North America Cholesterol Testing Market

Market Size in USD Billion

USD

2.69 Billion

USD

4.90 Billion

2025

2033

USD

2.69 Billion

USD

4.90 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.69 Billion | |

| USD 4.90 Billion | |

| % | |

|

North America Cholesterol Testing Market Size

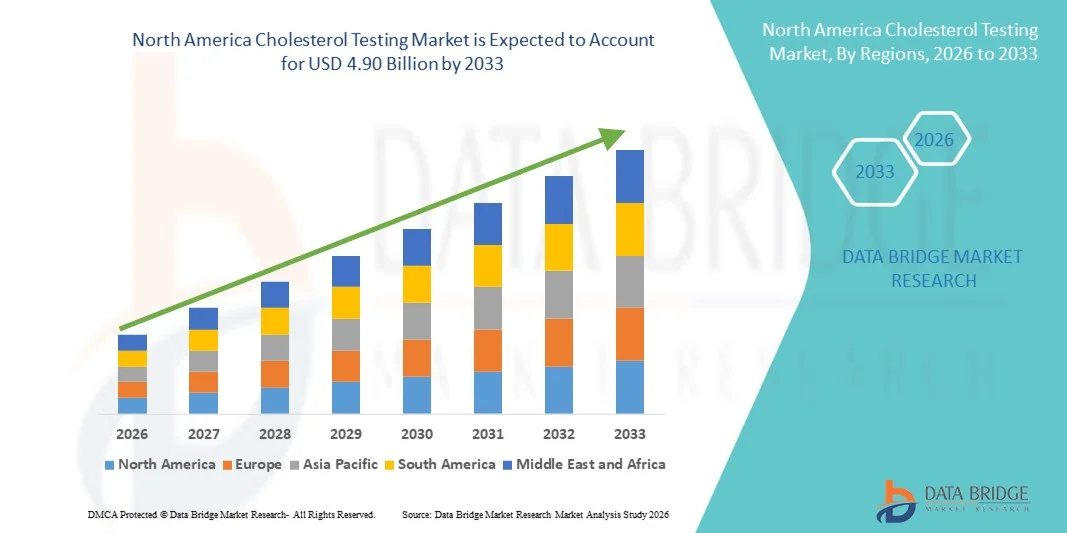

- The North America cholesterol testing market size was valued at USD 2.69 billion in 2025 and is expected to reach USD 4.90 billion by 2033, at a CAGR of 7.81% during the forecast period

- The market growth is largely fueled by rising awareness of cardiovascular health risks, increased preventive healthcare screening, and growing adoption of advanced cholesterol testing products and services across clinical and home care settings

- Furthermore, strong healthcare infrastructure in the United States and Canada, supportive public health initiatives promoting regular lipid monitoring, and technological innovation in test kits and diagnostic devices are driving demand for accurate, accessible cholesterol testing solutions. These converging factors are accelerating market uptake and significantly boosting industry growth throughout the forecast period

North America Cholesterol Testing Market Analysis

- Cholesterol testing, encompassing blood lipid analysis for total cholesterol, LDL, HDL, and triglycerides, is becoming an essential component of preventive healthcare and cardiovascular risk management in both clinical and home care settings due to its accuracy, convenience, and growing availability of point-of-care and at-home testing solutions

- The rising demand for cholesterol testing is primarily driven by increasing awareness of cardiovascular diseases, preventive health initiatives, and a growing trend toward regular health monitoring among individuals seeking early detection and management of high cholesterol levels

- The United States dominated the North America cholesterol testing market with the largest revenue share of 78.2% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and widespread adoption of preventive health screenings, with significant growth in both clinical and at-home cholesterol testing driven by innovations in rapid diagnostic kits and digital health platforms

- Canada is expected to be the fastest-growing country in North America cholesterol testing market during the forecast period due to increasing healthcare access, rising awareness of cardiovascular health, and improving affordability of diagnostic tests

- The Test Kits segment dominated the cholesterol testing market with a market share of 45.9% in 2025, driven by their ease of use, rapid results, and growing adoption in both clinical laboratories and home testing applications

Report Scope and North America Cholesterol Testing Market Segmentation

|

Attributes |

North America Cholesterol Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Cholesterol Testing Market Trends

Advanced Testing Convenience Through Digital and Home Integration

- A significant and accelerating trend in the North America cholesterol testing market is the increasing adoption of digital and at-home testing solutions, allowing patients and clinicians to monitor lipid levels more conveniently and efficiently. This integration is enhancing preventive healthcare management and patient compliance

- For instance, home-use lipid test kits such as CardioCheck and Everlywell allow users to collect samples at home and obtain results via smartphone applications, reducing the need for frequent clinic visits

- Digital integration in cholesterol testing enables features such as automatic result logging, personalized health insights, and trend tracking over time. For instance, some Lumen Health platforms provide reminders for testing schedules and generate insights on lifestyle impact based on repeated measurements

- The seamless integration of cholesterol testing devices with mobile health platforms and electronic health records facilitates centralized monitoring by healthcare providers. Through a single interface, clinicians can track patient lipid profiles alongside other vital health parameters, improving preventive care and treatment outcomes

- This trend towards more accessible, connected, and user-friendly cholesterol testing solutions is reshaping patient expectations for preventive health. Consequently, companies such as Abbott Laboratories are developing digital-enabled cholesterol tests that provide instant results and integration with smartphone applications for tracking and alerts

- The demand for cholesterol testing solutions with digital and home-use integration is growing rapidly across both residential and clinical sectors, as consumers and healthcare providers increasingly prioritize convenience, accuracy, and proactive health management

- Advances in AI-driven predictive analytics are enabling cholesterol tests to offer personalized risk assessments, helping users and clinicians make better-informed lifestyle or treatment decisions

North America Cholesterol Testing Market Dynamics

Driver

Growing Need Due to Rising Cardiovascular Awareness and Preventive Health Initiatives

- The increasing prevalence of cardiovascular diseases, coupled with growing preventive healthcare awareness, is a significant driver for the heightened demand for cholesterol testing

- For instance, in March 2025, Abbott Laboratories launched an advanced point-of-care cholesterol test with rapid results to improve early detection and patient management. Such strategies by key companies are expected to drive market growth during the forecast period

- As consumers become more conscious of heart health risks and seek early detection, cholesterol testing offers quick and reliable assessment of lipid profiles, providing a compelling case for regular monitoring

- Furthermore, government and healthcare initiatives promoting routine screenings and preventive care are making cholesterol testing an essential component of wellness programs, increasing its adoption in clinics and at home

- The convenience of at-home testing, smartphone-enabled result tracking, and integration with healthcare management apps are key factors propelling the adoption of cholesterol tests in both clinical and residential sectors. The trend towards digital health and remote patient monitoring further contributes to market growth

- Rising health insurance coverage for preventive testing in the United States and Canada is reducing out-of-pocket costs, encouraging more individuals to undertake regular cholesterol checks

- Increasing awareness campaigns by healthcare organizations about cholesterol management and cardiovascular disease prevention are boosting testing frequency among high-risk populations

Restraint/Challenge

Accuracy Concerns and Regulatory Compliance Hurdles

- Concerns surrounding the accuracy and reliability of some home-use or point-of-care cholesterol tests pose a challenge to broader market adoption. Variations in results compared to laboratory testing can make some consumers and healthcare providers hesitant

- For instance, reports of discrepancies in results from certain rapid test kits have made some users prefer clinical laboratory testing over at-home devices

- Addressing these accuracy concerns through rigorous validation, regulatory approvals, and quality certification is crucial for building consumer trust. Companies such as Roche and Abbott emphasize standardized testing protocols and FDA-clearance to reassure users

- While costs are gradually decreasing, perceived complexity or premium pricing can still hinder adoption, especially among individuals who do not perceive an immediate need for frequent cholesterol monitoring

- Overcoming these challenges through enhanced test accuracy, clear regulatory compliance, consumer education, and development of cost-effective testing solutions will be vital for sustained market growth

- Lack of standardization among home-use testing kits and varying sensitivity levels across brands may limit clinician trust and slow adoption in clinical settings

- Data privacy and security concerns regarding digital integration of test results with mobile apps or cloud platforms can create hesitancy among consumers, particularly in older demographics

North America Cholesterol Testing Market Scope

The market is segmented on the basis of product type, test, test type, prescription mode, and end-users

- By Product Type

On the basis of product type, the North America cholesterol testing market is segmented into test kits and testing strips. The Test Kits segment dominated the market with the largest revenue share of 45.9% in 2025. This dominance is driven by their comprehensive testing capabilities, ease of use in both clinical and home settings, and the ability to provide rapid and reliable results. Consumers and clinics prefer test kits for their versatility in assessing multiple lipid parameters at once, making them ideal for preventive healthcare and routine screenings. Test kits often come with user-friendly digital interfaces that enable patients to track results and integrate them with mobile health applications, increasing their adoption. Leading companies such as Abbott and Roche continue to innovate in test kit designs to improve accuracy and user experience.

The Testing Strips segment is expected to witness the fastest growth at a CAGR of 9% from 2026 to 2033, fueled by their affordability, portability, and suitability for frequent at-home monitoring. Testing strips are increasingly adopted in homecare and telehealth settings due to their minimal requirement for equipment and ease of integration with digital readers. Their compact form factor allows for convenient storage and single-use testing, appealing to both patients and healthcare providers. The growth is further accelerated by rising consumer awareness about proactive cholesterol management and lifestyle monitoring.

- By Test

On the basis of test, the market is segmented into Total Cholesterol Test, High-Density Lipoprotein (HDL) Cholesterol, and Low-Density Lipoprotein (LDL) Cholesterol tests. The Total Cholesterol Test segment dominated in 2025 due to its broad clinical applicability, being a standard measure in lipid profiling and cardiovascular risk assessment. Total cholesterol testing is often the first line of screening, widely recommended in clinics, hospitals, and preventive health programs. It is valued for providing a quick snapshot of a patient’s lipid status, which guides further detailed testing if required. The test is supported by both laboratory and at-home test kits, making it widely accessible across North America. High reliability, regulatory approvals, and integration with electronic health records further support its dominance.

The LDL Cholesterol segment is expected to grow fastest during 2026–2033, driven by increasing focus on “bad cholesterol” management and rising awareness of its link to cardiovascular diseases. LDL testing is critical for risk stratification, treatment monitoring, and preventive healthcare initiatives, making it increasingly demanded in clinics, hospitals, and homecare settings. Innovative test kits now provide LDL-specific results rapidly, supporting patient engagement and proactive intervention. The growth is further supported by physician recommendations and insurance coverage for LDL monitoring.

- By Test Type

On the basis of test type, the market is segmented into Non-Invasive and Invasive tests. The Invasive segment dominated the market in 2025, as traditional blood sampling and laboratory-based cholesterol testing remain the gold standard for clinical accuracy. Invasive tests are widely used in hospitals, diagnostic centers, and clinics, ensuring high sensitivity and reliability. Their adoption is supported by advanced laboratory infrastructure, clinician trust, and regulatory compliance. The accuracy and comprehensive reporting of invasive tests make them essential in both preventive and therapeutic healthcare settings.

The Non-Invasive segment is expected to witness the fastest growth during 2026–2033 due to technological advancements in biosensors, wearable devices, and fingertip testing solutions. Non-invasive tests appeal to patients who prefer painless, convenient, and rapid monitoring. Increasing adoption in homecare and telehealth, combined with AI-assisted analytics for predictive insights, is driving this segment’s growth. Growing consumer preference for self-monitoring and preventive health management is also boosting adoption of non-invasive methods.

- By Prescription Mode

On the basis of prescription mode, the market is segmented into Over-The-Counter (OTC) and Prescription-Based cholesterol tests. The Prescription-Based segment dominated the market in 2025, driven by clinical reliance on physician-guided testing for accurate diagnosis, monitoring, and treatment decisions. Prescription-based tests are commonly used in hospitals and diagnostic centers, ensuring adherence to healthcare protocols. Their dominance is also supported by insurance reimbursement policies and integration with patient health records. Clinicians prefer these tests for comprehensive lipid analysis, reliability, and regulatory compliance.

The Over-The-Counter segment is expected to grow fastest during 2026–2033 due to rising consumer interest in home testing solutions and digital health monitoring. OTC tests allow patients to conduct cholesterol assessments independently, often integrating with mobile applications to track results and provide lifestyle guidance. Growing awareness about cardiovascular health and proactive self-care are fueling the adoption of OTC tests. Continuous innovation in user-friendly design and affordability further accelerates growth in this segment.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, ambulatory centers, homecare, and diagnostic centers. The Hospitals segment dominated in 2025, holding the largest revenue share due to the concentration of advanced testing infrastructure, trained medical personnel, and high patient footfall. Hospitals provide comprehensive lipid profiling and follow-up services, making them the primary users of cholesterol testing products. The dominance is also attributed to regular screening programs and chronic disease management initiatives conducted in hospital settings.

The Homecare segment is expected to witness the fastest growth during 2026–2033, driven by increasing adoption of at-home test kits, digital health platforms, and telehealth consultations. Rising consumer preference for convenient, self-administered testing, combined with growing awareness of preventive healthcare, is accelerating demand. The COVID-19 pandemic further boosted homecare adoption by promoting remote monitoring. Integration with mobile apps, cloud-based tracking, and AI analytics enhances the usability of homecare testing, contributing to faster market growth.

North America Cholesterol Testing Market Regional Analysis

- The United States dominated the North America cholesterol testing market with the largest revenue share of 78.2% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and widespread adoption of preventive health screenings, with significant growth in both clinical and at-home cholesterol testing driven by innovations in rapid diagnostic kits and digital health platforms

- Consumers and healthcare providers in the region highly value the accuracy, convenience, and rapid results offered by modern cholesterol testing products, including both point-of-care kits and at-home testing solutions

- This widespread adoption is further supported by advanced healthcare infrastructure, high healthcare expenditure, and growing integration of digital health platforms, establishing cholesterol testing as an essential tool for routine health monitoring in both clinical and homecare settings

U.S. Cholesterol Testing Market Insight

The U.S. cholesterol testing market captured the largest revenue share of 78.2% in 2025 within North America, driven by widespread awareness of cardiovascular diseases and the growing adoption of preventive healthcare practices. Consumers and healthcare providers increasingly prioritize accurate and convenient cholesterol monitoring through clinical, point-of-care, and at-home test solutions. The rising trend of digital health integration, including mobile app-based result tracking and telehealth consultations, is further propelling market growth. In addition, government initiatives promoting routine lipid screenings and insurance coverage for preventive testing are significantly contributing to the expansion of the U.S. market.

Canada Cholesterol Testing Market Insight

The Canada cholesterol testing market is expected to grow at a robust CAGR during the forecast period, driven by increasing preventive healthcare awareness and the rising prevalence of cardiovascular conditions. The adoption of at-home testing kits, combined with telehealth integration, is facilitating easier monitoring and early detection. Canadians are showing strong preference for quick, reliable, and user-friendly test solutions, supported by advanced healthcare infrastructure and government health campaigns promoting regular screenings. The market is also benefiting from collaborations between diagnostic companies and digital health platforms for remote monitoring.

Mexico Cholesterol Testing Market Insight

The Mexico cholesterol testing market is projected to grow steadily due to rising awareness of cardiovascular diseases and improving healthcare access. Adoption of point-of-care and home-use test kits is increasing as consumers seek convenient and rapid testing options. Government initiatives aimed at preventive health and chronic disease management are supporting market growth. Affordability and increasing availability of testing solutions, coupled with partnerships between local diagnostic centers and global manufacturers, are further boosting adoption across urban and semi-urban areas.

North America Cholesterol Testing Market Share

The North America Cholesterol Testing industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Siemens Healthineers AG (Germany)

- Beckman Coulter, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Randox Laboratories Ltd. (U.K.)

- PerkinElmer, Inc. (U.S.)

- Eurofins Scientific (Luxembourg)

- DiaSorin S.p.A. (Italy)

- PTS Diagnostics (U.S.)

- ACON Laboratories, Inc. (U.S.)

- Nova Biomedical (U.S.)

- Labcorp (U.S.)

- Sekisui Diagnostics LLC (U.S.)

- Trinity Biotech plc (Ireland)

- Ortho Clinical Diagnostics (U.S.)

- Cell Biolabs, Inc. (U.S.)

- Clinical Reference Laboratory, Inc. (U.S.)

- BioReference Health, LLC (U.S.)

What are the Recent Developments in North America Cholesterol Testing Market?

- In January 2025, Roche Diagnostics announced that the Tina‑quant® Lipoprotein (a) Gen.2 Molarity assay received 510(k) clearance from the U.S. Food and Drug Administration (FDA) the first FDA‑cleared test of its kind in the U.S. to measure lipoprotein (a) (Lp(a)) in nanomoles per liter, improving cardiovascular risk assessment accuracy. This test enables clinicians to more precisely stratify risk beyond traditional cholesterol metrics, representing a meaningful advance in preventive cardiology diagnostics

- In January 2025, Quest Diagnostics reported expanding its consumer‑initiated testing platform to include high‑risk Lipoprotein(a) cholesterol testing, along with other diagnostic tests, enhancing direct access for consumers who want to monitor cholesterol and other biomarkers without a physician order. This reflects the trend toward direct‑to‑consumer lab services and broader awareness of advanced cholesterol‑related risk factors

- In September 2024, the Family Heart Foundation launched “Cholesterol Connect®,” a free at‑home cholesterol screening and personalized support program to help address cardiovascular disease risk by offering at‑home lipid testing kits and live guidance from care navigators. This initiative provides standard lipid panel test kits that measure total cholesterol, LDL, HDL, triglycerides, and lipoprotein(a), empowering individuals to better understand and manage their heart health without requiring insurance

- In August 2024, Amgen expanded its no‑cost LDL‑C cholesterol testing program across approximately 1,000 MinuteClinic locations in the United States, making free LDL cholesterol tests available to individuals at select CVS Pharmacy clinics nationwide. This expansion aimed to improve access to preventive cardiovascular screening and help address disparities in heart health testing

- In May 2024, Roche’s Tina‑quant® Lp(a) RxDx assay received FDA Breakthrough Device Designation for identifying patients who may benefit from emerging Lp(a)‑lowering therapies. Although not yet fully cleared for commercialization, this designation acknowledges the clinical importance of Lp(a) as a cardiovascular risk biomarker and accelerates regulatory review pathways

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.