Global Sporotrichosis Market

Market Size in USD Million

USD

850.00 Million

USD

1,181.30 Million

2025

2033

USD

850.00 Million

USD

1,181.30 Million

2025

2033

| 2026 - 2033 | |

| USD 850.00 Million | |

| USD 1,181.30 Million | |

| % | |

|

Sporotrichosis Market Size

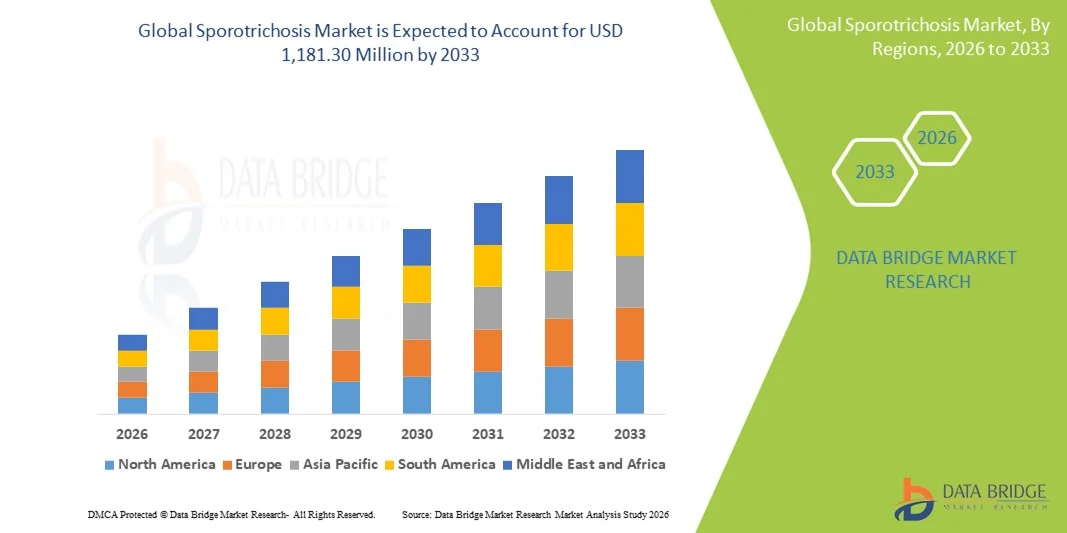

- The global sporotrichosis market size was valued at USD 850.00 million in 2025 and is expected to reach USD 1,181.30 million by 2033, at a CAGR of 4.20% during the forecast period

- The market growth is largely fueled by the rising prevalence of sporotrichosis globally and increased awareness about fungal infections, prompting higher demand for diagnosis and effective antifungal treatments

- Furthermore, advances in antifungal therapies (oral, topical and intravenous), expansion of healthcare access in emerging economies, and improved diagnostic capabilities are making treatment more accessible and reliable driving uptake of Sporotrichosis treatment solutions

Sporotrichosis Market Analysis

- Sporotrichosis, a fungal infection caused by Sporothrix species, is primarily managed through antifungal therapies and early diagnosis, making treatment and diagnostic solutions crucial for both endemic and emerging regions

- The escalating demand for sporotrichosis management is driven by rising incidence rates, increased awareness among healthcare professionals, improved diagnostic capabilities, and the growing focus on antifungal drug development

- North America dominated the sporotrichosis market with the largest revenue share of 41.7% in 2025, characterized by advanced healthcare infrastructure, high awareness of fungal infections, and a strong presence of key pharmaceutical and diagnostic players, with the U.S. experiencing substantial growth in both antifungal therapies and molecular diagnostic adoption, particularly in hospitals and specialty clinics

- Asia-Pacific is expected to be the fastest growing region in the sporotrichosis market during the forecast period due to increasing healthcare infrastructure, rising awareness about fungal infections, and improved accessibility of antifungal treatments

- Antifungal drugs segment dominated the sporotrichosis market with a market share of 46.8% in 2025, driven by the established efficacy of itraconazole and terbinafine in treating cutaneous and disseminated infections, along with their wide availability in both hospital and outpatient settings

Report Scope and Sporotrichosis Market Segmentation

|

Attributes |

Sporotrichosis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Sporotrichosis Market Trends

Advancement in Rapid Molecular Diagnostics

- A significant and accelerating trend in the global sporotrichosis market is the increasing adoption of rapid molecular diagnostic technologies, including PCR-based kits, which enable early and accurate detection of Sporothrix infections

- For instance, the SpeedX PCR Sporotrichosis Test can detect Sporothrix DNA within hours, significantly reducing diagnosis time compared to traditional culture methods, and allowing faster initiation of antifungal therapy

- Molecular diagnostics also allow differentiation between Sporothrix species, which helps in targeted treatment and reduces the risk of antifungal resistance. Several kits, such as MycoDetect, are being enhanced with automated sample processing and AI-driven result interpretation to improve accuracy and reliability

- The integration of rapid diagnostic solutions into routine hospital workflows facilitates timely clinical decision-making and reduces complications associated with delayed treatment. This is particularly important in immunocompromised patients and in regions with high incidence of zoonotic transmission

- This trend towards faster, more precise, and user-friendly diagnostic tools is fundamentally reshaping clinical management of sporotrichosis, with companies such as LabCorp developing molecular tests capable of high-throughput screening and species-specific identification

- The demand for advanced molecular diagnostics is growing rapidly across both endemic and non-endemic regions, as healthcare providers increasingly prioritize early detection and effective management of sporotrichosis

- In addition, integration of digital health platforms with diagnostic tools is enabling remote monitoring and telemedicine consultations, further enhancing patient outcomes and accessibility

- Development of multiplex diagnostic kits that simultaneously detect Sporothrix and other fungal pathogens is emerging, offering comprehensive fungal infection screening in a single test

Sporotrichosis Market Dynamics

Driver

Rising Incidence and Awareness of Sporotrichosis

- The increasing prevalence of sporotrichosis, particularly in North America and Latin America, coupled with heightened awareness among healthcare professionals, is a significant driver for market growth

- For instance, in March 2025, the CDC highlighted a surge in zoonotic sporotrichosis cases linked to domestic cats, prompting hospitals to adopt improved diagnostic and treatment protocols

- As clinicians become more vigilant about fungal infections, early diagnosis and antifungal therapy are being prioritized, enhancing adoption of treatment solutions

- Furthermore, government health programs and veterinary-human health initiatives are promoting education about sporotrichosis prevention and management, increasing demand for both diagnostics and antifungal drugs

- The availability of improved antifungal therapies, easy-to-administer formulations, and the integration of diagnostics with treatment guidelines are key factors driving adoption in clinical settings, especially in hospitals and specialty clinics

- In addition, partnerships between pharmaceutical companies and diagnostic providers are fostering combined treatment and testing solutions, streamlining patient care and driving market expansion. Increasing research funding for fungal infections and development of novel antifungal agents is further accelerating innovation and market growth

- Awareness campaigns targeting both urban and rural populations are enhancing early consultation rates, further increasing the uptake of diagnostic and therapeutic solutions

Restraint/Challenge

Limited Awareness and High Treatment Costs

- Limited awareness about sporotrichosis among the general population, coupled with underdiagnosis in non-endemic regions, poses a significant challenge to broader market penetration

- For instance, delayed recognition of Sporothrix infections in rural clinics often leads to prolonged disease progression, highlighting the need for wider education and training of healthcare providers

- Addressing these awareness gaps through public health campaigns, clinician training, and accessible diagnostic services is crucial for improving early detection and treatment uptake. In addition, the relatively high cost of advanced antifungal drugs, such as itraconazole and terbinafine, can be a barrier to adoption in low-income or rural populations

- While generic formulations are available, the cost of species-specific molecular diagnostics and newer drug formulations often remains high, limiting access in resource-constrained settings

- Overcoming these challenges through cost reduction strategies, government subsidies, and enhanced healthcare outreach will be vital for sustained growth of the sporotrichosis market

- Furthermore, lack of standardized treatment guidelines across regions can lead to inconsistent therapy, affecting overall market adoption and clinical outcomes. Challenges in cold-chain storage and distribution of certain antifungal formulations in remote areas also hinder consistent availability and use, particularly in tropical and subtropical regions

- Resistance to conventional antifungal therapies in some Sporothrix strains is emerging, necessitating research into alternative drugs and posing a potential barrier for widespread market growth

Sporotrichosis Market Scope

The market is segmented on the basis of disease type, treatment, diagnosis, dosage, route of administration, symptoms, end-users, and distribution channel.

- By Disease Type

On the basis of disease type, the sporotrichosis market is segmented into cutaneous sporotrichosis, disseminated sporotrichosis, and pulmonary sporotrichosis. The cutaneous sporotrichosis segment dominated the market with the largest revenue share of 52.4% in 2025, driven by its high prevalence among adults and gardeners exposed to contaminated soil and plant matter. Cutaneous infections are easier to diagnose and manage with standard antifungal therapy, making this segment the largest contributor to market revenue. Physicians often prioritize early treatment of cutaneous sporotrichosis to prevent progression to more severe forms. The segment also benefits from the availability of both oral and injectable antifungal drugs. Awareness campaigns and routine screening in endemic regions further support adoption. The high occurrence of painless bumps and lesions ensures strong demand for both diagnostic and treatment solutions in this segment.

The pulmonary sporotrichosis segment is expected to witness the fastest growth at a CAGR of 20.1% from 2026 to 2033, fueled by rising cases among immunocompromised patients and increasing hospitalizations. Pulmonary infections often require more advanced diagnostics, such as imaging and laboratory testing, driving demand for specialized hospital services. Increasing prevalence of respiratory comorbidities in North America and Europe contributes to segment growth. The segment also sees innovation in targeted antifungal therapy to improve treatment outcomes. Hospitals and specialty clinics are adopting rapid molecular diagnostics to manage pulmonary cases efficiently. Awareness of occupational exposure risks in mining and agriculture further supports the adoption of early intervention strategies in this segment.

- By Treatment

On the basis of treatment, the sporotrichosis market is segmented into antifungal drugs, surgery, and others. The antifungal drugs segment dominated the market with a market share of 46.8% in 2025, driven by the established efficacy of itraconazole and terbinafine in treating both cutaneous and systemic infections. Oral and injectable formulations provide flexibility for patient-specific treatment regimens. The segment benefits from strong physician confidence and widespread clinical adoption. Antifungal drugs are also supported by molecular diagnostics for species-specific identification. Continuous research into novel antifungal agents is expanding the drug portfolio. Patient adherence and favorable safety profiles further strengthen market dominance.

The surgery segment is expected to witness the fastest growth at a CAGR of 18.9% from 2026 to 2033, primarily in cases of severe or disseminated infections requiring debridement or lesion removal. Surgical intervention is increasingly adopted in combination with antifungal therapy to improve clinical outcomes. Hospitals in North America and Europe are investing in surgical infrastructure and training for complex sporotrichosis cases. Early identification and intervention in severe cases drive demand for surgical procedures. Specialty clinics treating immunocompromised patients are key adopters. Increasing awareness of alternative treatment options supports growth in the surgical segment.

- By Diagnosis

On the basis of diagnosis, the market is segmented into blood tests, laboratory tests, skin biopsy, and others. The laboratory tests segment dominated the market with a revenue share of 44.7% in 2025, due to its widespread use for culture-based identification and species confirmation. Laboratories provide reliable results, guiding antifungal therapy selection. Laboratory diagnostics are commonly available in both urban and semi-urban hospitals. High adoption rates among clinicians and integration with treatment protocols support segment dominance. Continuous improvements in lab techniques improve turnaround time and accuracy. The availability of trained personnel further strengthens the segment.

The blood tests segment is expected to witness the fastest growth at a CAGR of 22.5% from 2026 to 2033, driven by rising adoption of serological and molecular testing for early detection. Blood-based diagnostics are minimally invasive and suitable for immunocompromised patients. Rapid turnaround time and automation enhance clinical workflow efficiency. Increasing prevalence of zoonotic sporotrichosis supports early screening initiatives. Advanced blood tests are integrated with hospital information systems for efficient patient management. Growing investments in diagnostic technology are accelerating adoption in emerging markets.

- By Dosage

On the basis of dosage, the market is segmented into tablet, injection, and others. The tablet segment dominated the market with a 50.2% share in 2025, driven by ease of administration and patient compliance. Tablets are widely prescribed for both cutaneous and mild systemic infections. Availability of generic formulations reduces cost and increases accessibility. Physicians favor oral therapy for outpatient management. High patient adherence supports consistent treatment outcomes. Tablets are compatible with home-based treatment strategies, reducing hospital burden.

The injection segment is expected to witness the fastest growth at a CAGR of 21.3% from 2026 to 2033, primarily for severe or disseminated sporotrichosis cases requiring intravenous antifungal therapy. Injectable formulations ensure rapid drug delivery and bioavailability. Hospitals and specialty clinics are key adopters due to acute case management. Increasing immunocompromised populations drive demand for injectable therapy. Injectable antifungals are often paired with molecular diagnostics to monitor treatment efficacy. Growing awareness of effective systemic therapy supports market growth.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, intravenous, and others. The oral segment dominated the market with a 53.1% share in 2025, driven by convenience, affordability, and patient preference for home-based therapy. Oral administration supports long-term treatment regimens for cutaneous and mild systemic infections. High adoption rates among clinics and outpatient departments reinforce segment dominance. Oral therapy is widely integrated with prescription guidelines and patient monitoring programs. Availability of generic oral antifungals reduces cost barriers. Oral route facilitates better adherence and reduces hospitalization needs.

The intravenous segment is expected to witness the fastest growth at a CAGR of 20.9% from 2026 to 2033, primarily for critical, disseminated, and pulmonary infections requiring immediate intervention. IV administration ensures rapid systemic delivery and higher efficacy in severe cases. Hospitals are increasingly equipping specialty units to manage IV therapy. Rising incidence of immunocompromised patients boosts adoption. Intravenous antifungals are often used in combination with diagnostics for optimal treatment outcomes. Increasing awareness among healthcare providers supports segment growth.

- By Symptoms

On the basis of symptoms, the market is segmented into fever, cough, chest pain, painless bump, shortness of breath, and others. The painless bump segment dominated the market with a 48.6% share in 2025, due to the high prevalence of cutaneous lesions in most sporotrichosis cases. Early recognition of bumps facilitates prompt treatment and reduces systemic spread. Dermatologists and primary care physicians are key drivers of diagnosis. The symptom is highly visible, increasing clinical consultations. Treatment protocols often begin immediately upon detection. Awareness campaigns in endemic regions further reinforce early treatment.

The shortness of breath segment is expected to witness the fastest growth at a CAGR of 21.8% from 2026 to 2033, driven by pulmonary sporotrichosis in immunocompromised patients and individuals with respiratory comorbidities. Hospitals and specialty clinics are primary adopters for diagnostic and therapeutic solutions. Early symptom recognition encourages adoption of rapid diagnostic tests. Severe cases often require combined therapy approaches, driving market demand. Pulmonary symptom awareness campaigns enhance detection rates. Emerging markets with rising respiratory disease prevalence are contributing to rapid segment growth.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, and others. The hospitals segment dominated the market with a 55.4% share in 2025, driven by the management of severe, disseminated, and pulmonary infections requiring advanced diagnostics and treatment. Hospitals offer integrated care including IV therapy, laboratory testing, and follow-up. High patient footfall and specialist availability support segment dominance. Adoption of molecular diagnostics and antifungal therapy is highest in hospitals. Hospitals are investing in staff training and advanced treatment protocols. Government programs and insurance coverage further drive hospital utilization.

The clinics segment is expected to witness the fastest growth at a CAGR of 22.1% from 2026 to 2033, fueled by rising outpatient diagnosis and treatment of cutaneous sporotrichosis. Clinics provide easy access to oral therapy and basic diagnostics. Telemedicine integration and community outreach programs are increasing clinic adoption. Early intervention in rural or semi-urban areas supports growth. Clinics are becoming increasingly equipped with rapid diagnostic kits. Rising awareness and affordability make clinics a preferred choice for mild cases.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with a 51.8% share in 2025, due to direct supply of antifungal drugs and diagnostic kits for in-hospital patient management. Hospitals ensure consistent availability and prescription adherence. Integration with hospital treatment protocols strengthens segment dominance. Hospital pharmacies also provide guidance on proper drug administration. Regular restocking and reliable supply chains support widespread adoption. Hospital pharmacies facilitate combination therapy approaches for severe cases.

The online pharmacy segment is expected to witness the fastest growth at a CAGR of 23.4% from 2026 to 2033, driven by increasing e-commerce penetration, convenience, and accessibility for patients in remote areas. Online channels offer home delivery of antifungal drugs and diagnostic kits. Telemedicine prescriptions complement online sales. Price competitiveness and promotional offers attract patients. Growing smartphone and internet penetration accelerate adoption. Awareness campaigns and patient education support the online pharmacy growth trend.

Sporotrichosis Market Regional Analysis

- North America dominated the sporotrichosis market with the largest revenue share of 41.7% in 2025, characterized by advanced healthcare infrastructure, high awareness of fungal infections, and a strong presence of key pharmaceutical and diagnostic players

- Healthcare providers and patients in the region highly value early diagnosis, access to effective antifungal therapies, and integration of rapid molecular diagnostics into clinical workflows, improving treatment outcomes

- This widespread adoption is further supported by strong research funding, well-established hospital networks, and advanced laboratory facilities, establishing North America as a leading market for both sporotrichosis treatment and diagnostic solutions

U.S. Sporotrichosis Market Insight

The U.S. sporotrichosis market captured the largest revenue share of 82% in 2025 within North America, fueled by rising zoonotic infections, advanced healthcare infrastructure, and increasing awareness among clinicians and veterinarians. Early adoption of rapid molecular diagnostics and effective antifungal therapies is enabling timely diagnosis and treatment. The growing preference for outpatient care and integration of telemedicine services further propels the market. Moreover, ongoing research and development in antifungal drugs and diagnostics are significantly contributing to market expansion. Public health initiatives and awareness campaigns regarding sporotrichosis prevention also play a vital role in boosting adoption.

Europe Sporotrichosis Market Insight

The Europe sporotrichosis market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of fungal infections and growing healthcare investments. The increase in urbanization, coupled with the demand for advanced diagnostics and antifungal treatments, is fostering market growth. European healthcare providers are emphasizing early detection and management, reducing complications associated with delayed treatment. The market is experiencing significant growth across hospitals, specialty clinics, and laboratory services, with sporotrichosis management being incorporated into broader fungal infection programs. Stringent healthcare standards and reimbursement policies are also supporting adoption.

U.K. Sporotrichosis Market Insight

The U.K. sporotrichosis market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing clinical awareness and the rising prevalence of sporotrichosis cases in both humans and domestic animals. Concerns regarding zoonotic transmission are encouraging healthcare providers to adopt rapid diagnostic tests and effective antifungal therapies. The U.K.’s well-developed healthcare infrastructure and emphasis on research and development are expected to stimulate market growth. Public health campaigns and veterinary collaborations are further promoting early intervention and effective disease management. Growing patient awareness about preventive measures also supports market expansion.

Germany Sporotrichosis Market Insight

The Germany sporotrichosis market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of fungal infections and the demand for technologically advanced diagnostic solutions. Germany’s robust healthcare infrastructure and focus on innovation in infectious disease management promote adoption. Hospitals and specialty clinics are investing in molecular diagnostics and antifungal treatments to improve patient outcomes. The integration of advanced diagnostics with routine care is becoming increasingly prevalent, with strong emphasis on preventive strategies and zoonotic infection control. Government-backed awareness programs and funding for fungal disease research are further supporting market growth.

Asia-Pacific Sporotrichosis Market Insight

The Asia-Pacific sporotrichosis market is poised to grow at the fastest CAGR of 25% during the forecast period of 2026 to 2033, driven by rising incidence of sporotrichosis, expanding healthcare infrastructure, and increasing awareness in countries such as China, India, and Japan. The region’s growing focus on early diagnosis and treatment, supported by government health initiatives and public awareness campaigns, is driving adoption. Furthermore, APAC is witnessing improvements in access to rapid diagnostics and antifungal drugs, enhancing treatment efficiency. Increasing urbanization, rising disposable incomes, and technological advancements are also contributing to faster market growth.

Japan Sporotrichosis Market Insight

The Japan sporotrichosis market is gaining momentum due to rising cases among immunocompromised patients, a high-tech healthcare system, and a strong emphasis on preventive care. The Japanese market prioritizes early detection through molecular diagnostics and effective antifungal treatment options. Integration of laboratory testing with hospital-based treatment protocols is fueling growth. In addition, increasing awareness among healthcare providers and patients regarding zoonotic infections is supporting adoption. Japan’s aging population is expected to spur demand for easy-to-administer therapies and outpatient care solutions.

India Sporotrichosis Market Insight

The India sporotrichosis market accounted for the largest revenue share in Asia Pacific in 2025, attributed to rising incidence rates, growing awareness among healthcare providers, and expanding access to diagnostic and treatment facilities. India is experiencing increased adoption of rapid molecular diagnostics and oral antifungal therapies in both urban and rural healthcare settings. Government health programs and initiatives promoting infectious disease management are key factors propelling market growth. The affordability of diagnostics and generic antifungal drugs supports widespread adoption. Increasing clinical training and public awareness campaigns further strengthen market expansion.

Sporotrichosis Market Share

The Sporotrichosis industry is primarily led by well-established companies, including:

- Merck & Co., Inc., (U.S.)

- Pfizer Inc., (U.S.)

- Novartis AG (Switzerland)

- Teva Pharmaceutical Industries Ltd., (Israel)

- Bayer AG (Germany)

- GSK plc (U.K.)

- Astellas Pharma Inc., (Japan)

- Sun Pharmaceutical Industries Ltd., (India)

- Glenmark Pharmaceuticals Ltd (India)

- Abbott (U.S.)

- Sanofi (France)

- Aurobindo Pharma (India)

- Cadila Healthcare (India)

- Dr. Reddy’s Laboratories (India)

- Leadiant Biosciences, Inc., (U.S.)

- SCYNEXIS, Inc., (U.S.)

- Gilead Sciences, Inc., (U.S.)

What are the Recent Developments in Global Sporotrichosis Market?

- In June 2025, A new center hosted at University of São Paulo (Brazil) was inaugurated to study endemic fungal infections in Latin America. Among its research priorities is sporotrichosis. The center seeks to coordinate research, improve diagnostics and treatment strategies, and promote public‑health surveillance of fungal diseases

- In April 2025, New class of antifungal drug candidate identified (DT-23), which could pave way for future broad‑spectrum antifungal therapies. Researchers reported that IPK inhibitor DT‑23 shows potential as a novel antifungal with a different mechanism of action compared to existing antifungals addressing limitations such as drug toxicity, limited spectrum, and resistance

- In March 2025, Academic collaboration aiming to develop novel antifungal drugs targeting fungal‑specific enzyme for broad‑spectrum fungal infections. A cross-disciplinary project (agriculture + pharmacy) at Purdue University is working to develop new antifungal compounds that inhibit a fungal enzyme (Cdc14) with the goal to produce novel, patent‑pending antifungal candidates

- In January 2025, New pre‑clinical study identifies alternative antifungal agents (including Isavuconazole and Posaconazole) effective against strains of Sporothrix schenckii, including itraconazole‑non‑wild‑type isolates. The study found that all tested drugs inhibited fungal growth within 24 hours, and that isavuconazole (ISA) was fungicidal for non‑wild‑type strains

- In August 2024, Repurposing of veterinary drug Milteforan (miltefosine) as potential treatment for feline sporotrichosis. Researchers demonstrated that Milteforan has fungicidal activity in vitro against S. brasiliensis and S. schenckii, including effects in infected epithelial cells and macrophages

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.