Middle East And Africa Lymphangioleiomyomatosis Lam Market

Market Size in USD Million

USD

6.44 Million

USD

8.35 Million

2024

2032

USD

6.44 Million

USD

8.35 Million

2024

2032

| 2025 - 2032 | |

| USD 6.44 Million | |

| USD 8.35 Million | |

| % | |

|

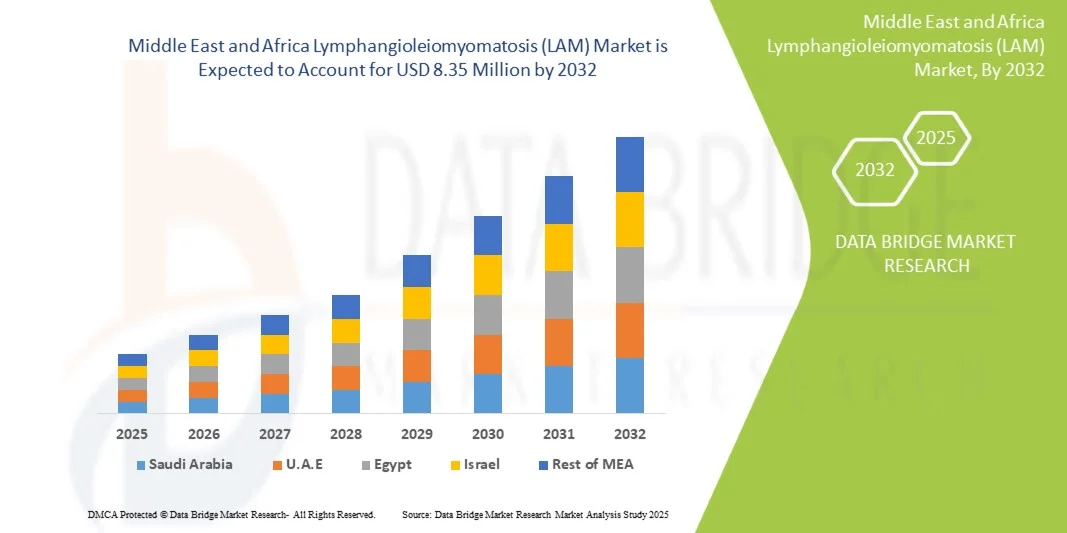

Middle East and Africa Lymphangioleiomyomatosis (LAM) Market Size

- The Middle East and Africa Lymphangioleiomyomatosis (LAM) market size was valued at USD 6.44 million in 2024 and is expected to reach USD 8.35 million by 2032, at a CAGR of 3.30% during the forecast period

- The market growth is primarily driven by increasing awareness of rare lung diseases, growing access to advanced diagnostic techniques, and expanding healthcare infrastructure across the region, which are improving early detection and treatment of LAM

- Moreover, the rising focus of global pharmaceutical companies on expanding into emerging markets, along with regional initiatives promoting rare disease research and patient support, is fostering market development. These combined factors are contributing to the steady growth of the Middle East and Africa LAM market

Middle East and Africa Lymphangioleiomyomatosis (LAM) Market Analysis

- Lymphangioleiomyomatosis (LAM), a rare lung disease that primarily affects women of reproductive age, is gaining increasing clinical awareness across the Middle East and Africa, supported by advancements in diagnostic imaging, research collaborations, and growing investments in rare disease care infrastructure

- The market growth is largely driven by rising prevalence of chronic respiratory conditions, improved access to specialized healthcare, and expanding diagnostic capabilities, enabling earlier identification and management of LAM cases

- Saudi Arabia dominated the Middle East and Africa LAM market with the largest revenue share of 32.9% in 2024, attributed to strong government initiatives for rare disease management, well-established healthcare facilities, and collaborations with international research institutions

- South Africa is projected to be the fastest-growing country in the market during the forecast period, fueled by growing awareness, improving clinical expertise, and enhanced access to diagnostic and treatment options for rare lung disorders

- The treatment segment dominated the market with the largest share of 59.2% of the Middle East and Africa LAM market in 2024, driven by increasing use of pharmacological therapies, ongoing clinical trials, and supportive healthcare policies promoting effective disease management

Report Scope and Middle East and Africa Lymphangioleiomyomatosis (LAM) Market Segmentation

|

Attributes |

Middle East and Africa Lymphangioleiomyomatosis (LAM) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Lymphangioleiomyomatosis (LAM) Market Trends

“Advancements in Diagnostic Imaging and Early Detection”

- A significant and accelerating trend in the Middle East and Africa LAM market is the growing adoption of advanced diagnostic imaging technologies such as high-resolution computed tomography (HRCT) and genetic testing, which are improving early detection and disease characterization

- For instance, HRCT is increasingly being utilized across tertiary hospitals in Saudi Arabia and the UAE to identify cystic lung lesions associated with LAM, enabling earlier intervention and more effective disease management

- The integration of advanced diagnostic tools and biomarker-based testing allows for more accurate differentiation between LAM and other lung conditions, leading to timely treatment decisions and improved patient outcomes. For instance, specialized centers in South Africa are employing genetic screening to identify TSC gene mutations associated with tuberous sclerosis complex LAM. Furthermore, these technological advances are aiding in disease monitoring and therapy evaluation

- The establishment of multidisciplinary care models that combine pulmonology, radiology, and genetics is creating a more comprehensive approach to LAM management. Through coordinated care, patients receive streamlined diagnostics, personalized treatment plans, and long-term monitoring

- This trend toward precision diagnostics and integrated care is fundamentally improving disease awareness and treatment outcomes across the region. Consequently, countries such as Saudi Arabia and the UAE are strengthening collaborations with international research institutions to enhance diagnostic and clinical capabilities

- The demand for accurate, early, and non-invasive LAM diagnostics is growing rapidly across hospitals and specialty clinics, as healthcare providers increasingly focus on improving patient quality of life and long-term disease management

Middle East and Africa Lymphangioleiomyomatosis (LAM) Market Dynamics

Driver

“Rising Awareness and Expanding Access to Rare Disease Treatment”

- The increasing awareness of rare pulmonary diseases and improving healthcare infrastructure across Middle Eastern and African countries are significant drivers propelling the LAM market growth

- For instance, in March 2024, King Faisal Specialist Hospital in Saudi Arabia initiated a rare lung disease program to enhance early detection and treatment accessibility for LAM and similar disorders. Such initiatives by regional healthcare institutions are expected to drive the market during the forecast period

- As physicians and patients become more informed about LAM symptoms and available treatment options, diagnosis rates are improving, supporting timely medical interventions and improved outcomes

- Furthermore, government-led health reforms and international collaborations with rare disease organizations are promoting access to advanced therapies such as mTOR inhibitors, expanding treatment availability across the region

- The growing role of hospitals and specialty clinics in providing dedicated care pathways, along with awareness campaigns, is increasing patient engagement and disease recognition, strengthening overall healthcare response to LAM. The integration of modern diagnostic technologies and improved clinical training among pulmonologists are also fueling growth

- The shift toward early diagnosis and the rising adoption of standardized care practices are key factors propelling the market, while enhanced investment in research and patient registries further contributes to long-term development

Restraint/Challenge

“Limited Disease Awareness and High Treatment Costs”

- The rarity of LAM and limited public awareness across several Middle Eastern and African countries pose a significant challenge to widespread disease diagnosis and management. Many patients remain undiagnosed or are misdiagnosed due to overlapping symptoms with other respiratory disorders

- For instance, in resource-limited healthcare settings across Sub-Saharan Africa, LAM is often mistaken for asthma or chronic obstructive pulmonary disease (COPD), delaying accurate diagnosis and appropriate treatment initiation

- Addressing these awareness gaps through physician education, improved diagnostic infrastructure, and patient advocacy programs is essential for improving detection rates and access to care. For instance, rare disease organizations in South Africa and the UAE are working to increase LAM visibility through workshops and awareness drives. In addition, inconsistent access to high-resolution imaging and genetic testing further constrains early detection efforts

- The high cost of lifelong treatment, particularly mTOR inhibitors such as sirolimus, remains a major barrier to therapy accessibility, especially in low-income populations or areas lacking reimbursement support

- While pharmaceutical pricing reforms and international aid programs are being introduced, affordability continues to be a restraint for sustained treatment adherence, limiting long-term patient management

- Overcoming these challenges through regional partnerships, government subsidies, and public–private collaboration for rare disease funding will be vital to ensuring equitable access and continuous care for LAM patients in the Middle East and Africa

Middle East and Africa Lymphangioleiomyomatosis (LAM) Market Scope

The market is segmented on the basis of disease type, type, complications, route of administration, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the Middle East and Africa LAM market is segmented into Tuberous Sclerosis Complex (TSC) LAM and Sporadic LAM. The Sporadic LAM segment dominated the market with the largest revenue share in 2024, primarily due to its higher prevalence across the region and increasing diagnostic accuracy through high-resolution computed tomography (HRCT). Sporadic LAM cases are more frequently identified in women without a family history of tuberous sclerosis, making it the most reported form in clinical settings. Growing awareness among pulmonologists and the adoption of advanced imaging in countries such as Saudi Arabia and South Africa have contributed significantly to this dominance. The presence of referral networks and specialist pulmonary clinics has also improved case recognition and management. Furthermore, ongoing regional health initiatives focusing on rare lung diseases continue to enhance early identification and monitoring of sporadic LAM.

The Tuberous Sclerosis Complex (TSC) LAM segment is projected to witness the fastest growth rate during the forecast period, driven by expanding access to genetic testing and molecular diagnostics in tertiary hospitals. Increasing awareness of TSC-related manifestations, coupled with the integration of genetic screening programs in the UAE and South Africa, is enabling early detection among women with tuberous sclerosis. The rising number of collaborations between healthcare authorities and international research networks is further supporting this segment’s growth. In addition, advancements in diagnostic imaging and multidisciplinary care models are improving disease surveillance and treatment outcomes for TSC-LAM patients in the region.

- By Type

On the basis of type, the market is segmented into diagnosis and treatment. The Treatment segment dominated the Middle East and Africa LAM market with the largest revenue share of 59.2% in 2024, owing to the rising use of pharmacological therapies such as mTOR inhibitors (sirolimus and everolimus). These drugs have proven clinical efficacy in stabilizing lung function and reducing disease progression. Increased healthcare spending in Saudi Arabia and the UAE, along with the introduction of rare disease reimbursement programs, has supported wider therapeutic adoption. Hospitals and specialty clinics across the region are increasingly adopting international treatment guidelines to ensure standardized care. Moreover, growing patient awareness and expanded availability of essential drugs through hospital pharmacies further enhance the treatment segment’s dominance.

The Diagnosis segment is anticipated to register the fastest growth during the forecast period, driven by the growing use of HRCT imaging, biomarker testing (VEGF-D), and genetic screening tools. The integration of these diagnostic methods in tertiary hospitals and research laboratories is enabling earlier and more accurate detection of LAM. For instance, specialized centers in South Africa and the UAE are implementing targeted diagnostic protocols for suspected LAM patients. Increasing physician education, improved referral systems, and investment in diagnostic infrastructure are key contributors to this segment’s growth. The introduction of awareness programs by rare disease organizations is also boosting early diagnostic rates across the region.

- By Complications

On the basis of complications, the market is categorized into pneumothorax, chylothorax, kidney tumor, pleural effusions, swelling & fluid build-up, and others. The Pneumothorax segment dominated the Middle East and Africa LAM market in 2024 with the largest revenue share, as it remains the most common and clinically significant complication in LAM patients. Pneumothorax often requires hospitalization and surgical intervention, increasing healthcare spending and clinical attention in this area. The rising number of emergency care facilities equipped with thoracic specialists in Saudi Arabia and South Africa has improved management and outcomes of these complications. Increasing awareness among clinicians of recurrent pneumothorax as an early indicator of LAM has also enhanced diagnosis rates. Furthermore, ongoing research on pleurodesis techniques and preventive management is strengthening this segment’s market position.

The Kidney Tumor segment is expected to grow at the fastest rate during the forecast period, supported by rising detection of angiomyolipomas in LAM patients through routine imaging. The use of MRI and ultrasound screening in tertiary hospitals has improved renal tumor diagnosis, particularly in TSC-associated cases. Multidisciplinary collaboration between nephrologists and pulmonologists is further enabling comprehensive disease management. Increased research funding and advancements in minimally invasive procedures are improving patient outcomes. In addition, the introduction of targeted therapies and early imaging programs in the UAE and South Africa are propelling this segment’s expansion.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and parenteral. The Oral segment dominated the market in 2024, accounting for the largest share due to the convenience, safety, and adherence benefits associated with oral drug delivery. Oral mTOR inhibitors such as sirolimus remain the preferred treatment option for long-term management of LAM due to their established efficacy and ease of administration. Hospitals and specialty clinics in Saudi Arabia and the UAE are prescribing oral therapies as first-line treatment to ensure patient compliance. In addition, the expansion of online and hospital pharmacy networks ensures consistent drug availability. The preference for oral medications is further reinforced by favorable patient outcomes and minimal invasiveness.

The Parenteral segment is projected to exhibit the fastest growth over the forecast period, driven by ongoing clinical research into biologic agents and injectable formulations for advanced LAM cases. Parenteral delivery allows for targeted and faster-acting therapeutic effects, which are particularly beneficial for patients with severe disease progression. Increasing investments in clinical research by regional academic institutions are enhancing awareness and access to injectable therapies. Hospitals in South Africa and the UAE are increasingly equipped to administer parenteral therapies safely under specialist supervision. The development of new formulations and delivery methods is expected to further expand the segment’s scope in the coming years.

- By End User

On the basis of end user, the Middle East and Africa LAM market is segmented into hospitals, specialty clinics, diagnostic centers, home healthcare, and others. The Hospitals segment dominated the market with the largest share in 2024, owing to their central role in diagnosis, drug administration, and surgical management of complications. Hospitals in Saudi Arabia, the UAE, and South Africa have developed specialized pulmonary units capable of providing integrated LAM care, from diagnosis to treatment follow-up. The presence of government-supported healthcare facilities and skilled pulmonologists ensures wide accessibility to patients. Hospitals also facilitate multidisciplinary collaboration among specialists in pulmonology, nephrology, and radiology, which enhances patient outcomes. In addition, the growing number of hospital-based rare disease centers is strengthening this segment’s market share.

The Specialty Clinics segment is anticipated to register the fastest growth during the forecast period, driven by the emergence of rare disease-focused outpatient facilities and increasing preference for personalized care. These clinics offer specialized diagnostic and therapeutic services tailored for LAM patients, ensuring close monitoring and consistent disease management. The trend toward telemedicine integration and outpatient consultation in the UAE and South Africa is expanding access to care for rural and underserved populations. Specialty clinics also play a vital role in coordinating patient education and facilitating participation in clinical studies. The combination of affordability, flexibility, and convenience is expected to accelerate this segment’s expansion through 2032.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, hospital pharmacies, retail pharmacies, online pharmacies, and others. The Hospital Pharmacies segment dominated the Middle East and Africa LAM market in 2024, driven by the centralized distribution of prescription drugs and the critical role hospitals play in managing rare diseases. Hospital pharmacies ensure controlled access to essential therapies, particularly sirolimus, and provide necessary patient counseling for long-term treatment adherence. The reliability of hospital procurement systems and inclusion of LAM drugs in public healthcare formularies in Saudi Arabia and the UAE further contribute to this dominance. Moreover, hospital pharmacists collaborate with clinicians to optimize dosage and monitor side effects, reinforcing patient safety.

The Online Pharmacies segment is projected to grow at the fastest rate over the forecast period, supported by digital health advancements and the growing preference for home delivery of chronic disease medications. Expanding e-pharmacy networks in South Africa and the UAE, coupled with regulatory improvements for prescription-based sales, are facilitating access to rare disease therapies. The convenience of remote ordering and competitive pricing are attracting patients seeking long-term refills. In addition, the rise of teleconsultation platforms that directly link with e-pharmacy services is enhancing medication adherence. As awareness of digital healthcare rises, online channels are expected to play a pivotal role in improving LAM drug accessibility across the region.

Middle East and Africa Lymphangioleiomyomatosis (LAM) Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa LAM market with the largest revenue share of 32.9% in 2024, attributed to strong government initiatives for rare disease management, well-established healthcare facilities, and collaborations with international research institutions

- The country’s strong government support through the Vision 2030 healthcare initiatives has led to the establishment of advanced diagnostic centers and rare disease registries, enabling early identification and treatment of LAM cases

- Rising awareness among pulmonologists and genetic specialists has driven early diagnosis, while national rare disease campaigns have enhanced patient engagement and data collection

The Saudi Arabia Lymphangioleiomyomatosis (LAM) Market Insight

The Saudi Arabia LAM market dominated the region with a revenue share of 32.9% in 2024, supported by strong healthcare modernization under Vision 2030 and the presence of specialized respiratory centers. The country’s government-led initiatives are improving access to advanced therapeutics such as mTOR inhibitors and enhancing disease awareness among clinicians. Collaborations between research institutions and international biopharma companies are promoting clinical trials and genetic research related to LAM. Moreover, increasing investments in digital health platforms are facilitating early diagnosis and patient follow-ups. These factors collectively strengthen Saudi Arabia’s leading position in the Middle East and Africa LAM market.

United Arab Emirates (UAE) Lymphangioleiomyomatosis (LAM) Market Insight

The UAE LAM market is projected to grow at the fastest CAGR during the forecast period, fueled by rapid healthcare advancements, international collaborations, and an increasing focus on rare disease management. The country’s robust healthcare infrastructure, supported by both public and private sector investments, is enabling timely diagnosis and access to innovative treatments. Medical tourism initiatives and partnerships with global pharmaceutical companies are enhancing the availability of specialized LAM care. Moreover, growing awareness among pulmonologists and the introduction of advanced imaging technologies in hospitals are fostering the expansion of the LAM market in the UAE.

South Africa Lymphangioleiomyomatosis (LAM) Market Insight

The South Africa LAM market is witnessing steady development, driven by the country’s increasing adoption of rare disease registries and growing access to diagnostic tools in tertiary hospitals. Government and private organizations are collaborating to enhance awareness and training among healthcare professionals for better identification of rare conditions such as LAM. Though access to targeted therapies remains limited, ongoing initiatives by health ministries and research partnerships are expected to improve treatment availability. The rising number of clinical studies and educational programs is strengthening South Africa’s role as a key market for LAM management within the African continent.

Egypt Lymphangioleiomyomatosis (LAM) Market Insight

Egypt’s LAM market is gradually expanding due to increasing awareness among pulmonologists, improved diagnostic capabilities, and ongoing efforts to integrate rare disease management within the national healthcare framework. The government’s focus on upgrading healthcare facilities and expanding patient support programs is aiding early detection and treatment access. Collaborations between Egyptian universities and international research networks are promoting genetic and epidemiological studies on LAM. In addition, efforts to improve drug availability through hospital and retail pharmacies are anticipated to accelerate market growth.

Middle East and Africa Lymphangioleiomyomatosis (LAM) Market Share

The Middle East and Africa Lymphangioleiomyomatosis (LAM) industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Johnson & Johnson Services, Inc. (U.S.)

- Merck & Co., Inc., (U.S.)

- AstraZeneca (U.K.)

- GSK plc (U.K.)

- Sanofi (France)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- AbbVie Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Eli Lilly and Company (U.S.)

- Ipsen Pharma (France)

- Amgen Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Abbott (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- QIAGEN (Netherlands)

- BIOMÉRIEUX (France)

What are the Recent Developments in Middle East and Africa Lymphangioleiomyomatosis (LAM) Market?

- In August 2024, The LAM Foundation publicly recorded that it expanded its LAM Clinic & Research Network in 2023 listing clinics added in 2023 that included Johannesburg, South Africa. The filing also documents intensified virtual programming and global outreach that help identify and connect patients in under-served regions

- In March 2024, a Johns Hopkins Medicine blog reported a pulmonary clinic joining the LAM Foundation Clinic & Research Network, an instance of major academic centres expanding the global care network and workflow for LAM patients. That same trend improves referral pathways for patients in neighbouring regions and supports clinicians in MEA to obtain expert collaboration and participate in trials

- In December 2023, a detailed case report of LAM with retroperitoneal masses during pregnancy was published in Frontiers in Medicine. The paper highlights diagnostic challenges, the role of HRCT and pathology/VEGF-D in diagnosis, and successful management including surgery a useful instance that raised clinical awareness of atypical/extrapulmonary LAM presentations relevant to clinicians worldwide, including physicians in MEA who face similar diagnostic pitfalls

- In September 2023, presentations at the ERS International Congress included sessions and posters reporting new diagnostic approaches and biomarker work for cystic lung diseases including LAM. Those ERS activities strengthened international best-practice dissemination, improving recognition/diagnosis in the region

- In February 2021, a systematic review of LAM diagnosis and molecular mechanisms was published in Biomed Research International a comprehensive review that summarized diagnostic criteria, molecular drivers and therapeutic implications. This review underpins many subsequent diagnosis/treatment decisions worldwide and has been widely cited by clinicians in all regions, helping raise the baseline of regional clinical knowledge

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.