Middle East And Africa Healthcare Logistics Market

Market Size in USD Billion

USD

3.22 Billion

USD

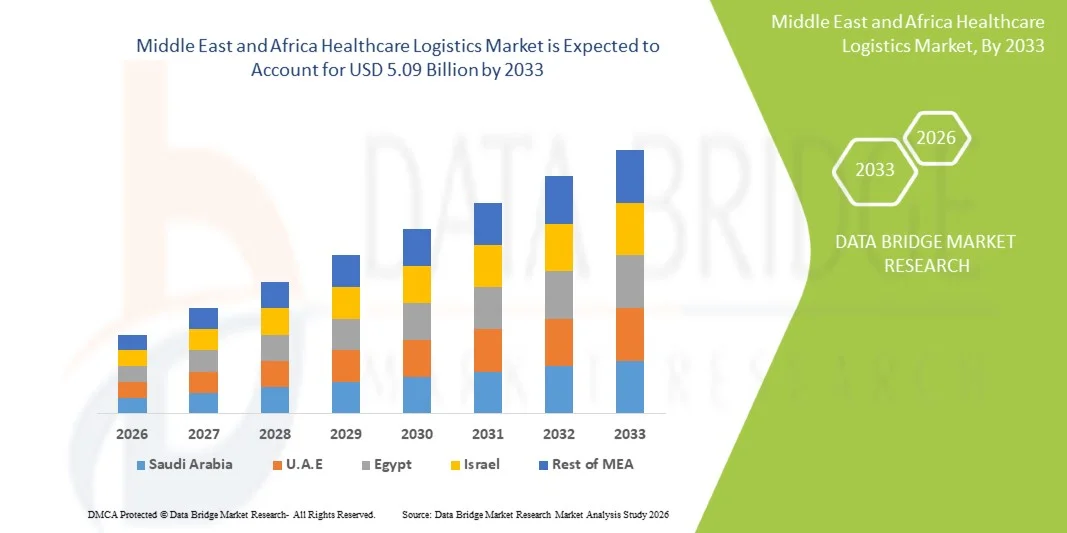

5.09 Billion

2025

2033

USD

3.22 Billion

USD

5.09 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.22 Billion | |

| USD 5.09 Billion | |

| % | |

|

What is the Middle East and Africa Healthcare Logistics Market Size and Growth Rate

- The Middle East and Africa Healthcare Logistics Market size was valued at USD 3.22 billion in 2025 and is expected to reach USD 5.09 billion by 2033, at a CAGR of 5.90% during the forecast period

- The market growth is largely fueled by the increasing demand for efficient healthcare supply chains, rising adoption of digital tracking technologies, and continuous advancements in cold chain infrastructure, automation, and inventory management systems across hospitals, pharmacies, and medical distributors

- Furthermore, growing demand for timely delivery of pharmaceuticals, vaccines, medical devices, and laboratory samples, along with rising focus on regulatory compliance, product safety, and end-to-end visibility, is establishing Healthcare Logistics solutions as a critical component of modern healthcare systems. These converging factors are accelerating the uptake of Healthcare Logistics solutions, thereby significantly boosting the industry's growth

Market Size & Forecast

- Global Market Value (2025): USD 3.22 billion

- Expected Market Value (2033): USD 5.09 billion

- Forecast CAGR (2026–2033): 5.90%

Middle East and Africa Healthcare Logistics Market Analysis

- Healthcare Logistics solutions, including pharmaceutical transportation, cold chain management, warehousing, inventory control, medical device distribution, and last-mile healthcare delivery services, are increasingly vital components of modern healthcare systems due to their role in ensuring timely, safe, and compliant movement of critical medical products.

- The escalating demand for Healthcare Logistics solutions is primarily fueled by rising pharmaceutical production, growing demand for temperature-sensitive biologics and vaccines, increasing healthcare infrastructure investments, and expanding adoption of digital supply chain tracking technologies

- Saudi Arabia dominated the Middle East and Africa Healthcare Logistics Market in the Middle East with the largest revenue share of approximately 36.8% in 2025, characterized by strong healthcare infrastructure expansion, rising pharmaceutical imports, government healthcare modernization initiatives, and increasing investments in cold chain and medical warehousing capabilities

- U.A.E. is expected to be the fastest growing market in the healthcare logistics sector during the forecast period due to expanding healthcare facilities, strong logistics infrastructure, increasing role as a regional distribution hub, and rising investments in smart warehousing, air cargo, and pharmaceutical free-zone capabilities

- The Cold Chain segment dominated the largest market revenue share of 57.8% in 2025, driven by the increasing need for temperature-sensitive transportation of vaccines, biologics, insulin, and specialty medicines

Report Scope and Middle East and Africa Healthcare Logistics Market Segmentation

|

Attributes |

Healthcare Logistics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

What is the Key Trend in the Middle East and Africa Healthcare Logistics Market?

“Enhanced Efficiency Through Cold Chain Modernization and Digital Supply Chain Visibility”

- A significant and accelerating trend in the global Middle East and Africa Healthcare Logistics Market is the increasing adoption of cold chain modernization, IoT-enabled shipment monitoring, and real-time digital supply chain visibility systems to improve the safe transportation of pharmaceuticals, vaccines, biologics, and medical devices. These innovations are strengthening operational efficiency and product integrity worldwide

- Advanced logistics platforms are increasingly being used to monitor temperature-sensitive shipments, optimize routes, and reduce delivery delays across healthcare network

- For instance, companies such as DHL Supply Chain, UPS Healthcare, FedEx HealthCare Solutions, and Kuehne+Nagel provide specialized healthcare logistics services with real-time tracking and validated cold chain solutions

- The growing demand for biologics, specialty drugs, cell and gene therapies, and vaccines is also driving investments in ultra-cold storage, smart warehousing, and compliant transportation systems

- Another major trend is the integration of AI-based demand forecasting and inventory optimization tools that help hospitals, pharmacies, and distributors reduce stockouts and wastage

- In addition, healthcare providers are increasingly outsourcing logistics operations to specialized third-party providers to improve scalability, regulatory compliance, and delivery performance

- This shift toward resilient, technology-enabled, and quality-focused logistics networks is fundamentally reshaping the global healthcare supply chain

Middle East and Africa Healthcare Logistics Market Dynamics

Driver

“Rising Demand for Pharmaceuticals, Vaccines, and Advanced Medical Products”

- Increasing global demand for pharmaceuticals, vaccines, medical devices, and diagnostic products is a major driver for the Middle East and Africa Healthcare Logistics Market. Expanding healthcare access and aging populations are creating higher volumes of healthcare product movement across regions

- Growth in temperature-sensitive medicines and biologics is further accelerating market expansion

- For instance, increasing distribution of mRNA vaccines, insulin products, monoclonal antibodies, and oncology therapies has significantly boosted demand for specialized cold chain logistics services worldwide

- Rising healthcare infrastructure investments in emerging economies are also supporting growth in warehousing, transportation, and last-mile healthcare delivery networks

- Furthermore, the expansion of e-pharmacies, home healthcare, and direct-to-patient delivery models is increasing the need for fast and reliable logistics solutions

- Strong regulatory focus on product traceability, patient safety, and timely delivery is expected to further strengthen market demand during the forecast period

Restraint/Challenge

“High Operational Costs, Regulatory Complexity, and Infrastructure Gaps”

- One of the major challenges restraining the Middle East and Africa Healthcare Logistics Market is the high cost of operating compliant cold chain networks, specialized transportation fleets, secure warehousing facilities, and advanced tracking technologies

- Infrastructure limitations and inconsistent transport networks in some regions can disrupt timely delivery of critical healthcare products

- For instance, remote areas across Africa, parts of Latin America, and certain rural Asian markets may face delays in vaccine and medicine distribution due to inadequate cold storage capacity or limited road connectivity

- Complex and varying regulatory requirements across countries for pharmaceutical handling, customs clearance, and documentation can also increase operational burden

- In addition, rising fuel prices, labor shortages, and geopolitical disruptions may create volatility in healthcare supply chains

- Overcoming these barriers through infrastructure investment, harmonized regulations, automation, and stronger regional distribution partnerships will be essential for sustained market growth

Middle East and Africa Healthcare Logistics Market Scope

The market is segmented on the basis of type, component, temperature type, logistics, logistic type, application, and end user.

• By Type

On the basis of type, the Middle East and Africa Healthcare Logistics Market is segmented into Cold Chain and Non-Cold Chain. The Cold Chain segment dominated the largest market revenue share of 57.8% in 2025, driven by the increasing need for temperature-sensitive transportation of vaccines, biologics, insulin, and specialty medicines. Rising pharmaceutical exports and growing immunization programs across the Middle East and Africa are supporting segment dominance. Cold chain systems are essential to maintain product efficacy and regulatory compliance during transit and storage. Expansion of healthcare infrastructure and advanced warehousing facilities further strengthens demand. Growing investments in refrigerated transportation fleets are also contributing to market leadership. Increased focus on reducing product wastage and spoilage continues to support adoption.

The Non-Cold Chain segment is expected to witness the fastest growth rate of 21.6% from 2026 to 2033, driven by rising demand for conventional pharmaceutical products, medical devices, and healthcare consumables. Increasing healthcare access across emerging economies is significantly boosting shipment volumes. Growth in hospital networks and retail pharmacies is accelerating logistics requirements for non-temperature-sensitive goods. Cost-effectiveness and simpler handling processes are major factors supporting adoption. Expansion of domestic pharmaceutical manufacturing is further driving segment growth. Increasing cross-border healthcare trade activities are strengthening demand. Investments in supply chain modernization are also supporting rapid expansion.

• By Component

On the basis of component, the Middle East and Africa Healthcare Logistics Market is segmented into Hardware, Software, and Services. The Services segment held the largest market revenue share of 46.9% in 2025, driven by increasing outsourcing of transportation, warehousing, inventory management, and distribution activities. Healthcare companies increasingly rely on third-party logistics providers to improve operational efficiency and compliance. Specialized handling requirements for pharmaceuticals and medical goods further support demand. Rising need for last-mile delivery solutions is strengthening service adoption. Growth in regional trade routes and healthcare imports also boosts the segment. Increasing focus on cost optimization reinforces its dominant position.

The Software segment is expected to witness the fastest CAGR of 24.3% from 2026 to 2033, driven by rising adoption of digital supply chain platforms and real-time tracking systems. Logistics companies are investing in warehouse management and transportation management software for better visibility. Growing regulatory requirements for traceability are accelerating demand. AI-enabled route optimization and predictive analytics are supporting market expansion. Increasing smartphone and cloud adoption in the region further strengthens uptake. Demand for automated inventory systems is rising steadily. Digital transformation initiatives continue to fuel rapid growth.

• By Temperature Type

On the basis of temperature type, the Middle East and Africa Healthcare Logistics Market is segmented into Ambient, Chilled/Refrigerated, Frozen and Cryogenic. The Ambient segment accounted for the largest market revenue share of 39.7% in 2025, driven by large-scale transportation of tablets, capsules, medical devices, and general healthcare products. Ambient logistics offers lower transportation costs and easier infrastructure requirements. High demand for routine medicines and hospital supplies supports segment dominance. Expansion of pharmacy chains and healthcare distribution centers is further boosting growth. Increasing urban healthcare access strengthens shipment volumes. Broad applicability across multiple healthcare products supports continued leadership.

The Cryogenic segment is expected to witness the fastest growth rate of 25.1% from 2026 to 2033, driven by increasing transport demand for cell therapies, advanced biologics, and reproductive materials. Growth in precision medicine and biotechnology research is accelerating adoption. Cryogenic systems are essential for maintaining ultra-low temperatures during storage and transit. Rising investments in specialty healthcare infrastructure are supporting demand. Increasing clinical trial activity across the region further boosts growth. Development of advanced cold storage facilities is expanding capacity. Innovation in life sciences logistics continues to drive the segment rapidly.

• By Logistics

On the basis of logistics, the Middle East and Africa Healthcare Logistics Market is segmented into Transportation, Packaging, Storage, and Others. The Transportation segment dominated the largest market revenue share of 42.6% in 2025, driven by high demand for domestic and international movement of medicines, vaccines, and medical equipment. Expansion of road, air, and multimodal transport networks supports strong segment performance. Timely delivery requirements in healthcare make transportation a critical service area. Increasing imports of pharmaceuticals into African markets further strengthen demand. Growth in emergency medical shipments also contributes to leadership. Rising outsourcing to specialized transport providers supports expansion.

The Storage segment is expected to witness the fastest CAGR of 22.7% from 2026 to 2033, driven by increasing need for compliant warehousing and temperature-controlled inventory management. Pharmaceutical companies are expanding regional storage hubs to reduce lead times. Rising demand for vaccine reserves and emergency stockpiles supports growth. Smart warehouses with automated monitoring systems are gaining traction. Increasing healthcare product volumes require advanced storage capacity. Investments in free trade zones and logistics parks are accelerating development. Long-term healthcare infrastructure growth continues to fuel the segment.

• By Logistic Type

On the basis of logistic type, the Middle East and Africa Healthcare Logistics Market is segmented into Sea Freight Logistics, Air Freight Logistics, Overland Logistics, and Contract Logistics. The Overland Logistics segment held the largest market revenue share of 36.4% in 2025, driven by strong reliance on road transportation for domestic and cross-border healthcare deliveries. Trucks and vans are widely used for hospital supply distribution and pharmacy replenishment. Expanding road connectivity across Gulf and African markets supports demand. Cost efficiency and flexible route access strengthen segment leadership. Rising urban healthcare demand further boosts shipment frequency. Growth in regional trade corridors supports continued expansion.

The Air Freight Logistics segment is expected to witness the fastest CAGR of 23.9% from 2026 to 2033, driven by urgent delivery needs for vaccines, biologics, and emergency medical supplies. Air freight provides faster transit times and high reliability for critical shipments. Increasing pharmaceutical imports and exports are supporting market growth. Expansion of airport cargo infrastructure is further accelerating demand. Growing healthcare emergencies and humanitarian aid movements strengthen adoption. Rising cold chain air cargo capabilities continue to support rapid expansion.

• By Application

On the basis of application, the Middle East and Africa Healthcare Logistics Market is segmented into Medicine, Bulk Drug Handlers, Vaccine, Chemical & Other Raw Material, Biological Material, and Organs, Hazardous Cargo and Others. The Medicine segment accounted for the largest market revenue share of 34.8% in 2025, driven by continuous demand for prescription drugs, OTC products, and hospital medicines. Rising chronic disease prevalence is increasing pharmaceutical consumption across the region. Expanding retail pharmacy networks further strengthen shipment volumes. Healthcare reforms and better insurance access are boosting medicine demand. Frequent replenishment cycles support consistent logistics activity. Broad product variety reinforces segment leadership.

The Vaccine segment is expected to witness the fastest growth rate of 24.8% from 2026 to 2033, driven by expanding immunization programs and pandemic preparedness strategies. Governments are investing heavily in vaccine storage and transportation systems. Rising pediatric and adult vaccination awareness supports long-term demand. Cold chain modernization is accelerating efficient vaccine movement. International donor-supported healthcare programs further contribute to growth. Increasing local manufacturing capacity is also boosting logistics needs. Vaccine security and traceability requirements continue to drive rapid expansion.

• By End User

On the basis of end user, the Middle East and Africa Healthcare Logistics Market is segmented into Biopharmaceutical Companies, Hospitals & Clinics, Research Institutes, and Others. The Biopharmaceutical Companies segment dominated the largest market revenue share of 44.1% in 2025, driven by increasing production and trade of medicines, biologics, and specialty therapies. These companies require advanced warehousing, transportation, and compliance-driven logistics solutions. Rising regional pharmaceutical manufacturing investments support strong demand. Export-oriented production hubs are further boosting shipment volumes. Growing product pipelines strengthen outsourcing needs. Expansion of contract manufacturing also reinforces leadership.

The Research Institutes segment is expected to witness the fastest CAGR of 22.5% from 2026 to 2033, driven by increasing clinical trials, biotechnology research, and laboratory sample transport requirements. Governments and private investors are funding life sciences innovation across the region. Sensitive materials require precise and reliable logistics solutions. Growth in academic-medical collaborations is supporting shipment demand. Expansion of biomedical laboratories further boosts the segment. Rising cross-border research partnerships are accelerating logistics activity. Continuous scientific development supports long-term growth.

Middle East and Africa Healthcare Logistics Market Regional Analysis

- The Middle East Middle East and Africa Healthcare Logistics Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rapid healthcare infrastructure development, increasing pharmaceutical imports, and rising demand for efficient medical supply chain management

- Growing investments in hospitals, specialty clinics, and biopharmaceutical manufacturing facilities are fostering the need for advanced healthcare logistics services. Regional stakeholders are also prioritizing temperature-controlled transportation, inventory visibility, and regulatory compliance to ensure safe delivery of medicines and medical devices

- The market is experiencing significant growth across pharmaceutical distribution, medical equipment transportation, vaccine storage, and hospital supply chain applications, with logistics modernization becoming a strategic priority across the region

Saudi Arabia Middle East and Africa Healthcare Logistics Market Insight

Saudi Arabia Middle East and Africa Healthcare Logistics Market dominated the Middle East and Africa Healthcare Logistics Market in the Middle East with the largest revenue share of approximately 36.8% in 2025, characterized by strong healthcare infrastructure expansion, rising pharmaceutical imports, government healthcare modernization initiatives, and increasing investments in cold chain and medical warehousing capabilities. The country’s Vision 2030 healthcare transformation strategy is accelerating demand for reliable logistics networks, automated warehouses, and efficient last-mile medical delivery services. Moreover, increasing demand for specialty drugs, biologics, and imported medical technologies is significantly contributing to market growth.

U.A.E. Middle East and Africa Healthcare Logistics Market Insight

The U.A.E. Middle East and Africa Healthcare Logistics Market is expected to be the fastest growing market during the forecast period, driven by expanding healthcare facilities, world-class logistics infrastructure, and its increasing role as a regional healthcare distribution hub. The country is witnessing rising investments in smart warehousing, air cargo capacity, pharmaceutical free zones, and advanced cold chain transportation systems. Dubai and Abu Dhabi continue to strengthen their positions as strategic gateways for healthcare product movement across the Middle East, Africa, and South Asia. Additionally, increasing adoption of digital supply chain platforms and customs efficiency is expected to further stimulate market expansion.

Middle East and Africa Healthcare Logistics Market Share

The Healthcare Logistics industry is primarily led by well-established companies, including:

- DHL Group (Germany)

- UPS Healthcare (U.S.)

- FedEx Corporation (U.S.)

- Kuehne + Nagel International AG (Switzerland)

- DB Schenker (Germany)

- SF Express Co., Ltd. (China)

- Nippon Express Co., Ltd. (Japan)

- C.H. Robinson Worldwide, Inc. (U.S.)

- CEVA Logistics (France)

- DSV A/S (Denmark)

- AmerisourceBergen Corporation (U.S.)

- Cardinal Health, Inc. (U.S.)

- McKesson Corporation (U.S.)

- Agility Logistics (Kuwait)

- Aramex PJSC (U.A.E.)

- Gulf Warehousing Company (Qatar)

- Yusen Logistics Co., Ltd. (Japan)

- Hellmann Worldwide Logistics (Germany)

- Expeditors International (U.S.)

- GEODIS (France)

Latest Developments in Middle East and Africa Healthcare Logistics Market

- In April 2021, UPS Healthcare announced the expansion of its cold chain and healthcare logistics capabilities across Europe and North America to support rising demand for vaccine distribution, biologics, and temperature-sensitive pharmaceuticals. The expansion strengthened UPS’s position in precision healthcare logistics during a period of global supply chain stress.

- In September 2021, DHL Supply Chain expanded dedicated life sciences and healthcare logistics solutions, including temperature-controlled warehousing and compliant transport networks for pharmaceuticals and medical devices. The move reflected increasing outsourcing of regulated healthcare supply chains to specialized logistics providers.

- In March 2023, UPS Healthcare unveiled a new 20,000-square-foot cold chain warehouse in Singapore as part of its Asia-Pacific expansion strategy. The facility, equipped with real-time monitoring systems and storage capacity from 2°C to -80°C, was designed to meet growing regional demand for advanced healthcare logistics services.

- In April 2023, DHL Supply Chain announced the expansion of its global cold chain logistics network with the launch of new temperature-controlled facilities in India and the Netherlands. This strategic investment enhanced end-to-end delivery of biologics, vaccines, and high-value pharmaceuticals, reinforcing DHL’s commitment to compliant and secure healthcare logistics solutions.

- In February 2024, FedEx announced its new FedEx Life Science Center in India to support the clinical trial logistics and storage requirements of healthcare customers in India and companies shipping into the country. The launch strengthened FedEx’s healthcare presence in one of the fastest-growing pharmaceutical markets globally.

- In September 2024, UPS announced plans to acquire Germany-based Frigo-Trans and its sister company BPL to enhance healthcare cold-chain capabilities in Europe. The acquisition added temperature-controlled warehousing, freight forwarding, and pan-European cold chain transportation services to UPS Healthcare’s portfolio.

- In January 2025, UPS completed the acquisitions of Frigo-Trans and BPL, accelerating its strategy to provide end-to-end temperature-controlled healthcare logistics solutions across Europe. The deal expanded capabilities ranging from cryopreservation logistics (-196°C) to ambient pharmaceutical distribution.

- In March 2025, DHL Group announced the acquisition of CRYOPDP from Cryoport to strengthen DHL Health Logistics. CRYOPDP is a specialty courier focused on clinical trials, biopharma, and cell & gene therapies, and the acquisition significantly enhanced DHL’s global life sciences supply chain capabilities.

- In April 2025, UPS announced its agreement to acquire Canada-based Andlauer Healthcare Group for USD 1.6 billion to strengthen healthcare logistics operations in North America. The acquisition expanded UPS’s portfolio of cold chain, temperature-sensitive transportation, and third-party logistics services

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.