Global Venous Diseases Treatment Market

Market Size in USD Billion

USD

6.62 Billion

USD

11.63 Billion

2024

2032

USD

6.62 Billion

USD

11.63 Billion

2024

2032

| 2025 - 2032 | |

| USD 6.62 Billion | |

| USD 11.63 Billion | |

| % | |

|

Venous Diseases Treatment Market Size

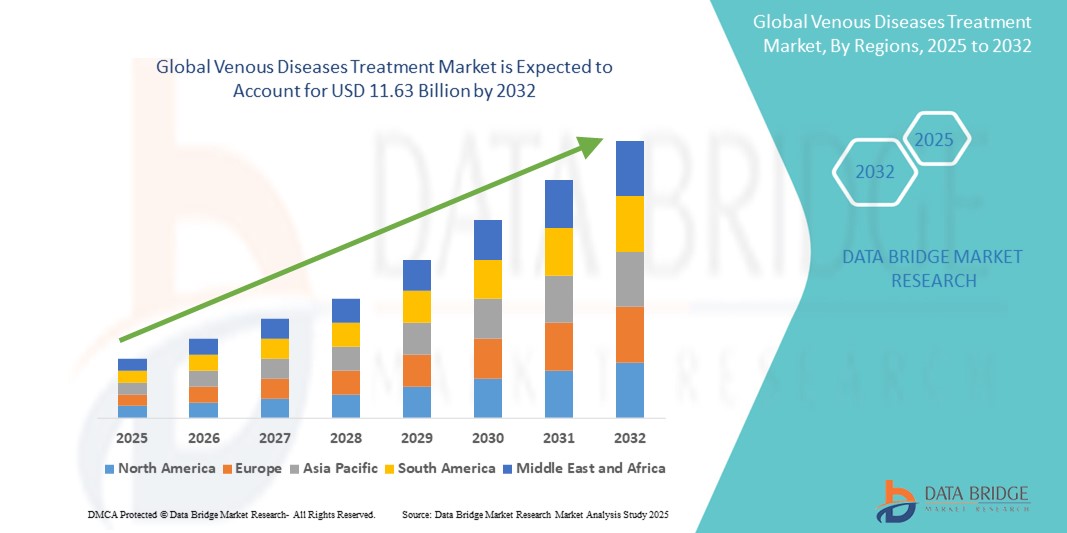

- The global venous diseases treatment market size was valued at USD 6.62 billion in 2024 and is expected to reach USD 11.63 billion by 2032, at a CAGR of 7.30% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic venous disorders, varicose veins, and deep vein thrombosis, alongside greater awareness and diagnosis of these conditions, especially in aging populations

- Furthermore, advancements in minimally invasive treatment options such as endovenous laser therapy, sclerotherapy, and radiofrequency ablation are improving patient outcomes and driving adoption. These combined factors are accelerating the uptake of venous disease treatments, thereby significantly boosting the industry's growth

Venous Diseases Treatment Market Analysis

- Venous Treatments for venous diseases including varicose veins, deep vein thrombosis (DVT), and chronic venous insufficiency are becoming essential components of vascular healthcare systems worldwide due to their rising incidence in aging populations and increasing risk factors such as obesity and sedentary lifestyles

- The escalating demand for venous disease therapies is primarily fueled by technological advancements in minimally invasive procedures, greater patient awareness, and the shift toward outpatient care solutions that offer faster recovery and reduced procedural risks

- North America dominated the venous diseases treatment market with the largest revenue share of 40.1% in 2024, driven by advanced healthcare infrastructure, a high patient pool, and strong adoption of endovenous techniques, especially in the U.S., where both private and public healthcare providers continue to invest in modern vascular care technologies

- Asia-Pacific is expected to be the fastest growing region in the venous diseases treatment market during the forecast period due to growing healthcare access, increasing awareness of vascular conditions, and the rising number of specialized clinics offering affordable treatment options

- The ablation devices segment dominated the venous diseases treatment market by product type with a market share of 30.5% in 2024, owing to its widespread adoption in radiofrequency and laser procedures for varicose and incompetent veins

Report Scope and Venous Diseases Treatment Market Segmentation

|

Attributes |

Venous Diseases Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Venous Diseases Treatment Market Trends

“Shift Toward Minimally Invasive and Outpatient Therapies”

- A significant and accelerating trend in the global venous diseases treatment market is the growing adoption of minimally invasive procedures such as endovenous ablation, sclerotherapy, and ambulatory phlebectomy. These techniques are significantly enhancing patient outcomes by offering faster recovery times, reduced procedural risks, and improved comfort compared to traditional vein stripping surgeries

- For instance, radiofrequency ablation (RFA) and endovenous laser therapy (EVLT) are widely replacing conventional surgery for varicose veins, allowing patients to return to daily activities in a matter of days. Similarly, foam sclerotherapy is gaining traction as an outpatient procedure due to its cost-effectiveness and reduced downtime

- Technological advancements in catheters, imaging guidance, and thermal ablation tools are further supporting the shift toward minimally invasive therapies. Devices from companies such as Medtronic and AngioDynamics are enabling physicians to offer precise, targeted vein treatments with fewer complications

- The availability of these procedures in outpatient and clinic-based settings is enhancing accessibility and reducing the burden on hospitals. Patients increasingly prefer treatments that do not require general anesthesia or extended hospital stays, driving the popularity of office-based vein care centers

- This trend toward less invasive, more efficient treatment options is fundamentally reshaping how venous diseases are managed. Consequently, healthcare providers and device manufacturers are focusing on innovation in this space to meet the growing demand for safe, effective, and patient-friendly venous disease treatments

- The demand for minimally invasive venous procedures is growing rapidly across both developed and emerging markets, as consumers and providers increasingly prioritize convenience, cosmetic outcomes, and cost-efficiency in vascular care

Venous Diseases Treatment Market Dynamics

Driver

“Rising Prevalence of Venous Disorders and Aging Population”

- The increasing prevalence of venous disorders such as varicose veins, deep vein thrombosis (DVT), and chronic venous insufficiency (CVI), particularly among the aging population, is a major driver fueling demand for effective treatment solutions

- For instance, global estimates indicate that up to 25–30% of adults are affected by varicose veins, with significantly higher incidence in older individuals and women. Sedentary lifestyles, obesity, and prolonged standing further exacerbate the risk of developing these conditions

- As populations in North America, Europe, and parts of Asia age, the associated rise in vascular conditions is creating sustained demand for both diagnostic and therapeutic interventions. Healthcare systems are increasingly investing in vascular care infrastructure to address this growing burden

- Minimally invasive and outpatient treatments, such as laser therapy, sclerotherapy, and venous stenting, are gaining traction as preferred solutions due to their safety profile and favorable outcomes. These procedures are also supported by a growing number of specialized vein clinics and vascular surgeons

- The rising number of awareness initiatives and screening programs is contributing to early diagnosis and timely intervention, thereby driving patient volumes and supporting market expansion

- The demand for efficient, durable, and aesthetically acceptable treatments is propelling innovation across multiple product categories, positioning venous disease therapy as a key focus within the broader vascular treatment market

Restraint/Challenge

“High Cost of Advanced Therapies and Limited Reimbursement Coverage”

- The relatively high cost of advanced venous treatments, such as endovenous ablation and venous stenting, presents a significant barrier to market penetration, particularly in cost-sensitive or underserved regions

- While these procedures offer improved patient outcomes and lower complication rates, their adoption can be hindered by the upfront expense of specialized devices, imaging equipment, and trained personnel. This makes access difficult for patients without sufficient insurance coverage or disposable income

- For instance, in many developing countries, varicose vein treatment is often considered cosmetic rather than medically necessary, which limits insurance coverage and public health investment. Even in developed markets, reimbursement for newer technologies can vary based on clinical indications and local guidelines

- Addressing these financial barriers will require collaborative efforts between medical device companies, insurers, and healthcare providers to expand reimbursement frameworks and improve affordability. Demonstrating the long-term economic benefits of early intervention—such as reduced complication rates and improved quality of life—will be critical

- In addition, limited awareness among primary care providers and patients in lower-income regions may contribute to underdiagnosis and delayed treatment, compounding the economic impact of untreated venous disease

- Overcoming these challenges through targeted education, value-based pricing strategies, and policy advocacy will be essential for enabling broader access to advanced venous care and ensuring sustained market growth

Venous Diseases Treatment Market Scope

The market is segmented on the basis of product type, disease type, treatment type, end user, and distribution channel.

- By Product Type

On the basis of product type, the venous diseases treatment market is segmented into sclerotherapy injection, ablation devices, venous closure products, venous stents, medication, and others. The ablation devices segment dominated the market with the largest revenue share of 30.5% in 2024, driven by the increasing adoption of minimally invasive procedures such as endovenous laser and radiofrequency ablation. These devices provide effective, outpatient-based treatment options with reduced recovery time, driving their preference over traditional surgeries. The demand is especially high in developed countries where patient preference is shifting toward minimally invasive alternatives.

The sclerotherapy injection segment is anticipated to witness strong growth from 2025 to 2032, due to its cost-effectiveness, simplicity, and increasing use in early-stage varicose vein treatments. It is particularly popular in aesthetic vein clinics and outpatient settings where non-surgical treatments are preferred.

- By Disease Type

On the basis of disease type, the venous diseases treatment market is segmented into deep vein thrombosis (DVT), chronic venous insufficiency (CVI), pulmonary embolism, superficial thrombophlebitis, varicose veins, and others. The varicose veins segment held the largest market share of 31.9% in 2024, owing to its high global prevalence, especially among aging populations and women. The condition is often associated with cosmetic and functional concerns, which drives significant demand for treatments such as ablation and sclerotherapy.

The deep vein thrombosis (DVT) segment is expected to witness fastest growth during the forecast period due to increasing incidence related to lifestyle factors, immobility, and post-surgical complications. Growing awareness of the risks of untreated DVT and the availability of anticoagulant therapy are boosting this segment's development.

- By Treatment Type

On the basis of treatment type, the venous diseases treatment market is segmented into sclerotherapy, radiofrequency ablation therapy, laser treatment, ambulatory phlebectomy, vein ligation and stripping, angioplasty or stenting, surgeries, compression therapy, venoactive medication, vena cava filter, and other therapies. Radiofrequency ablation therapy led the treatment segment with the largest market share of 15.2% in 2024, due to its efficacy, safety, and growing use in minimally invasive vein procedures. It offers rapid recovery and has become a first-line option in many clinical settings for treating incompetent veins.

Laser treatment and sclerotherapy are also growing fastest during forecast period, due to their outpatient convenience, with laser therapy especially favored in combination with ultrasound guidance for precision. Compression therapy remains a foundational conservative treatment, but its long-term compliance challenges slightly limit its dominance.

- By End User

On the basis of end user, the venous diseases treatment market is segmented into hospitals, clinics, ambulatory surgical centers (ASCs), and others. The hospitals segment held the largest revenue share of 42.3% in 2024, due to their comprehensive diagnostic capabilities, surgical facilities, and availability of trained vascular specialists. Hospitals remain the primary destination for complex cases and invasive venous procedures.

The ambulatory surgical centers segment is anticipated to grow with the fastest rate from 2025 to 2032, as more patients opt for outpatient treatments. ASCs offer cost-effective, same-day procedures and cater to the growing demand for minimally invasive therapies such as RFA and sclerotherapy in less intensive care settings.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and others. Direct tender dominated the market with the largest share of 48.1% in 2024, as hospitals and large healthcare facilities procure bulk medical devices, consumables, and medications through tenders from major suppliers. This channel ensures reliable sourcing for high-volume users and institutional buyers.

Retail sales are expected to grow steadily during forecast period, especially for over-the-counter compression products and venoactive medications, supported by increasing consumer awareness and the rise of online pharmacies.

Venous Diseases Treatment Market Regional Analysis

- North America dominated the venous diseases treatment market with the largest revenue share of 40.1% in 2024, driven by advanced healthcare infrastructure, a high patient pool, and strong adoption of endovenous techniques, especially in the U.S., where both private and public healthcare providers continue to invest in modern vascular care technologies

- Patients in the region increasingly seek advanced, outpatient-based therapies such as radiofrequency ablation and sclerotherapy, which offer effective outcomes with minimal recovery time. This demand is further fueled by heightened disease awareness, routine screening, and access to specialized vascular care

- The market’s growth is also supported by an aging population, favorable reimbursement policies, and strong presence of leading medical device manufacturers, positioning North America as a key hub for innovation and procedure volume in venous disease treatment

U.S. Venous Diseases Treatment Market Insight

The U.S. venous diseases treatment market captured the largest revenue share of 84% in 2024 within North America, fueled by a high prevalence of chronic venous disorders, early diagnosis, and wide availability of advanced treatment options. Patients increasingly prefer minimally invasive procedures such as radiofrequency ablation and sclerotherapy offered in outpatient settings. The strong presence of vascular specialists, favorable insurance coverage, and growing awareness campaigns contribute significantly to market growth. In addition, ongoing technological advancements and rising aesthetic concerns support continued adoption across both urban and suburban populations.

Europe Venous Diseases Treatment Market Insight

The Europe venous diseases treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by aging demographics, a high burden of varicose veins and DVT, and strong investments in vascular health. Governments and health institutions are emphasizing early screening and prevention, which is driving treatment volumes. The region is also seeing rising demand for minimally invasive interventions across public and private healthcare facilities, with endovenous techniques gaining traction in both urban hospitals and outpatient centers.

U.K. Venous Diseases Treatment Market Insight

The U.K. venous diseases treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by the increasing focus on outpatient care and NHS-driven initiatives for vascular health. Rising patient awareness about the complications of untreated venous disorders, along with advancements in sclerotherapy and laser-based procedures, is encouraging early treatment adoption. In addition, the growing presence of private vein clinics and innovations in cosmetic vein therapy are boosting demand in both urban and rural populations.

Germany Venous Diseases Treatment Market Insight

The Germany venous diseases treatment market is expected to expand at a considerable CAGR during the forecast period, driven by a strong healthcare infrastructure, high patient awareness, and widespread use of advanced medical technologies. Germany’s well-established vascular care ecosystem encourages the use of innovative, eco-conscious, and minimally invasive treatment options. Procedures such as ambulatory phlebectomy and endovenous ablation are widely used in both public hospitals and private clinics, while insurers support early intervention to reduce long-term healthcare costs.

Asia-Pacific Venous Diseases Treatment Market Insight

The Asia-Pacific venous diseases treatment market is poised to grow at the fastest CAGR of 22.8% during the forecast period of 2025 to 2032, driven by urbanization, increased healthcare access, and rising awareness of chronic venous disorders. Countries such as China, Japan, and India are witnessing growing demand for non-surgical treatments, fueled by a combination of lifestyle changes, aging populations, and government support for vascular disease prevention. Expanding healthcare infrastructure and a rise in medical tourism further support growth across the region.

Japan Venous Diseases Treatment Market Insight

The Japan venous diseases treatment market is gaining momentum due to the country’s advanced healthcare system, aging population, and technological expertise. The increasing prevalence of venous insufficiency and varicose veins is encouraging adoption of modern interventions such as endovenous laser therapy and compression systems. In addition, Japan’s integration of AI and robotics in healthcare is beginning to influence vascular treatment procedures, enhancing precision and patient outcomes in both inpatient and outpatient settings.

India Venous Diseases Treatment Market Insight

The India venous diseases treatment market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country’s large patient base, rising health awareness, and growth in private multispecialty hospitals. Rapid urbanization and sedentary lifestyles have contributed to a rise in venous conditions, driving demand for affordable and minimally invasive solutions. Local manufacturers are increasingly producing cost-effective treatment devices, while the government’s focus on strengthening secondary care facilities and digital health access is improving early diagnosis and treatment adoption.

Venous Diseases Treatment Market Share

The venous diseases treatment industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- Koninklijke Philips N.V., (Netherlands)

- BD (U.S.)

- Cook Medical (U.S.)

- Teleflex Incorporated (U.S.)

- Stryker (U.S.)

- AngioDynamics, Inc. (U.S.)

- LeMaitre Vascular, Inc. (U.S.)

- Terumo Corporation (Japan)

- Cardinal Health, Inc. (U.S.)

- Penumbra, Inc. (U.S.)

- Biotronik SE & Co. KG (Germany)

- Merit Medical Systems, Inc. (U.S.)

- Sirtex Medical Pty Ltd (Australia)

- Endologix LLC (U.S.)

- enVVeno Medical Corporation (U.S.)

- Theraclion SA (France)

- Varicose Vein Center GmbH (Germany)

What are the Recent Developments in Global Venous Diseases Treatment Market?

- In June 2024, Royal Philips launched the FDA-approved Duo Venous Stent System, designed to treat symptomatic venous outflow obstruction in patients with chronic venous insufficiency. Featuring Duo Hybrid and Duo Extend stents, the system demonstrated strong clinical outcomes, including a 90.2% 12-month primary patency in the VIVID trial. This launch underscores Philips' commitment to offering innovative and effective minimally invasive solutions for venous diseases, reinforcing its leadership in vascular care technologies

- In April 2023, the U.S. FDA granted Investigational Device Exemption (IDE) approval for the VEINRESET pivotal trial evaluating Sonovein, a high-intensity focused ultrasound (HIFU) system developed by Theraclion. This trial aims to explore a completely non-invasive approach to treating superficial venous reflux. The regulatory milestone highlights growing interest in non-thermal, non-invasive treatment modalities and reflects Sonovein’s potential to reshape the future of venous disease management

- In December 2023, Theraclion completed the patient enrollment phase for its Sonovein FDA pivotal trial, marking a key milestone toward regulatory approval. The company announced that the 12-month follow-up phase was underway, with data and submission to the FDA expected by mid-2025. This progress showcases continued momentum for HIFU as a promising alternative to conventional endovenous therapies

- In March 2024, enVVeno Medical reported continued advancement in the development of its VenoValve, a surgically implanted device designed to restore valve function in patients with chronic venous insufficiency. The device is currently under evaluation in the U.S.-based SAVVE pivotal trial, with the company also progressing its transcatheter-based enVVe valve. This dual-platform strategy highlights enVVeno’s dedication to addressing unmet needs in both surgical and catheter-based venous valve repair

- In April 2024, AngioDynamics, Inc. received expanded FDA clearance for its AlphaVac F18 System, now approved for the removal of pulmonary emboli in addition to its original indication for venous thromboemboli. This approval broadens the therapeutic utility of the system and reinforces AngioDynamics’ role in offering versatile and innovative solutions for the treatment of complex venous thrombotic conditions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.