Global Silicon Carbide Power Semiconductors Market

Market Size in USD Billion

USD

2.43 Billion

USD

14.63 Billion

2024

2032

USD

2.43 Billion

USD

14.63 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.43 Billion | |

| USD 14.63 Billion | |

| % | |

|

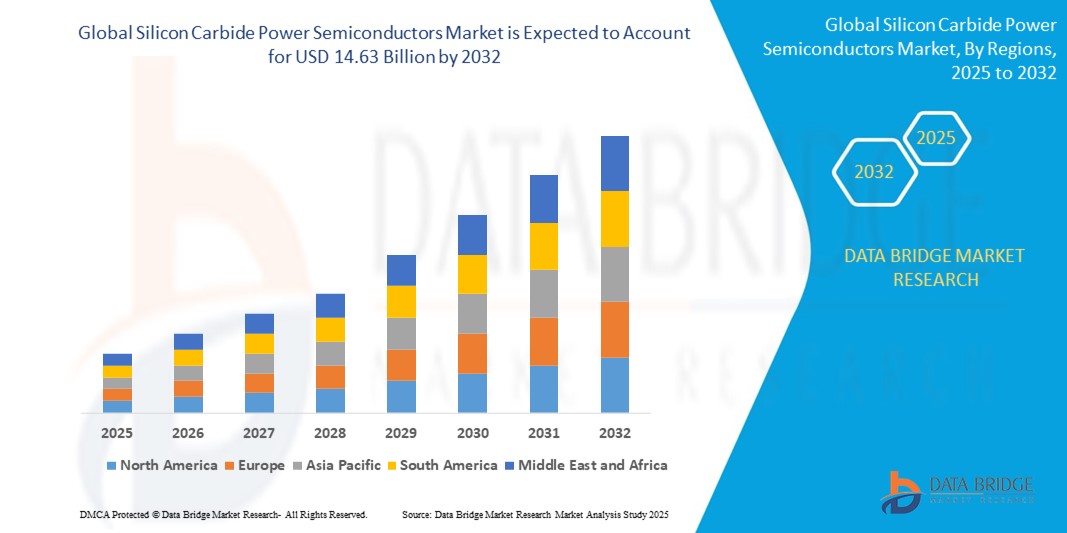

Silicon Carbide Power Semiconductors Market Size

- The global silicon carbide power semiconductors market size was valued at USD 2.43 billion in 2024 and is expected to reach USD 14.63 billion by 2032, at a CAGR of 25.10% during the forecast period

- The market growth is largely fuelled by the rising demand for energy-efficient power electronics in applications such as electric vehicles, renewable energy systems, and industrial automation

- Technological advancements and increased investment in wide bandgap semiconductor research are further accelerating the adoption of silicon carbide power devices across high-performance and high-voltage applications

Silicon Carbide Power Semiconductors Market Analysis

- The silicon carbide power semiconductors market is witnessing strong momentum due to the growing shift toward efficient power management solutions

- Manufacturers are focusing on optimizing device performance to meet the rising demand in high-voltage and high-temperature applications

- North America dominates the silicon carbide power semiconductors market with the largest revenue share of 38.7% in 2024, driven by strong demand from the automotive and industrial sectors, as well as growing adoption of electric vehicles (EVs) and renewable energy systems

- The Asia-Pacific region is expected to witness the highest growth rate in the global silicon carbide power semiconductors market, driven by rapid industrialization, increasing electric vehicle production, expanding renewable energy projects, and supportive government policies in countries such as China, India, Japan, and South Korea

- The SFP+ and SFP28 segment holds the largest market revenue share in 2024, driven by their widespread adoption in high-speed data transmission systems and compatibility with existing network infrastructures. These form factors offer a balance of performance, power efficiency, and scalability, making them the preferred choice for data centers and telecommunication networks

Report Scope and Silicon Carbide Power Semiconductors Market Segmentation

|

Attributes |

Silicon Carbide Power Semiconductors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Silicon Carbide Power Semiconductors Market Trends

“Integration of Silicon Carbide Devices in Electric Mobility”

- The shift toward electric mobility is significantly influencing the demand for silicon carbide power semiconductors in modern vehicle systems

- These semiconductors offer improved thermal conductivity, faster switching, and lower energy loss, making them ideal for efficient power conversion

- Automakers are using silicon carbide in inverters, powertrains, and onboard chargers to enhance performance and increase driving range

- For instance, BYD integrates silicon carbide components in its electric vehicles to improve power efficiency and support longer battery life

- This trend is also expanding into commercial transport, supported by the development of fast-charging infrastructure and government incentives promoting clean mobility

Silicon Carbide Power Semiconductors Market Dynamics

Driver

“Increasing Demand for Energy-Efficient Power Electronics in High-Performance Applications”

- The demand for energy-efficient and high-performance power electronics is driving growth in the silicon carbide power semiconductors market

- Industries such as electric vehicles, renewable energy, and industrial automation are adopting silicon carbide for better efficiency and reliability

- Silicon carbide devices offer faster switching speeds, lower conduction losses, and can operate at higher temperatures than traditional silicon

- For instance, electric vehicle manufacturers use silicon carbide-based inverters and chargers to enhance powertrain efficiency and extend driving range

- These semiconductors also help reduce energy losses in solar and wind energy systems, supporting global efforts to lower carbon emissions

Restraint/Challenge

“High Production Costs and Complex Manufacturing Processes”

- High production costs and complex manufacturing processes pose significant challenges for the silicon carbide power semiconductors market

- Producing silicon carbide wafers requires advanced crystal growth techniques at very high temperatures, leading to increased energy consumption and equipment expenses

- The need for high-quality raw materials and precise wafer slicing further adds to the overall cost and complexity

- For instance, limited availability of large-diameter silicon carbide wafers restricts mass production and results in higher material waste

- These factors make silicon carbide devices more expensive than traditional silicon, limiting adoption in price-sensitive applications until manufacturing efficiencies improve

Silicon Carbide Power Semiconductors Market Scope

The market is segmented on the basis of form factor, data rate, distance, wavelength, connector, and application.

- By Form Factor

On the basis of form factor, the silicon carbide power semiconductors market is segmented into SFF and SFP; SFP+ and SFP28; QSFP, QSFP+, QSFP14, and QSFP28; CFP, CFP2, and CFP4; XFP; and CXP. The SFP+ and SFP28 segment holds the largest market revenue share in 2024, driven by their widespread adoption in high-speed data transmission systems and compatibility with existing network infrastructures. These form factors offer a balance of performance, power efficiency, and scalability, making them the preferred choice for data centers and telecommunication networks.

The CFP family is expected to witness the fastest growth rate from 2025 to 2032, owing to its support for very high data rates and long-distance transmission, particularly in large-scale enterprise and telecom applications.

- By Data Rate

On the basis of data rate, the silicon carbide power semiconductors market is segmented into less than 10 Gbps, 10 Gbps to 40 Gbps, 41 Gbps to 100 Gbps, and more than 100 Gbps. The 10 Gbps to 40 Gbps segment accounted for the largest revenue share in 2024, fuelled by the growing demand for high-speed communication in data centers and enterprise networks. This range balances cost and performance, enabling efficient transmission for most applications.

The segment above 100 Gbps is expected to witness the fastest growth rate from 2025 to 2032, driven by the increasing deployment of ultra-high-speed networks supporting 5G, cloud computing, and AI workloads.

- By Distance

On the basis of distance, the silicon carbide power semiconductors market is segmented into less than 1 km, 1 to 10 km, 11 to 100 km, and more than 100 km. The less than 1 km segment held the largest market share in 2024, as this distance range is typical for short-reach applications in data centers and enterprise networks.

The 11 to 100 km segment is expected to witness the fastest growth rate from 2025 to 2032, due to increasing demand for metro and regional area networks requiring medium to long-haul optical transmission with silicon carbide power semiconductor components, which offer high efficiency and thermal management benefits.

- By Wavelength

On the basis of wavelength, the silicon carbide power semiconductors market is segmented into 850 nm band, 1310 nm band, 1550 nm band, and others. The 850 nm band segment dominated the market in 2024, largely attributed to its use in short-range optical communication and cost-effective components.

The 1550 nm band is expected to witness the fastest growth rate from 2025 to 2032, driven by its suitability for long-distance and high-capacity communication networks, supported by the growing deployment of silicon carbide-based power devices enhancing transmission efficiency.

- By Connector

On the basis of connector type, the silicon carbide power semiconductors market is segmented into LC connector, SC connector, MPO connector, and RJ-45. The LC connector segment captured the largest revenue share in 2024, owing to its compact design and widespread adoption in fiber optic networks.

The MPO connector segment is expected to witness the fastest growth rate from 2025 to 2032, driven by demand for high-density, multi-fiber connections in data centers and telecommunication infrastructure supporting silicon carbide semiconductor integration.

- By Application

On the basis of application, the silicon carbide power semiconductors market is segmented into telecommunication, data center, and enterprise. The data center segment accounted for the largest market revenue share in 2024, fueled by the rising need for energy-efficient, high-performance power devices to support cloud computing, big data, and AI operations.

The telecommunication segment is expected to witness the fastest growth rate from 2025 to 2032, propelled by the expansion of 5G infrastructure and smart city projects requiring reliable and high-speed power semiconductor components.

Silicon Carbide Power Semiconductors Market Regional Analysis

- North America dominates the silicon carbide power semiconductors market with the largest revenue share of 38.7% in 2024, driven by strong demand from the automotive and industrial sectors, as well as growing adoption of electric vehicles (EVs) and renewable energy systems

- Consumers and industries in the region prioritize energy efficiency, high performance, and reliability offered by silicon carbide power semiconductors for power conversion and motor control applications

- This widespread adoption is further supported by robust R&D investments, advanced manufacturing capabilities, and government initiatives promoting clean energy and electrification, establishing North America as a key market for SiC power devices across automotive, industrial, and energy segments

U.S. Silicon Carbide Power Semiconductors Market Insight

The U.S. silicon carbide power semiconductors market held the largest revenue share of 80% within North America in 2024, propelled by the rapid growth of electric vehicles, increased adoption of energy-efficient power electronics, and strong presence of leading semiconductor manufacturers. The country’s focus on reducing carbon emissions and enhancing grid stability fuels demand for SiC devices in inverters, chargers, and power supplies. In addition, government incentives supporting EV adoption and clean energy infrastructure further accelerate market expansion.

Europe Silicon Carbide Power Semiconductors Market Insight

The Europe silicon carbide power semiconductors market is expected to witness the fastest growth rate from 2025 to 2032, driven by stringent energy efficiency regulations, increasing EV adoption, and investments in renewable energy projects. The region’s automotive industry is transitioning towards electrification, boosting demand for high-performance silicon carbide power semiconductors devices. European governments are also actively supporting clean energy initiatives, encouraging the integration of silicon carbide power semiconductors technology in industrial and energy applications.

U.K. Silicon Carbide Power Semiconductors Market Insight

The U.K. silicon carbide power semiconductors market is expected to witness the fastest growth rate from 2025 to 2032, fuelled by rising EV penetration, smart grid modernization, and growing adoption of energy-efficient industrial equipment. The U.K.’s commitment to net-zero emissions and advancements in semiconductor research contribute to the increasing demand for silicon carbide power semiconductors power components. Moreover, strong government support and favorable policies are encouraging investments in silicon carbide power semiconductors technology development.

Germany Silicon Carbide Power Semiconductors Market Insight

The Germany silicon carbide power semiconductors power semiconductors market is expected to witness the fastest growth rate from 2025 to 2032, supported by the country’s strong automotive sector, leadership in renewable energy, and focus on Industry 4.0 initiatives. The demand for energy-efficient and high-temperature tolerant power devices is rising across automotive, industrial, and energy segments. Germany’s well-established manufacturing base and emphasis on sustainable technologies are driving the adoption of silicon carbide power semiconductors power semiconductors in electric vehicles, power converters, and industrial drives.

Asia-Pacific Silicon Carbide Power Semiconductors Market Insight

The Asia-Pacific silicon carbide power semiconductors power semiconductors market i is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid industrialization, increasing EV production, and expanding renewable energy installations in countries such as China, Japan, South Korea, and India. The region is emerging as a major manufacturing hub for semiconductor devices, benefiting from government incentives and technological advancements. The growing focus on energy-efficient electronics and rising demand from automotive and industrial sectors are key growth drivers.

Japan Silicon Carbide Power Semiconductors Market Insight

The Japan silicon carbide power semiconductors power semiconductors market is expected to witness the fastest growth rate from 2025 to 2032, due to the country’s advanced automotive industry, strong emphasis on energy conservation, and high technological expertise. The adoption of silicon carbide power semiconductors devices is driven by the increasing deployment of electric and hybrid vehicles, as well as smart grid applications. Japan’s aging population and demand for reliable, compact power electronics solutions further encourage market growth in both automotive and industrial sectors.

China Silicon Carbide Power Semiconductors Market Insight

The China accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to its booming electric vehicle market, rapid industrial growth, and substantial investments in renewable energy infrastructure. China is home to several key manufacturers and benefits from government policies promoting domestic semiconductor production and energy-efficient technologies. The nation’s push towards smart cities and electrification is propelling the adoption of silicon carbide power semiconductors power semiconductors across multiple applications.

Silicon Carbide Power Semiconductors Market Share

The Silicon Carbide Power Semiconductors industry is primarily led by well-established companies, including:

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

- WOLFSPEED, INC. (U.S.)

- Renesas Electronics Corporation (Japan)

- Semiconductor Components Industries, LLC (U.S.)

- Mitsubishi Electric Corporation (Japan)

- ROHM CO., LTD. (Japan)

- Qorvo, Inc (U.S.)

- Nexperia (Netherlands)

- TOSHIBA CORPORATION (Japan)

- Allegro MicroSystems, Inc. (U.S.)

- GeneSiC Semiconductor Inc. (U.S.)

- Fuji Electric Co., Ltd (Japan)

- Vishay Intertechnology, Inc. (U.S.)

- Hitachi Power Semiconductor Device, Ltd. (Japan)

- Littelfuse, Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- Microchip Technology Inc. (U.S.)

- Semikron Danfoss (Germany)

- WeEn Semiconductors (China)

- Solitron Devices, Inc. (U.S.)

- SemiQ Inc. (U.S.)

- Xiamen Powerway Advanced Material (China)

- MaxPower Semiconductor (China)

Latest Developments in Global Silicon Carbide Power Semiconductors Market

- In December 2022, STMicroelectronics announced a collaboration with Soitec to qualify Soitec’s SmartSiC technology for its upcoming 200mm silicon carbide substrate manufacturing. This partnership aims to enable volume production in the midterm, strengthening STMicroelectronics’ production capabilities and supporting growth in the global silicon carbide power semiconductor market

- In November 2022, Infineon Technologies signed a non-binding Memorandum of Understanding for a multi-year supply cooperation with Stellantis’s direct Tier 1 suppliers. The agreement, valued at over EUR 1 billion, plans to deliver CoolSiC bare die chips in the latter half of the decade, enhancing Infineon’s market position and contributing significantly to the expansion of the global silicon carbide power semiconductor market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATION

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 KEY TAKEAWAYS

2.2 ARRIVING AT THE GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET

2.2.1 VENDOR POSITIONING GRID

2.2.2 TECHNOLOGY LIFE LINE CURVE

2.2.3 MARKET GUIDE

2.2.4 COMPANY POSITIONING GRID

2.2.5 COMAPANY MARKET SHARE ANALYSIS

2.2.6 MULTIVARIATE MODELLING

2.2.7 TOP TO BOTTOM ANALYSIS

2.2.8 STANDARDS OF MEASUREMENT

2.2.9 VENDOR SHARE ANALYSIS

2.2.10 DATA POINTS FROM KEY PRIMARY INTERVIEWS

2.2.11 DATA POINTS FROM KEY SECONDARY DATABASES

2.3 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET: RESEARCH SNAPSHOT

2.4 ASSUMPTIONS

3 MARKET OVERVIEW

3.1 DRIVERS

3.2 RESTRAINTS

3.3 OPPORTUNITIES

3.4 CHALLENGES

4 EXECUTIVE SUMMARY

5 PREMIUM INSIGHT

5.1 PORTERS FIVE FORCES

5.2 REGULATORY STANDARDS

5.3 TECHNOLOGICAL TRENDS

5.4 PATENT ANALYSIS

5.5 CASE STUDY

5.6 VALUE CHAIN ANALYSIS

5.7 COMPANY COMPARITIVE ANALYSIS

5.8 PRICING ANALYSIS

6 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET, BY TYPE

6.1 OVERVIEW

6.2 MOSFETS

6.3 HYBRID MODULES

6.4 BIPOLAR JUNCTION TRANSISTOR (BJT)

6.5 SCHOTTKY BARRIER DIODES (SBDS)

6.6 SIC BARE DIE

6.7 PIN DIODE

6.8 JUNCTION FET (JFET)

6.9 OTHERS

7 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET, BY VOLTAGE RANGE

7.1 OVERVIEW

7.2 LESS THAN 300 V

7.3 301 V TO 900 V

7.4 901 V TO 1700 V

7.5 1701 V & ABOVE

8 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET, BY WAFER SIZE

8.1 OVERVIEW

8.2 2 INCH

8.3 4 INCH

8.4 6 INCH & ABOVE

9 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET, BY WAFER TYPE

9.1 OVERVIEW

9.2 SIC EPITAXIAL WAFERS

9.3 BLANK SIC WAFERS

10 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET, BY APPLICATION

10.1 OVERVIEW

10.2 POWER SUPPLIES

10.2.1 BY TYPE

10.2.1.1. MOSFETS

10.2.1.2. HYBRID MODULES

10.2.1.3. BIPOLAR JUNCTION TRANSISTOR (BJT)

10.2.1.4. SCHOTTKY BARRIER DIODES (SBDS)

10.2.1.5. SIC BARE DIE

10.2.1.6. PIN DIODE

10.2.1.7. JUNCTION FET (JFET)

10.2.1.8. OTHERS

10.3 INDUSTRIAL MOTOR DRIVES

10.3.1 BY TYPE

10.3.1.1. MOSFETS

10.3.1.2. HYBRID MODULES

10.3.1.3. BIPOLAR JUNCTION TRANSISTOR (BJT)

10.3.1.4. SCHOTTKY BARRIER DIODES (SBDS)

10.3.1.5. SIC BARE DIE

10.3.1.6. PIN DIODE

10.3.1.7. JUNCTION FET (JFET)

10.3.1.8. OTHERS

10.4 ELECTRIC VEHICLES (EV)

10.4.1 BY TYPE

10.4.1.1. MOSFETS

10.4.1.2. HYBRID MODULES

10.4.1.3. BIPOLAR JUNCTION TRANSISTOR (BJT)

10.4.1.4. SCHOTTKY BARRIER DIODES (SBDS)

10.4.1.5. SIC BARE DIE

10.4.1.6. PIN DIODE

10.4.1.7. JUNCTION FET (JFET)

10.4.1.8. OTHERS

10.5 INVERTERS

10.5.1 BY TYPE

10.5.1.1. MOSFETS

10.5.1.2. HYBRID MODULES

10.5.1.3. BIPOLAR JUNCTION TRANSISTOR (BJT)

10.5.1.4. SCHOTTKY BARRIER DIODES (SBDS)

10.5.1.5. SIC BARE DIE

10.5.1.6. PIN DIODE

10.5.1.7. JUNCTION FET (JFET)

10.5.1.8. OTHERS

10.6 RF DEVICES

10.6.1 BY TYPE

10.6.1.1. MOSFETS

10.6.1.2. HYBRID MODULES

10.6.1.3. BIPOLAR JUNCTION TRANSISTOR (BJT)

10.6.1.4. SCHOTTKY BARRIER DIODES (SBDS)

10.6.1.5. SIC BARE DIE

10.6.1.6. PIN DIODE

10.6.1.7. JUNCTION FET (JFET)

10.6.1.8. OTHERS

10.7 PHOTOVOLTAICS

10.7.1 BY TYPE

10.7.1.1. MOSFETS

10.7.1.2. HYBRID MODULES

10.7.1.3. BIPOLAR JUNCTION TRANSISTOR (BJT)

10.7.1.4. SCHOTTKY BARRIER DIODES (SBDS)

10.7.1.5. SIC BARE DIE

10.7.1.6. PIN DIODE

10.7.1.7. JUNCTION FET (JFET)

10.7.1.8. OTHERS

10.8 OTHERS

11 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET, BY VERTICAL

11.1 OVERVIEW

11.2 RENEWABLES / GRIDS

11.2.1 SOLAR INVERTERS

11.2.2 AUXILIARY POWER SUPPLY (APS)

11.2.3 ENERGY STORAGE SYSTEMS

11.3 AEROSPACE & DEFENSE

11.3.1 FLIGHT ACTUATORS

11.3.2 PROPULSION DRIVE

11.3.3 E-FUSE TECHNOLOGY

11.3.4 POWER DISTRIBUTION

11.3.5 TRACTION DRIVE

11.4 AUTOMOTIVE & TRANSPORTATION

11.4.1 DC FAST CHARGING

11.4.2 ON-BOARD CHARGERS (OBCS)

11.4.3 ON-BOARD DC-DC CONVERSION

11.4.4 OTHERS

11.5 DATA CENTERS

11.5.1 POWER SUPPLY UNITS (PSU)

11.5.2 POWER FACTOR CORRECTION (PFC)

11.5.3 DC-DC CONVERSION

11.5.4 BACKUP POWER

11.5.5 TELECOM/5G POWER SUPPLIES

11.5.6 OTHERS

11.6 INDUSTRIAL

11.6.1 SEMICONDUCTOR CAPITAL EQUIPMENT

11.6.2 INDUCTION HEATING

11.6.3 WELDING / PLASMA CUTTING

11.6.4 UNINTERRUPTIBLE POWER SUPPLY (UPS)

11.6.5 ROBOTICS

11.7 MEDICAL

11.7.1 AC-DC CONVERSION

11.7.2 DC-DC CONVERSION

11.7.3 OTHERS

11.8 CONSUMER ELECTRONICS

11.9 OTHERS

12 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET, BY GEOGRAPHY

GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET, (ALL SEGMENTATION PROVIDED ABOVE IS REPRESENTED IN THIS CHAPTER BY COUNTRY)

12.1 NORTH AMERICA

12.1.1 U.S.

12.1.2 CANADA

12.1.3 MEXICO

12.2 EUROPE

12.2.1 GERMANY

12.2.2 FRANCE

12.2.3 U.K.

12.2.4 ITALY

12.2.5 SPAIN

12.2.6 RUSSIA

12.2.7 TURKEY

12.2.8 BELGIUM

12.2.9 NETHERLANDS

12.2.10 NORWAY

12.2.11 FINLAND

12.2.12 SWITZERLAND

12.2.13 DENMARK

12.2.14 SWEDEN

12.2.15 POLAND

12.2.16 REST OF EUROPE

12.3 ASIA PACIFIC

12.3.1 JAPAN

12.3.2 CHINA

12.3.3 SOUTH KOREA

12.3.4 INDIA

12.3.5 AUSTRALIA

12.3.6 NEW ZEALAND

12.3.7 SINGAPORE

12.3.8 THAILAND

12.3.9 MALAYSIA

12.3.10 INDONESIA

12.3.11 PHILIPPINES

12.3.12 TAIWAN

12.3.13 VIETNAM

12.3.14 REST OF ASIA PACIFIC

12.4 SOUTH AMERICA

12.4.1 BRAZIL

12.4.2 ARGENTINA

12.4.3 REST OF SOUTH AMERICA

12.5 MIDDLE EAST AND AFRICA

12.5.1 SOUTH AFRICA

12.5.2 EGYPT

12.5.3 SAUDI ARABIA

12.5.4 U.A.E

12.5.5 OMAN

12.5.6 BAHRAIN

12.5.7 ISRAEL

12.5.8 KUWAIT

12.5.9 QATAR

12.5.10 REST OF MIDDLE EAST AND AFRICA

12.6 KEY PRIMARY INSIGHTS: BY MAJOR COUNTRIES

13 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET,COMPANY LANDSCAPE

13.1 COMPANY SHARE ANALYSIS: GLOBAL

13.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

13.3 COMPANY SHARE ANALYSIS: EUROPE

13.4 COMPANY SHARE ANALYSIS: ASIA PACIFIC

13.5 MERGERS & ACQUISITIONS

13.6 NEW PRODUCT DEVELOPMENT AND APPROVALS

13.7 EXPANSIONS

13.8 REGULATORY CHANGES

13.9 PARTNERSHIP AND OTHER STRATEGIC DEVELOPMENTS

14 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET, SWOT & DBMR ANALYSIS

15 GLOBAL SILICON CARBIDE POWER SEMICONDUCTORS MARKET, COMPANY PROFILE

15.1 ROHM CO., LTD

15.1.1 COMPANY SNAPSHOT

15.1.2 REVENUE ANALYSIS

15.1.3 GEOGRAPHIC PRESENCE

15.1.4 PRODUCT PORTFOLIO

15.1.5 RECENT DEVELOPMENT

15.2 DANFOSS

15.2.1 COMPANY SNAPSHOT

15.2.2 REVENUE ANALYSIS

15.2.3 GEOGRAPHIC PRESENCE

15.2.4 PRODUCT PORTFOLIO

15.2.5 RECENT DEVELOPMENT

15.3 MICROCHIP TECHNOLOGY INC.

15.3.1 COMPANY SNAPSHOT

15.3.2 REVENUE ANALYSIS

15.3.3 GEOGRAPHIC PRESENCE

15.3.4 PRODUCT PORTFOLIO

15.3.5 RECENT DEVELOPMENT

15.4 STMICROELECTRONICS

15.4.1 COMPANY SNAPSHOT

15.4.2 REVENUE ANALYSIS

15.4.3 GEOGRAPHIC PRESENCE

15.4.4 PRODUCT PORTFOLIO

15.4.5 RECENT DEVELOPMENT

15.5 INFINEON TECHNOLOGIES AG

15.5.1 COMPANY SNAPSHOT

15.5.2 REVENUE ANALYSIS

15.5.3 GEOGRAPHIC PRESENCE

15.5.4 PRODUCT PORTFOLIO

15.5.5 RECENT DEVELOPMENT

15.6 WOLFSPEED, INC.

15.6.1 COMPANY SNAPSHOT

15.6.2 REVENUE ANALYSIS

15.6.3 GEOGRAPHIC PRESENCE

15.6.4 PRODUCT PORTFOLIO

15.6.5 RECENT DEVELOPMENT

15.7 SEMICONDUCTOR COMPONENTS INDUSTRIES, LLC

15.7.1 COMPANY SNAPSHOT

15.7.2 REVENUE ANALYSIS

15.7.3 GEOGRAPHIC PRESENCE

15.7.4 PRODUCT PORTFOLIO

15.7.5 RECENT DEVELOPMENT

15.8 ALLEGRO MICROSYSTEMS, INC

15.8.1 COMPANY SNAPSHOT

15.8.2 REVENUE ANALYSIS

15.8.3 GEOGRAPHIC PRESENCE

15.8.4 PRODUCT PORTFOLIO

15.8.5 RECENT DEVELOPMENT

15.9 FUJI ELECTRIC CO., LTD

15.9.1 COMPANY SNAPSHOT

15.9.2 REVENUE ANALYSIS

15.9.3 GEOGRAPHIC PRESENCE

15.9.4 PRODUCT PORTFOLIO

15.9.5 RECENT DEVELOPMENT

15.1 GENESIC SEMICONDUCTOR INC. (A PART OF NAVITAS SEMICONDUCTOR)

15.10.1 COMPANY SNAPSHOT

15.10.2 REVENUE ANALYSIS

15.10.3 GEOGRAPHIC PRESENCE

15.10.4 PRODUCT PORTFOLIO

15.10.5 RECENT DEVELOPMENT

15.11 HITACHI POWER SEMICONDUCTOR DEVICE, LTD

15.11.1 COMPANY SNAPSHOT

15.11.2 REVENUE ANALYSIS

15.11.3 GEOGRAPHIC PRESENCE

15.11.4 PRODUCT PORTFOLIO

15.11.5 RECENT DEVELOPMENT

15.12 LITTELFUSE, INC.

15.12.1 COMPANY SNAPSHOT

15.12.2 REVENUE ANALYSIS

15.12.3 GEOGRAPHIC PRESENCE

15.12.4 PRODUCT PORTFOLIO

15.12.5 RECENT DEVELOPMENT

15.13 MITSUBISHI ELECTRIC CORPORATION

15.13.1 COMPANY SNAPSHOT

15.13.2 REVENUE ANALYSIS

15.13.3 GEOGRAPHIC PRESENCE

15.13.4 PRODUCT PORTFOLIO

15.13.5 RECENT DEVELOPMENT

15.14 RENESAS ELECTRONICS CORPORATION

15.14.1 COMPANY SNAPSHOT

15.14.2 REVENUE ANALYSIS

15.14.3 GEOGRAPHIC PRESENCE

15.14.4 PRODUCT PORTFOLIO

15.14.5 RECENT DEVELOPMENT

15.15 SEMIQ INC.

15.15.1 COMPANY SNAPSHOT

15.15.2 REVENUE ANALYSIS

15.15.3 GEOGRAPHIC PRESENCE

15.15.4 PRODUCT PORTFOLIO

15.15.5 RECENT DEVELOPMENT

15.16 TEXAS INSTRUMENTS INCORPORATED

15.16.1 COMPANY SNAPSHOT

15.16.2 REVENUE ANALYSIS

15.16.3 GEOGRAPHIC PRESENCE

15.16.4 PRODUCT PORTFOLIO

15.16.5 RECENT DEVELOPMENT

15.17 TOSHIBA ELECTRONIC DEVICES AND STORAGE CORPORATION

15.17.1 COMPANY SNAPSHOT

15.17.2 REVENUE ANALYSIS

15.17.3 GEOGRAPHIC PRESENCE

15.17.4 PRODUCT PORTFOLIO

15.17.5 RECENT DEVELOPMENT

15.18 UNITEDSIC (A PART OF QORVO)

15.18.1 COMPANY SNAPSHOT

15.18.2 REVENUE ANALYSIS

15.18.3 GEOGRAPHIC PRESENCE

15.18.4 PRODUCT PORTFOLIO

15.18.5 RECENT DEVELOPMENT

15.19 SAMSUNG

15.19.1 COMPANY SNAPSHOT

15.19.2 REVENUE ANALYSIS

15.19.3 GEOGRAPHIC PRESENCE

15.19.4 PRODUCT PORTFOLIO

15.19.5 RECENT DEVELOPMENT

15.2 XIAMEN POWERWAY ADVANCED MATERIAL CO. LTD.

15.20.1 COMPANY SNAPSHOT

15.20.2 REVENUE ANALYSIS

15.20.3 GEOGRAPHIC PRESENCE

15.20.4 PRODUCT PORTFOLIO

15.20.5 RECENT DEVELOPMENT

15.21 WEEN SEMICONDUCTORS

15.21.1 COMPANY SNAPSHOT

15.21.2 REVENUE ANALYSIS

15.21.3 GEOGRAPHIC PRESENCE

15.21.4 PRODUCT PORTFOLIO

15.21.5 RECENT DEVELOPMENT

15.22 TOYOTA MOTOR CORPORATION

15.22.1 COMPANY SNAPSHOT

15.22.2 REVENUE ANALYSIS

15.22.3 GEOGRAPHIC PRESENCE

15.22.4 PRODUCT PORTFOLIO

15.22.5 RECENT DEVELOPMENT

15.23 MAXPOWER SIC SEMICONDUCTOR CO., LTD

15.23.1 COMPANY SNAPSHOT

15.23.2 REVENUE ANALYSIS

15.23.3 GEOGRAPHIC PRESENCE

15.23.4 PRODUCT PORTFOLIO

15.23.5 RECENT DEVELOPMENT

15.24 NEXPERIA

15.24.1 COMPANY SNAPSHOT

15.24.2 REVENUE ANALYSIS

15.24.3 GEOGRAPHIC PRESENCE

15.24.4 PRODUCT PORTFOLIO

15.24.5 RECENT DEVELOPMENT

NOTE: THE COMPANIES PROFILED IS NOT EXHAUSTIVE LIST AND IS AS PER OUR PREVIOUS CLIENT REQUIREMENT. WE PROFILE MORE THAN 100 COMPANIES IN OUR STUDY AND HENCE THE LIST OF COMPANIES CAN BE MODIFIED OR REPLACED ON REQUEST

16 CONCLUSION

17 QUESTIONNAIRE

18 RELATED REPORTS

19 ABOUT DATA BRIDGE MARKET RESEARCH

Global Silicon Carbide Power Semiconductors Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Silicon Carbide Power Semiconductors Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Silicon Carbide Power Semiconductors Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.