Global Otc Medications Market

Market Size in USD Billion

USD

56.40 Billion

USD

100.58 Billion

2025

2033

USD

56.40 Billion

USD

100.58 Billion

2025

2033

| 2026 - 2033 | |

| USD 56.40 Billion | |

| USD 100.58 Billion | |

| % | |

|

Over-the-Counter (OTC) Medications Market Overview

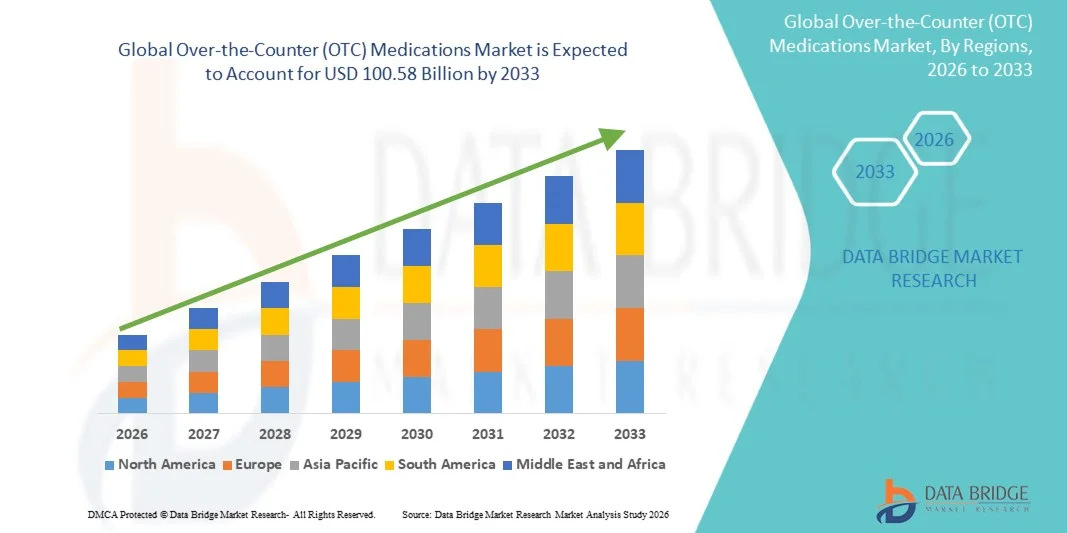

The Over-the-Counter (OTC) Medications Market was valued at USD 56.40 billion in 2025 and is projected to reach USD 100.58 billion by 2033, growing at a CAGR of 7.50% from 2026 to 2033. The market is experiencing steady growth driven by the increasing prevalence of common illnesses, growing consumer preference for self-medication, expanding accessibility of healthcare products, and continuous innovation in non-prescription drug formulations. Rising healthcare costs and increasing awareness regarding preventive healthcare are encouraging consumers to manage minor health conditions through over-the-counter (OTC) medications, supporting market expansion across both developed and emerging economies.

The growing burden of conditions such as cough and cold, allergies, gastrointestinal disorders, pain, fever, and dermatological issues is significantly increasing demand for OTC medications worldwide. In addition, expanding retail pharmacy networks, rising penetration of e-commerce healthcare platforms, and increasing availability of pharmacist-guided self-care solutions are enhancing product accessibility. Governments and healthcare systems are also promoting responsible self-medication to reduce the burden on healthcare facilities and optimize healthcare resources. Furthermore, advancements in drug delivery technologies, growing demand for convenient dosage forms, and increasing consumer focus on wellness and preventive healthcare continue to drive adoption of OTC medications globally.

Key Market Trends & Insights

- North America dominated the Over-the-Counter (OTC) Medications Market with the largest revenue share of 38.92% in 2025, supported by high consumer awareness regarding self-medication, widespread availability of OTC products, strong retail pharmacy networks, and increasing healthcare expenditure. The region benefits from favorable regulatory frameworks, high adoption of preventive healthcare practices, and growing demand for convenient treatment options for minor ailments.

- The branded OTC drugs segment dominated the market with a share of 57.36% in 2025, due to strong consumer trust, high brand recognition, and extensive marketing and promotional activities.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.3% from 2026 to 2033, fueled by expanding healthcare access, rising disposable incomes, increasing self-care awareness, and growing penetration of retail and online pharmacy channels across China, India, Japan, and Southeast Asian countries.

- Online Pharmacy is the fastest-growing distribution channel, projected to register a CAGR of 8.8% from 2026 to 2033, reflecting increasing digitalization of healthcare services, growing consumer preference for home delivery, wider product availability, and rapid expansion of e-commerce healthcare platforms globally.

- The Tablets segment dominates the dosage form category with a 36.87% revenue share in 2025, owing to ease of administration, longer shelf life, cost-effectiveness, accurate dosing, and widespread consumer acceptance across a broad range of OTC therapeutic categories.

- Retail Pharmacies account for 45.26% of the market in 2025, remaining the preferred distribution channel due to extensive product availability, pharmacist consultation services, immediate accessibility, and strong consumer trust in community pharmacy networks.

- The Generic Drugs segment is the fastest-growing category, with a CAGR of 8.1% from 2026 to 2033, driven by increasing demand for affordable healthcare solutions, rising acceptance of generic formulations, expanding regulatory approvals, and growing efforts to reduce overall healthcare expenditures while maintaining treatment effectiveness.

Market Size & Forecast

- Global Market Value (2025): USD 56.40 Billion

- Expected Market Value (2033): USD 100.58 Billion

- Forecast CAGR (2026–2033): 7.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Over-the-Counter (OTC) Medications Market Segmentation

|

Attributes |

Over-the-Counter (OTC) Medications Key Market Insights |

|

Segments Covered |

· By Product Type: Cough, Cold, and Flu Products; Analgesics; Dermatology Products; Gastrointestinal Products; Vitamins, Minerals, and Supplements (VMS); Weight-loss/Dietary Products; Ophthalmic Products; Sleeping Aids; and Other Product Types · By Dosage Form: Tablets; Hard Capsules; Powders; Ointments; Soft Capsules; Liquids; and Others · By Category: Branded Drugs and Generic Drugs · By Distribution Channel: Hospital Pharmacies; Retail Pharmacies; Online Pharmacy; and Other Distribution Channels |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Johnson & Johnson (U.S.) |

|

Market Opportunities |

· Rising Demand for Preventive Healthcare and Wellness Products · Expansion of E-Commerce and Online Pharmacy Platforms · Growth Potential in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Over-the-Counter (OTC) Medications Market Trends

Trend: Rising Shift Toward Self-Care and Expanding OTC Drug Switch Approvals

One of the most significant trends shaping the Over-the-Counter (OTC) Medications Market is the growing consumer preference for self-medication and preventive healthcare, supported by increasing awareness of minor disease management and easy access to pharmacy and online retail channels. Regulatory authorities are also accelerating prescription-to-OTC switches to improve accessibility and reduce healthcare system burden. For instance, in July 2023, the U.S. Food and Drug Administration (FDA) approved the first daily oral contraceptive Opill (norgestrel) for over-the-counter use, marking a major milestone in women’s healthcare accessibility. Similarly, in March 2023, the FDA approved Narcan (naloxone) nasal spray for OTC sale, significantly expanding access to life-saving opioid overdose treatment. These developments highlight a broader shift toward consumer-driven healthcare and increased availability of essential medicines without prescription barriers, strengthening OTC market expansion globally.

Over-the-Counter (OTC) Medications Market Dynamics

Key Market Driver: Rising Burden of Common Ailments and Expansion of Self-Medication Practices The increasing prevalence of common health conditions such as cough, cold, flu, allergies, gastrointestinal disorders, pain, and vitamin deficiencies is a major driver of the global OTC medications market. Growing urban lifestyles, environmental pollution, stress-related disorders, and seasonal infections are fueling frequent demand for easily accessible treatments. Consumers are increasingly opting for OTC products such as analgesics, antihistamines, antacids, and nutritional supplements to avoid physician visits for minor conditions. In addition, expansion of retail pharmacy chains and rapid growth of e-pharmacy platforms such as Amazon Pharmacy and Walmart Health & Wellness services are improving product availability and driving market penetration. Rising healthcare expenditure and government initiatives promoting responsible self-medication further support sustained demand growth across developed and emerging markets.

Key Restraint/Challenge: Risk of Misuse, Side Effects, and Regulatory Constraints

A key challenge in the OTC medications market is the potential risk of inappropriate self-medication, dosage errors, and delayed diagnosis of underlying conditions. Unlike prescription drugs, OTC medicines are widely accessible, which increases the likelihood of overuse or misuse, particularly for painkillers, cold medications, and sleep aids. This can lead to adverse drug reactions, dependency risks, or masking of serious medical conditions. In addition, regulatory authorities maintain strict frameworks for drug classification, labeling requirements, and safety monitoring, which can slow down prescription-to-OTC switch approvals. Variations in regulatory standards across regions such as the U.S., Europe, and Asia-Pacific also create complexity for global pharmaceutical companies seeking market expansion.

For instance, while OTC availability of drugs like ibuprofen and antihistamines has improved patient convenience, health agencies continue to issue warnings regarding long-term unsupervised use due to gastrointestinal, cardiovascular, or sedative side effects, reinforcing the need for consumer education and pharmacist guidance.

Key Market Opportunity: Digital Pharmacy Expansion and Prescription-to-OTC Switch Pipeline

The growing expansion of digital healthcare platforms and continued pipeline of prescription-to-OTC switch candidates present a major opportunity for the OTC medications market. Online pharmacies and telehealth services are enabling consumers to access medicines conveniently, compare products, and receive pharmacist consultations remotely. This is especially important in emerging economies where healthcare access remains limited. In parallel, pharmaceutical companies are actively pursuing regulatory approvals to convert prescription drugs into OTC versions, improving accessibility and market reach. For example, FDA approvals such as Opill (2023) and Narcan nasal spray (2023) demonstrate increasing regulatory openness toward OTC expansion for critical and preventive therapies. With rising demand for self-care, digital health integration, and expanding retail penetration in Asia-Pacific and Latin America, the OTC market is expected to unlock substantial growth opportunities over the coming years.

Over-the-Counter (OTC) Medications Market Scope

The Over-the-Counter (OTC) Medications market is segmented on the basis of product type, dosage form, category, and distribution channel.

- By Product Type

On the basis of product type, the Over-the-Counter (OTC) Medications Market is segmented into cough, cold, and flu products, analgesics, dermatology products, gastrointestinal products, vitamins, minerals, and supplements (VMS), weight-loss/dietary products, ophthalmic products, sleeping aids, and other product types. The analgesics segment dominated the market with a revenue share of 28.64% in 2025, owing to its widespread usage in managing pain-related conditions such as headaches, arthritis, muscle pain, fever, and post-operative discomfort. Increasing global prevalence of chronic pain disorders and lifestyle-related musculoskeletal conditions is significantly driving demand. Rising preference for self-medication and easy accessibility of OTC pain relievers in retail pharmacies and online platforms further strengthens segment dominance. Strong brand penetration of products such as ibuprofen, acetaminophen, and aspirin contributes to sustained sales growth. In addition, growing geriatric population worldwide, which is more prone to pain-related ailments, supports continuous consumption. High physician recommendation for mild-to-moderate pain management using OTC drugs also boosts adoption. Expanding pharmacy chains in emerging economies is improving product availability. Aggressive marketing campaigns by pharmaceutical companies are reinforcing consumer trust. Furthermore, affordability compared to prescription alternatives makes analgesics the most preferred OTC category globally. Continuous product innovation in fast-acting formulations is further enhancing demand. Overall, analgesics remain the backbone of OTC consumption globally.

The Vitamins, Minerals, and Supplements (VMS) segment is expected to register the fastest growth with a CAGR of 7.8% from 2026 to 2033, driven by rising health consciousness and preventive healthcare trends. Increasing awareness about immunity-boosting supplements post-COVID-19 pandemic has significantly accelerated demand. Consumers are increasingly adopting daily vitamin intake for overall wellness, energy, and nutritional balance. Growing prevalence of nutrient deficiencies, especially vitamin D, iron, and calcium deficiencies, is further supporting growth. Rising aging population globally is increasing consumption of bone health and immunity supplements. Expanding fitness and wellness trends among younger populations are also boosting demand. E-commerce platforms have made VMS products more accessible and affordable. Subscription-based supplement delivery models are gaining popularity in urban markets. Pharmaceutical companies are expanding functional nutrition product portfolios. Rising demand for herbal and natural supplements is another key trend supporting growth. Increasing endorsement by healthcare professionals is improving consumer trust. Overall, VMS is emerging as the fastest-expanding OTC category globally.

- By Dosage Form

On the basis of dosage form, the market is segmented into tablets, hard capsules, powders, ointments, soft capsules, liquids, and others. The tablets segment dominated the market with a share of 34.92% in 2025, due to high consumer acceptance, ease of administration, accurate dosing, and cost-effective manufacturing. Tablets are the most widely used dosage form across analgesics, cold and flu, gastrointestinal, and vitamin products. Their longer shelf life compared to liquid formulations makes them highly preferred in global distribution. Strong pharmaceutical manufacturing infrastructure supports large-scale production of tablets. Consumers prefer tablets due to portability and convenience. Retail pharmacies stock tablets in higher volumes due to high turnover. Tablets also offer stability advantages under varying climatic conditions. Branding and packaging innovations further enhance consumer preference. Pharmaceutical companies favor tablets due to lower production costs. High prescription-to-OTC switch drugs are commonly introduced in tablet form. Additionally, widespread physician and pharmacist recommendation strengthens adoption. Overall, tablets remain the dominant dosage form in OTC markets globally.

The liquid dosage form segment is expected to grow at the fastest CAGR of 7.2% from 2026 to 2033, driven by increasing suitability for pediatric and geriatric populations. Liquids provide faster absorption and quicker onset of action compared to solid dosage forms. Rising demand for flavored syrups and easy-to-consume formulations is boosting acceptance. Pediatric OTC medications heavily rely on liquid formulations for accurate dosing. Elderly patients with swallowing difficulties prefer liquid medicines. Technological advancements in taste-masking and stability enhancement are improving product appeal. Pharmaceutical companies are launching innovative liquid-based cold, cough, and vitamin formulations. Increasing home healthcare treatment trends are further driving usage. Online pharmacies are expanding availability of liquid OTC products. Rising demand for immunity syrups and herbal liquid supplements is also contributing. Improved packaging such as single-dose sachets is enhancing convenience. Overall, liquids are emerging as the fastest-growing OTC dosage form.

- By Category

On the basis of category, the market is segmented into branded drugs and generic drugs. The branded OTC drugs segment dominated the market with a share of 57.36% in 2025, due to strong consumer trust, high brand recognition, and extensive marketing and promotional activities. Major pharmaceutical companies invest heavily in advertising to maintain brand loyalty across global markets. Branded OTC drugs are perceived as safer and more effective by consumers. Strong presence in retail pharmacies enhances visibility and accessibility. Well-established distribution networks support consistent product availability. Consumers often rely on familiar brands for self-medication decisions. Pharmaceutical giants continuously innovate branded formulations for better efficacy. Premium pricing strategies also contribute to revenue dominance. Pharmacist recommendations further reinforce branded drug preference. High repeat purchase rates strengthen market share. Branding plays a crucial role in influencing OTC purchasing behavior. Overall, branded OTC products remain dominant due to trust and awareness advantages.

The generic OTC drugs segment is expected to grow at the fastest CAGR of 6.9% from 2026 to 2033, driven by rising demand for cost-effective healthcare solutions. Increasing healthcare expenditure pressures are pushing consumers toward affordable alternatives. Government initiatives promoting generic drug usage are supporting adoption globally. Expanding middle-class population in emerging economies is boosting demand. Retail pharmacies are increasingly stocking generic equivalents of branded drugs. Improved quality standards are enhancing consumer confidence in generics. Online pharmacies are offering competitive pricing on generic OTC products. Pharmaceutical companies are expanding generic product portfolios. Growing insurance limitations in some regions encourage self-pay generic purchases. Awareness about bioequivalence is improving acceptance. Economic inflation is further accelerating shift toward generics. Overall, generics are emerging as a high-growth OTC segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacy, and other distribution channels. The retail pharmacies segment dominated the market with a share of 46.81% in 2025, due to widespread availability, strong consumer trust, and immediate product access. Retail pharmacies serve as the first point of contact for OTC drug purchases globally. Pharmacist guidance enhances safe self-medication practices. Strong presence in urban and rural regions ensures accessibility. Established pharmacy chains dominate OTC distribution networks. Consumers prefer physical stores for urgent medication needs. Promotional discounts and in-store branding boost sales. Retail pharmacies also support cross-selling of OTC product categories. Strong supply chain integration ensures product availability. High footfall in pharmacies drives consistent revenue generation. Government licensing regulations ensure trust in retail channels. Overall, retail pharmacies remain the dominant OTC distribution channel.

The online pharmacy segment is expected to grow at the fastest CAGR of 8.4% from 2026 to 2033, driven by rapid digitalization and increasing consumer preference for convenience. Smartphone penetration and internet access are expanding globally. Home delivery services are enhancing medication accessibility. E-pharmacy platforms are offering discounts and subscription models. Telehealth integration is increasing OTC medicine prescriptions online. Consumers prefer privacy for purchasing sensitive health products. AI-driven recommendation systems are improving user experience. Digital payment adoption is supporting online transactions. Expansion of platforms like Amazon Pharmacy and regional startups is accelerating growth. COVID-19 accelerated shift toward online healthcare purchasing. Rural areas are benefiting from improved medicine access. Overall, online pharmacies are the fastest-growing OTC distribution channel.

Over-the-Counter (OTC) Medications Market Regional Analysis

North America dominated the Over-the-Counter (OTC) Medications Market and accounted for the largest revenue share of 38.92% in 2025, supported by high consumer awareness regarding self-medication, strong healthcare infrastructure, and widespread availability of OTC products across retail pharmacies, supermarkets, and online platforms. The region benefits from well-established regulatory frameworks such as the U.S. FDA OTC monograph system, which ensures safety, efficacy, and easy product accessibility. Rising healthcare expenditure and strong consumer preference for convenient treatment of minor ailments such as pain, cold, cough, and digestive disorders are further driving market growth. Increasing adoption of preventive healthcare practices and wellness-oriented consumption patterns is also strengthening demand. The presence of major pharmaceutical companies and strong brand penetration across analgesics, vitamins, and gastrointestinal products further supports regional dominance. High digital pharmacy adoption and expansion of e-commerce platforms such as Amazon Pharmacy and Walmart Health are improving product reach. Growing geriatric population and rising prevalence of lifestyle-related disorders are boosting OTC medication consumption. In addition, strong retail pharmacy chains such as CVS and Walgreens ensure easy product availability. Continuous product innovation and aggressive marketing strategies by key players further reinforce North America’s leadership position in the global OTC market. Overall, the region remains the most mature and high-value market globally.

U.S. Over-the-Counter (OTC) Medications Market Insight

The U.S. Over-the-Counter (OTC) Medications market is witnessing strong and sustained growth due to rising consumer inclination toward self-care, increasing healthcare costs, and growing preference for non-prescription treatment options. The country has one of the most advanced OTC regulatory systems, enabling smooth prescription-to-OTC switches for drugs such as pain relievers, allergy medications, and gastrointestinal treatments. High prevalence of chronic conditions such as headaches, obesity-related disorders, and seasonal allergies is significantly driving OTC consumption. Strong retail pharmacy infrastructure, including CVS Health, Walgreens Boots Alliance, and Walmart Pharmacy, ensures widespread accessibility. Rapid expansion of e-pharmacy services and telehealth integration is further improving OTC drug distribution. Increasing awareness of preventive healthcare and wellness supplements is boosting demand for VMS (vitamins, minerals, and supplements). The U.S. also has strong pharmaceutical R&D capabilities, leading to continuous product innovation in fast-acting and combination therapies. High consumer trust in branded OTC products supports market stability. In addition, digital health platforms and subscription-based wellness models are expanding product reach. Overall, the U.S. remains the largest individual OTC market globally with strong innovation-driven growth.

Europe Over-the-Counter (OTC) Medications Market Insight

The Europe Over-the-Counter (OTC) Medications market remains a key contributor to global revenue, driven by strong healthcare systems, increasing aging population, and high demand for self-medication solutions. Countries such as Germany, France, and the U.K. have well-regulated OTC frameworks that promote safe and effective drug usage. Rising prevalence of seasonal illnesses, gastrointestinal disorders, and musculoskeletal pain is fueling demand for OTC analgesics and cold & flu products. Strong pharmacy networks and pharmacist-led consultations support safe drug usage across the region. Increasing focus on preventive healthcare and wellness supplements is also supporting market expansion. Europe has a high penetration of branded OTC drugs, supported by strong consumer trust and pharmaceutical innovation. Growing adoption of digital pharmacies and cross-border e-commerce platforms is improving accessibility. Governments are also encouraging OTC switches to reduce healthcare burden on public systems. In addition, sustainability and natural/organic OTC product demand is rising rapidly. Overall, Europe continues to maintain a stable and mature OTC market with steady growth.

U.K. Over-the-Counter (OTC) Medications Market Insight

The U.K. Over-the-Counter (OTC) Medications market is experiencing steady growth, supported by a strong National Health Service (NHS) framework and increasing shift toward self-care and community pharmacy-based treatment. Rising demand for pain relief medications, cold and flu remedies, and gastrointestinal treatments is driving OTC consumption. Pharmacist-led consultations under NHS pharmacy first initiatives are improving access to OTC therapies. Increasing adoption of digital pharmacy platforms such as Boots Online Doctor and LloydsPharmacy Online is enhancing convenience. Growing awareness of preventive healthcare and wellness supplements is boosting demand for VMS products. The U.K. also has strong regulatory oversight by the MHRA, ensuring safety and quality standards. Rising aging population is increasing consumption of OTC pain and bone health products. Seasonal illness prevalence further supports consistent demand throughout the year. Expansion of retail pharmacy chains is improving accessibility in rural areas. Overall, the U.K. represents a highly structured and digitally evolving OTC market.

Germany Over-the-Counter (OTC) Medications Market Insight

The Germany Over-the-Counter (OTC) Medications market is expanding steadily due to strong pharmaceutical manufacturing capabilities and a highly structured healthcare system. Germany has one of the most regulated OTC frameworks in Europe, ensuring high product safety and consumer trust. Rising prevalence of gastrointestinal disorders, pain-related conditions, and respiratory illnesses is driving OTC demand. Strong pharmacy networks and pharmacist consultation requirements support responsible self-medication. Increasing preference for herbal and natural OTC medicines, particularly in gastrointestinal and sleep aid categories, is a key trend. Germany also has strong domestic pharmaceutical companies contributing to product innovation. High adoption of vitamins and dietary supplements among aging population is boosting VMS segment growth. Expansion of digital pharmacy platforms such as Shop Apotheke Europe is improving product accessibility. Government policies supporting healthcare efficiency are encouraging OTC usage for minor ailments. Overall, Germany remains one of the most stable and high-value OTC markets in Europe.

Asia-Pacific Over-the-Counter (OTC) Medications Market Insight

The Asia-Pacific Over-the-Counter (OTC) Medications market is expected to witness the fastest growth, with a CAGR of 8.3% from 2026 to 2033, fueled by rising healthcare access, increasing disposable incomes, and growing awareness of self-medication practices. Expanding retail pharmacy networks and rapid digitalization of healthcare services are improving OTC drug availability across China, India, Japan, and Southeast Asia. High population base and increasing prevalence of common illnesses such as cold, flu, digestive disorders, and vitamin deficiencies are driving strong demand. Government initiatives aimed at improving healthcare accessibility are further supporting market expansion. Rising penetration of online pharmacies such as PharmEasy, Tata 1mg, and JD Health is transforming distribution channels. Increasing urbanization and lifestyle changes are boosting demand for pain relief and wellness products. Growing awareness of preventive healthcare and immunity-boosting supplements is accelerating VMS consumption. Pharmaceutical companies are expanding regional manufacturing to meet growing demand. In addition, rising middle-class population is increasing affordability of OTC medicines. Overall, Asia-Pacific represents the most dynamic and high-growth OTC market globally.

Japan Over-the-Counter (OTC) Medications Market Insight

The Japan Over-the-Counter (OTC) Medications market is witnessing stable growth due to an aging population, strong healthcare infrastructure, and increasing demand for self-care solutions. High prevalence of lifestyle-related disorders such as gastrointestinal issues, sleep disorders, and chronic pain is driving OTC consumption. Japan has a well-regulated OTC classification system that supports safe self-medication practices. Increasing adoption of vitamins, herbal supplements, and digestive health products is a key trend. Strong retail pharmacy chains such as Matsumoto Kiyoshi support product availability nationwide. Digital pharmacy adoption is gradually increasing, improving access for elderly populations. High awareness of preventive healthcare is boosting demand for immunity-supporting supplements. Pharmaceutical innovation in low-dose and fast-acting formulations is strengthening market growth. Government policies promoting healthcare efficiency are encouraging OTC usage. Overall, Japan represents a mature but steadily growing OTC market.

China Over-the-Counter (OTC) Medications Market Insight

The China Over-the-Counter (OTC) Medications market is growing rapidly due to expanding healthcare infrastructure, rising disposable incomes, and increasing awareness of self-medication. High prevalence of respiratory infections, digestive disorders, and vitamin deficiencies is driving strong demand for OTC products. Government healthcare reforms are improving access to medicines in both urban and rural areas. Rapid expansion of online pharmacy platforms such as Alibaba Health and JD Health is significantly boosting OTC distribution. Increasing adoption of traditional Chinese medicine (TCM) in OTC formulations is a unique market driver. Strong domestic pharmaceutical manufacturing capabilities support large-scale production. Rising middle-class population is increasing spending on health and wellness products. Growing elderly population is boosting demand for chronic care OTC medications. Expansion of retail pharmacy chains is improving accessibility in lower-tier cities. In addition, increasing focus on preventive healthcare and immunity enhancement is driving VMS growth. Overall, China is one of the fastest-growing OTC markets globally with strong long-term potential.

Over-the-Counter (OTC) Medications Market Share

The Over-the-Counter (OTC) Medications industry is primarily led by well-established companies, including:

- Johnson & Johnson (U.S.)

- Haleon plc (U.K.)

- Bayer AG (Germany)

- Sanofi S.A. (France)

- Procter & Gamble Company (U.S.)

- Reckitt Benckiser Group plc (U.K.)

- Perrigo Company plc (Ireland)

- Kenvue Inc. (U.S.)

- Viatris Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Cipla Limited (India)

- Glenmark Pharmaceuticals Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Takeda Pharmaceutical Company Limited (Japan)

- Otsuka Holdings Co., Ltd. (Japan)

- Prestige Consumer Healthcare Inc. (U.S.)

- Alkem Laboratories Ltd. (India)

- Himalaya Wellness Company (India)

- Dabur India Ltd. (India)

- Church & Dwight Co., Inc. (U.S.)

- STADA Arzneimittel AG (Germany)

- Aurobindo Pharma Limited (India)

- Amneal Pharmaceuticals, Inc. (U.S.)

- Bausch Health Companies Inc. (Canada)

- Boehringer Ingelheim International GmbH (Germany)

- Pfizer Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Nestlé Health Science (Switzerland)

- GSK Consumer Healthcare Brands (U.K.)

- Zydus Lifesciences Limited (India)

- Torrent Pharmaceuticals Ltd. (India)

- Lupin Limited (India)

- Taisho Pharmaceutical Holdings Co., Ltd. (Japan)

- Hisamitsu Pharmaceutical Co., Inc. (Japan)

Latest Developments in Over-the-Counter (OTC) Medications Market

- In July 2022, GlaxoSmithKline completed the demerger of its Consumer Healthcare business to form Haleon, one of the world’s largest standalone OTC medicines companies. The separation included major global OTC brands such as Panadol, Advil, Sensodyne, and Voltaren. This strategic move created a pure-play consumer health leader focused entirely on over-the-counter medicines, oral care, and wellness products, significantly reshaping global competition in the OTC market.

- In May 2023, Kenvue Inc. was officially listed on the New York Stock Exchange following its spin-off from Johnson & Johnson, marking one of the largest IPOs in the consumer healthcare sector. The company manages leading OTC brands such as Tylenol, Motrin, and Benadryl, and the IPO raised approximately $3.8 billion. This event strengthened the global OTC industry structure by establishing Kenvue as a dedicated self-care and consumer health company

- Between 2020 and June 2021, the U.S. FDA approved six Rx-to-OTC switch applications, including allergy, pain relief, and head lice treatments. These approvals expanded consumer access to non-prescription medicines and reinforced the growing trend of prescription-to-OTC conversions globally, which remains a key growth driver for OTC market expansion

- In November 2024, the U.S. FDA proposed removing oral phenylephrine from over-the-counter cold and flu medicines after determining it is not effective as a nasal decongestant. The proposal impacted widely used OTC brands including Tylenol, Advil, and Benadryl formulations, and signaled increased regulatory scrutiny of active ingredients used in OTC cough and cold products

- In May 2026 (published FDA update), the U.S. Food and Drug Administration reaffirmed and updated the regulatory framework for prescription-to-OTC switch approvals, emphasizing stricter safety and efficacy requirements for non-prescription drug conversion. This reflects the ongoing expansion of Rx-to-OTC pathways, which continues to shape innovation and product pipeline strategies in the global OTC medications market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.