Global Polyanionic Cellulose Market

Market Size in USD Million

USD

837.69 Million

USD

966.19 Million

2024

2032

USD

837.69 Million

USD

966.19 Million

2024

2032

| 2025 - 2032 | |

| USD 837.69 Million | |

| USD 966.19 Million | |

| % | |

|

What is the Global Polyanionic Cellulose Market Size and Growth Rate?

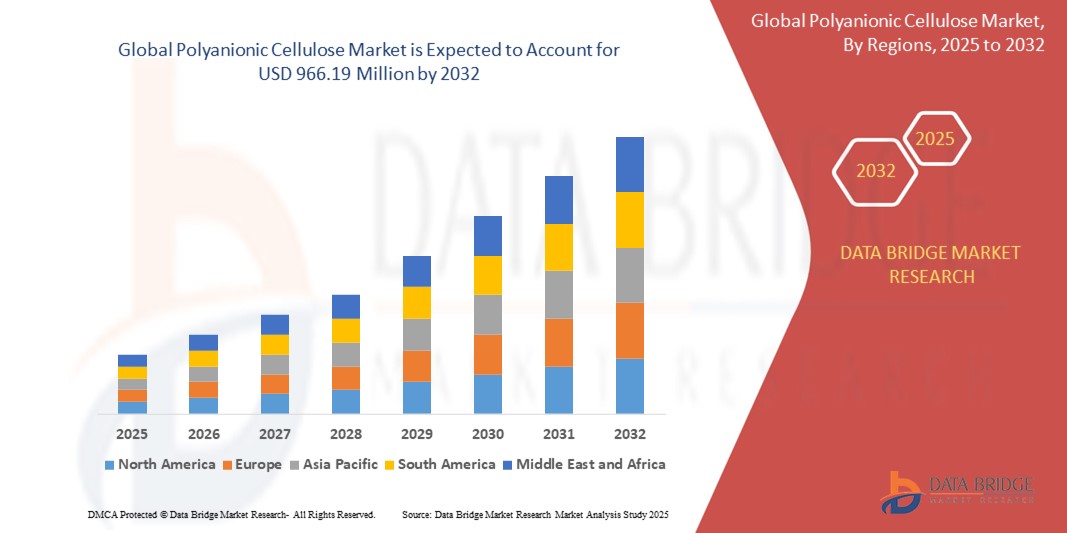

- The global polyanionic cellulose market size was valued at USD 837.69 million in 2024 and is expected to reach USD 966.19 million by 2032, at a CAGR of 1.80% during the forecast period

- Polyanionic cellulose (PAC) market growth is driven by advancements in oilfield services and water treatment technologies. New methods involve enhanced PAC formulations for improved performance and cost efficiency

- The market is expanding due to rising demand in hydraulic fracturing and drilling fluids, coupled with innovations in biodegradable and eco-friendly PAC solutions, promoting sustainable practices

What are the Major Takeaways of Polyanionic Cellulose Market?

- The growth of the oil and gas industry drives the PAC market as it's crucial in drilling fluids for viscosity control and fluid loss prevention. For instance, in major projects such as BP’s deepwater drilling initiatives in the Gulf of Mexico, PAC is essential for managing drilling conditions. The surge in exploration and production activities worldwide boosts PAC demand, supporting market expansion

- North America dominated the polyanionic cellulose market with the largest revenue share of 34.25% in 2024, driven by its extensive oil & gas activities, growing pharmaceutical production, and robust R&D investments across industrial applications

- Asia-Pacific polyanionic cellulose market is poised to grow at the fastest CAGR of 11.24% from 2025 to 2032, driven by large-scale infrastructure projects, rising demand from the food and beverage sector, and the expanding pharmaceutical landscape in countries such as China, India, and Japan

- The Regular Viscosity Polyanionic Cellulose segment dominated the market with the largest revenue share of 37.4% in 2024, driven by its widespread use across diverse industries including oil drilling, construction, and pharmaceuticals

Report Scope and Polyanionic Cellulose Market Segmentation

|

Attributes |

Polyanionic Cellulose Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Polyanionic Cellulose Market?

“Growing Demand for High-Performance Additives in Drilling and Construction”

- A key trend in the polyanionic cellulose (PAC) market is the increasing use of polyanionic cellulose as a performance-enhancing additive in oil drilling, construction, and pharmaceutical industries due to its exceptional rheological and filtration properties

- In the oil and gas sector, polyanionic cellulose is widely adopted as a fluid loss control agent in water-based drilling fluids. For instance, Schlumberger and other major service providers are incorporating polyanionic cellulose in advanced drilling systems to improve borehole stability and reduce fluid invasion

- In construction, polyanionic cellulose is being integrated into cement and mortar formulations for better water retention, improved workability, and enhanced adhesion. With the global boom in infrastructure projects, demand for such modified additives is rising

- In pharma, low-viscosity polyanionic cellulose grades are increasingly used as binders and stabilizers in tablet formulations. Companies such as Ashland offer pharma-grade polyanionic cellulose for these applications

- This trend is supported by the rise of sustainability-focused formulations, with polyanionic cellulose being favored for being biodegradable and non-toxic. Moreover, technological advancements have enabled the customization of polyanionic cellulose grades for industry-specific performance needs

- As industries continue to prioritize efficiency, cost savings, and eco-friendly alternatives, polyanionic cellulose is set to emerge as a key multifunctional additive across multiple high-growth sectors

What are the Key Drivers of Polyanionic Cellulose Market?

- Rising exploration activities in the oil & gas sector, especially in North America, the Middle East, and offshore fields, are significantly boosting the demand for PAC-based drilling fluids due to their superior filtration control and thermal stability

- For instance, in May 2024, Halliburton expanded its drilling operations in the Permian Basin, incorporating advanced PAC-based systems to enhance fluid efficiency and wellbore integrity

- In addition, the expanding construction industry, especially in emerging economies such as India and Indonesia, is driving PAC usage in cement and dry mix applications due to its ability to improve setting time and reduce water loss

- PAC is also gaining traction in pharmaceuticals and food processing as a thickener and binder, particularly in applications requiring high purity and safety. The rise in clean-label product demand is further supporting its adoption

- The growing emphasis on sustainability and the increasing regulatory pressure on synthetic additives are encouraging industries to adopt bio-based, non-toxic alternatives such as PAC, contributing to its robust market growth

Which Factor is challenging the Growth of the Polyanionic Cellulose Market?

- One of the primary challenges facing the PAC market is the volatile pricing and availability of raw materials, particularly cellulose derivatives derived from wood pulp or cotton linters, which are subject to supply chain disruptions and environmental constraints

- For instance, the 2023 raw material shortage in China due to stricter forestry regulations caused a ripple effect in PAC pricing globally, impacting procurement for key players in the oilfield chemicals sector

- Another challenge is the intense competition from alternative polymers such as carboxymethyl cellulose (CMC) and synthetic additives that offer similar performance in specific applications, sometimes at a lower cost

- Furthermore, the limited awareness about PAC’s multifunctional benefits in emerging markets, along with technical limitations in high-salinity environments, can restrict its full potential in critical applications

- To overcome these barriers, manufacturers need to invest in R&D for high-performance PAC grades, promote sustainable sourcing, and create strategic collaborations to stabilize raw material supply chains and broaden application awareness

How is the Polyanionic Cellulose Market Segmented?

The market is segmented on the basis of product type and end use.

- By Product Type

On the basis of product type, the polyanionic cellulose market is segmented into Low Viscosity Polyanionic Cellulose, Regular Viscosity Polyanionic Cellulose, High Viscosity Polyanionic Cellulose, and Extra High Viscosity Polyanionic Cellulose. The Regular Viscosity Polyanionic Cellulose segment dominated the market with the largest revenue share of 37.4% in 2024, driven by its widespread use across diverse industries including oil drilling, construction, and pharmaceuticals. Its balanced properties—such as moderate thickening, fluid loss control, and ease of solubility—make it a versatile choice in both water-based and salt-contaminated systems.

The High Viscosity Polyanionic Cellulose segment is projected to witness the fastest growth rate of 22.3% from 2025 to 2032, owing to increasing demand from industries requiring advanced rheological performance. This includes deepwater drilling, ceramic processing, and specialty chemical applications where superior suspension and film-forming properties are critical. Rising R&D investments aimed at optimizing drilling muds and filtration systems are further fueling this segment's growth.

- By End Use

On the basis of end use, the polyanionic cellulose market is segmented into Oil and Gas, Food and Beverage, Pharmaceutical, Agrochemical, Electronics, Leather Processing, Chemical, Printing, Plastic and Polymer, Ceramic, and Others. The Oil and Gas segment accounted for the largest market revenue share of 44.8% in 2024, owing to PAC’s critical role in drilling fluid formulations to control fluid loss, stabilize boreholes, and enhance operational efficiency in both onshore and offshore drilling environments.

The Pharmaceutical segment is expected to witness the fastest CAGR from 2025 to 2032, driven by growing applications in drug formulation, tablet binding, and controlled drug release systems. The rising demand for non-toxic, biocompatible excipients and clean-label formulations is further driving the integration of pharmaceutical-grade PAC in various therapeutic segments.

Which Region Holds the Largest Share of the Polyanionic Cellulose Market?

- North America dominated the polyanionic cellulose market with the largest revenue share of 34.25% in 2024, driven by its extensive oil & gas activities, growing pharmaceutical production, and robust R&D investments across industrial applications. The demand for efficient fluid loss control agents in drilling operations, along with increasing regulatory emphasis on eco-friendly additives, supports this dominance

- In addition, the region benefits from a mature chemicals infrastructure and a rising focus on performance-enhancing additives in construction and ceramics. The use of PAC as a thickener and binder across multiple applications further strengthens its market appeal

- High industrial automation, the adoption of sustainable formulations, and the availability of domestic manufacturers contribute to making North America a core hub for PAC production and utilization

U.S. Polyanionic Cellulose Market Insight

The U.S. polyanionic cellulose market captured the largest share in 2024 within North America, fueled by a well-established oil drilling sector, leading pharmaceutical firms, and growing environmental compliance mandates. The increasing adoption of PAC in advanced drilling fluids and its role in pharmaceutical binding and stabilization are accelerating market growth. Moreover, the U.S. benefits from a strong pipeline of R&D initiatives and a rising shift towards biodegradable alternatives, further boosting demand across multiple industries.

Europe Polyanionic Cellulose Market Insight

The Europe polyanionic cellulose market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising demand for clean-label and sustainable additives across food, pharmaceutical, and construction industries. Stricter environmental regulations and growing investments in renewable drilling projects are enhancing the region’s uptake of PAC. The integration of PAC in high-performance materials and coatings, especially in Western Europe, reflects a mature but innovation-driven market outlook.

U.K. Polyanionic Cellulose Market Insight

The U.K. polyanionic cellulose market is anticipated to grow at a noteworthy CAGR during the forecast period, led by increased pharmaceutical production, demand for organic additives in the food sector, and infrastructure modernization. The country’s emphasis on green chemistry and compliance with EU-derived safety standards positions PAC as a key material in construction, printing, and consumer product applications.

Germany Polyanionic Cellulose Market Insight

The Germany polyanionic cellulose market is expected to expand at a considerable CAGR during the forecast period, supported by advancements in chemical manufacturing and growing application of PAC in ceramics, pharmaceuticals, and oilfield operations. Germany’s commitment to sustainability and innovation in industrial polymers is boosting the preference for cellulose-based solutions that align with carbon-neutral goals and product efficiency expectations.

Which Region is the Fastest Growing Region in the Polyanionic Cellulose Market?

Asia-Pacific polyanionic cellulose market is poised to grow at the fastest CAGR of 11.24% from 2025 to 2032, driven by large-scale infrastructure projects, rising demand from the food and beverage sector, and the expanding pharmaceutical landscape in countries such as China, India, and Japan. The region’s low-cost manufacturing capabilities and favorable government policies promoting sustainable chemicals are accelerating PAC adoption. Rapid urbanization, drilling activity, and investments in water treatment further boost the region’s growth trajectory.

Japan Polyanionic Cellulose Market Insight

The Japan polyanionic cellulose market is gaining traction due to its innovation-centric chemical industry, demand for eco-conscious materials, and precision manufacturing standards. PAC is increasingly being integrated into pharmaceutical formulations, ceramics, and electronic components that require viscosity control and binding performance. Japan’s emphasis on regulatory compliance and quality assurance makes it a high-value market for advanced PAC products.

China Polyanionic Cellulose Market Insight

The China polyanionic cellulose market accounted for the largest revenue share in Asia-Pacific in 2024, propelled by well-established oil drilling sector, leading pharmaceutical firms, and growing environmental compliance mandates. China is a key supplier and consumer of PAC, benefiting from cost-effective production and growing demand across construction, textile, and agriculture sectors. Government incentives supporting green materials and increasing export potential further strengthen China’s market leadership.

Which are the Top Companies in Polyanionic Cellulose Market?

The polyanionic cellulose industry is primarily led by well-established companies, including:

- Dow (U.S.)

- Ashland (U.S.)

- SIDLEY CHEMICAL CO., LTD. (China)

- AL BATTAL FACTORY FOR CHEMICAL INDUSTRIES COMPANY (Saudi Arabia)

- Silverfern Chemical (U.S.)

- Chemstar Products Company (U.S.)

- Akzo Nobel N.V. (Netherlands)

- Changshu Wealthy Science and Technology Co., Ltd. (China)

- USK KIMYA CORP (Turkey)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Polyanionic Cellulose Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Polyanionic Cellulose Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Polyanionic Cellulose Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.