Global Programmatic Display Advertising Market

Market Size in USD Billion

USD

1,539.98 Billion

USD

17,917.22 Billion

2025

2033

USD

1,539.98 Billion

USD

17,917.22 Billion

2025

2033

| 2026 - 2033 | |

| USD 1,539.98 Billion | |

| USD 17,917.22 Billion | |

| % | |

|

Programmatic Display Advertising Market Overview

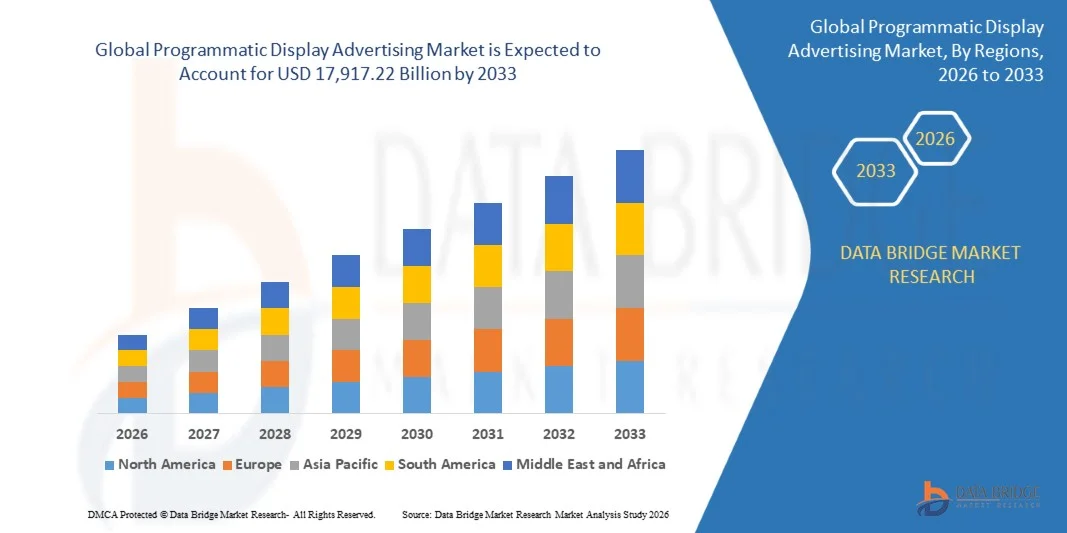

As per Data Bridge Market Research analysis The Programmatic Display Advertising Market was valued at USD 1,539.98 billion in 2025 and is projected to reach USD 17,917.22 billion by 2033, growing at a CAGR of 35.90% from 2026 to 2033. The market is witnessing strong expansion driven by the rapid shift toward automated, data-driven ad buying, increasing digital media consumption, and growing adoption of AI-powered advertising technologies across industries.

The rising penetration of smartphones, connected TV (CTV), and high-speed internet is significantly accelerating programmatic adoption among advertisers seeking real-time audience targeting and improved return on ad spend. In addition, advancements in machine learning, first-party data utilization, and privacy-compliant targeting solutions are reshaping the ecosystem, enabling more precise audience segmentation and campaign optimization across display, video, and native ad formats.

Key Market Trends & Insights

- North America dominated the Programmatic Display Advertising Market with a revenue share of 40.12% in 2025, supported by strong ad-tech infrastructure, high digital ad spends, and dominant DSP/SSP ecosystem presence.

- The Online Display segment led the market with a 36.42% share in 2025, driven by its widespread use across websites, portals, and desktop-based advertising inventory.

- Asia-Pacific is expected to be the fastest-growing region, registering a CAGR of 15.84% from 2026 to 2033, fueled by rapid digitalization, mobile-first consumer behavior, and expanding e-commerce ecosystems.

- Online Video are the fastest-growing ad format type, projected to register a CAGR of 17.84%, reflecting the surge in consumption of streaming content and digital entertainment platforms.

- The Demand-Side Platforms (DSPs) segment dominated the platform category with a 44.21% revenue share in 2025, led by strong adoption of automated real-time bidding, centralized campaign management capabilities, and advanced AI-driven audience targeting that enables advertisers to optimize media buying efficiency.

- Real-Time Bidding (RTB) accounted for 46.35% of the market, preferred by its high scalability, automated auction mechanism, and widespread adoption across open internet advertising.

- The SMBs segment is the fastest-growing enterprise size category, with a CAGR of 19.41%, driven by the increasing accessibility of self-serve programmatic platforms and lower entry barriers.

Market Size & Forecast

- Global Market Value (2025): USD 1,539.98 Billion

- Expected Market Value (2033): USD 17,917.22 Billion

- Forecast CAGR (2026–2033): 35.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Programmatic Display Advertising Market Segmentation

|

Attributes |

Programmatic Display Advertising Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Google LLC (U.S.) · The Trade Desk, Inc. (U.S.) · Meta Platforms, Inc. (U.S.) · Amazon.com, Inc. (U.S.) · Microsoft Corporation (U.S.) · Yahoo Inc. (U.S.) · Xandr Inc. (U.S.) · Adobe Inc. (U.S.) · PubMatic, Inc. (U.S.) · Magnite, Inc. (U.S.) · Index Exchange Inc. (Canada) · OpenX Technologies, Inc. (U.S.) · Criteo S.A. (France) · Taboola.com Ltd. (Israel) · Outbrain Inc. (U.S.) · Smaato, Inc. (Germany) · MediaMath, Inc. (U.S.) · Zeta Global Holdings Corp. (U.S.) · StackAdapt Inc. (Canada) · SmartyAds Inc. (U.K.) |

|

Market Opportunities |

· Rising adoption of CTV and streaming platforms programmatic inventory · Increasing demand for first-party data–driven targeting solutions · Expansion of retail media networks (RMNs) enabling brands to run programmatic ads directly on e-commerce platforms |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Programmatic Display Advertising Market Trends

Trend: Expansion of Video, CTV & Omnichannel Programmatic Growth

The market is witnessing a strong shift toward video advertising and Connected TV (CTV) as advertisers increasingly follow audiences away from traditional desktop browsing into streaming platforms and mobile-first ecosystems. Programmatic technology is enabling unified buying across display, video, in-app, and CTV inventory, allowing brands to run fully integrated omnichannel campaigns with consistent messaging and real-time optimization. AI-driven bidding systems are improving campaign efficiency by dynamically adjusting bids based on user behavior, contextual relevance, and predicted conversion probability. At the same time, retail media networks and premium publisher partnerships are expanding programmatic inventory availability, giving advertisers more controlled and brand-safe environments for high-impact placements.

For instance, global streaming platforms and large retail ecosystems are increasingly opening programmatic access to CTV and in-app video inventory, enabling advertisers to target audiences across multiple screens within a single campaign structure.

Programmatic Display Advertising Market Dynamics

Key Market Driver: Surge in Data-Driven and Automated Ad Buying

The major driver of the market is the rapid adoption of automated, data-driven advertising systems that replace traditional manual media buying with real-time, algorithm-based decision-making. Advertisers are increasingly leveraging Demand-Side Platforms (DSPs), AI models, and predictive analytics to identify high-value audiences and optimize ad placements within milliseconds through real-time bidding mechanisms. The growing use of first-party data collected from websites, apps, and customer databases is significantly improving targeting precision, especially in a privacy-restricted environment. This shift is also enabling better measurement of campaign performance, allowing advertisers to allocate budgets more efficiently across channels such as display, mobile, and video.

For instance, global brands are now integrating customer data platforms (CDPs) with programmatic DSPs to unify user profiles and deliver personalized advertising across multiple digital touchpoints.

Key Restraint/Challenge: Privacy Regulations and Signal Loss Constraints

One of the key challenges restricting market growth is the increasing global emphasis on data privacy and the gradual elimination of third-party cookies, which traditionally powered programmatic targeting and audience tracking. Regulations such as GDPR and similar privacy frameworks across regions have significantly limited the availability of granular user-level data, making it more difficult for advertisers to track behavior across websites and devices. In addition, browser restrictions and consent-based tracking models are reducing the effectiveness of retargeting and cross-site attribution, forcing advertisers to adapt their strategies. This shift is increasing operational complexity for advertisers and ad-tech platforms, which must now rely on less precise but compliant methods such as contextual targeting and aggregated audience modeling.

For instance, major browser platforms have introduced tracking prevention features that restrict third-party data sharing, pushing the industry toward privacy-first advertising architectures.

Key Market Opportunity: Growth of Retail Media Networks and First-Party Ecosystems

A significant growth opportunity in the market is the rapid expansion of retail media networks, where e-commerce platforms monetize their first-party shopper data by offering programmatic advertising solutions to brands. These ecosystems are highly valuable because they combine user browsing behavior, purchase intent signals, and transaction data, enabling extremely precise targeting and higher conversion rates compared to open-web advertising. The integration of retail media with programmatic platforms is also creating a new advertising ecosystem where brands can reach consumers directly at the point of purchase decision-making. In addition, the growing use of closed-loop measurement systems allows advertisers to track ad exposure directly to sales outcomes, improving ROI transparency.

For instance, major global e-commerce platforms are now providing self-serve DSP-like tools that allow brands to run programmatic campaigns directly within their retail environments using proprietary customer data.

Programmatic Display Advertising Market Scope

The programmatic display advertising market is segmented on the basis of ad format, platform, sales channel, and enterprise size.

- By Ad Format

On the basis of ad format, the Programmatic Display Advertising Market is segmented into online display, online video, mobile display, and mobile video. The Online Display segment dominated the market with a significant share of 36.42% in 2025, driven by its widespread use across websites, portals, and desktop-based advertising inventory. It remains a core format for branding and performance marketing due to its broad reach and cost efficiency. Advertisers prefer online display for programmatic campaigns because of its strong measurability, standardized ad units, and integration with DSP platforms. Continuous optimization through AI-based bidding has further strengthened its performance across industries such as retail, BFSI, and media. Despite competition from video formats, its scalability and low entry cost maintain its dominance in the ecosystem.

The Online Video segment is projected to register the fastest growth at a CAGR of 17.84% from 2026 to 2033, driven by increasing consumption of streaming content and digital entertainment platforms. Rising popularity of OTT services and short-form video content is significantly boosting advertiser spending in this category. Video ads offer higher engagement rates, improved brand recall, and stronger emotional impact compared to static formats. Programmatic integration allows real-time personalization and targeting based on user behavior and viewing history. Advancements in high-speed internet and 5G connectivity are further enhancing video ad delivery quality. This segment is rapidly becoming the preferred choice for performance-driven and brand storytelling campaigns.

- By Platform

On the basis of platform, the market is segmented into Demand-Side Platforms (DSPs), Supply-Side Platforms (SSPs), Ad Exchanges, and Data Management Platforms (DMPs). The Demand-Side Platforms (DSPs) segment dominated the market with a share of 44.21% in 2025, as advertisers increasingly rely on DSPs for centralized campaign management and automated media buying. DSPs enable real-time bidding, audience targeting, and cross-channel campaign optimization, making them essential for programmatic execution. Their integration with AI and machine learning improves bid accuracy and return on ad spend. DSPs also support cross-device tracking and advanced analytics, strengthening their role in omnichannel advertising strategies. Their dominance is reinforced by strong adoption among global advertisers and agencies.

The Data Management Platforms (DMPs) segment is expected to register the fastest growth at a CAGR of 16.92% from 2026 to 2033, driven by increasing demand for first-party data activation and audience intelligence. As third-party cookies decline, DMPs are becoming critical for collecting, organizing, and activating user data in a privacy-compliant manner. These platforms enable advertisers to build detailed audience segments and improve personalization across campaigns. Integration of DMPs with DSPs enhances targeting precision and campaign efficiency. Growing emphasis on data-driven marketing strategies is accelerating adoption across enterprises. Their role is becoming increasingly important in privacy-first advertising ecosystems.

- By Sales Channel

On the basis of sales channel, the market is segmented into Real-Time Bidding (RTB), Private Marketplaces (PMP), Hybrid, Direct Deals, and Automated Guaranteed (AG). The Real-Time Bidding (RTB) segment dominated the market with a share of 46.35% in 2025, due to its high scalability, automated auction mechanism, and widespread adoption across open internet advertising. RTB allows advertisers to bid for impressions in milliseconds, ensuring efficient budget utilization and precise targeting. It is widely used across mobile, display, and video inventory, making it the backbone of programmatic advertising. Continuous improvements in algorithmic bidding and AI optimization are enhancing its efficiency. Its dominance is further supported by strong integration with DSP ecosystems.

The Private Marketplaces (PMP) segment is projected to register the fastest growth at a CAGR of 18.27% from 2026 to 2033, driven by increasing demand for brand-safe, premium advertising environments. PMP allows advertisers to access high-quality publisher inventory with controlled bidding and transparency. Growing concerns around ad fraud and brand safety are pushing advertisers toward curated programmatic deals. PMP also offers better audience quality and higher engagement rates compared to open exchanges. Publishers benefit from higher yield optimization and direct advertiser relationships. Rising adoption among premium media publishers is accelerating its expansion.

- By Enterprise Size

On the basis of enterprise size, the market is segmented into SMBs and Large Enterprises. The Large Enterprises segment dominated the market with a share of 63.58% in 2025, driven by high digital advertising budgets and advanced adoption of programmatic technologies. Large organizations leverage DSPs, AI-driven analytics, and cross-channel strategies to optimize global campaigns. They invest heavily in data integration, customer segmentation, and omnichannel marketing automation. Their ability to scale campaigns across regions and platforms strengthens their dominance. Strong focus on brand building and performance marketing further supports their leadership position.

The SMBs segment is expected to register the fastest growth at a CAGR of 19.41% from 2026 to 2033, driven by increasing accessibility of self-serve programmatic platforms and lower entry barriers. Cloud-based advertising solutions and automated campaign tools are enabling small businesses to run targeted campaigns efficiently. Affordable DSP integrations and pay-per-click models are supporting adoption among cost-sensitive advertisers. Growing digitalization of SMEs across emerging economies is further accelerating demand. Simplified interfaces and AI-based campaign optimization are making programmatic advertising more accessible. This segment is rapidly expanding due to democratization of digital advertising technologies.

Programmatic Display Advertising Market Regional Analysis

North America dominated the Programmatic Display Advertising Market with a revenue share of 40.12% in 2025, supported by strong ad-tech infrastructure, high digital ad spends, and dominant DSP/SSP ecosystem presence. The region benefits from widespread use of Demand-Side Platforms (DSPs), high digital ad spending across retail and media sectors, and strong integration of AI-driven audience targeting technologies. Increasing investment in Connected TV (CTV), retail media networks, and data-driven marketing strategies continues to strengthen North America’s leadership position in the global market.

U.S. Programmatic Display Advertising Market Insight

The U.S. programmatic display advertising market is witnessing strong growth due to high digital ad spending, advanced ad-tech infrastructure, and widespread adoption of automated media buying solutions. The country’s mature ecosystem of Demand-Side Platforms (DSPs), Supply-Side Platforms (SSPs), and ad exchanges is driving large-scale programmatic adoption across retail, media, and technology sectors. In addition, increasing investment in Connected TV (CTV), retail media networks, and AI-driven audience targeting is accelerating demand across display, video, and mobile advertising formats.

Europe Programmatic Display Advertising Market Insight

The Europe programmatic display advertising market remains a key contributor to global revenue, driven by strong regulatory frameworks, rising digital transformation, and growing adoption of data-driven advertising strategies. The widespread use of programmatic platforms across retail, automotive, and BFSI sectors is supporting market expansion in the region. Increasing focus on privacy-compliant advertising, contextual targeting, and first-party data activation continues to strengthen programmatic adoption throughout Europe.

U.K. Programmatic Display Advertising Market Insight

The U.K. programmatic display advertising market is experiencing steady growth, supported by a highly developed digital advertising industry and strong presence of global ad-tech companies. Increasing adoption of AI-powered DSPs, real-time bidding systems, and omnichannel marketing strategies is driving market expansion across brands and agencies. Furthermore, growing investments in digital video, CTV advertising, and data-driven personalization are enhancing campaign efficiency and strengthening the U.K.’s position as a leading programmatic hub.

Germany Programmatic Display Advertising Market Insight

The Germany programmatic display advertising market is expanding steadily due to strong industrial digitization, high adoption of performance marketing, and increasing use of automated advertising technologies. Enterprises across automotive, manufacturing, and retail sectors are increasingly leveraging programmatic platforms for precise audience targeting and campaign optimization. Continuous advancements in data analytics, AI integration, and privacy-focused advertising solutions are further driving market growth in Germany.

Asia-Pacific Programmatic Display Advertising Market Insight

The Asia-Pacific programmatic display advertising market is expected to witness rapid growth, driven by rising internet penetration, expanding e-commerce ecosystems, and increasing mobile-first advertising adoption. Growing investments in digital infrastructure and the rapid expansion of OTT platforms are significantly boosting programmatic ad demand across the region. In addition, increasing adoption of AI-based ad targeting and real-time bidding systems is accelerating market expansion across both developed and emerging economies.

Japan Programmatic Display Advertising Market Insight

The Japan programmatic display advertising market is witnessing consistent growth due to strong technological advancement, high digital media consumption, and increasing adoption of automated advertising solutions. Advertisers in Japan are increasingly using DSPs and data-driven platforms to enhance targeting precision and campaign efficiency. Moreover, rising investment in video advertising, mobile marketing, and AI-based personalization is further supporting market growth.

China Programmatic Display Advertising Market Insight

The China programmatic display advertising market is growing rapidly, driven by massive digital commerce expansion, high smartphone penetration, and strong ecosystem of domestic ad-tech platforms. Increasing adoption of AI-powered advertising systems, mobile-first programmatic campaigns, and retail media networks is significantly boosting market demand. In addition, continuous innovation in e-commerce advertising and data-driven targeting is positioning China as one of the fastest-growing programmatic markets globally.

Programmatic Display Advertising Market Share

The programmatic display advertising industry is primarily led by well-established companies, including:

- Google LLC (U.S.)

- The Trade Desk, Inc. (U.S.)

- Meta Platforms, Inc. (U.S.)

- com, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Yahoo Inc. (U.S.)

- Xandr Inc. (U.S.)

- Adobe Inc. (U.S.)

- PubMatic, Inc. (U.S.)

- Magnite, Inc. (U.S.)

- Index Exchange Inc. (Canada)

- OpenX Technologies, Inc. (U.S.)

- Criteo S.A. (France)

- com Ltd. (Israel)

- Outbrain Inc. (U.S.)

- Smaato, Inc. (Germany)

- MediaMath, Inc. (U.S.)

- Zeta Global Holdings Corp. (U.S.)

- StackAdapt Inc. (Canada)

- SmartyAds Inc. (U.K.)

Latest Developments in Programmatic Display Advertising Market

- In November 2025, Amazon enhanced its advertising ecosystem by expanding its Demand-Side Platform (DSP) capabilities with deeper integration of retail media data and connected TV (CTV) inventory, leveraging first-party shopping insights to improve targeting precision and strengthen competition in the global programmatic advertising market

- In October 2025, The Trade Desk advanced retail media integration by partnering with Koddi, enabling advertisers to programmatically access onsite retail inventory and unify commerce media with broader omnichannel campaign strategies, strengthening the convergence of retail media and open internet advertising.

- In September 2025, the IAB Tech Lab launched the Deals API, a major industry initiative aimed at standardizing programmatic deal workflows across DSPs and SSPs, improving transparency, reducing manual errors, and enabling more efficient private marketplace transactions across the ecosystem

- In June 2025, the company further strengthened programmatic capabilities through the integration of generative AI creative solutions with Rembrand, allowing advertisers to deliver more contextual and personalized advertising experiences within video and influencer content, improving engagement and automation in creative workflows

- In April 2025, The Trade Desk expanded its programmatic ecosystem by introducing Deal Desk within its Kokai platform, enhancing transparency and optimization of private marketplace (PMP) deals by enabling real-time monitoring of deal performance, pacing, and inventory quality

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.