10.50% during the forecast period

- The market growth is primarily driven by increasing R&D investments, rising orphan drug designations, and expanding clinical activity targeting ultra-rare dermatological conditions, supported by favorable regulatory frameworks that incentivize innovation

- In addition, increasing demand for effective, targeted, and disease-modifying treatments among patients with limited therapeutic options combined with advancements in gene therapy, biologics, and RNA-based platforms is accelerating adoption. These converging factors are significantly boosting the growth trajectory of the orphan dermatology disorders drug industry

Orphan Dermatology Disorders Drug Market Analysis

- Orphan dermatology disorder drugs, designed to treat rare and severe skin conditions, are becoming increasingly significant within the rare-disease therapeutic landscape due to rising unmet clinical needs, expanded genetic understanding of dermatologic disorders, and advancements in precision medicine platforms that enable targeted and disease-modifying treatment approaches

- The demand for orphan dermatology therapies is primarily propelled by increased rare-disease awareness, improved diagnostic capabilities, and strong regulatory incentives such as orphan drug exclusivity, priority review, and accelerated approval pathways, which collectively encourage innovation, clinical development, and commercial uptake across global healthcare systems

- North America dominated the orphan dermatology disorders drug market with the largest revenue share of 40.62% in 2025, supported by robust biotechnology research, higher treatment accessibility, and active clinical pipelines focused on conditions such as epidermolysis bullosa, ichthyosis, and autoimmune blistering diseases, with the U.S. demonstrating expanding adoption of biologics, gene therapies, and advanced wound-care solutions

- Asia-Pacific is expected to be the fastest-growing region in the orphan dermatology disorders drug market during the forecast period, driven by improving healthcare infrastructure, increasing investment in rare-disease research, and growing patient identification initiatives across Japan, China, India, and South Korea

- The biologics segment dominated the orphan dermatology disorders drug market with a market share of 53.1% in 2025, attributed to their targeted mechanisms of action, superior clinical efficacy, and rising adoption for managing complex and genetically mediated rare dermatologic conditions, coupled with ongoing advancements in monoclonal antibodies and recombinant protein therapies

Report Scope and Orphan Dermatology Disorders Drug Market Segmentation

|

Attributes |

Orphan Dermatology Disorders Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Orphan Dermatology Disorders Drug Market Trends

“Advancement of Precision Therapies Through Gene and Biologic Innovation”

- A significant and accelerating trend in the global orphan dermatology disorders drug market is the rapid advancement of precision medicine, particularly through gene therapies, RNA-based platforms, and next-generation biologics that target the underlying molecular defects of rare dermatologic conditions, fundamentally transforming treatment possibilities for patients

- For instance, investigational gene therapies for epidermolysis bullosa are demonstrating meaningful wound-healing responses in trials, while novel monoclonal antibodies for autoimmune blistering diseases offer improved targeting of disease pathways, expanding the scope of specialized rare-skin disorder treatments

- AI-enabled diagnostic tools and molecular profiling platforms are also elevating clinical accuracy by identifying specific genetic mutations and disease subtypes; for instance, AI dermatology tools are increasingly used to assist clinicians in diagnosing ichthyosis variants, pemphigus staging, and other ultra-rare conditions, enabling earlier intervention and optimized therapy selection

- The integration of digital health platforms with rare-disease management systems supports remote monitoring, patient-reported outcome tracking, and data-driven care optimization, allowing clinicians to assess treatment responses for patients with chronic rare dermatologic disorders through coordinated digital ecosystems

- This shift toward highly personalized, mechanism-targeted, and technologically supported therapies is reshaping expectations for rare skin disease management globally, prompting companies to accelerate development of advanced therapeutic candidates such as gene-corrective approaches and biologics engineered for rare inflammatory pathways

- The demand for sophisticated therapies particularly gene therapies, biologics, and RNA-based drugs is rising rapidly across key healthcare markets as patients, clinicians, and regulatory bodies increasingly prioritize targeted treatment options with meaningful clinical benefits for underserved rare dermatology populations

Orphan Dermatology Disorders Drug Market Dynamics

Driver

“Rising Therapeutic Need Due to Limited Treatment Options and Strong Regulatory Support”

- The increasing prevalence of diagnosed rare dermatologic disorders, combined with the severe unmet treatment needs in conditions such as epidermolysis bullosa, ichthyosis, and autoimmune blistering diseases, is a major driver of demand for orphan dermatology therapies across global healthcare systems

- For instance, in May 2025, the FDA granted an orphan drug designation to a gene-edited therapy for dystrophic epidermolysis bullosa, reflecting the growing pace of clinical innovation supported by global regulatory bodies. Such incentives are expected to drive significant development activity in the forecast period

- As clinicians and patients seek more effective therapeutic options, advanced treatments such as biologics, recombinant proteins, and targeted immunotherapies are gaining prominence, offering capabilities such as reduced disease severity, improved wound healing, and better long-term management outcomes compared to conventional care

- Furthermore, accelerating adoption of precision-therapy platforms and rare-disease-focused clinical research networks is positioning orphan dermatology therapies as integral components of the broader rare-disease treatment ecosystem, with strong alignment between patient advocacy groups, research institutions, and biotech developers

- The availability of regulatory incentives including market exclusivity, tax credits, fee waivers, and priority reviews continues to propel investment and R&D interest from pharmaceutical companies, increasing both the volume and diversity of pipeline programs targeting orphan dermatologic disorders

- The trend toward specialized, mechanism-focused therapeutics and the growing willingness of healthcare providers to adopt advanced treatment modalities are contributing to expanded access and uptake of orphan dermatology drugs across both established and emerging markets

Restraint/Challenge

“High Treatment Costs and Complex Regulatory Requirements”

- The high cost of developing and manufacturing specialized therapies particularly gene therapies and biologics poses a significant challenge to broader access and affordability in the orphan dermatology disorders drug market, as these treatments often require highly specialized production and distribution systems

- For instance, concerns over the multimillion-dollar price tags of certain gene therapies have raised questions within healthcare systems regarding reimbursement feasibility and long-term sustainability, making some stakeholders cautious about widespread adoption

- In addition, the rarity and complexity of these conditions result in small patient populations, creating challenges for designing statistically robust clinical trials and slowing overall development timelines, making it more difficult for companies to bring new therapies to market efficiently

- Regulatory agencies require extensive safety and long-term outcome data for advanced therapies such as gene-editing and viral-vector treatments, leading to prolonged approval processes that may delay patient access and increase development costs for manufacturers

- While treatment awareness is improving, many regions still face diagnostic gaps, limited specialist availability, and inconsistent rare-disease infrastructure, which restrict the identification and treatment of patients who could benefit from emerging orphan dermatology therapies

- Overcoming these challenges through expanded diagnostic networks, improved reimbursement frameworks, and increased global investment will be essential for ensuring long-term growth and broader adoption of innovative treatments within the orphan dermatology disorders drug market

Orphan Dermatology Disorders Drug Market Scope

The market is segmented on the basis of drug class, route of administration, disease type, and distribution channel.

- By Drug Class

On the basis of drug class, the orphan dermatology disorders drug market is segmented into biologics, gene therapies, cell therapies, oligonucleotide therapies, small molecules, and novel topical delivery systems. The biologics segment dominated the market with the largest revenue share of 53.1% in 2025, driven by their targeted mechanism of action and strong clinical effectiveness across rare dermatologic conditions such as autoimmune blistering diseases and ichthyosis. Biologics offer precision targeting of immune pathways that are often central to the pathology of rare skin disorders, making them the first-line option in many advanced treatment regimens. Their wider availability, established regulatory pathways, and increasing clinician confidence further support their leadership position. Adoption has also accelerated due to the growing use of monoclonal antibodies that demonstrate durable responses and better safety profiles. Moreover, ongoing pipeline expansion continues to strengthen the biologics segment, with many companies focusing on developing next-generation antibody platforms tailored for ultra-rare dermatologic indications.

The gene therapies segment is anticipated to witness the fastest growth from 2026 to 2033, driven by breakthroughs in gene-editing technologies and increasing clinical success in treating genetic dermatologic disorders such as epidermolysis bullosa. Gene therapies offer the potential for long-lasting or even curative outcomes by addressing the root genetic defect rather than managing symptoms, representing a transformative shift in rare-disease care. Advancements in viral vectors, ex vivo gene correction, and non-viral gene delivery platforms are accelerating development timelines. Rising investment from biotech firms and strong regulatory incentives such as orphan drug designation and priority review are further propelling growth. Increased patient advocacy and clinical trial participation globally are also enabling faster expansion of the gene therapy segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, intravenous, subcutaneous, topical, and intradermal. The topical segment dominated the market in 2025, primarily due to its direct, localized application, which is particularly suited for dermatologic conditions where visible lesions and skin-surface manifestations are the primary focus of treatment. Topical formulations offer ease of use, reduced systemic exposure, and better adherence—all essential factors for managing chronic rare skin disorders. Many small-molecule drugs and novel delivery systems are developed specifically for topical administration due to targeted therapeutic penetration needs. In addition, topical therapies continue to expand as new nano-delivery and lipid-based carriers improve drug penetration into deeper layers of diseased skin. The segment remains preferred in clinical practice because of its convenience for both patients and caregivers.

The intravenous segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the growing use of systemic biologics and advanced therapies requiring infusion-based delivery. Many high-efficacy biologics for autoimmune blistering diseases and severe genodermatoses are only available through intravenous infusion, increasing demand for this route. In addition, gene therapies and certain cell-based products also require controlled IV administration performed in specialty centers. Improvements in infusion infrastructure, growing specialist availability, and increasing hospital adoption of rare-disease infusion therapies further support growth. As systemic treatments become more targeted and potent, demand for intravenous delivery is expected to rise significantly.

- By Disease

On the basis of disease type, the market is segmented into epidermolysis bullosa, ichthyosis, autoimmune blistering diseases, porphyrias, monogenic dermatologic disorders, and other rare dermatology disorders. The epidermolysis bullosa segment dominated the market in 2025, driven by the high clinical burden of the disorder, the strong research focus, and the large number of emerging therapies being developed specifically for EB. The condition’s severe, chronic, and life-impacting nature has led to substantial investment in biologics, gene therapies, and cell-based treatments. EB has one of the most active pipelines among rare dermatologic disorders, supported by patient advocacy groups and extensive global clinical trial activity. Healthcare systems are prioritizing EB management due to its high complexity, unmet needs, and frequent hospitalization requirements. This extensive research and clinical focus reinforce EB’s dominant market position.

The monogenic dermatologic disorders segment is projected to grow at the fastest pace during the forecast period, driven by increasing genomic research and rapid identification of previously underdiagnosed single-gene skin diseases. Advances in next-generation sequencing and precision medicine are enabling tailored therapies targeting specific genetic mutations. As more monogenic disorders receive formal classification and diagnostic attention, companies are investing in gene-corrective, oligonucleotide, and RNA-based platforms to address newly recognized therapeutic needs. Growing patient registry development and improved global awareness of hereditary rare skin diseases further accelerate growth.

- By Distribution Channel

On the basis of distribution channel, the orphan dermatology drug market is segmented into hospital pharmacies, specialty pharmacies, retail pharmacies, and online pharmacies. Specialty pharmacies dominated the market in 2025 due to their ability to handle complex therapies such as biologics, gene therapies, and advanced infusion drugs that require cold-chain management, patient counseling, and coordinated clinical support. Rare dermatology drugs often involve strict handling requirements, prior authorization processes, and close patient monitoring, all of which specialty pharmacies are specifically equipped to manage. Their strong collaboration with hospitals, clinicians, and rare-disease care networks further strengthens their role. Specialty pharmacies also offer disease-specific support programs, enhancing adherence and patient outcomes.

Online pharmacies are anticipated to witness the fastest growth from 2026 to 2033, driven by the increasing digitalization of healthcare and rising patient preference for home delivery of chronic-therapy medications. Patients with rare dermatologic disorders often require long-term treatment, making online ordering and subscription-based supply models highly attractive. Digital pharmacies are expanding service offerings, including teleconsultations, automated prescription renewals, and remote adherence support. Increased regulatory acceptance of e-pharmacy operations, particularly in North America and parts of Asia-Pacific, further propels growth. As digital infrastructure strengthens globally, online platforms are rapidly emerging as accessible and cost-efficient distribution channels for chronic rare-disease therapies.

Orphan Dermatology Disorders Drug Market Regional Analysis

- North America dominated the orphan dermatology disorders drug market with the largest revenue share of 40.62% in 2025, supported by robust biotechnology research, higher treatment accessibility, and active clinical pipelines focused on conditions such as epidermolysis bullosa, ichthyosis, and autoimmune blistering diseases, with the U.S. demonstrating expanding adoption of biologics, gene therapies, and advanced wound-care solutions

- The region benefits from well-established reimbursement frameworks and accelerated approval pathways, which encourage pharmaceutical companies to invest in advanced therapies such as biologics, gene therapies, and novel topical formulations

- In addition, a strong presence of leading biotechnology firms, active patient advocacy groups, and widespread adoption of precision medicine significantly contribute to market leadership, with growing diagnosis rates and increased access to specialty dermatology care further propelling growth across the U.S. and Canada

U.S. Orphan Dermatology Disorders Drug Market Insight

The U.S. orphan dermatology disorders drug market captured the largest revenue share in 2025 within North America, driven by strong regulatory incentives such as Orphan Drug Designation, Priority Review, and accelerated approvals for rare disease therapies. The presence of leading biotechnology innovators and specialized research centers fosters rapid advancement in biologics, gene therapies, and precision medicine. Patients and clinicians are increasingly shifting toward targeted therapies due to better efficacy compared to conventional treatments. The expanding network of specialty pharmacies and enhanced access to genetic testing further supports early diagnosis and treatment adoption. In addition, robust patient advocacy movements and well-structured reimbursement policies significantly strengthen the U.S. market position.

Europe Orphan Dermatology Disorders Drug Market Insight

The Europe orphan dermatology disorders drug market is projected to expand at a substantial CAGR throughout the forecast period, driven by strong support from the European Medicines Agency (EMA) for orphan drug development. Increasing diagnosis rates of rare dermatologic conditions and rising awareness among dermatologists and tertiary care centers are major contributing factors. The region is witnessing rising adoption of biologics and cell-based therapies due to advancements in clinical research. Demand is also strengthened by supportive healthcare infrastructure and government policies that encourage innovation. Moreover, Europe is experiencing increased enrollment in clinical trials, boosting the development pipeline across multiple rare skin disorders.

U.K. Orphan Dermatology Disorders Drug Market Insight

The U.K. orphan dermatology disorders drug market is anticipated to grow at a noteworthy CAGR, supported by the National Health Service (NHS) framework that facilitates early diagnosis and treatment access for rare diseases. A growing emphasis on genomics and precision dermatology is accelerating the adoption of innovative therapies. Concerns regarding underdiagnosed rare skin disorders are prompting improved screening initiatives and clinician education. The U.K.’s vibrant biotech ecosystem and strong academic-industry collaborations continue to contribute to novel therapy development. In addition, patient support programs and rare disease registries are enhancing treatment adoption and long-term management.

Germany Orphan Dermatology Disorders Drug Market Insight

The Germany orphan dermatology disorders drug market is expected to expand at a considerable CAGR, driven by high investments in rare disease research and strong pharmaceutical manufacturing capabilities. German healthcare providers are increasingly adopting advanced biologics and gene-based therapies for severe inherited skin disorders. The country’s focus on innovation, coupled with stringent quality standards, encourages the use of cutting-edge therapeutic solutions. Rising awareness of rare dermatologic conditions and increased demand for specialized dermatology services are supporting market growth. Moreover, Germany’s robust insurance system improves patient access to high-cost orphan drugs, strengthening overall market uptake.

Asia-Pacific Orphan Dermatology Disorders Drug Market Insight

The Asia-Pacific orphan dermatology disorders drug market is poised to grow at the fastest CAGR during the forecast period, driven by expanding healthcare infrastructure and rising diagnosis rates across countries such as Japan, China, South Korea, and India. Increasing investments in biotechnology and rare disease research are accelerating access to advanced therapies. Government-supported rare disease programs and improving reimbursement environments are also fostering greater treatment adoption. The region’s growing focus on clinical trials and genomic initiatives is expanding therapeutic availability. In addition, patient advocacy and better awareness campaigns are helping overcome historical underdiagnosis in APAC.

Japan Orphan Dermatology Disorders Drug Market Insight

The Japan orphan dermatology disorders drug market is gaining momentum due to the country’s strong regulatory frameworks for rare diseases and rapid technological advancements in gene and cell therapy. Growing demand for targeted treatments is driven by Japan’s high diagnostic accuracy and emphasis on early intervention. Integration of orphan dermatology drugs with advanced patient management systems is supporting long-term treatment adherence. A strong culture of innovation and the presence of leading pharmaceutical companies contribute to accelerated product development. Furthermore, Japan’s aging population increases demand for specialized dermatologic care, supporting continued market expansion.

India Orphan Dermatology Disorders Drug Market Insight

The India orphan dermatology disorders drug market accounted for a significant share in Asia Pacific in 2025, supported by rising awareness of rare diseases and expanding access to specialty healthcare services. Increasing adoption of genetic testing and the emergence of domestic biotech companies are strengthening the availability of advanced therapies. Government initiatives to include rare diseases under national health programs are improving diagnosis and treatment accessibility. The growing middle class and rapid urbanization contribute to greater demand for innovative dermatology treatments. In addition, collaborations between global pharmaceutical firms and Indian research institutions are accelerating clinical research and drug availability across the country.

Orphan Dermatology Disorders Drug Market Share

The Orphan Dermatology Disorders Drug industry is primarily led by well-established companies, including:

- Krystal Biotech, Inc. (U.S.)

- Abeona Therapeutics Inc. (U.S.)

- Castle Creek Biosciences, Inc. (U.S.)

- LEO Pharma A/S (Denmark)

- Arcutis Biotherapeutics, Inc. (U.S.)

- GSK plc (U.K.)

- BioMendics (U.S.)

- Amryt Pharma plc (U.K.)

- Novartis AG (Switzerland)

- Pfizer, Inc. (U.S.)

- AbbVie, Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- GALDERMA (Switzerland)

- Sanofi (France)

- UCB S.A. (Belgium)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Incyte Corporation (U.S.)

- AnaptysBio, Inc. (U.S.)

What are the Recent Developments in Global Orphan Dermatology Disorders Drug Market?

- In April 2025, the FDA approved Zevaskyn (prademagene zamikeracel), developed by Abeona Therapeutics, as the first and only cell-based gene-modified therapy for patients (adult and pediatric) with Recessive Dystrophic Epidermolysis Bullosa (RDEB). This offers a one-time graft treatment for chronic wounds, representing a major advance over supportive care

- In February 2025, a promising drug-candidate originally developed at Tampere University was licensed to biopharma Theravia for further development and commercialization, targeting treatments for broad forms of Epidermolysis Bullosa. This licensing agreement reflects growing academic-industry collaboration to bring novel therapeutics for rare skin diseases to clinical stage

- In December 2023, the active pharmaceutical ingredient Filsuvez (birch bark-derived triterpenes) received regulatory approval in the United States (after earlier EU approval) for treatment of wounds associated with Epidermolysis Bullosa expanding the therapeutic toolbox beyond gene/cell therapies to include topical, non-viral, small-molecule/derivative-based options

- In May 2023, the Vyjuvek (beremagene geperpavec-svdt) by Krystal Biotech was approved by the U.S. Food and Drug Administration (FDA) as the first topical gene therapy for Dystrophic Epidermolysis Bullosa (DEB), a rare genetic skin disorder. The treatment delivers the functional COL7A1 gene to wounds, promoting collagen VII production and wound healing

- In May 2023, the Japanese regulatory authority (MHLW) granted orphan drug designation to Redasemtide for treatment of dystrophic epidermolysis bullosa, marking a significant regulatory milestone and enabling potential expedited development and approval in Japan

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.