Middle East And Africa Thyroid Cancer Diagnostics Market

Market Size in USD Million

USD

314.61 Million

USD

457.79 Million

2024

2032

USD

314.61 Million

USD

457.79 Million

2024

2032

| 2025 - 2032 | |

| USD 314.61 Million | |

| USD 457.79 Million | |

| % | |

|

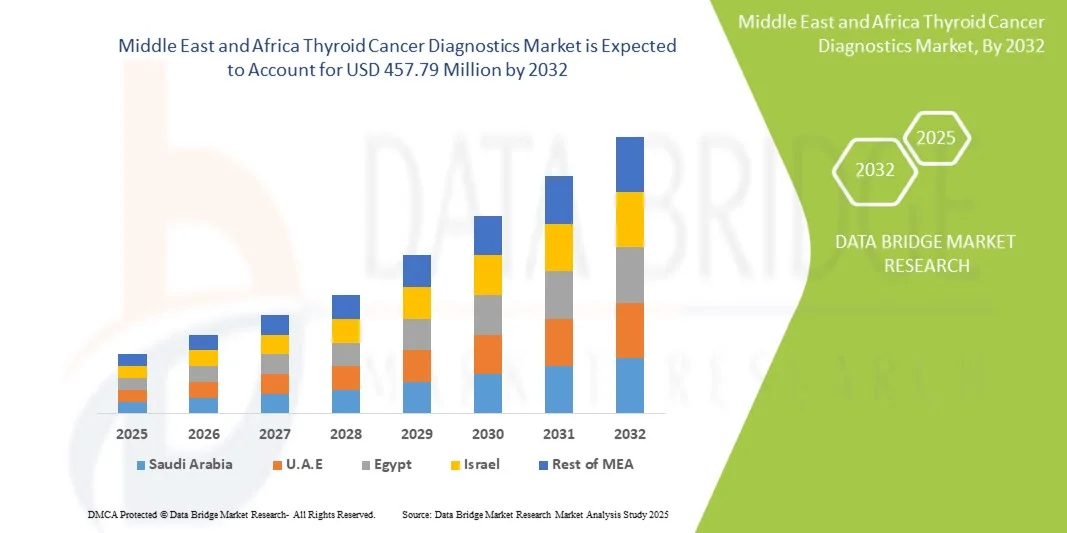

Middle East and Africa Thyroid Cancer Diagnostics Market Size

- The Middle East and Africa thyroid cancer diagnostics market size was valued at USD 314.61 million in 2024 and is expected to reach USD 457.79 million by 2032, at a CAGR of 4.8% during the forecast period

- The market growth is largely fueled by the increasing prevalence of thyroid cancer, especially among women in the UAE, and the rising adoption of advanced diagnostic techniques such as molecular testing and next-generation sequencing (NGS) panels, leading to improved early detection and personalized treatment planning

- Furthermore, growing demand for accurate, rapid, and minimally invasive diagnostic solutions in both clinical and hospital settings is establishing modern molecular and imaging-based diagnostics as the preferred choice. These converging factors are accelerating the uptake of thyroid cancer diagnostics, thereby significantly boosting the industry's growth

Middle East and Africa Thyroid Cancer Diagnostics Market Analysis

- Thyroid cancer diagnostics, encompassing imaging, biopsy, and blood tests for early detection and characterization of thyroid nodules, are becoming essential tools in both clinical and hospital settings across the Middle East and Africa due to their ability to improve diagnostic accuracy, guide personalized treatment, and reduce invasive procedures

- The rising demand for thyroid cancer diagnostics is primarily driven by increasing prevalence of thyroid cancer, especially among women, growing awareness of early detection benefits, and adoption of advanced imaging and biopsy techniques across hospitals and diagnostic centers

- Saudi Arabia dominated the MEA thyroid cancer diagnostics market with the largest revenue share of 39% in 2024, attributed to higher healthcare spending, advanced medical infrastructure, and rising incidence rates, with major hospitals and diagnostic centers adopting imaging and biopsy diagnostics extensively

- United Arab Emirates is expected to be the fastest growing country in the MEA thyroid cancer diagnostics market during the forecast period due to increasing investment in healthcare infrastructure, growing diagnostic awareness, and expanding access to modern laboratories

- Instruments segment dominated the MEA thyroid cancer diagnostics market with a market share of 45.7% in 2024, driven by widespread adoption of imaging and biopsy devices in hospitals, associated labs, and diagnostic imaging centers for accurate and timely diagnosis

Report Scope and Middle East and Africa Thyroid Cancer Diagnostics Market Segmentation

|

Attributes |

Middle East and Africa Thyroid Cancer Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Middle East and Africa Thyroid Cancer Diagnostics Market Trends

Advancements in Imaging and Biopsy Technologies

- A significant and accelerating trend in the MEA thyroid cancer diagnostics market is the adoption of high-resolution ultrasound, fine-needle aspiration (FNA), and molecular testing technologies, which are enhancing diagnostic accuracy and reducing unnecessary surgeries

- For instance, advanced ultrasound systems in leading hospitals in Saudi Arabia allow clinicians to detect smaller nodules with higher precision, improving early-stage diagnosis and patient outcomes

- Molecular diagnostics integration enables identification of genetic mutations in thyroid nodules, helping guide personalized treatment plans and risk stratification

- The combination of imaging, biopsy, and molecular testing facilitates comprehensive evaluation through a single workflow, allowing clinicians to make informed treatment decisions efficiently

- This trend towards more accurate, minimally invasive, and integrated diagnostics is reshaping expectations for thyroid cancer care, prompting diagnostic labs and hospitals to invest in cutting-edge instruments

- The demand for advanced thyroid cancer diagnostics is growing rapidly across hospitals, diagnostic imaging centers, and associated laboratories, as patients and healthcare providers prioritize early detection and precise diagnosis

Middle East and Africa Thyroid Cancer Diagnostics Market Dynamics

Driver

Increasing Prevalence and Awareness of Thyroid Cancer

- The rising incidence of thyroid cancer in MEA countries, particularly among women, coupled with growing awareness of early detection benefits, is a key driver for the adoption of advanced diagnostics

- For instance, hospitals in the UAE have reported increasing patient visits for thyroid nodule evaluation, encouraging investment in ultrasound, biopsy, and molecular testing solutions

- Improved access to diagnostic technologies in urban centers allows clinicians to detect cancer at early stages, improving prognosis and treatment success rates

- Government health initiatives and awareness campaigns are promoting routine screenings, further boosting market growth

- Rising insurance coverage for diagnostic procedures is encouraging more patients to opt for advanced thyroid cancer testing

- Partnerships between international diagnostic companies and local healthcare providers are facilitating the introduction of cutting-edge diagnostic solutions in the region

- The convenience of minimally invasive procedures, rapid reporting, and integration of multiple testing modalities makes these diagnostics increasingly preferred in hospitals and diagnostic laboratories

Restraint/Challenge

High Cost and Limited Accessibility in Some Regions

- The relatively high cost of advanced imaging and molecular testing solutions poses a challenge for widespread adoption, particularly in low-resource areas within MEA

- For instance, smaller clinics and rural diagnostic centers often face budget constraints that limit procurement of state-of-the-art ultrasound or molecular testing instruments

- Limited availability of trained personnel to operate advanced diagnostic systems can slow adoption, particularly in emerging healthcare markets

- Regulatory approvals and quality certifications for new diagnostic instruments may delay market entry and increase operational costs for suppliers

- Addressing these challenges through affordable testing solutions, mobile diagnostic units, and training programs for medical staff will be vital for broader market penetration

- Variability in healthcare infrastructure and regional disparities in medical service quality can limit the reach of advanced diagnostic technologies

- Data privacy and handling concerns related to molecular diagnostics and telemedicine solutions may slow adoption unless robust compliance measures are implemented

Middle East and Africa Thyroid Cancer Diagnostics Market Scope

The market is segmented on the basis of product type, test type, cancer type, stages, age group, end user, and distribution channel.

- By Product Type

On the basis of product type, the MEA thyroid cancer diagnostics market is segmented into instruments and consumables & accessories. The instruments segment dominated the market with the largest revenue share of 45.7% in 2024, driven by widespread adoption of imaging and biopsy devices in hospitals, associated labs, and diagnostic imaging centers. Hospitals prefer instruments such as high-resolution ultrasound machines and fine-needle aspiration systems due to their accuracy, reliability, and ability to deliver rapid results. These devices also support integration with molecular testing platforms, enabling comprehensive evaluation of thyroid nodules. Investments in modern hospitals across Saudi Arabia and UAE are further supporting the adoption of diagnostic instruments. The demand is also fueled by the increasing prevalence of thyroid cancer, encouraging continuous upgrades of diagnostic infrastructure. Furthermore, the resale and maintenance potential of these instruments adds to the overall market attractiveness.

The consumables & accessories segment is expected to witness the fastest growth from 2025 to 2033, driven by rising demand for biopsy needles, reagents, slides, and kits required for molecular testing and imaging procedures. Consumables are recurring purchase items, ensuring steady revenue for suppliers. The segment benefits from increasing patient visits and frequent testing requirements in both hospitals and independent diagnostic laboratories. In addition, the growing adoption of minimally invasive diagnostic procedures is propelling the need for specialized consumables. Urban healthcare centers in UAE and Saudi Arabia are increasingly stocking advanced consumables to support early and accurate thyroid cancer diagnosis. The shift towards integrated diagnostic workflows combining imaging, biopsy, and molecular tests also accelerates consumables demand.

- By Test Type

On the basis of test type, the market is segmented into imaging test, biopsy, blood test, and others. The imaging test segment dominated the market in 2024 due to its ability to detect thyroid nodules non-invasively, with high accuracy and early-stage detection potential. Imaging modalities such as high-resolution ultrasound and elastography are widely used in hospitals and diagnostic imaging centers across MEA. They provide clinicians with critical information regarding nodule size, structure, and vascularity, which informs biopsy decisions. The segment is supported by increasing investment in diagnostic imaging infrastructure and the rising incidence of thyroid cancer. Frequent monitoring and follow-ups for patients further contribute to market revenue. Training programs for radiologists and clinicians on advanced imaging technologies also enhance adoption.

The biopsy segment is expected to witness the fastest growth from 2025 to 2033, driven by the rising need for minimally invasive procedures to confirm malignancy and guide treatment decisions. Fine-needle aspiration (FNA) and core needle biopsies are increasingly preferred due to their diagnostic reliability and patient comfort. Hospitals and independent laboratories are adopting automated and ultrasound-guided biopsy systems, which improve accuracy and efficiency. The increasing prevalence of suspicious thyroid nodules in the region drives repeated biopsy procedures. In addition, molecular testing often relies on biopsy samples, further supporting growth in this segment.

- By Cancer Type

On the basis of cancer type, the market is segmented into papillary carcinoma, follicular carcinoma, and others. The papillary carcinoma segment dominated the market with a share of 80.01% in 2024, as it is the most prevalent form of thyroid cancer in MEA countries, especially in Saudi Arabia and UAE. Early detection through imaging and biopsy techniques significantly improves treatment outcomes for papillary carcinoma patients. Hospitals and diagnostic centers are focusing on advanced monitoring and molecular profiling to personalize therapy for this type. The high prevalence ensures continuous demand for diagnostic services. Clinical research and awareness campaigns further support adoption of screening programs.

The follicular carcinoma segment is expected to witness the fastest growth from 2025 to 2033 due to increasing identification of cases and the need for precise differentiation from other thyroid malignancies. Molecular diagnostics and biopsy tests are enabling better detection rates. Awareness among clinicians about rare thyroid cancer types is growing, leading to higher diagnostic testing. Expansion of independent diagnostic laboratories is facilitating access to testing for follicular carcinoma. Rising research initiatives in GCC countries also contribute to market growth for this segment.

- By Stages

On the basis of stages, the market is segmented into Stage I, Stage II, Stage III, and Stage IV. The Stage I segment dominated the market in 2024, as early detection through imaging, biopsy, and molecular tests enables improved prognosis and less invasive treatment. Hospitals prioritize early-stage diagnosis to enhance survival rates and reduce treatment costs. Awareness campaigns and routine screening programs support early detection. Stage I patients are more such asly to undergo repeated monitoring, contributing to market revenue. Hospitals in Saudi Arabia and UAE are investing heavily in early detection equipment. The segment is also supported by clinical guidelines recommending early-stage intervention.

The Stage II segment is expected to witness the fastest growth from 2025 to 2033, driven by rising detection of moderately advanced cases and adoption of advanced diagnostic methods to differentiate disease progression. Molecular testing and imaging follow-ups are increasingly used for accurate staging. The growing incidence of thyroid cancer in MEA countries drives the need for early-to-mid stage diagnosis. Expansion of hospital networks and diagnostic centers ensures accessibility of Stage II testing. Technological advancements supporting precise staging are accelerating adoption.

- By Age Group

On the basis of age group, the market is segmented into below 21, 21–29, 30–65, and 65 and above. The 30–65 age group segment dominated the market in 2024, as thyroid cancer prevalence is highest among adults in this age range. This population frequently undergoes routine health check-ups, supporting demand for imaging, biopsy, and molecular diagnostics. Hospitals and diagnostic centers focus on this age group for early screening and follow-up tests. Awareness about thyroid health and early detection drives higher adoption of advanced diagnostic solutions. The segment contributes consistently to consumables and instrument demand due to repeat testing. Increasing corporate health programs and private insurance coverage also enhance adoption.

The 21–29 age group segment is expected to witness the fastest growth from 2025 to 2033 due to rising awareness among young adults about thyroid health, early detection benefits, and increased health screenings. University clinics and private diagnostic centers are increasingly providing targeted testing for this age group. Social media campaigns and government initiatives promote thyroid cancer awareness. Adoption of advanced minimally invasive procedures encourages younger patients to undergo testing. Urban healthcare infrastructure growth supports easier access for this population.

- By End User

On the basis of end user, the market is segmented into hospital, associated labs, independent diagnostic laboratories, diagnostic imaging centers, cancer research institutes, and others. The hospital segment dominated the market in 2024 due to established infrastructure, higher patient footfall, and availability of comprehensive diagnostic services. Hospitals integrate imaging, biopsy, and molecular diagnostics under a single workflow for accurate and timely detection. Investments in advanced equipment and trained personnel support dominance. The segment benefits from repeat testing and follow-ups for thyroid cancer patients. Hospitals in GCC countries are actively upgrading diagnostic capabilities. Collaborative research initiatives also strengthen hospital dominance.

The independent diagnostic laboratories segment is expected to witness the fastest growth from 2025 to 2033, driven by increasing demand for specialized and cost-effective diagnostic services outside hospital settings. These laboratories offer quick access to imaging and molecular tests, appealing to urban populations. Expansion of diagnostic centers in UAE, Saudi Arabia, and North Africa supports this growth. The convenience and shorter turnaround times compared to hospitals attract patients. Collaborations with insurance providers enhance affordability and reach. Increasing investment in lab automation improves efficiency and accuracy.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and retail sales. The direct tender segment dominated the market in 2024, as large hospitals and government healthcare institutions prefer procuring instruments and consumables directly from manufacturers to ensure quality and maintain long-term supply agreements. Bulk procurement ensures cost savings and reliable access to advanced diagnostic equipment. Suppliers also provide installation, maintenance, and training services as part of tenders. Government-led screening programs further support the dominance of direct tenders. Long-term service agreements encourage repeated purchases.

The retail sales segment is expected to witness the fastest growth from 2025 to 2033, driven by rising demand among private clinics, independent diagnostic centers, and smaller hospitals seeking flexible procurement options. Retail channels allow easier access to consumables, kits, and instruments without large-volume contracts. Expansion of medical distributors and e-commerce platforms in the region facilitates retail sales. Private clinics in urban centers increasingly prefer retail purchasing for quick replenishment. Growing awareness of thyroid diagnostics fuels demand through retail channels.

Middle East and Africa Thyroid Cancer Diagnostics Market Regional Analysis

- Saudi Arabia dominated the MEA thyroid cancer diagnostics market with the largest revenue share of 39% in 2024, attributed to higher healthcare spending, advanced medical infrastructure, and rising incidence rates, with major hospitals and diagnostic centers adopting imaging and biopsy diagnostics extensively

- Patients and healthcare providers in the country highly value the accuracy, early detection capabilities, and minimally invasive nature of imaging, biopsy, and molecular testing solutions. Hospitals and diagnostic centers are prioritizing modern instruments and consumables to enhance diagnostic efficiency and patient outcomes

- This widespread adoption is further supported by government health initiatives, growing awareness of thyroid cancer screening, and increasing access to advanced diagnostic centers, establishing Saudi Arabia as the leading market for thyroid cancer diagnostics in the MEA region

The Saudi Arabia Thyroid Cancer Diagnostics Market Insight

The Saudi Arabia thyroid cancer diagnostics market captured the largest revenue share of 39% in 2024 within the MEA region, fueled by rising incidence rates of thyroid cancer and increasing investment in advanced diagnostic technologies. Hospitals and diagnostic centers are prioritizing the adoption of high-resolution imaging, biopsy systems, and molecular testing platforms to improve early detection and patient outcomes. The growing awareness of thyroid health and government-led screening programs further propels the market. Moreover, urban healthcare infrastructure expansion and increasing patient visits are significantly contributing to market growth. The integration of advanced diagnostics with hospital workflows is enhancing efficiency and accessibility for patients.

United Arab Emirates Thyroid Cancer Diagnostics Market Insight

The UAE thyroid cancer diagnostics market is expected to grow at a substantial CAGR during the forecast period, driven by high healthcare spending, advanced medical infrastructure, and rising awareness about early detection. Private hospitals and independent diagnostic laboratories are increasingly adopting imaging, biopsy, and molecular testing solutions. The availability of trained specialists and state-of-the-art laboratories supports high adoption rates. Government initiatives and public health campaigns encouraging routine screening are fostering market expansion. The country’s focus on digital health and integrated diagnostic solutions further enhances accessibility and efficiency. The UAE’s rising prevalence of thyroid nodules and cancers ensures a continuous demand for accurate diagnostic services.

Egypt Thyroid Cancer Diagnostics Market Insight

The Egypt thyroid cancer diagnostics market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing prevalence of thyroid disorders and expanding healthcare infrastructure. Urban hospitals and diagnostic centers are adopting imaging and biopsy technologies to improve detection and monitoring. Rising awareness among patients and clinicians about early detection benefits is encouraging more frequent testing. Government-led health initiatives and insurance coverage support diagnostic adoption. Expansion of independent laboratories and diagnostic imaging centers is also fueling growth. The introduction of cost-effective diagnostic solutions in Egypt is making advanced testing more accessible.

South Africa Thyroid Cancer Diagnostics Market Insight

The South Africa thyroid cancer diagnostics market is expected to expand at a considerable CAGR during the forecast period, fueled by rising thyroid cancer prevalence and increasing adoption of advanced diagnostic technologies. Hospitals and cancer research institutes are integrating high-resolution imaging, biopsy, and molecular testing solutions to enhance early detection and treatment planning. The presence of well-established healthcare infrastructure supports market growth. Increasing patient awareness campaigns and regular health screenings are driving demand. Independent diagnostic laboratories are contributing to higher accessibility of diagnostic tests. The adoption of minimally invasive procedures and molecular assays is improving diagnostic accuracy and efficiency.

Nigeria Thyroid Cancer Diagnostics Market Insight

The Nigeria thyroid cancer diagnostics market is poised to grow at the fastest CAGR during the forecast period, driven by improving healthcare infrastructure, increasing urbanization, and rising awareness about thyroid health. Expansion of hospitals and independent diagnostic laboratories is enabling better access to imaging and biopsy services. Public and private healthcare initiatives promoting early detection are fueling adoption. The market benefits from increased availability of modern instruments and consumables. Training programs for medical staff are enhancing diagnostic accuracy and efficiency. Growing patient demand for minimally invasive and reliable diagnostic tests is accelerating market growth.

Middle East and Africa Thyroid Cancer Diagnostics Market Share

The Middle East and Africa Thyroid Cancer Diagnostics industry is primarily led by well-established companies, including:

- Thyrocare Technologies Limited (India)

- Labcorp (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Siemens Healthineers AG (Germany)

- GE Healthcare (U.K.)

- Koninklijke Philips N.V., (Netherlands)

- Abbott (U.S.)

- Thermo Fisher Scientific, Inc. (U.S.)

- PerkinElmer (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Medtronic (Ireland)

- BD (U.S.)

- Ortho Clinical Diagnostics (U.S.)

- Sysmex Corporation (Japan)

- AbbVie Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- Johnson & Johnson Services, Inc. (U.S.)

What are the Recent Developments in Middle East and Africa Thyroid Cancer Diagnostics Market?

- In June 2025, ImmunityBio, in collaboration with Saudi Arabia's Ministry of Investment, King Faisal Specialist Hospital & Research Centre (KFSHRC), and King Abdullah International Medical Research Center (KAIMRC), announced the introduction of the FDA-approved Cancer BioShield platform in Saudi Arabia. This strategic partnership aims to enhance cancer diagnostics and treatment options in the region

- In April 2025, researchers from the University of Hong Kong and the London School of Hygiene & Tropical Medicine unveiled the world's first artificial intelligence (AI) model designed to classify both the cancer stage and risk category of thyroid cancer. The model achieved an impressive accuracy exceeding 90%, marking a significant advancement in diagnostic technology

- In March 2025, a leading diagnostic center in the UAE expanded its services to include liquid biopsy for thyroid cancer detection. This non-invasive method allows for the detection of genetic alterations in thyroid cancer patients, providing an alternative to traditional tissue biopsies. The expansion reflects the growing demand for less invasive diagnostic options in the region

- In December 2023, a major hospital in Egypt implemented artificial intelligence (AI)-based imaging solutions to assist in the diagnosis of thyroid cancer. These AI tools analyze ultrasound and CT scan images to identify potential malignancies, aiming to reduce diagnostic errors and improve early detection rates

- In February 2021, Kenya revised its national cancer research agenda to strengthen cancer research efforts. The strategy focuses on supporting and adequately resourcing a comprehensive cancer research agenda to inform policy, including the creation of a national cancer research repository for use by all stakeholders

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.