Global Spinal Cord Compression Market

Market Size in USD Billion

USD

14.76 Billion

USD

26.77 Billion

2025

2033

USD

14.76 Billion

USD

26.77 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.76 Billion | |

| USD 26.77 Billion | |

| % | |

|

Spinal Cord Compression Market Size

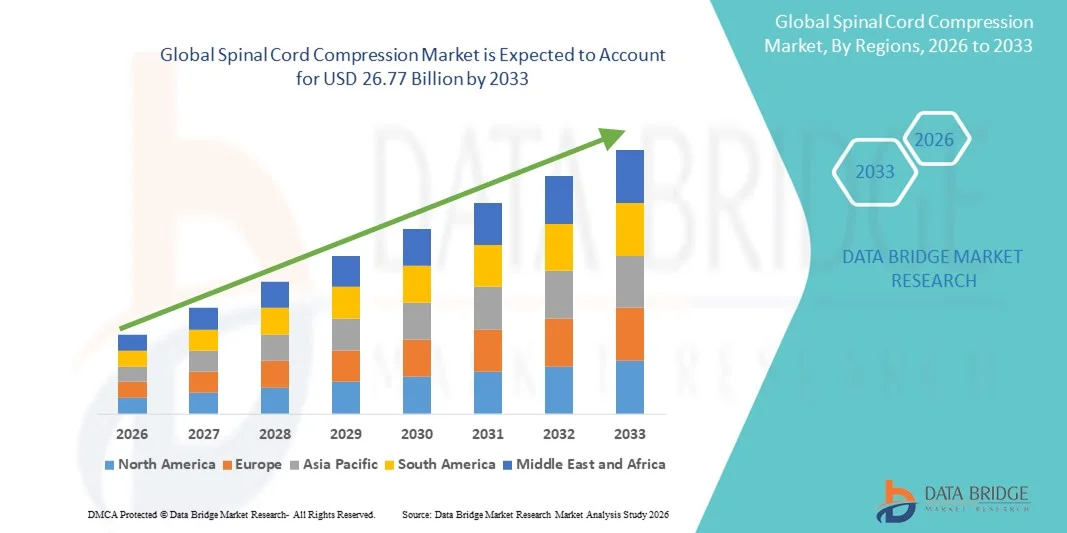

- The global spinal cord compression market size was valued at USD 14.76 billion in 2025 and is expected to reach USD 26.77 billion by 2033, at a CAGR of 7.73% during the forecast period

- The market growth is largely driven by the rising prevalence of spinal disorders, metastatic cancers, traumatic injuries, and degenerative conditions, along with advances in diagnostic imaging, minimally invasive spine surgery, and targeted therapeutic interventions

- Furthermore, increasing awareness of early diagnosis, growing adoption of advanced surgical techniques and radiation therapies, and rising healthcare expenditure are positioning spinal cord compression management as a critical component of modern neurological and oncological care, thereby significantly boosting the industry’s growth

Spinal Cord Compression Market Analysis

- Spinal cord compression, a neurological condition resulting from narrowing or obstruction of the spinal canal due to degenerative changes, trauma, or pathological growths, is a major clinical concern owing to its impact on mobility, sensory function, and overall quality of life

- The rising demand for spinal cord compression diagnosis and treatment is primarily driven by the increasing prevalence of lumbar and cervical spinal disorders, aging populations, sedentary lifestyles, and improved awareness of early intervention to prevent long-term neurological complications

- North America dominated the spinal cord compression market with the largest revenue share of 39.4% in 2025, supported by advanced diagnostic imaging availability, high adoption of surgical and non-surgical treatment modalities, and strong healthcare infrastructure across hospitals and specialty clinics

- Asia-Pacific is expected to be the fastest growing region in the spinal cord compression market during the forecast period due to a growing elderly population, rising incidence of spinal stenosis, expanding access to imaging-based diagnosis, and increasing investments in orthopedic and neurological care facilities

- Lumbar spinal stenosis segment dominated the spinal cord compression market with a market share of 46.8% in 2025, driven by its high prevalence among aging populations, widespread diagnosis through imaging modalities, and higher treatment volumes across hospitals, clinics, and physiotherapy and orthopedic centers

Report Scope and Spinal Cord Compression Market Segmentation

|

Attributes |

Spinal Cord Compression Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Spinal Cord Compression Market Trends

Advancements in Imaging and Minimally Invasive Treatment Approaches

- A significant and accelerating trend in the global spinal cord compression market is the increasing adoption of advanced imaging technologies and minimally invasive treatment techniques, enabling earlier diagnosis, precise localization of compression, and improved patient outcomes across neurological and orthopedic care settings

- For instance, high-resolution MRI and CT imaging systems are increasingly being utilized in hospitals and specialty clinics to accurately identify lumbar, cervical, and central stenosis, allowing clinicians to tailor treatment strategies more effectively

- Technological advancements in minimally invasive spinal decompression procedures are reducing surgical trauma, shortening hospital stays, and minimizing postoperative complications. For instance, image-guided spinal interventions and endoscopic decompression techniques are gaining traction for treating spinal cord compression with enhanced precision

- The integration of advanced imaging with treatment planning systems facilitates coordinated decision-making between neurologists, orthopedic surgeons, and physiotherapists, ensuring a more streamlined and patient-centric care pathway

- This trend toward precision diagnostics and less invasive treatment modalities is reshaping clinical standards for spinal cord compression management. Consequently, healthcare providers are increasingly standardizing minimally invasive approaches across treatment protocols

- The demand for accurate diagnostic tools and minimally invasive treatment options is growing steadily across hospitals, clinics, and physiotherapy and orthopedic centers, as healthcare systems prioritize faster recovery and improved quality of life for patients

- Growing integration of digital health platforms for imaging review, treatment planning, and rehabilitation monitoring is further enhancing continuity of care in spinal cord compression management

Spinal Cord Compression Market Dynamics

Driver

Rising Prevalence of Spinal Disorders and Aging Population

- The increasing prevalence of spinal disorders, combined with a rapidly aging global population, is a major driver fueling demand for spinal cord compression diagnosis and treatment services

- For instance, healthcare systems worldwide are reporting higher incidences of lumbar spinal stenosis and cervical stenosis among elderly patients, prompting greater utilization of imaging-based diagnosis and both surgical and non-surgical interventions

- As age-related degenerative changes, osteoporosis, and disc degeneration become more common, the need for timely spinal cord compression management is intensifying across hospitals and specialty clinics

- Furthermore, improved awareness regarding early diagnosis and intervention is encouraging patients to seek medical attention sooner, reducing the risk of permanent neurological damage

- The expanding availability of treatment options, including non-surgical therapies and rehabilitation services, is further supporting market growth by addressing a broader spectrum of patient needs

- The growing burden of spinal disorders, coupled with improved access to healthcare services, is significantly driving the adoption of spinal cord compression diagnostic and treatment solutions globally

- Increasing healthcare expenditure and government initiatives to strengthen orthopedic and neurological care infrastructure are further accelerating market growth

- The rising number of trained spine specialists and multidisciplinary care teams is improving treatment accessibility and supporting higher diagnosis and treatment rates

Restraint/Challenge

High Treatment Costs and Limited Access in Emerging Regions

- The high costs associated with advanced imaging, surgical treatment, and prolonged rehabilitation pose a significant challenge to the widespread adoption of spinal cord compression management solutions

- For instance, the expense of MRI-based diagnosis and surgical decompression procedures can be prohibitive for patients in low- and middle-income regions, limiting timely access to care

- The requirement for specialized infrastructure, skilled surgeons, and multidisciplinary care teams further increases treatment costs and creates disparities between developed and developing healthcare systems

- In addition, limited awareness and delayed diagnosis in certain regions can result in advanced disease progression, complicating treatment and increasing overall healthcare expenditure

- While non-surgical treatment options and physiotherapy offer cost-effective alternatives, inconsistent reimbursement policies and limited availability can hinder their adoption

- Overcoming these challenges through improved healthcare funding, expanded access to diagnostic facilities, and increased emphasis on early screening will be crucial for sustaining long-term market growth

- Shortage of advanced imaging facilities and spine specialists in rural and underserved areas continues to restrict market penetration

- Variability in treatment guidelines and reimbursement frameworks across regions further complicates standardized adoption of spinal cord compression management solutions

Spinal Cord Compression Market Scope

The market is segmented on the basis of type, diagnosis, treatment type, and end user.

- By Type

On the basis of type, the global spinal cord compression market is segmented into lumbar spinal stenosis, cervical stenosis, and central stenosis. The lumbar spinal stenosis segment dominated the market with the largest revenue share of 46.8% in 2025, driven by its high prevalence among the aging population and individuals with degenerative spine disorders. Lumbar spinal stenosis is commonly associated with age-related spinal degeneration, making it one of the most frequently diagnosed forms of spinal cord compression. The widespread use of imaging techniques such as MRI has improved detection rates, further supporting segment dominance. In addition, higher treatment volumes across hospitals and orthopedic centers contribute to sustained revenue generation. The availability of both surgical and non-surgical treatment options also enhances patient management and segment growth.

The cervical stenosis segment is expected to be the fastest growing during the forecast period, driven by rising cases linked to poor posture, sedentary lifestyles, and increasing screen time. Cervical spinal cord compression often presents with severe neurological symptoms, prompting earlier clinical intervention. Growing awareness of the risks associated with untreated cervical compression is accelerating diagnostic and treatment demand. Advances in minimally invasive cervical spine procedures are further supporting growth. Improved access to specialized neurological care is also enhancing treatment uptake. Together, these factors are positioning cervical stenosis as a rapidly expanding subsegment.

- By Diagnosis

On the basis of diagnosis, the market is segmented into physical examination and imaging. The imaging segment dominated the market in 2025, owing to its critical role in accurately identifying the location and severity of spinal cord compression. Advanced imaging modalities such as MRI and CT scans are widely used as standard diagnostic tools in hospitals and specialty clinics. Imaging provides detailed visualization of spinal structures, enabling precise treatment planning. The increasing availability of high-resolution imaging systems has further strengthened this segment. In addition, imaging is essential for monitoring disease progression and post-treatment outcomes. These factors collectively support the dominant position of the imaging segment.

The physical examination segment is expected to grow at the fastest rate during the forecast period, supported by its role as the first-line diagnostic approach. Early neurological assessments help clinicians identify symptoms that warrant further imaging evaluation. Growing awareness of early diagnosis and improved training of healthcare professionals are increasing reliance on structured physical examinations. In resource-limited settings, physical examination remains a cost-effective diagnostic method. Its integration with standardized clinical guidelines is further enhancing its adoption. As access to healthcare expands, this segment is expected to witness steady growth.

- By Treatment Type

On the basis of treatment type, the market is segmented into surgical treatment and non-surgical treatment. The surgical treatment segment dominated the market in 2025, driven by its effectiveness in relieving severe spinal cord compression and preventing permanent neurological damage. Surgical decompression procedures are commonly recommended for advanced or progressive cases. Technological advancements in spine surgery have improved success rates and reduced recovery times. Hospitals with specialized spine units continue to perform high volumes of surgical interventions. Strong clinical outcomes further support physician preference for surgical solutions. These factors contribute to the segment’s leading market position.

The non-surgical treatment segment is anticipated to be the fastest growing over the forecast period, supported by increasing preference for conservative management in early-stage cases. Non-surgical approaches such as physiotherapy, medications, and lifestyle modifications are gaining traction due to lower risk and cost-effectiveness. Growing emphasis on pain management and functional rehabilitation is expanding adoption. Patients are increasingly opting for non-invasive therapies before considering surgery. Improved physiotherapy protocols and rehabilitation programs are further driving growth. This shift toward conservative care is accelerating segment expansion.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, and physiotherapy and orthopaedic centers. The hospitals and clinics segment dominated the market in 2025, owing to the availability of advanced diagnostic infrastructure and specialized medical professionals. Hospitals serve as primary centers for imaging-based diagnosis, surgical treatment, and multidisciplinary care. Higher patient inflow for severe and acute cases supports strong revenue contribution. The presence of neurology and orthopedic departments further strengthens this segment. Hospitals also play a key role in managing complex spinal cord compression cases. These factors collectively drive segment dominance.

The physiotherapy and orthopaedic centers segment is expected to grow at the fastest rate during the forecast period, driven by rising demand for rehabilitation and non-surgical management. Increasing focus on long-term recovery and mobility improvement is boosting patient visits to these centers. Orthopaedic centers are expanding their service offerings to include comprehensive spine care. Growing awareness of physiotherapy’s role in pain relief and functional restoration supports adoption. Cost-effectiveness compared to hospital-based care further enhances appeal. As outpatient care models expand, this segment is poised for rapid growth.

Spinal Cord Compression Market Regional Analysis

- North America dominated the spinal cord compression market with the largest revenue share of 39.4% in 2025, supported by advanced diagnostic imaging availability, high adoption of surgical and non-surgical treatment modalities, and strong healthcare infrastructure across hospitals and specialty clinics

- Patients and healthcare providers in the region place significant emphasis on early diagnosis, access to advanced imaging modalities, and availability of both surgical and non-surgical treatment options across hospitals and specialty clinics

- This widespread adoption is further supported by high healthcare expenditure, favorable reimbursement frameworks, and a strong presence of specialized spine centers and trained medical professionals, positioning spinal cord compression management as a critical component of advanced healthcare delivery

U.S. Spinal Cord Compression Market Insight

The U.S. spinal cord compression market captured the largest revenue share within North America in 2025, driven by the high prevalence of degenerative spinal disorders, metastatic cancers, and traumatic spinal injuries. Patients and clinicians increasingly prioritize early diagnosis and timely intervention to prevent permanent neurological damage. The widespread availability of advanced imaging technologies and specialized spine care centers further supports market growth. Moreover, strong reimbursement coverage and high healthcare spending continue to fuel demand for both surgical and non-surgical treatment options across hospitals and specialty clinics.

Europe Spinal Cord Compression Market Insight

The Europe spinal cord compression market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by an aging population and rising incidence of spinal stenosis and degenerative spine diseases. Increasing emphasis on early diagnosis and standardized treatment guidelines is supporting adoption across the region. Growth in advanced imaging infrastructure and minimally invasive spine procedures is further contributing to market expansion. The region is witnessing increasing treatment demand across hospitals, rehabilitation centers, and orthopedic clinics, supported by well-established public healthcare systems.

U.K. Spinal Cord Compression Market Insight

The U.K. spinal cord compression market is anticipated to grow at a notable CAGR during the forecast period, driven by rising awareness of spinal health and increasing diagnosis of age-related spinal conditions. The growing burden of lumbar and cervical stenosis is encouraging greater utilization of imaging-based diagnostics and multidisciplinary treatment approaches. Expansion of orthopedic and neurological care services within the National Health Service is supporting market growth. In addition, improved access to physiotherapy and rehabilitation services is strengthening long-term patient management.

Germany Spinal Cord Compression Market Insight

The Germany spinal cord compression market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure and high adoption of advanced diagnostic technologies. Germany’s emphasis on precision medicine and early intervention supports timely identification and treatment of spinal cord compression. The presence of specialized spine centers and trained orthopedic surgeons enhances treatment accessibility. Furthermore, increasing preference for minimally invasive surgical techniques and structured rehabilitation programs is contributing to sustained market growth.

Asia-Pacific Spinal Cord Compression Market Insight

The Asia-Pacific spinal cord compression market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid population aging, rising incidence of spinal disorders, and improving access to healthcare services. Increasing awareness of spinal health and expanding availability of imaging diagnostics are accelerating diagnosis rates. Government investments in healthcare infrastructure across countries such as China, Japan, and India are further supporting market expansion. In addition, growing adoption of non-surgical treatment and rehabilitation services is broadening patient reach across the region.

Japan Spinal Cord Compression Market Insight

The Japan spinal cord compression market is gaining momentum due to the country’s rapidly aging population and high prevalence of degenerative spinal conditions. Japan places strong emphasis on early diagnosis and preventive healthcare, driving the use of advanced imaging modalities. The integration of surgical and non-surgical treatment pathways supports comprehensive patient management. Moreover, growing demand for rehabilitation and physiotherapy services is enhancing long-term outcomes for spinal cord compression patients in both hospital and outpatient settings.

India Spinal Cord Compression Market Insight

The India spinal cord compression market accounted for a significant revenue share in Asia-Pacific in 2025, attributed to increasing awareness of spinal disorders, rising healthcare access, and expanding diagnostic capabilities. Rapid urbanization and lifestyle changes are contributing to higher incidence of spinal conditions such as lumbar and cervical stenosis. The growing number of multispecialty hospitals and orthopedic centers is improving treatment availability. In addition, increasing adoption of cost-effective non-surgical therapies and physiotherapy services is supporting broader market growth across urban and semi-urban regions.

Spinal Cord Compression Market Share

The Spinal Cord Compression industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

- DePuy Synthes (U.S.)

- Globus Medical (U.S.)

- NuVasive, Inc. (U.S.)

- Orthofix Medical Inc. (U.S.)

- MicroPort Scientific Corporation (China)

- K2M, Inc. (U.S.)

- Alphatec Spine, Inc. (U.S.)

- Paradigm Spine (U.S.)

- Vertos Medical Inc. (U.S.)

- Vertiflex Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- B. Braun SE (Germany)

- RTI Surgical Holdings, Inc. (U.S.)

- SpineGuard (France)

- Ekso Bionics Holdings Inc. (U.S.)

- Spineart (Switzerland)

- SeaSpine Holdings Corporation (U.S.)

What are the Recent Developments in Global Spinal Cord Compression Market?

- In September 2025, advocacy and awareness efforts for spinal cord injuries expanded globally with events such as the “Wheelchair Rally 2025” in Trichy, reinforcing public focus on SCI prevention, rehabilitation access, and quality of life improvements for individuals affected by spinal cord compression and injury. While not a clinical treatment, such initiatives enhance public understanding and support for research and care infrastructures that benefit SCI patients

- In July 2025, multiple rehabilitation centers reported that early results from the ARC-EX Up-LIFT trial indicated significant functional improvements in hand and arm strength for people with cervical spinal cord injuries, reinforcing the therapy’s clinical impact and supporting broader adoption of non-invasive stimulation within rehabilitative care. This follow-up report highlights the sustained clinical benefits of electrical stimulation beyond initial findings

- In July 2025, Indian medical centers increasingly adopted endoscopic and navigation-assisted minimally invasive spinal decompression techniques reducing hospitalization time, procedural trauma, and recovery periods for patients compared with conventional open surgery approaches. These real-world advancements in surgical practice reflect broader trends toward safer, less invasive spine interventions

- In March 2025, Cellino and Matricelf announced a global collaboration to scale personalized induced pluripotent stem cell (iPSC)-based treatments for spinal cord injury, combining Cellino’s automated Nebula™ iPSC manufacturing technology with Matricelf’s regenerative tissue engineering approach to generate functional neural tissues that could pave the way for future clinical applications. This partnership targets scalable regenerative therapies for SCI patients, potentially shifting treatment paradigms toward personalized medicine

- In May 2024, ONWARD Medical published results from its global Up-LIFT trial of the non-invasive ARC-EX spinal stimulation therapy in Nature Medicine, showing significant improvements in upper limb strength, sensory function, and quality of life for people with chronic cervical spinal cord injury, marking one of the most promising clinical advances in non-invasive SCI treatment. These outcomes demonstrated meaningful gains in strength and function well above rehabilitation alone, underscoring the potential of electrical spinal cord stimulation to improve functional outcomes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.