North America Acute Lymphocytic Lymphoblastic Leukemia All Diagnostics Market

Market Size in USD Million

USD

631.39 Million

USD

1,134.49 Million

2024

2032

USD

631.39 Million

USD

1,134.49 Million

2024

2032

| 2025 - 2032 | |

| USD 631.39 Million | |

| USD 1,134.49 Million | |

| % | |

|

North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Size

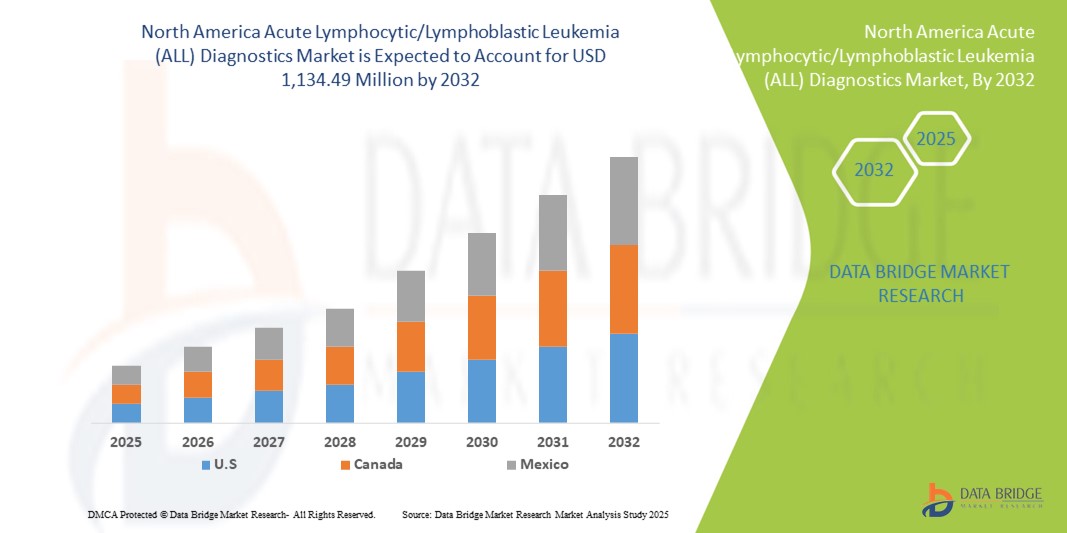

- The North America acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market size was valued at USD 631.39 million in 2024 and is expected to reach USD 1,134.49 million by 2032, at a CAGR of 7.6% during the forecast period

- The market growth is largely fueled by advancements in molecular diagnostics, increasing prevalence of ALL in both pediatric and adult populations, and rising awareness for early detection and personalized treatment approaches

- Furthermore, growing investments by healthcare providers, adoption of innovative diagnostic technologies such as flow cytometry and next-generation sequencing, and supportive government initiatives for cancer diagnostics are establishing North America as a dominant region for ALL diagnostic solutions. These converging factors are accelerating the uptake of ALL diagnostics, thereby significantly boosting the industry's growth

North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Analysis

- ALL diagnostics, encompassing instruments, consumables, imaging tests, biopsies, blood tests, and molecular assays, are increasingly vital components of early detection and treatment planning for both pediatric and adult patients due to their ability to provide accurate, rapid, and personalized diagnostic information

- The escalating demand for ALL diagnostics is primarily fueled by the rising incidence of ALL in North America, growing awareness of early detection benefits, and the adoption of advanced diagnostic technologies across hospitals, independent labs, and cancer research institutes

- U.S. dominated the North America acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market with the largest revenue share of 40.4% in 2024, characterized by advanced healthcare infrastructure, high healthcare expenditure, and a strong presence of leading diagnostic companies, with substantial growth in ALL testing across both B-cell and T-cell lymphoblastic leukemia patients, particularly in pediatric hospitals and specialized oncology centers

- Canada is expected to be the fastest growing country in the North America acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market during the forecast period due to increasing healthcare investments, rising awareness of cancer diagnostics, and adoption of innovative workflows in hospitals, associated labs, and diagnostic imaging centers

- The instruments segment dominated the North America acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market with a share of 57.9% in 2024, driven by the growing need for high-precision equipment to ensure accurate and rapid ALL detection

Report Scope and North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Segmentation

|

Attributes |

North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Trends

Advancements in AI-Driven and High-Precision Diagnostics

- A significant and accelerating trend in the North America ALL diagnostics market is the increasing integration of artificial intelligence (AI) and automated analysis in molecular testing, flow cytometry, and imaging platforms, enhancing diagnostic accuracy and speed

- For instance, AI-enabled software in hematology analyzers can automatically classify lymphoblast subtypes, reducing human error and improving turnaround time for treatment decisions. Similarly, next-generation sequencing platforms provide rapid, high-throughput detection of genetic mutations linked to ALL

- AI integration allows features such as pattern recognition in blood smears and predictive analytics for patient risk stratification, helping clinicians tailor therapies and monitor disease progression. For instance, some Cytognos systems use AI to identify abnormal cell populations and flag unusual patterns for review

- The seamless adoption of AI and automation in diagnostics enables centralized laboratory management and real-time reporting, improving workflow efficiency and supporting integrated care in hospitals and cancer research institutes

- This trend towards intelligent, automated, and high-precision diagnostic systems is fundamentally reshaping clinical expectations for ALL testing. Consequently, companies such as Abbott Laboratories and BD Diagnostics are developing AI-enabled platforms with automated classification, reporting, and predictive analytics

- The demand for ALL diagnostics that offer AI-driven accuracy and automation is growing rapidly across both hospitals and specialized oncology labs, as clinicians increasingly prioritize timely and precise diagnostic insights

North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Dynamics

Driver

Rising ALL Incidence and Adoption of Advanced Diagnostic Technologies

- The increasing prevalence of ALL among pediatric and adult populations, coupled with growing adoption of molecular and high-throughput diagnostic technologies, is a significant driver for heightened demand in North America

- For instance, in March 2024, BD Biosciences reported the launch of an automated flow cytometry panel for ALL, demonstrating how AI-enabled instrumentation can accelerate early detection and improve patient management

- As clinicians and hospitals become more aware of the importance of early diagnosis and personalized treatment, advanced diagnostics such as NGS and automated cytometry provide a compelling upgrade over traditional blood and biopsy analyses

- Furthermore, expanding cancer research centers and specialized pediatric oncology units are driving demand for sophisticated diagnostic solutions capable of supporting complex treatment protocols

- The ability to quickly process large volumes of patient samples, track disease progression, and generate actionable reports enhances adoption across hospitals, labs, and research institutes, ensuring widespread market growth

Restraint/Challenge

High Diagnostic Costs and Regulatory Compliance Hurdles

- Concerns surrounding the high cost of advanced ALL diagnostics and stringent regulatory requirements pose significant challenges to broader market penetration in North America

- For instance, expensive NGS platforms and automated flow cytometers require substantial capital investment, which may limit adoption in smaller hospitals or diagnostic centers

- Ensuring compliance with FDA regulations, CLIA certification, and quality standards is essential, as failure to meet these requirements can delay product approvals and market entry

- In addition, the complexity of advanced diagnostic workflows and the need for trained personnel to operate sophisticated equipment can create operational barriers for laboratories and research institutes

- Rising helium shortage and rising risk of excessive radiation exposure are projected to restrict the use of CT scanners, threatening the possibilities of rising capital investments and low benefit-cost ratio for biomarkers

- Many hospitals in developing countries cannot invest in diagnostic imaging equipment, which has led to an increase in the use of reconstructed diagnostic imaging due to high expenditures and financial restrictions

- Overcoming these challenges through cost optimization, regulatory support, and staff training programs will be vital for sustained growth of the North America ALL diagnostics market.

North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Scope

The market is segmented on the basis of product type, test type, cancer type, age group, gender, end user, and distribution channel.

- By Product Type

On the basis of product type, the acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into instruments and consumables & accessories. The Instruments segment dominated the market with the largest revenue share of 57.9% in 2024, driven by the growing demand for high-precision diagnostic equipment in hospitals and specialized oncology labs. Instruments such as automated flow cytometers, hematology analyzers, and next-generation sequencing platforms enable accurate classification and rapid detection of lymphoblastic leukemia. Hospitals and research institutes prioritize instruments for their reliability, consistency, and ability to process large volumes of patient samples efficiently. The segment benefits from continuous technological advancements and AI integration, enhancing diagnostic accuracy and workflow efficiency. Increasing government funding and high adoption of precision diagnostics in North America further support the dominance of instruments in ALL diagnostics.

The consumables & accessories segment is anticipated to witness the fastest growth at a CAGR of 7.2% from 2025 to 2032, driven by the recurring need for reagents, kits, and sample processing materials in molecular and cytogenetic testing. Consumables are critical for supporting the functionality of diagnostic instruments and ensuring standardized, accurate test results. Rising incidence of ALL and expansion of outpatient and diagnostic labs are boosting demand. In addition, specialized pediatric and adult leukemia kits are gaining traction. Continuous product innovation, increasing partnerships with hospitals, and expansion of diagnostic centers contribute to rapid growth in this segment.

- By Test Type

On the basis of test type, the acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into imaging test, biopsy, blood test, and others. The Blood Test segment dominated the market with the largest revenue share of 48.6% in 2024, owing to its critical role in early detection and routine monitoring of ALL patients. Blood tests provide rapid and minimally invasive diagnostic insights, allowing clinicians to identify abnormal lymphoblast counts efficiently. Automated hematology analyzers and flow cytometry systems further enhance precision. Blood testing is widely adopted in hospitals, associated labs, and outpatient diagnostic centers due to accessibility, cost-effectiveness, and speed. Increasing awareness among healthcare providers and early intervention initiatives contribute to dominance. Advanced blood test panels for pediatric and adult patients further reinforce this segment’s leadership.

The biopsy segment is expected to witness the fastest growth with a CAGR of 8.1% during 2025–2032, driven by its ability to provide detailed morphological and genetic information for precise ALL classification. Biopsies are critical for identifying subtypes such as B-cell and T-cell lymphoblastic leukemia and planning targeted therapies. Innovations in minimally invasive biopsy procedures enhance patient compliance and adoption. Integration with molecular diagnostics boosts efficiency and accuracy. Expanding research activities and clinical trials further accelerate demand. Growth is particularly notable in specialized oncology centers and pediatric hospitals.

- By Cancer Type

On the basis of cancer type, the acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into B-cell Lymphoblastic Leukemia/Lymphoma and T-cell Lymphoblastic Leukemia. The B-cell Lymphoblastic Leukemia/Lymphoma segment dominated the market with the largest share of 61.3% in 2024, owing to its higher prevalence among pediatric and adult patients. Accurate and early diagnosis is critical for effective chemotherapy and immunotherapy management. Hospitals and oncology centers prefer comprehensive B-cell diagnostic panels. Rising awareness programs and government screening initiatives support market dominance. Molecular and flow cytometry-based diagnostics are widely used in this segment. High research focus and technological advancements further strengthen its position.

The T-cell Lymphoblastic Leukemia segment is expected to witness the fastest growth at a CAGR of 7.9% from 2025 to 2032, driven by increasing awareness of its aggressive nature and the need for early detection. Targeted diagnostics and subtype-specific assays are boosting adoption. Pediatric T-cell ALL cases are increasing, requiring timely interventions. Specialized labs and oncology centers are adopting advanced instruments and kits. Integration with AI-driven diagnostic tools further supports growth. Expansion of testing programs across North America is contributing to rapid uptake in this segment.

- By Age Group

On the basis of age group, the acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into Below 21, 21–29, 30–65, and 65 and Above. The Below 21 segment dominated the market with a share of 44.5% in 2024, as ALL is most prevalent in pediatric patients. Hospitals, pediatric oncology centers, and research institutes prioritize diagnostic testing for early intervention. Blood tests, molecular assays, and flow cytometry panels are widely used. Government funding and awareness campaigns focused on childhood leukemia support market dominance. Advanced testing kits for pediatric patients enhance accuracy and reduce procedural risk. Adoption is growing in both urban and rural healthcare facilities.

The 30–65 age group is expected to witness the fastest growth at a CAGR of 6.8% from 2025 to 2032, due to rising ALL incidence among adults and routine monitoring requirements. Specialized oncology centers and diagnostic labs are increasing adoption of molecular and automated diagnostic instruments. Awareness programs and clinical guidelines for adult leukemia drive demand. Advanced technologies enable precise detection of disease progression. Hospitals and associated labs are expanding adult leukemia testing capacity. Continuous introduction of innovative diagnostic tools supports growth.

- By Gender

On the basis of gender, the acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into male and female. The Male segment dominated the market with a share of 52.1% in 2024, attributed to a slightly higher reported prevalence in North America. Hospitals and research institutes use specialized diagnostic panels targeting male-specific leukemia profiles. Blood tests, flow cytometry, and molecular assays are widely used. Male patient dominance also drives demand for pediatric and adult diagnostic services. Awareness campaigns and early detection initiatives support this segment. Adoption in both hospitals and outpatient labs reinforces its leadership.

The female segment is anticipated to witness the fastest growth at a CAGR of 6.5% from 2025 to 2032, fueled by increasing early screening and awareness programs. Outpatient centers, research programs, and hospitals are expanding access. Advanced diagnostic instruments and consumables are increasingly used for female patients. Targeted leukemia panels and molecular assays contribute to growth. Expansion of testing networks in North America supports adoption. Government and private programs are encouraging proactive female leukemia diagnostics.

- By End User

On the basis of end user, the market is segmented into hospitals, associated labs, independent diagnostic laboratories, diagnostic imaging centers, cancer research institutes, and others. The Hospitals segment dominated the market with a share of 60.7% in 2024, driven by centralized testing facilities and access to advanced instruments. Hospitals perform routine blood tests, biopsies, and molecular analyses for early detection and treatment guidance. Pediatric and adult oncology centers prioritize hospitals for comprehensive diagnostic workflows. Hospital adoption is reinforced by availability of specialized personnel and infrastructure. Government funding and research initiatives further support dominance. Hospitals remain the preferred choice for complex ALL diagnostics.

The Independent Diagnostic Laboratories segment is expected to witness the fastest growth at a CAGR of 7.3% from 2025 to 2032, driven by outsourcing of specialized tests from hospitals and research centers. Expansion of outpatient diagnostic facilities and collaborations with hospitals boost adoption. Advanced instruments and consumables are increasingly used in labs. Targeted testing services for pediatric and adult patients support growth. Labs benefit from technological integration and workflow automation. Rising demand for rapid and precise diagnostics accelerates segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and retail sales. The Direct Tender segment dominated the market with a share of 58.2% in 2024, as hospitals and research institutes procure instruments, consumables, and kits directly from manufacturers. Bulk purchases ensure cost efficiency and steady supply of essential diagnostic materials. Direct tender enables faster installation, maintenance, and staff training. Hospitals prefer manufacturer support and warranties for advanced diagnostic equipment. Centralized procurement by healthcare institutions reinforces dominance. Government and private funding programs further promote this channel.

The Retail Sales segment is anticipated to witness the fastest growth at a CAGR of 7.0% from 2025 to 2032, fueled by increasing availability of diagnostic kits, reagents, and instruments through distributors and online channels. Retail caters to smaller labs, outpatient centers, and associated labs. Convenience, accessibility, and faster replenishment drive adoption. Growth is supported by increased awareness among healthcare providers and expansion of testing networks. Technological support from manufacturers ensures reliability. Rapid uptake of consumables and instruments accelerates segment expansion.

North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Regional Analysis

- U.S. dominated the North America acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market with the largest revenue share of 40.4% in 2024, characterized by advanced healthcare infrastructure, high healthcare expenditure, and a strong presence of leading diagnostic companies

- Healthcare providers in the region highly value rapid, accurate, and personalized diagnostics through instruments such as automated flow cytometers, molecular testing platforms, and next-generation sequencing, enabling early detection and effective treatment planning

- This widespread adoption is further supported by high healthcare expenditure, strong government initiatives for cancer screening, and the presence of leading diagnostic companies. The growing number of specialized pediatric and adult oncology centers, along with the rising demand for centralized laboratory testing, establishes ALL diagnostics as a preferred solution for both clinical and research applications

The U.S. ALL Diagnostics Market Insight

The U.S. acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market captured the largest revenue share in 2024 within North America, fueled by the growing prevalence of ALL and the widespread adoption of advanced diagnostic technologies. Hospitals and specialized oncology centers are increasingly prioritizing high-precision instruments, such as automated flow cytometers and next-generation sequencing platforms, for early detection and treatment planning. The growing integration of AI-based diagnostic tools and automated analysis is enhancing accuracy and efficiency. In addition, increasing awareness among healthcare providers and caregivers about early intervention benefits is driving adoption. The U.S. market is further supported by government funding, research initiatives, and strong private sector investments in cancer diagnostics.

Canada ALL Diagnostics Market Insight

The Canada acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is projected to grow at a substantial CAGR during the forecast period, primarily driven by increasing healthcare investments and rising awareness of early leukemia detection. Hospitals, associated labs, and diagnostic centers are expanding their capabilities for pediatric and adult ALL testing. The adoption of molecular assays, flow cytometry, and high-throughput screening is facilitating rapid and accurate diagnosis. Moreover, government initiatives for cancer screening and improved healthcare accessibility are promoting adoption. The market is witnessing growth across urban hospitals, research institutes, and outpatient diagnostic centers, with a focus on comprehensive and timely testing.

Mexico ALL Diagnostics Market Insight

The Mexico acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing investments in healthcare infrastructure and rising demand for early cancer detection. Hospitals and independent diagnostic laboratories are upgrading to modern instruments and consumables for reliable ALL diagnostics. Increasing awareness of pediatric leukemia and adult ALL, along with supportive government health programs, is encouraging adoption. Expansion of regional diagnostic centers and training of skilled personnel are further boosting the market. Mexico’s growing focus on preventive healthcare and integration of advanced diagnostic platforms enhances accessibility and reliability.

North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Share

The North America acute lymphocytic/lymphoblastic leukemia (all) diagnostics industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- Abbott (U.S.)

- Danaher (U.S.)

- Siemens (Germany)

- BD (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Sysmex Corporation (Japan)

- Labcorp (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- PerkinElmer (U.S.)

- Hologic, Inc. (U.S.)

- Ortho Clinical Diagnostics, Inc. (U.S.)

- BIOMÉRIEUX. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- GE Healthcare (U.K.)

- Koninklijke Philips N.V., (Netherlands)

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Lilly USA, LLC (U.S.)

What are the Recent Developments in North America Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market?

- In August 2025, researchers developed a deep learning model for early diagnosis of acute lymphoblastic leukemia (ALL), utilizing microscopic blood smear images. This AI-based approach aims to enhance diagnostic accuracy and speed, facilitating timely treatment interventions

- In February 2025, the National Cancer Institute (NCI) announced that blinatumomab (Blincyto) is now expected to become part of the standard initial treatment for many children with acute lymphoblastic leukemia (ALL), following positive results from a large clinical trial

- In January 2025, Seattle Children's Hospital reported a breakthrough in B-cell acute lymphoblastic leukemia (B-ALL) treatment, with a study showing that blinatumomab significantly improved treatment outcomes. The results indicate a potential shift in therapeutic strategies for B-ALL

- In November 2024, the U.S. Food and Drug Administration (FDA) approved Obecabtagene Autoleucel (Aucatzyl), a CD19-directed genetically modified autologous T cell immunotherapy, for adults with relapsed or refractory B-cell precursor acute lymphoblastic leukemia (ALL). This approval marks a significant advancement in personalized immunotherapy for ALL patients

- In October 2024, researchers at Dana-Farber Cancer Institute developed a CRISPR-based rapid molecular diagnostic tool capable of detecting gene fusions in acute promyelocytic leukemia (APL) and chronic myeloid leukemia (CML). This innovation aims to expedite diagnosis and treatment decisions, potentially saving lives

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.