Global Osteogenesis Imperfecta Treatment Market

Market Size in USD Million

USD

740.14 Million

USD

894.78 Million

2024

2032

USD

740.14 Million

USD

894.78 Million

2024

2032

| 2025 - 2032 | |

| USD 740.14 Million | |

| USD 894.78 Million | |

| % | |

|

Osteogenesis Imperfecta Treatment Market Size

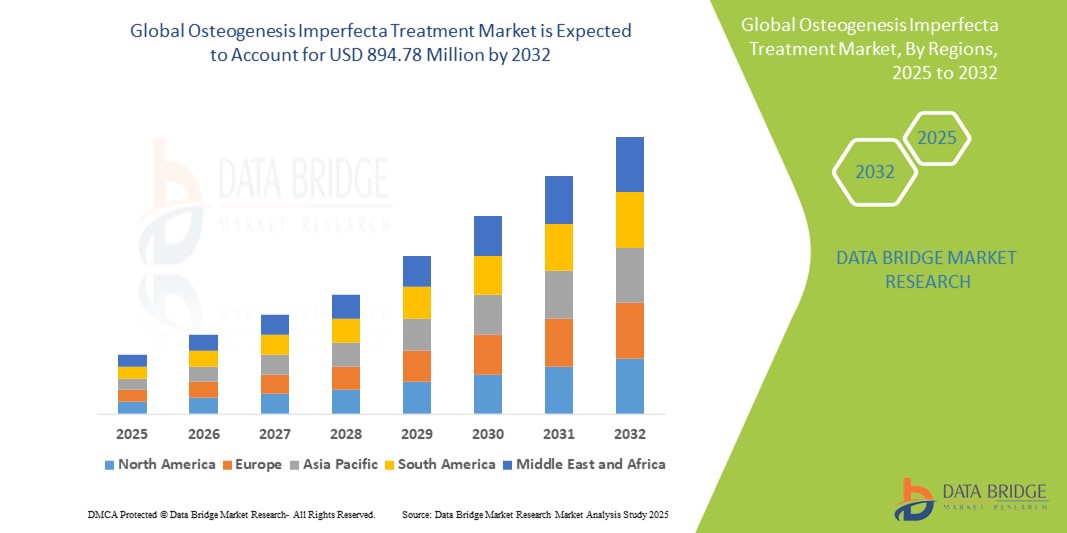

- The global osteogenesis imperfecta treatment market size was valued at USD 740.14 million in 2024 and is expected to reach USD 894.78 million by 2032, at a CAGR of 2.40% during the forecast period

- The market growth is largely driven by increasing awareness about osteogenesis imperfecta (OI), advancements in genetic research, and the development of novel therapies aimed at improving bone strength and reducing fracture rates in patients

- Furthermore, rising investments in R&D by pharmaceutical companies, alongside growing patient populations seeking better management options for OI, are positioning innovative treatment modalities as key players in disease management. These converging factors are accelerating the adoption of advanced OI treatments, thereby significantly boosting the industry’s expansion

Osteogenesis Imperfecta Treatment Market Analysis

- Osteogenesis imperfecta treatments, encompassing pharmacologic agents such as bisphosphonates and denosumab, are increasingly vital components of rare disease management strategies in both pediatric and adult populations due to their ability to strengthen bone mass, reduce fracture frequency, and improve mobility outcomes

- The escalating demand for osteogenesis imperfecta treatments is primarily fueled by improved diagnostic capabilities, increasing global awareness of rare genetic disorders, supportive regulatory frameworks for orphan drugs, and rising investments in novel therapies such as gene-based interventions and monoclonal antibodies

- North America dominates the osteogenesis imperfecta treatment market with the largest revenue share of 52.5% in 2024, characterized by well-established healthcare infrastructure, high per capita health expenditure, and strong presence of research-focused pharmaceutical companies

- Asia-Pacific is expected to be the fastest growing region in the osteogenesis imperfecta treatment market during the forecast period due to increasing healthcare access, rising public and private investments in rare disease treatment, and growing awareness and diagnosis rates across developing nations

- Intravenous segment dominates the osteogenesis imperfecta treatment market with a market share of 51.5% in 2024, driven by its rapid therapeutic action, higher bioavailability, and frequent use in administering bisphosphonates in clinical settings

Report Scope and Osteogenesis Imperfecta Treatment Market Segmentation

|

Attributes |

Osteogenesis Imperfecta Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Osteogenesis Imperfecta Treatment Market Trends

“Advancing Therapeutics Through Biologics and Precision Medicine”

- A significant and accelerating trend in the global osteogenesis imperfecta treatment market is the advancement of biologic therapies and the increasing incorporation of precision medicine approaches. This evolution is fundamentally transforming how OI is managed by moving beyond symptomatic treatment toward targeted interventions that address the underlying genetic and molecular causes of the disease

- For instance, denosumab, a monoclonal antibody that inhibits bone resorption, is emerging as a promising alternative to traditional bisphosphonates, particularly in patients with severe or treatment-resistant forms of OI. Meanwhile, novel therapies in development, such as gene editing techniques and sclerostin inhibitors, are gaining attention for their potential to correct or mitigate the genetic defects responsible for bone fragility

- Precision medicine is enabling healthcare providers to tailor treatment regimens based on individual patient profiles, such as genetic mutations, disease severity, and responsiveness to specific drugs. This approach is increasingly supported by improvements in genetic testing and data analytics, which facilitate early diagnosis and more effective treatment planning

- Biopharmaceutical companies and academic research centers are collaborating to accelerate clinical trials and bring these next-generation therapies to market. For example, ongoing studies funded by organizations such as the Osteogenesis Imperfecta Foundation are investigating gene therapy and cell-based approaches aimed at long-term or curative outcomes

- The shift toward biologic and genetically-informed therapies is not only expanding the treatment landscape but also raising patient and caregiver expectations for improved quality of life and long-term disease management. As a result, companies such as Ultragenyx and Mereo BioPharma are actively investing in pipeline drugs that align with these emerging treatment paradigms

- The demand for innovative and targeted osteogenesis imperfecta therapies is growing rapidly across both pediatric and adult populations, as healthcare providers and patients increasingly prioritize long-term efficacy, reduced side effects, and personalized treatment strategies over traditional one-size-fits-all approaches

Osteogenesis Imperfecta Treatment Market Dynamics

Driver

“Growing Demand Due to Advancements in Rare Disease Therapies and Increased Awareness”

- The rising global awareness of rare genetic disorders, coupled with increasing investment in advanced therapeutic solutions, is a significant driver for the expanding demand in the osteogenesis imperfecta treatment market

- For instance, in February 2024, Ultragenyx Pharmaceutical Inc. announced continued development of setrusumab, a monoclonal antibody targeting sclerostin, as part of its Phase 3 clinical trial for treating OI. Such strategic developments by key biopharmaceutical players are expected to drive market growth through 2032

- As healthcare systems become more proactive in identifying and managing rare diseases, patients with OI are benefiting from earlier diagnosis and access to targeted therapies that go beyond symptomatic treatment, such as bone-strengthening agents and emerging gene therapies

- Furthermore, support from regulatory authorities—such as orphan drug designations, priority reviews, and fast-track approvals—is accelerating the development and commercial availability of innovative OI treatments, enhancing market momentum

- The increasing recognition of the importance of lifelong care for OI patients, including pediatric and adult management strategies, is fostering greater demand for treatment options that are both clinically effective and safe over the long term

- In addition, growing patient advocacy and education initiatives, such as those led by the Osteogenesis Imperfecta Foundation, are playing a pivotal role in raising public and professional awareness, encouraging early intervention, and supporting research funding. These combined efforts are significantly advancing the treatment landscape and fueling the global market's upward trajectory

Restraint/Challenge

“High Treatment Costs and Limited Access to Specialized Care”

- The high cost of treatment and limited access to specialized care centers present significant challenges to broader adoption of osteogenesis imperfecta therapies, particularly in low- and middle-income regions. Advanced treatments such as monoclonal antibodies, gene therapies, and long-term bisphosphonate regimens often carry a premium price tag, making them less accessible to uninsured or underinsured patients

- For instance, emerging biologic therapies such as setrusumab and denosumab involve complex development and administration protocols, which can substantially increase the cost burden on healthcare systems and families. These high costs, coupled with limited reimbursement policies in certain countries, may delay or restrict treatment initiation

- Addressing these cost-related barriers through expanded insurance coverage, government-supported rare disease programs, and tiered pricing strategies is essential for ensuring more equitable access. Companies such as Mereo BioPharma and Ultragenyx are actively engaging in advocacy and policy discussions to make advanced OI therapies more affordable and accessible

- Furthermore, access to specialized care teams—including geneticists, endocrinologists, orthopedic surgeons, and rehabilitation experts—is unevenly distributed, particularly in rural and underserved regions. Patients may need to travel significant distances or experience long wait times to receive appropriate care, delaying diagnosis and treatment

- While telemedicine and global awareness campaigns are helping to bridge the gap, the lack of a standardized care framework for OI management continues to pose a challenge. Overcoming these access issues through healthcare system strengthening, provider training, and rare disease infrastructure development will be vital for long-term market growth and patient outcomes

Osteogenesis Imperfecta Treatment Market Scope

The market is segmented on the basis of drug class, route of administration, end user, and distribution channel.

- By Drug Class

On the basis of drug class, the osteogenesis imperfecta treatment market is segmented into teriparatide, denosumab, and others. The others segment including bisphosphonates dominated the largest market revenue share in 2024, driven by their long-standing clinical efficacy in reducing fracture incidence and increasing bone mineral density. Bisphosphonates are widely used as first-line treatment for children and adults with moderate to severe forms of OI and are often administered in hospital settings due to their intravenous delivery format.

The denosumab segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by its mechanism of action as a RANKL inhibitor, which offers an alternative approach to reducing bone resorption.

- By Route Of Administration

On the basis of route of administration, the market is segmented into oral, intravenous, and subcutaneous. The intravenous segment dominated the largest market revenue share of 51.5% in 2024, driven by its widespread use for delivering bisphosphonates in clinical settings where higher bioavailability and controlled dosing are required. IV therapy remains the preferred method for patients requiring intensive bone strengthening, particularly in severe or pediatric cases.

The subcutaneous segment is projected to witness the fastest CAGR during the forecast period, supported by the rise in self-administered biologics such as denosumab. Its convenience, lower frequency of administration, and suitability for homecare delivery models are fueling its adoption

- By End User

On the basis of end user, the osteogenesis imperfecta treatment market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment lead the market in terms of revenue share in 2024, owing to their critical role in administering IV therapies, monitoring treatment regimens, and offering multidisciplinary care for OI patients. Hospitals are often the first point of contact for diagnosis and long-term management, particularly in cases involving fractures or surgical interventions

The homecare segment is expected to grow at the fastest rate from 2025 to 2032, driven by advancements in subcutaneous drug delivery, rising healthcare cost pressures, and a shift toward decentralized care models. Home-based treatment supports greater convenience and patient adherence, especially in chronic management scenarios.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The hospital pharmacies segment dominated the largest market share in 2024, due to the concentration of specialty treatments such as IV bisphosphonates and denosumab being dispensed directly from hospital-based institutions. These settings ensure proper handling, storage, and administration of sensitive therapies used in OI management.

The online pharmacies segment is anticipated to record the fastest growth rate during the forecast period, reflecting broader digital health trends and improved accessibility of chronic treatment medications. Convenience, home delivery, and growing patient comfort with telemedicine platforms are supporting this segment’s expansion, particularly for oral and subcutaneous formulations.

Osteogenesis Imperfecta Treatment Market Regional Analysis

- North America dominates the osteogenesis imperfecta treatment market with the largest revenue share of 52.5% in 2024, driven by well-established healthcare infrastructure, high per capita health expenditure, and strong presence of research-focused pharmaceutical companies

- Patients and healthcare providers in the region prioritize access to innovative treatments such as bisphosphonates, denosumab, and emerging gene therapies, supported by favorable reimbursement policies and strong awareness of genetic disorders

- This widespread adoption is further bolstered by a robust network of specialty clinics and hospitals equipped for OI management, alongside growing patient advocacy initiatives that promote early diagnosis and comprehensive care, positioning North America as a leading market for osteogenesis imperfecta treatment globally

U.S. Osteogenesis Imperfecta Treatment Market Insight

The U.S. osteogenesis imperfecta treatment market captured the largest revenue share in 2024 within North America, fueled by advanced healthcare infrastructure and early adoption of innovative therapies. The high prevalence of rare disease awareness, combined with supportive insurance frameworks and government initiatives, drives demand for cutting-edge treatments such as bisphosphonates, denosumab, and emerging gene therapies. In addition, the presence of leading pharmaceutical companies and specialized OI centers enhances treatment accessibility and patient outcomes across the country.

Europe Osteogenesis Imperfecta Treatment Market Insight

The Europe osteogenesis imperfecta treatment market is projected to expand at a significant CAGR during the forecast period, driven by increasing diagnosis rates and growing investment in rare disease research. The region’s stringent healthcare regulations and reimbursement policies facilitate wider access to advanced OI treatments. Growing urbanization and rising healthcare expenditure, particularly in Western European countries, are further accelerating adoption. The market benefits from specialized care centers and increasing awareness among healthcare professionals and patients alike.

U.K. Osteogenesis Imperfecta Treatment Market Insight

The U.K. osteogenesis imperfecta treatment market is expected to grow steadily during the forecast period, supported by the government’s commitment to rare disease strategies and enhanced funding for genetic disorder therapies. Increased patient advocacy and the expansion of specialty clinics are driving early diagnosis and timely treatment. The U.K.’s strong pharmaceutical research base and access to advanced biologics also underpin market growth.

Germany Osteogenesis Imperfecta Treatment Market Insight

The Germany osteogenesis imperfecta treatment market is anticipated to witness considerable growth, driven by a robust healthcare system, high patient awareness, and increasing investments in innovative therapies. Germany’s focus on precision medicine and integration of multidisciplinary care approaches for rare diseases contribute to the adoption of novel treatments. Patient preference for personalized and sustainable treatment regimens is also encouraging uptake.

Asia-Pacific Osteogenesis Imperfecta Treatment Market Insight

The Asia-Pacific osteogenesis imperfecta treatment market is poised to grow at the fastest CAGR during the forecast period, supported by improving healthcare infrastructure, rising disposable incomes, and expanding rare disease diagnosis capabilities in countries such as China, Japan, and India. Government initiatives to improve access to orphan drugs and growing awareness among healthcare providers are further fueling demand. The increasing number of specialty clinics and enhanced reimbursement policies across key APAC countries also contribute to market expansion.

Japan Osteogenesis Imperfecta Treatment Market Insight

The Japan osteogenesis imperfecta treatment market is gaining momentum due to the country’s advanced healthcare system, high standard of patient care, and focus on aging population health management. Increased screening programs and access to innovative treatments such as denosumab and gene therapies are driving growth. Japan’s emphasis on technological integration in healthcare services supports better treatment adherence and monitoring.

India Osteogenesis Imperfecta Treatment Market Insight

The India osteogenesis imperfecta treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, driven by increasing awareness of rare diseases, rising healthcare expenditure, and expanding access to specialty healthcare services. India’s large population base, rapid urbanization, and growing presence of domestic and international pharmaceutical companies offering cost-effective OI therapies are key factors propelling market growth. Government initiatives to improve rare disease diagnosis and treatment accessibility also play a crucial role.

Osteogenesis Imperfecta Treatment Market Share

The osteogenesis imperfecta treatment industry is primarily led by well-established companies, including:

- Mereo BioPharma Group plc (U.K.)

- Ultragenyx Pharmaceutical Inc. (U.S.)

- Bone Therapeutics SA (Belgium)

- Asahi Kasei Corporation (U.S.)

- Novartis AG (Switzerland)

- Ipsen Pharma SAS (France)

- Pfizer Inc. (U.S.)

- F. Hoffmann-La Roche AG (Switzerland)

- Horizon Therapeutics plc (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Sobi (Sweden)

- Sandoz International GmbH (Switzerland)

- Mitsubishi Tanabe Pharma Corporation (Japan)

- Cytokinetics, Incorporated (U.S.)

- AbbVie Inc. (U.S.)

- Akebia Therapeutics, Inc. (U.S.)

- Helsinn Group (Switzerland)

- Lilly (U.S.)

Latest Developments in Global Osteogenesis Imperfecta Treatment Market

- In January 2024, Bone Therapeutics initiated a Phase I/IIa clinical trial for its allogeneic cell therapy product, ALLOB, targeting patients with osteogenesis imperfecta. The trial is designed to evaluate ALLOB's efficacy in improving bone strength and reducing fracture risk in affected individuals. This trial represents a pivotal advancement in the pursuit of innovative treatments aimed at enhancing outcomes for osteogenesis imperfecta patients

- In March 2023, Mereo BioPharma Group plc announced positive topline results from its Phase 2b ASTER study evaluating setrusumab, a novel anti-sclerostin antibody, in adults with osteogenesis imperfecta. The study showed promising safety and efficacy, positioning setrusumab as a potential therapeutic breakthrough for this rare bone disorder

- In July 2023, Ultragenyx Pharmaceutical Inc. reported the treatment of the first patients in its late-stage clinical trials for setrusumab, targeting pediatric and young adult patients with osteogenesis imperfecta types I, III, and IV. The Phase 3 portion of the pivotal Phase 2/3 Orbit study is comparing setrusumab to placebo on fracture rates in patients aged 5 to under 26 years. In addition, the Phase 3 Cosmic study is underway, evaluating setrusumab versus intravenous bisphosphonate therapy in children aged 2 to under 5 years

- In October 2022, The Osteogenesis Imperfecta Federation Europe (OIFE) formally re-established itself as a new legal entity based in Belgium, following the dissolution of its previous registration in the Netherlands. This organizational restructuring is intended to streamline operations and enhance advocacy efforts, ultimately strengthening patient support and awareness initiatives throughout Europe

- In October 2021, Mereo BioPharma Group plc, in partnership with the Osteogenesis Imperfecta Federation Europe (OIFE) and the Osteogenesis Imperfecta Foundation (OIF), completed enrollment for the IMPACT Survey — the largest global data collection on osteogenesis imperfecta’s effects on patients, families, and caregivers. Gathering over 2,200 responses from approximately 65 countries in just three months, the survey’s findings are set to guide future collaborative efforts to improve diagnosis, treatment, and care, as well as accelerate new therapy availability

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.