Global Paronychia Market

Market Size in USD Million

USD

631.55 Million

USD

1,177.64 Million

2024

2032

USD

631.55 Million

USD

1,177.64 Million

2024

2032

| 2025 - 2032 | |

| USD 631.55 Million | |

| USD 1,177.64 Million | |

| % | |

|

Paronychia Market Size

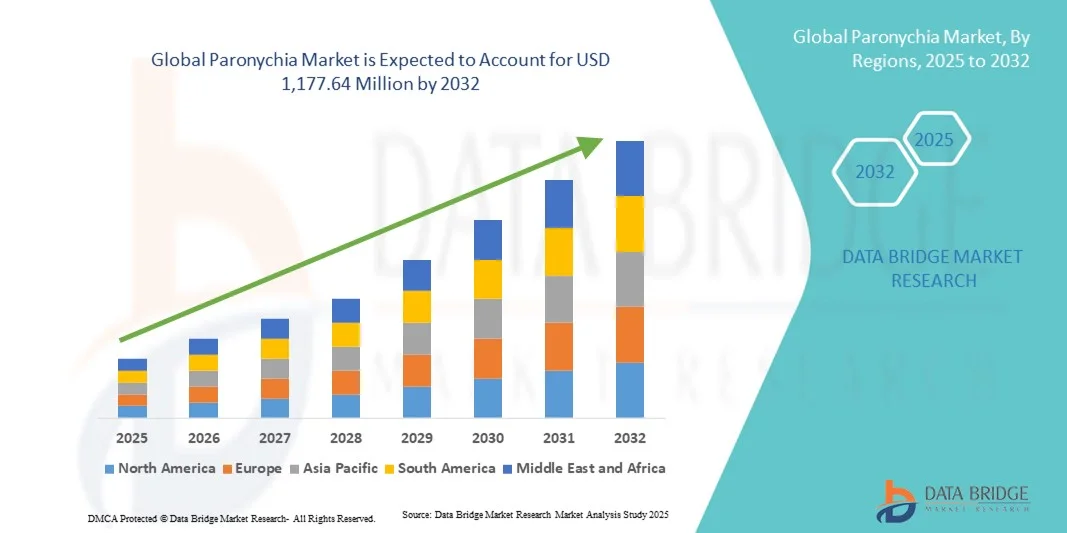

- The global paronychia market size was valued at USD 631.55 million in 2024 and is expected to reach USD 1,177.64 million by 2032, at a CAGR of 8.10% during the forecast period

- The market growth is largely fueled by the increasing prevalence of nail infections, rising consumer awareness regarding nail hygiene, and advancements in antifungal and antibacterial treatment options

- Furthermore, the demand for effective, safe, and rapid-acting treatment solutions, coupled with innovations in topical and systemic therapies, is establishing paronychia treatments as the preferred approach in both acute and chronic cases, thereby significantly boosting the industry's growth

Paronychia Market Analysis

- Paronychia, an infection of the skin surrounding the nails, represents a significant dermatological concern, with treatments increasingly focused on both acute and chronic cases, including topical and systemic therapies. The market is driven by the need for effective, fast-acting, and safe treatment solutions across both clinical and home-care settings

- The escalating demand for paronychia treatments is primarily fueled by the rising prevalence of nail infections, increasing awareness of personal hygiene, and advancements in antifungal and antibacterial therapies that improve treatment outcomes and patient compliance

- North America dominated the paronychia market with the largest revenue share of 33.6% in 2024, supported by advanced healthcare infrastructure, high patient awareness, and strong presence of leading pharmaceutical companies investing in research and development for innovative treatment options

- Asia-Pacific is expected to be the fastest-growing region in the paronychia market during the forecast period, driven by a large population base, increasing prevalence of fungal infections, and expanding healthcare infrastructure in countries such as China, India, and Japan

- Antifungal dominated the paronychia market with a market share of 47.4% in 2024, due to their ease of application, efficacy, and established use in both acute and chronic cases, making them the preferred first-line therapy for clinicians and patients

Report Scope and Paronychia Market Segmentation

|

Attributes |

Paronychia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Paronychia Market Trends

Rising Adoption of Rapid-Acting and Combination Therapies

- A significant and accelerating trend in the global paronychia market is the increasing use of combination antifungal and antibacterial therapies, which improve treatment efficacy and reduce recurrence

- For instance, dual-action creams combining antifungal and antibiotic agents are being developed to address both acute and chronic paronychia simultaneously

- Innovations in rapid-acting topical formulations allow faster symptom relief and shorter treatment durations, enhancing patient adherence and satisfaction

- The trend toward minimally invasive and home-use treatment options is enabling patients to manage mild infections without frequent clinical visits, supporting convenience and compliance

- Increased focus on natural and plant-based treatment formulations is emerging as a trend, appealing to patients seeking safer and low-side-effect options

- Telemedicine and digital health platforms are being leveraged to provide remote consultation and guidance for paronychia management, enhancing treatment accessibility

- This move toward more effective, patient-friendly, and integrated treatment solutions is fundamentally reshaping healthcare provider and patient expectations in paronychia care

- The demand for advanced topical and systemic therapies that offer faster results and improved outcomes is growing rapidly across both clinical and home-care settings

Paronychia Market Dynamics

Driver

Rising Prevalence of Nail Infections and Increased Awareness

- The increasing prevalence of nail infections, coupled with growing awareness of personal hygiene and preventive care, is a significant driver for the heightened demand for paronychia treatments

- For instance, rising cases of chronic paronychia among immunocompromised and diabetic patients are driving the need for more effective treatments

- As patients seek faster relief with minimal side effects, advanced antifungal and antibiotic therapies provide a compelling alternative to conventional treatments. Furthermore, the increasing number of dermatology clinics and home-care pharmacies offering accessible treatment solutions is accelerating adoption

- Easy availability of combination therapies and patient education on nail hygiene are key factors propelling the use of paronychia treatments globally

- The shift toward self-administered, convenient treatment regimens is further supporting market growth in both developed and emerging regions

- Growing investments by pharmaceutical companies in R&D for targeted paronychia therapies are expanding the pipeline of innovative treatments

- Rising prevalence of occupational nail injuries in healthcare, food service, and manual labor sectors is driving preventive and therapeutic treatment demand

Restraint/Challenge

Drug Resistance and High Cost of Innovative Treatments

- Concerns surrounding antimicrobial resistance and reduced efficacy of certain topical or systemic drugs pose a significant challenge to broader market penetration

- For instance, prolonged or improper use of antibiotics and antifungals has led to resistant strains, making treatment less predictable and outcomes variable

- Addressing these resistance issues through research, combination therapies, and adherence programs is crucial for maintaining treatment effectiveness

- In addition, the relatively high cost of advanced combination and rapid-acting therapies compared to generic options can hinder adoption in price-sensitive populations

- While some affordable alternatives exist, premium treatments with faster action or combination formulas remain out of reach for many patients, limiting market expansion

- Overcoming these challenges through patient education, cost optimization, and continued R&D for safe and effective therapies will be vital for sustained market growth

- Limited awareness about early signs of paronychia in rural and underdeveloped regions restricts timely treatment initiation, affecting market penetration

- Regulatory hurdles related to approval of new combination or innovative topical therapies in certain countries can delay market entry and commercialization

Paronychia Market Scope

The market is segmented on the basis of type, cause, diagnosis, treatment, route of administration, end user, and distribution channel.

- By Type

On the basis of type, the global paronychia market is segmented into acute paronychia and chronic paronychia. The acute paronychia segment dominated the market in 2024 with the largest revenue share of 62%, driven by its higher prevalence among the general population and rapid onset following nail injuries or minor trauma. Acute cases often require timely medical intervention, increasing demand for topical and oral therapies. Patients and clinicians prefer acute treatment options due to faster recovery and lower risk of complications. Healthcare providers also favor acute paronychia management as it reduces patient follow-ups and hospital visits. The high awareness of early symptoms and the need for immediate care further support the segment’s dominance. Rapid adoption of over-the-counter topical solutions also contributes to its strong market position.

The chronic paronychia segment is anticipated to witness the fastest growth rate of 8.5% CAGR from 2025 to 2032, fueled by increasing cases among immunocompromised individuals, diabetics, and frequent exposure to moisture in occupational settings. Chronic cases require longer-term treatment and innovative combination therapies, driving demand for specialized antifungal and antibacterial medications. Rising awareness of chronic nail conditions and preventive care contributes to adoption of chronic paronychia management solutions. Chronic paronychia also involves higher healthcare consultations, boosting hospital and clinic revenue. The segment benefits from increasing R&D in prolonged-acting treatment formulations.

- By Cause

On the basis of cause, the paronychia market is segmented into bacterial and yeast (fungal) infections. The bacterial segment dominated the market with a share of 58% in 2024, as bacterial infections such as Staphylococcus aureus are the most common triggers for acute paronychia. Bacterial infections often lead to rapid inflammation and pus formation, necessitating timely antibiotic therapy. Hospitals and clinics frequently stock bacterial treatment options due to high demand, contributing to market dominance. The prevalence of nail injuries in everyday life further supports the segment’s growth. Patients and physicians prefer quick-acting antibacterial treatments to minimize complications and absenteeism from work or daily activities. Increasing awareness of bacterial infection prevention also strengthens this segment.

The yeast segment is expected to register the fastest growth at 9% CAGR during the forecast period, driven by rising chronic paronychia cases caused by Candida species. Yeast infections are more common among individuals with prolonged exposure to water, chemicals, or occupational moisture, increasing demand for long-term antifungal therapy. The growth is further supported by increasing awareness of fungal nail infections and the need for preventive care in both developed and developing regions. Expansion of antifungal drug portfolios by pharmaceutical companies also fuels growth.

- By Diagnosis

On the basis of diagnosis, the paronychia market is segmented into physical examination and lab test. The physical examination segment dominated with a revenue share of 70% in 2024, due to the simplicity and cost-effectiveness of diagnosing paronychia based on visual inspection, symptom analysis, and patient history. Dermatologists and primary care physicians rely on physical exams for early-stage paronychia, reducing the need for expensive diagnostic procedures. Rapid diagnosis allows timely initiation of treatment, which is crucial in acute cases. Physical examination is widely accessible in both hospitals and clinics, ensuring broader adoption. It also enables immediate prescription of topical or oral therapies. The ease of use and minimal infrastructure requirements support its dominance.

The lab test segment is expected to witness the fastest growth with a CAGR of 8.2%, driven by increasing use of microbial cultures, fungal testing, and advanced diagnostic tools for chronic or complicated cases. Lab testing ensures accurate identification of pathogens, guiding targeted treatment and improving patient outcomes. Rising investment in diagnostic infrastructure and increasing awareness about treatment precision support this segment’s growth. Lab tests are increasingly used for treatment-resistant or recurring cases. Hospitals and specialized clinics are expanding their diagnostic capabilities, boosting this segment.

- By Treatment

On the basis of treatment, the paronychia market is segmented into home remedies, antibiotics, antifungal, topical ointments, and minor surgery. The antifungal segment dominated the paronychia market with a market share of 47.4% in 2024, driven by the rising prevalence of yeast-induced infections and chronic paronychia cases. Antifungal treatments are widely prescribed due to their high efficacy in treating fungal pathogens such as Candida species, which are common culprits of chronic infections. These therapies are preferred in both hospital and home-care settings for their safety, ease of use, and ability to be combined with topical or oral antibiotics for enhanced outcomes. Hospitals, clinics, and retail pharmacies stock antifungal medications as a first-line treatment, further contributing to their dominance. The availability of advanced antifungal formulations, including creams, gels, and sprays, supports patient adherence and faster recovery. Rising awareness about fungal infections and preventive care also bolsters the segment’s growth.

The minor surgery segment is expected to witness the fastest growth at 8.9% CAGR from 2025 to 2032, driven by increasing cases of chronic or complicated paronychia requiring nail bed drainage or removal. Minor surgical interventions are becoming more accepted due to their effectiveness in persistent infections. The segment is supported by skilled dermatologists and outpatient surgical clinics offering minimally invasive procedures. Rising awareness of surgical options among patients with recurrent paronychia fuels adoption. Insurance coverage for such procedures in developed regions further supports growth. Increasing integration of minor surgery with topical and systemic therapies enhances treatment outcomes and patient satisfaction.

- By Route of Administration

On the basis of route of administration, the paronychia market is segmented into oral and topical. The topical segment dominated the market with a revenue share of 67% in 2024, due to the ease of direct application, localized effect, and lower systemic side effects. Topical treatments are effective for mild-to-moderate infections and widely accepted in home-care and clinical settings. Patients prefer topical formulations for convenience and faster symptomatic relief. Physicians favor topical administration to reduce antibiotic resistance and minimize systemic exposure. Growing range of combination topical therapies supports segment growth. Availability in pharmacies and online channels enhances accessibility.

The oral segment is expected to register the fastest growth at 8.8% CAGR, driven by chronic or severe infections requiring systemic therapy. Oral medications are essential for treating persistent or complicated paronychia and are increasingly adopted in hospital and clinic settings. The growth is supported by combination therapy approaches integrating oral antibiotics with topical antifungals. Oral administration ensures better compliance in severe cases. Development of novel oral formulations enhances treatment outcomes.

- By End User

On the basis of end user, the paronychia market is segmented into hospitals, clinics, and others. The hospitals segment dominated with a market share of 54% in 2024, as hospitals are primary treatment centers for acute and complicated paronychia cases requiring professional diagnosis and systemic therapy. Hospitals provide access to both topical and oral treatment regimens, along with minor surgical interventions. The presence of dermatology departments and specialized care units further drives adoption. Hospitals are preferred for severe or recurring cases. The segment benefits from strong insurance coverage in developed regions. Availability of trained healthcare professionals ensures effective treatment.

The clinics segment is expected to witness the fastest growth at 9% CAGR, driven by increasing outpatient visits for mild-to-moderate paronychia, growing awareness of early treatment, and convenience of quick consultation. Dermatology and primary care clinics are expanding treatment services for paronychia, increasing market penetration. Clinics provide accessible care in urban and semi-urban areas. Home-based treatment guidance from clinics supports adoption. Rising telemedicine integration further accelerates clinic-based treatment uptake.

- By Distribution Channel

On the basis of distribution channel, the paronychia market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The retail pharmacy segment dominated with a revenue share of 48% in 2024, as it offers easy accessibility to topical ointments, antifungal creams, and home-use therapies. Retail pharmacies also provide pharmacists’ guidance for minor infections, increasing adoption. They are preferred for repeat purchases and immediate availability of medicines. Retail channels support over-the-counter sales of combination therapies. High consumer trust in local retail pharmacies strengthens this segment. Their wide presence across urban and semi-urban areas boosts reach.

The online pharmacy segment is expected to witness the fastest growth at 12% CAGR, fueled by increasing e-commerce penetration, convenience of home delivery, and rising adoption of self-care treatments. Patients are increasingly using online platforms to access specialized paronychia therapies, including combination creams and advanced topical formulations, supporting rapid market growth. Online channels also offer competitive pricing and wider product variety. Telemedicine recommendations often direct patients to online pharmacies. Digital marketing and subscription-based models enhance repeat purchases.

Paronychia Market Regional Analysis

- North America dominated the paronychia market with the largest revenue share of 33.6% in 2024, supported by advanced healthcare infrastructure, high patient awareness, and strong presence of leading pharmaceutical companies investing in research and development for innovative treatment options

- Patients and healthcare providers in the region prioritize early diagnosis and effective management of both acute and chronic paronychia, leading to widespread adoption of topical antifungal and antibiotic therapies

- This strong market presence is further supported by high healthcare spending, easy access to dermatology specialists, and a growing focus on preventive care, establishing North America as the most significant regional market for paronychia treatments

U.S. Paronychia Market Insight

The U.S. paronychia market captured the largest revenue share of 72% in North America in 2024, fueled by high awareness of nail hygiene, advanced healthcare infrastructure, and widespread availability of topical and oral antifungal and antibacterial treatments. Patients increasingly prioritize early diagnosis and effective management of both acute and chronic paronychia. The growing trend of self-care and over-the-counter topical therapies, combined with access to specialized dermatologists, further propels the market. Moreover, rising prevalence of chronic cases among diabetic and immunocompromised populations is significantly contributing to market expansion. The presence of key pharmaceutical companies investing in R&D for innovative treatment solutions also strengthens market growth.

Europe Paronychia Market Insight

The Europe paronychia market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of nail infections and the demand for effective treatments in both hospitals and clinics. Urbanization and rising healthcare expenditure are fostering adoption of advanced antifungal and combination therapies. European patients are also drawn to convenient topical treatments and minor surgical interventions when needed. The region is witnessing growth across residential care, dermatology clinics, and hospitals, with paronychia management becoming a standard preventive healthcare measure. In addition, regulatory frameworks supporting access to antifungal and antibacterial drugs enhance market penetration.

U.K. Paronychia Market Insight

The U.K. paronychia market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing incidence of nail infections and the growing focus on preventive healthcare. Concerns regarding recurrent infections encourage patients to seek professional care and reliable treatment options. The UK’s robust healthcare system and well-established dermatology clinics support the adoption of both topical and systemic therapies. Over-the-counter antifungal creams and combination therapies are widely used in home-care settings, supplementing clinical treatments. Moreover, rising awareness campaigns on nail hygiene and self-care practices are expected to stimulate market growth.

Germany Paronychia Market Insight

The Germany paronychia market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing patient awareness and demand for advanced treatment options. Germany’s well-developed healthcare infrastructure and emphasis on quality care promote the adoption of topical antifungal and antibiotic therapies. Patients show preference for early diagnosis and effective treatment of both acute and chronic cases. The integration of preventive care and dermatology consultation in routine healthcare services enhances market penetration. In addition, Germany’s focus on research and innovation in topical formulations supports segment growth. Public education on hygiene and occupational risk prevention further strengthens the market.

Asia-Pacific Paronychia Market Insight

The Asia-Pacific paronychia market is poised to grow at the fastest CAGR of 7.6% during 2025 to 2032, driven by rising prevalence of nail infections, growing population, and expanding healthcare infrastructure in countries such as China, India, and Japan. Increasing awareness of personal hygiene and preventive care is accelerating treatment adoption. Telemedicine and e-pharmacy platforms are facilitating access to antifungal and antibacterial therapies across urban and semi-urban regions. Government initiatives promoting healthcare access and dermatology services support growth. The availability of affordable topical and oral medications expands treatment accessibility to a wider population. In addition, rising occupational exposure to water and chemicals in industries further drives the need for effective paronychia management.

Japan Paronychia Market Insight

The Japan paronychia market is gaining momentum due to the country’s high awareness of healthcare, aging population, and demand for convenient treatment options. The prevalence of chronic paronychia among older adults is driving adoption of topical and oral therapies. Integration of dermatology clinics with home-care guidance facilitates effective management of mild-to-moderate infections. Patients increasingly prefer treatments that offer quick relief with minimal side effects. The market growth is further supported by innovations in antifungal and combination therapies. Public health campaigns emphasizing nail hygiene and preventive care contribute to expanding the patient base.

India Paronychia Market Insight

The India paronychia market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country’s large population, growing middle class, and increasing healthcare access. Awareness about nail hygiene and rising prevalence of fungal and bacterial infections are key factors driving market growth. Hospitals, clinics, and retail pharmacies are expanding their offerings of topical and oral therapies, making treatments more accessible. Government programs promoting preventive healthcare support adoption. Telemedicine and online pharmacies further enhance patient reach. In addition, cost-effective treatment options from domestic manufacturers are boosting market penetration across urban and semi-urban regions.

Paronychia Market Share

The Paronychia industry is primarily led by well-established companies, including:

- Lilly USA, LLC. (U.S.)

- GSK plc (U.K.)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- Teva Pharmaceutical Industries Ltd. (Israel)

- ConvaTec Group Plc (U.K.)

- Moberg Pharma AB (Sweden)

- Bausch Health Companies Inc. (Canada)

- Taro Pharmaceutical Industries Ltd. (U.S.)

- GLENMARK PHARMACEUTICALS LTD. (India)

- Fougera Pharmaceuticals Inc. (U.S.)

- Panacea Biotec Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

What are the Recent Developments in Global Paronychia Market?

- In July 2025, the U.S. Food and Drug Administration (FDA) approved ANZUPGO (delgocitinib) cream as the first and only topical pan-JAK inhibitor for the treatment of moderate-to-severe chronic hand eczema (CHE) in adults. While not specifically indicated for paronychia, this approval highlights the growing interest in advanced topical therapies for skin conditions

- In May 2025, updated recommendations for home treatment of paronychia were published. The guidelines suggest soaking the affected finger or toe in warm water with Epsom salt or antibacterial soap for 15 minutes, several times a day. This practice helps reduce swelling and promotes drainage of pus, offering an effective home remedy for mild cases of paronychia

- In February 2025, a study highlighted the use of the digital pressure test as a diagnostic tool for early-stage acute paronychia. This test involves applying gentle pressure to the nail fold to assess for signs of infection, aiding in timely diagnosis and treatment initiation. The adoption of this simple, non-invasive method enhances early detection and management of paronychia

- In December 2023, research indicated that zinc deficiency could be a contributing factor in chronic paronychia. Supplementing with 20 mg of zinc per day may help in the management of this condition, particularly in patients with identified deficiencies. This approach underscores the importance of nutritional assessment and supplementation in the comprehensive treatment of chronic paronychia

- In November 2023, a clinical guideline update emphasized the importance of proper drainage techniques for paronychia management. The guideline recommends making an incision parallel to the nail, at least 0.5 cm from the nail plate, on the non-contact aspect of the digit (radial aspect of the thumb, or ulnar aspect of the fingers) to avoid neurovascular bundles

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.