Global Sarcopenia Treatment Market

Market Size in USD Billion

USD

3.03 Billion

USD

4.45 Billion

2024

2032

USD

3.03 Billion

USD

4.45 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.03 Billion | |

| USD 4.45 Billion | |

| % | |

|

Sarcopenia Treatment Market Size

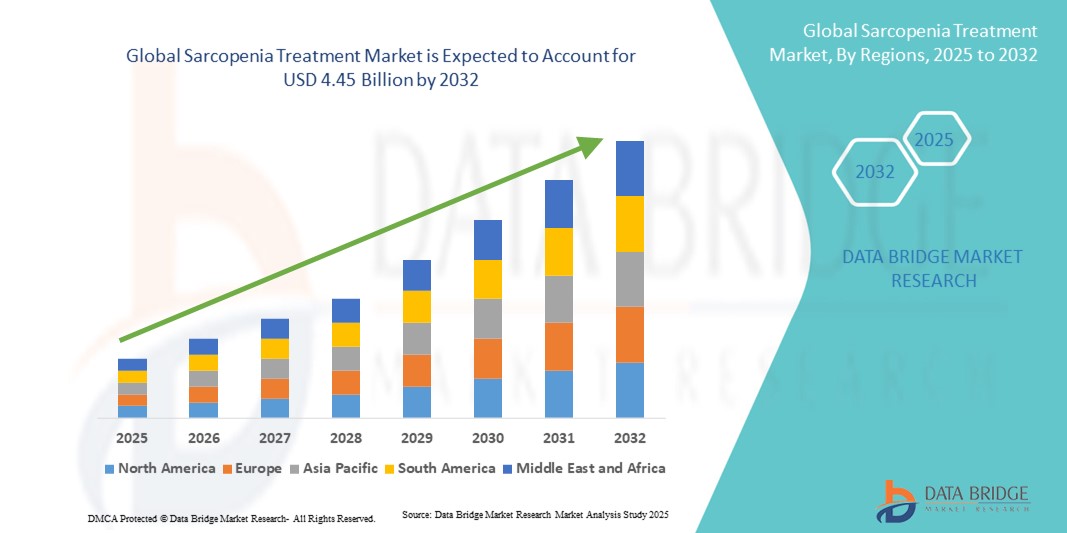

- The global sarcopenia treatment market size was valued at USD 3.03 billion in 2024 and is expected to reach USD 4.45 billion by 2032, at a CAGR of 4.9% during the forecast period

- The market growth is largely fueled by the rising prevalence of age-related muscle degeneration, increasing geriatric population, and growing awareness about maintaining muscle health through therapeutic interventions

- Furthermore, advancements in pharmacological treatments, nutritional supplements, and exercise-based therapies are driving demand for effective sarcopenia management solutions. These converging factors are accelerating the adoption of sarcopenia treatments, thereby significantly boosting the industry's growth

Sarcopenia Treatment Market Analysis

- Sarcopenia treatments, including medications, vitamin/dietary supplements, and other therapeutic interventions, are increasingly vital components of elderly care and preventive health management in both developed and emerging markets due to their efficacy in improving muscle mass, strength, and functional mobility

- The escalating demand for sarcopenia treatments is primarily fueled by the growing geriatric population, rising prevalence of age-related muscle degeneration, increasing healthcare expenditure, and heightened awareness about maintaining muscle health through preventive and therapeutic measures

- North America dominated the sarcopenia treatment market with the largest revenue share of 39.5% in 2024, characterized by early adoption of advanced therapeutics, well-established healthcare infrastructure, and a strong presence of key pharmaceutical and nutraceutical players, with the U.S. witnessing significant uptake in clinical therapies and nutritional supplementation for sarcopenia management

- Asia-Pacific is expected to be the fastest-growing region in the sarcopenia treatment market during the forecast period due to increasing aging population, rising healthcare awareness, and expanding access to treatment options in urban and semi-urban areas

- Medications segment dominated the sarcopenia treatment market with a market share of 41.9% in 2024, driven by continuous R&D, increasing drug approvals, and established efficacy in improving muscle mass and strength in elderly patients

Report Scope and Sarcopenia Treatment Market Segmentation

|

Attributes |

Sarcopenia Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Sarcopenia Treatment Market Trends

Integration of Advanced Therapeutics and Digital Health Tools

- A significant and accelerating trend in the global sarcopenia treatment market is the integration of advanced pharmacological therapies with digital health tools such as telemedicine platforms, wearable fitness trackers, and mobile health apps, enhancing patient monitoring and personalized care

- For instance, some digital platforms now allow clinicians to remotely track muscle mass, exercise adherence, and nutritional intake, enabling timely adjustments to treatment plans and improving patient outcomes

- Advanced therapeutics, including selective androgen receptor modulators (SARMs) and novel peptide-based drugs, are increasingly being combined with monitoring tools to provide personalized treatment and better adherence. For instance, certain clinics in Europe and North America integrate wearable activity trackers to optimize exercise-based interventions alongside pharmacological therapies

- The seamless integration of digital health platforms with treatment regimens allows centralized monitoring of multiple health parameters, including muscle strength, nutrition, and physical activity, creating a unified management plan for sarcopenia patients

- This trend toward more precise, technology-enabled, and patient-centered care is reshaping expectations for sarcopenia management. Consequently, companies and healthcare providers are developing digitally integrated treatment programs with real-time feedback, adherence reminders, and outcome tracking

- The demand for therapeutics combined with digital monitoring solutions is growing rapidly across both hospitals and home healthcare settings, as patients and caregivers increasingly prioritize convenience, personalization, and measurable treatment effectiveness

Sarcopenia Treatment Market Dynamics

Driver

Rising Geriatric Population and Awareness of Muscle Health

- The increasing prevalence of age-related muscle loss among the elderly, coupled with growing awareness about maintaining functional mobility, is a major driver for the heightened demand for sarcopenia treatments

- For instance, in March 2024, a clinic in the U.S. integrated a multidisciplinary sarcopenia program combining nutrition, exercise, and pharmacotherapy to address the rising elderly patient population

- As patients and caregivers become more aware of the impact of sarcopenia on independence and quality of life, treatments that improve muscle mass, strength, and mobility offer a compelling intervention over standard care

- Furthermore, the growing adoption of preventive healthcare practices and focus on active aging are making sarcopenia treatments an integral component of geriatric care programs, offering measurable functional improvements

- The accessibility of combination therapy approaches, including medications, dietary supplements, and physiotherapy, as well as digital monitoring tools, are key factors propelling the adoption of sarcopenia treatments in hospitals, specialty clinics, and home healthcare settings

Restraint/Challenge

Limited Awareness, High Treatment Costs, and Regulatory Hurdles

- Concerns surrounding limited awareness about sarcopenia and the high costs of advanced treatments pose significant challenges to broader market penetration, particularly in developing regions

- For instance, low adoption rates are reported in rural areas where patients and caregivers are unfamiliar with preventive therapies and nutraceutical interventions

- Addressing these challenges through patient education, awareness campaigns, and inclusion of treatments in insurance coverage is crucial for building market acceptance. For instance, certain European programs are providing subsidized supplements and therapy sessions to enhance accessibility

- In addition, regulatory hurdles related to clinical approval for new pharmacological therapies and nutraceutical claims can delay market entry, limiting the availability of innovative treatments in some regions

- While costs are gradually decreasing with increasing generic availability, the perceived premium for advanced pharmacological interventions and digital monitoring tools can still hinder widespread adoption, especially among price-sensitive populations

Sarcopenia Treatment Market Scope

The market is segmented on the basis of treatment type, type, stages, route of administration, gender, end user, and distribution channel.

- By Treatment Type

On the basis of treatment type, the sarcopenia treatment market is segmented into medications, vitamin/dietary supplements, and others. The medications segment dominated the market with the largest market revenue share of 41.9% in 2024, driven by the growing prevalence of age-related muscle loss and the increasing number of drug approvals targeting sarcopenia. Healthcare providers and geriatric clinics often prioritize medications for patients requiring pharmacological intervention, as these therapies directly target muscle mass and strength improvement. The segment also sees strong demand due to the combination of medications with physiotherapy and nutritional support, offering comprehensive care. Medications are widely prescribed in both hospital and outpatient settings, enhancing their market presence. Furthermore, continuous R&D and clinical trials bolster the adoption of pharmacological solutions for sarcopenia.

The vitamin/dietary supplements segment is anticipated to witness the fastest growth rate of 7.2% from 2025 to 2032, fueled by increased consumer awareness about nutrition’s role in maintaining muscle health. Supplements such as vitamin D, calcium, and protein powders are commonly recommended for early-stage sarcopenia management. The convenience of over-the-counter availability and ease of self-administration drives adoption among aging populations. These products are also increasingly integrated into preventive healthcare programs and home healthcare services. Growing research into synergistic effects of supplements with exercise and medications further accelerates their uptake. Retail and e-commerce distribution channels contribute significantly to the segment’s rapid expansion.

- By Type

On the basis of type, the sarcopenia treatment market is segmented into primary sarcopenia and secondary sarcopenia. The primary sarcopenia segment dominated the market with the largest revenue share of 58% in 2024, driven by age-related muscle degeneration without underlying disease. Healthcare providers focus on early diagnosis and preventive management for primary sarcopenia, increasing treatment uptake. Aging populations in developed countries are the key consumers of therapeutic interventions for this type. Public health initiatives promoting active aging and muscle maintenance contribute to market dominance. Integration of physical therapy, medications, and nutrition strategies enhances outcomes for primary sarcopenia patients. In addition, awareness campaigns targeting seniors reinforce adoption of preventive treatments.

The secondary sarcopenia segment is expected to witness the fastest growth rate of 8.1% from 2025 to 2032, fueled by rising prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders that exacerbate muscle loss. Patients with secondary sarcopenia increasingly seek specialized treatment plans combining disease management with muscle restoration therapies. Growing recognition of secondary sarcopenia in clinical guidelines is accelerating the adoption of integrated care approaches. Pharmaceutical and nutraceutical innovations targeting underlying causes drive market growth. Awareness campaigns and physician recommendations further support the segment’s expansion. The demand for personalized interventions makes secondary sarcopenia a fast-growing focus area.

- By Stages

On the basis of stages, the sarcopenia treatment market is segmented into pre-sarcopenia, sarcopenia, and severe sarcopenia. The pre-sarcopenia segment dominated the market with the largest revenue share of 44% in 2024, driven by early diagnosis and preventive interventions. Patients and healthcare providers focus on resistance training, nutritional support, and supplements to halt progression. Regular screening programs for at-risk populations increase treatment adoption. Public awareness campaigns emphasize maintaining muscle mass before functional decline occurs. Clinics and home healthcare services provide tailored early-stage programs. Early intervention improves long-term outcomes, supporting market dominance.

The severe sarcopenia segment is expected to witness the fastest growth rate of 7.9% from 2025 to 2032, due to increasing life expectancy and higher prevalence of frailty in aging populations. Severe sarcopenia requires comprehensive care, including medications, physiotherapy, and nutritional support. Hospitals and rehabilitation centers are key service providers for this stage. Innovative treatment protocols and clinical trials for advanced therapies contribute to rapid market growth. Increasing recognition of functional impairment and mobility loss drives patient demand. Integrated care models for severe sarcopenia are being adopted globally, enhancing treatment access and effectiveness.

- By Route of Administration

On the basis of route of administration, the sarcopenia treatment market is segmented into oral, injectable, and others. The oral segment dominated the market with the largest revenue share of 87% in 2024, driven by ease of administration, high patient compliance, and widespread use of medications and supplements. Oral therapies are preferred for both preventive and therapeutic purposes. Convenience of daily intake supports adoption among elderly populations. Integration with exercise and diet regimens improves treatment effectiveness. Home healthcare programs rely heavily on oral medications. Formulation improvements increase bioavailability and patient satisfaction.

The injectable segment is expected to witness the fastest growth rate of 8.2% from 2025 to 2032, fueled by the development of biologics, peptide-based therapies, and long-acting formulations. Injectable treatments are preferred for advanced sarcopenia or patients with low adherence to oral regimens. Clinical trials and new drug approvals are boosting market expansion. Hospitals and specialty clinics are key adoption points. Injectable therapies offer rapid efficacy in increasing muscle mass and strength. Growing patient awareness about injectable options supports rapid uptake.

- By Gender

On the basis of gender, the sarcopenia treatment market is segmented into male and female. The male segment dominated the market with the largest revenue share of 61% in 2024, driven by higher diagnosis rates and more noticeable muscle loss in men. Testosterone decline with aging contributes to earlier sarcopenia onset. Men are often prioritized in clinical interventions. Research into gender-specific treatment protocols enhances targeted care. Awareness campaigns for men’s health support adoption. Combination therapies with nutrition and exercise improve outcomes, reinforcing market dominance.

The female segment is expected to witness the fastest growth rate of 7.5% from 2025 to 2032, due to increased postmenopausal susceptibility and growing awareness of preventive care. Hormonal changes accelerate muscle loss in women. Targeted interventions, including resistance training and supplementation, support treatment uptake. Rising healthcare access and education for women enhance adoption. Research and clinical studies focusing on female-specific sarcopenia are expanding. Healthcare providers are increasingly emphasizing early intervention for women, boosting growth.

- By End User

On the basis of end user, the sarcopenia treatment market is segmented into hospitals, specialty clinics, home healthcare, and others. The hospitals segment dominated the market with the largest revenue share of 49% in 2024, driven by access to specialized care, diagnostic tools, and multidisciplinary treatment options. Hospitals manage advanced sarcopenia cases requiring pharmacological therapy and physiotherapy. Inpatient care allows tailored treatment plans. Geriatric wards integrate sarcopenia management into routine care. Collaboration among specialists improves patient outcomes. Hospital adoption is supported by clinical guidelines emphasizing evidence-based interventions.

The home healthcare segment is expected to witness the fastest growth rate of 8% from 2025 to 2032, fueled by aging-in-place trends and telehealth adoption. Remote monitoring and digital tools enable personalized care at home. Patients benefit from exercise programs, dietary guidance, and medication management. Convenience and comfort increase patient adherence. Expansion of home healthcare networks supports treatment accessibility. Growth is further driven by the integration of wearable devices and virtual consultations.

- By Distribution Channel

On the basis of distribution channel, the sarcopenia treatment market is segmented into direct tender, retail sales, and others. The direct tender segment dominated the market with the largest revenue share of 52% in 2024, driven by institutional procurement for hospitals, geriatric centers, and healthcare organizations. Bulk purchasing ensures consistent supply and cost savings. Government and healthcare programs often use tendering to supply medications and supplements. Efficiency and transparency in procurement support widespread adoption. Strategic partnerships with pharmaceutical companies ensure availability. Tender-based distribution aligns with national health policies targeting sarcopenia management.

The retail sales segment is expected to witness the fastest growth rate of 7.8% from 2025 to 2032, fueled by the increasing popularity of over-the-counter supplements and online sales platforms. Aging populations prefer convenient access through pharmacies and e-commerce. Preventive healthcare awareness campaigns drive direct consumer purchases. Retail channels enable rapid product availability and variety. Digital marketing and online platforms further support segment growth. Consumers increasingly seek self-management options, making retail sales a key growth driver.

Sarcopenia Treatment Market Regional Analysis

- North America dominated the sarcopenia treatment market with the largest revenue share of 39.5% in 2024, characterized by early adoption of advanced therapeutics, well-established healthcare infrastructure, and a strong presence of key pharmaceutical and nutraceutical players

- Patients and healthcare providers in the region highly value the accessibility of medications, nutritional supplements, and integrated care programs, which improve muscle mass, strength, and functional mobility in elderly populations

- This widespread adoption is further supported by high healthcare spending, strong clinical research activity, and early adoption of preventive care initiatives, establishing sarcopenia treatments as a preferred solution for hospitals, specialty clinics, and home healthcare services

U.S. Sarcopenia Treatment Market Insight

The U.S. sarcopenia treatment market captured the largest revenue share of 82% in 2024 within North America, driven by the high prevalence of age-related muscle loss and the growing geriatric population. Patients and caregivers are increasingly prioritizing interventions that improve muscle strength, mobility, and quality of life. The widespread adoption of preventive healthcare programs, coupled with advanced diagnostic tools and clinical guidelines, further propels the market. Moreover, the integration of medications, nutritional supplements, and physical therapy in coordinated care programs is enhancing treatment outcomes. Digital health platforms, telemedicine, and home monitoring devices are also contributing to the market’s expansion. The availability of insurance coverage and reimbursement policies strengthens adoption in both hospitals and home healthcare services.

Europe Sarcopenia Treatment Market Insight

The Europe sarcopenia treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by well-established geriatric care programs and national health initiatives targeting age-related muscle decline. Increasing urbanization and rising awareness of preventive healthcare are fostering adoption of medications, supplements, and exercise-based interventions. European patients are also drawn to integrated care approaches that combine clinical supervision with home-based therapy. The region is witnessing growth across hospitals, specialty clinics, and home healthcare services. Investments in research and development, along with clinical trials for new therapeutics, are further stimulating market growth. Cross-border healthcare collaborations are enhancing access to innovative sarcopenia treatments across multiple countries.

U.K. Sarcopenia Treatment Market Insight

The U.K. sarcopenia treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of sarcopenia and the importance of muscle health in aging populations. Rising incidence of chronic conditions, coupled with preventative healthcare programs, encourages both patients and healthcare providers to adopt comprehensive treatment solutions. The U.K.’s robust healthcare infrastructure and widespread availability of medications and nutritional supplements are supporting market expansion. Integration of sarcopenia management into routine geriatric care programs is further accelerating adoption. Digital health tools, such as teleconsultations and remote monitoring, enhance patient engagement and adherence. Government initiatives promoting healthy aging reinforce market growth in both clinical and home care settings.

Germany Sarcopenia Treatment Market Insight

The Germany sarcopenia treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of age-related muscle loss and the demand for evidence-based interventions. Germany’s advanced healthcare infrastructure and strong focus on innovation support the adoption of pharmacological therapies, dietary supplements, and exercise programs. Patients and providers emphasize early detection and preventive care, particularly in residential and clinical settings. Integration of digital monitoring tools and physiotherapy into treatment plans is becoming increasingly common. Local healthcare policies supporting geriatric care facilitate access to sarcopenia treatments. The preference for high-quality, clinically validated therapies aligns with German consumers’ expectations and contributes to market growth.

Asia-Pacific Sarcopenia Treatment Market Insight

The Asia-Pacific sarcopenia treatment market is poised to grow at the fastest CAGR of 8.5% during 2025–2032, driven by rapid urbanization, increasing life expectancy, and a rising geriatric population in countries such as China, Japan, and India. The region’s growing awareness of preventive healthcare and functional fitness is encouraging adoption of medications, supplements, and exercise-based interventions. Government initiatives promoting healthy aging and preventive programs are boosting accessibility. In addition, increasing healthcare infrastructure, coupled with rising disposable incomes, makes treatments more affordable for a wider population. The expansion of telemedicine and home healthcare services is further supporting treatment uptake. Cultural shifts towards active and independent aging are accelerating the market in APAC.

Japan Sarcopenia Treatment Market Insight

The Japan sarcopenia treatment market is gaining momentum due to the country’s aging population, high awareness of preventive healthcare, and demand for maintaining functional independence. Japanese patients prioritize integrated treatment programs combining medications, supplements, and physiotherapy. Hospitals and specialty clinics play a key role in diagnosis and management, while home healthcare services are increasingly utilized for continuity of care. Digital health platforms and wearable monitoring devices enhance adherence and track patient progress. Research into novel pharmacological interventions and nutrition-based therapies is ongoing, supporting market growth. The cultural emphasis on longevity and quality of life drives sustained adoption across residential and clinical settings.

India Sarcopenia Treatment Market Insight

The India sarcopenia treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the expanding elderly population, increasing health awareness, and improving healthcare infrastructure. India is witnessing growing adoption of nutritional supplements, exercise programs, and pharmacological interventions among seniors. Urbanization and rising disposable incomes contribute to higher market penetration. Government initiatives promoting preventive healthcare and geriatric wellness programs support accessibility. The availability of affordable treatment options and emerging domestic manufacturers further propels market growth. Hospitals, specialty clinics, and home healthcare services are increasingly integrating sarcopenia management into routine care programs.

Sarcopenia Treatment Market Share

The Sarcopenia Treatment industry is primarily led by well-established companies, including:

- Amgen Inc. (U.S.)

- Abbott (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Biophytis. (France)

- Lilly USA, LLC (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- GSK plc (U.K.)

- Johnson & Johnson and its affiliates (U.S.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Zydus Lifesciences Ltd (India)

- Bayer AG (Germany)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Biogen Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- AbbVie Inc. (U.S.)

What are the Recent Developments in Global Sarcopenia Treatment Market?

- In August 2025, researchers from Peking University and Hyproca Nutrition published a study in Food Science & Nutrition exploring the effects of various milk types on age-related muscle loss (sarcopenia). The study found that fortified low-fat goat milk was the most effective in promoting muscle regeneration and reducing inflammation compared to other milk types

- In July 2025, Biophytis partnered with Lynx Analytics to enhance the discovery of new treatments for sarcopenia. This collaboration focuses on utilizing artificial intelligence to accelerate the identification of potential drug candidates

- In March 2025, Biophytis received FDA authorization to launch SARA-31, the first-ever Phase 3 clinical trial specifically designed to treat sarcopenia. The study will evaluate Sarconeos (BIO101) in approximately 900 patients over 65 with severe sarcopenia, measuring the drug's ability to prevent major mobility disability over 12–36 months of treatment

- In September 2024, the University of Southern California (USC) Leonard Davis School launched studies to examine treatments and potential treatments for sarcopenia. Professors Michelle Keller and Hiroshi Kumagai received USD 25,000 each for one-year pilot projects aiming to improve how sarcopenia might be treated and potentially lower the costs for doing so

- In December 2024, TNF Pharmaceuticals announced a Phase 2 clinical trial of isomyosamine as a treatment for aging-related sarcopenia. Based on statistically significant positive results from a smaller Phase 2a study, the company plans to launch a Phase 2b study early in the first quarter of 2025

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.