North America Trauma Fixation Market

Market Size in USD Billion

USD

5.65 Billion

USD

12.38 Billion

2024

2032

USD

5.65 Billion

USD

12.38 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.65 Billion | |

| USD 12.38 Billion | |

| % | |

|

North America Trauma Fixation Market Size

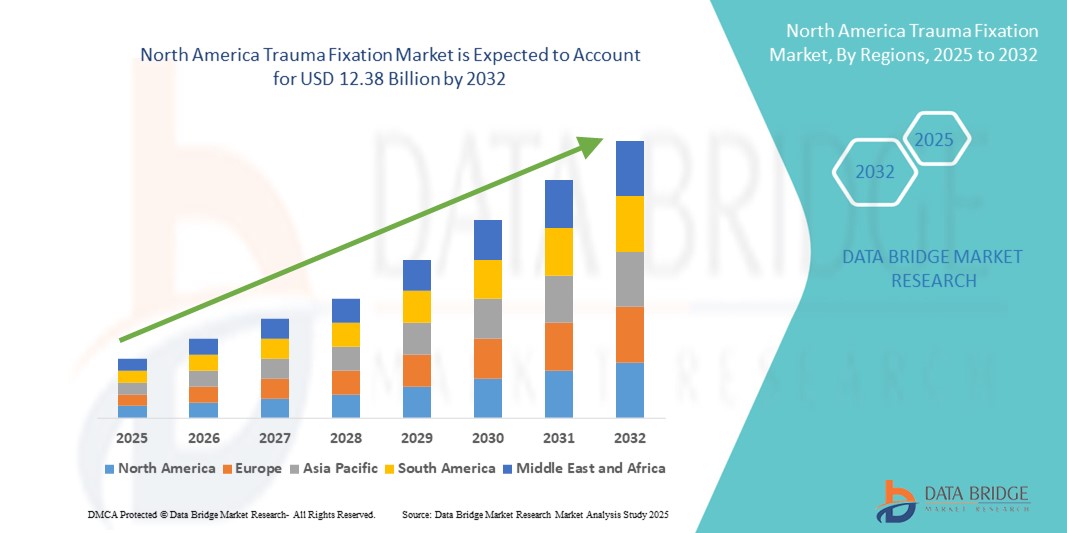

- The North America trauma fixation market size was valued at USD 5.65 billion in 2024 and is expected to reach USD 12.38 billion by 2032, at a CAGR of 10.3% during the forecast period

- The market growth is largely fueled by the rising incidence of trauma from road accidents, falls, and sports-related injuries—a trend intensified by urbanization, increasing vehicle usage, and an aging population. These factors are boosting demand for effective trauma fixation devices that stabilize fractures and support recovery

- Furthermore, technological innovation plays a crucial role—advancements such as minimally invasive surgical techniques, bioabsorbable materials in internal fixators, 3D-printed customized implants, and smart device coatings are enhancing device effectiveness, reducing recovery time, and improving patient outcomes

North America Trauma Fixation Market Analysis

- Trauma Fixation devices are witnessing robust adoption across North America, driven by rising incidence of traumatic injuries, growing geriatric population, and increasing orthopedic surgeries. In 2024, North America accounted for approximately 41.5% of the global Trauma Fixation market revenue, supported by advanced healthcare infrastructure, high awareness of innovative fixation techniques, and strong reimbursement frameworks across the region

- The increasing prevalence of road accidents, sports injuries, and age-related bone disorders is fueling demand for reliable internal and external fixation devices. Hospitals, trauma centers, and ambulatory surgical centers in North America are actively investing in trauma fixation solutions to improve patient outcomes, reduce recovery time, and minimize complications. The hospitals segment contributed around 72.3% of total Trauma Fixation market revenue in North America in 2024, reflecting the concentration of complex trauma care in hospital settings

- U.S. dominated the North America trauma fixation market, accounting for the largest revenue share of 85.4% in 2024. This is attributed to the country's well-established orthopedic surgery infrastructure, ongoing technological advancements in fixation devices, and the presence of key market players headquartered in the U.S. Continuous investments in trauma care research and rising insurance coverage further bolster the market dominance

- Canada is projected to be the fastest-growing country in the North America trauma fixation market, with an estimated CAGR of 10.9% from 2025 to 2032. Growth in Canada is driven by increasing government healthcare spending, expansion of trauma care facilities, and greater adoption of minimally invasive fixation techniques in orthopedic surgery. The growing geriatric population and rising awareness of advanced fixation options in rural areas also support this trend

- The internal fixator devices segment dominated the North America trauma fixation market with 61.4% of the market revenue share in 2024, driven by their ability to provide stable fixation, enable early mobilization, and reduce recovery times for patients with complex fractures

Report Scope and North America Trauma Fixation Market Segmentation

|

Attributes |

North America Trauma Fixation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Trauma Fixation Market Trends

Rise of Minimally Invasive and Patient-Centric Trauma Fixation Techniques

- A significant and accelerating trend in the North America trauma fixation market is the growing shift toward minimally invasive surgical (MIS) procedures. These approaches—such as percutaneous fixation, intramedullary nailing, and advanced plating systems—are being increasingly adopted because they reduce tissue trauma, lower infection risks, and significantly shorten patient recovery times, enabling faster discharge and improved clinical outcomes

- For instance, DePuy Synthes offers the VA LCP Periprosthetic Plating System, designed for MIS application, which minimizes surgical exposure while maintaining rigid fixation for complex fractures. Similarly, Smith+Nephew’s TRIGEN INTERTAN Intertrochanteric Nail allows fracture stabilization through smaller incisions, leading to less blood loss and quicker mobilization

- Hybrid fixation systems—combining elements of internal and external fixation—are also gaining traction as they provide customized stabilization strategies for complex fractures. For example, Orthofix’s Galaxy Fixation Gemini enables surgeons to transition from external to internal fixation without completely removing stabilization, allowing adaptability to patient-specific needs

- Another major advancement is the rise of patient-specific implants, produced through high-resolution imaging and additive manufacturing (3D printing). For instance, Materialise and Johnson & Johnson have collaborated to produce customized CMF plates tailored to each patient’s unique anatomy, improving implant fit, biomechanical performance, and patient satisfaction

- The adoption of advanced biomaterials is reshaping the market as well. Titanium remains the gold standard for strength and biocompatibility, while bioabsorbable materials such as PLA and PGA are gaining popularity, especially for pediatric cases, eliminating the need for a second surgery for implant removal. Stryker’s Vitoss Bioactive Foam is an example of a biomaterial that promotes bone regeneration while being resorbable over time

- The push toward ambulatory surgical center (ASC)-friendly fixation devices is also accelerating. Products designed for outpatient procedures—such as Zimmer Biomet’s Periarticular Locking Plate System—support quicker recovery, reduced hospital stays, and lower infection risks, aligning with healthcare systems’ increasing focus on cost-efficiency and patient comfort

North America Trauma Fixation Market Dynamics

Driver

Growing Need Due to Rising Incidence of Orthopedic Injuries and Advancements in Surgical Procedures

- The escalating prevalence of orthopedic injuries, fractures, and trauma cases caused by road accidents, sports-related incidents, and age-related bone degeneration is a major factor driving the demand for trauma fixation devices North Americaly. Both developed and developing nations are witnessing a surge in cases requiring surgical intervention for bone stabilization and alignment

- For instance, In May 2024, a study proposed an automatic genetic algorithm framework for optimizing three-dimensional surgical plans for forearm corrective osteotomies. This framework utilizes patient-specific 3D models and multi-objective optimization to determine the optimal position and orientation of the osteotomy plane and fixation hardware, aiming to improve surgical outcomes

- As healthcare professionals aim to improve recovery times and reduce post-surgical complications, trauma fixation devices—such as plates, screws, rods, and external fixators—are increasingly preferred for their ability to provide immediate bone stability and facilitate early mobilization of patients

- Furthermore, continuous advancements in minimally invasive orthopedic surgeries and the development of biocompatible fixation materials are making trauma fixation solutions more effective and safer. Such innovations are also contributing to reduced hospital stays and improved quality of life for patients

- The growing demand for customized fixation devices, availability of 3D printing in medical manufacturing, and an increasing number of specialized orthopedic trauma care units are further fueling the expansion of the trauma fixation market across both residential-style clinics and large-scale hospital settings

Restraint/Challenge

Concerns Regarding Surgical Risks and High Initial Costs

- Despite strong market potential, trauma fixation adoption faces challenges due to surgical risks such as infection, implant rejection, and the need for revision surgeries. These complications can affect patient confidence and influence surgeons' recommendations, particularly in regions with limited access to advanced post-operative care

- For instance, high-profile clinical reports of post-surgical complications—such as implant loosening or hardware failure—have raised awareness about the importance of quality assurance in trauma fixation manufacturing and surgical skill enhancement

- Addressing these risks requires the use of high-grade, biocompatible materials, adherence to strict sterilization protocols, and continuous training for orthopedic surgeons. Companies like Stryker and Zimmer Biomet highlight their robust R&D efforts to produce fixation systems with improved durability, reduced infection risk, and enhanced patient compatibility

- Another significant barrier is the relatively high initial cost of advanced trauma fixation systems compared to traditional orthopedic repair methods. In price-sensitive regions, especially in low- and middle-income countries, this can deter hospitals and patients from adopting premium solutions. While basic fixation devices are becoming more affordable, advanced systems—integrated with navigation tools or made from specialized alloys—remain expensive

- Overcoming these challenges requires not only making trauma fixation systems more cost-effective but also implementing public health policies that support subsidized orthopedic care, expanding health insurance coverage, and increasing patient awareness about the long-term benefits of high-quality trauma fixation devices

North America Trauma Fixation Market Scope

The market is segmented on the basis of product type, material, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the trauma fixation market is segmented into internal fixator devices and external fixator devices. The internal fixator devices segment accounted for 61.4% of the market revenue share in 2024, driven by their ability to provide stable fixation, enable early mobilization, and reduce recovery times for patients with complex fractures. Devices such as plates, screws, rods, and nails are widely preferred in both elective and emergency orthopedic surgeries due to their proven long-term outcomes and compatibility with minimally invasive techniques. The segment also benefits from continuous innovation in design, such as anatomically contoured plates and locking screw systems that enhance surgical precision.

The external fixator devices segment is expected to witness the fastest CAGR of 7.9% from 2025 to 2032, supported by their versatility in treating open fractures, complex bone deformities, and severe trauma cases where internal fixation is not viable. Growing demand for modular and lightweight external fixators, along with increased adoption in low-resource settings due to their reusability, is further fueling market expansion.

- By Material

On the basis of material, the trauma fixation market is segmented into metallic implants (steel, titanium, and other), carbon fiber (thermoplastic), hybrid implants, bioabsorbable materials, and grafts and orthobiologics. The metallic implant segment held 54.8% of the market share in 2024, with titanium dominating due to its biocompatibility, corrosion resistance, and ability to integrate with bone tissue. Stainless steel remains a cost-effective option, particularly in emerging economies, for high-strength load-bearing applications.

The carbon fiber (thermoplastic) segment is projected to grow at the fastest CAGR of 8.4% from 2025 to 2032, driven by its radiolucency—which allows for clear imaging without interference—and lightweight properties that improve patient comfort. The development of hybrid implants combining metallic and composite materials, as well as increased adoption of bioabsorbable implants that eliminate the need for removal surgery, is transforming the material landscape in trauma fixation.

- By Application

On the basis of application, the trauma fixation market is segmented into shoulder and elbow, hand and wrist, pelvic, hip and femur, tibia, craniomaxillofacial, knee, foot and ankle, spinal, and others. The hip and femur segment held the largest revenue share of 28.3% in 2024, driven by the high incidence of fractures in elderly populations and the increasing number of total and partial hip replacement procedures worldwide. These injuries often require robust fixation systems to restore mobility and reduce the risk of complications.

The craniomaxillofacial segment is expected to register the fastest CAGR of 9.1% from 2025 to 2032, fueled by advancements in 3D printing technology for patient-specific implants and the rising demand for reconstructive surgeries following trauma or congenital defects.

- By End User

On the basis of end user, the trauma fixation market is segmented into hospitals, ambulatory surgical centers, trauma centers, and others. The hospitals segment dominated the market in 2024 with 66.5% share, due to their advanced infrastructure, skilled orthopedic surgeons, and ability to manage complex trauma cases requiring multidisciplinary care. Hospitals also lead in adopting new surgical technologies and high-end fixation systems through collaborations with medical device manufacturers.

The ambulatory surgical centers segment is expected to experience the fastest CAGR of 8.2% from 2025 to 2032, driven by the shift toward outpatient orthopedic procedures, cost-efficiency, and reduced patient waiting times.

- By Distribution Channel

On the basis of distribution channel, the trauma fixation market is segmented into direct tender, retail sales, and online sales. The direct tender segment accounted for 72.8% of the revenue share in 2024, supported by bulk purchasing by hospitals and government healthcare institutions, which ensures consistent supply and cost savings.

The online sales segment is expected to witness the fastest CAGR of 9.4% from 2025 to 2032, owing to the growing acceptance of digital procurement platforms, increased product visibility, and competitive pricing.

North America Trauma Fixation Market Regional Analysis

- The North America trauma fixation market accounted for 47% of the global market revenue in 2024, driven by the rising number of trauma cases, high healthcare expenditure, and strong reimbursement frameworks supporting advanced fixation technologies across hospitals, trauma centers, and orthopedic clinics. North America benefits from a mature healthcare infrastructure, widespread adoption of minimally invasive surgical techniques, and ongoing innovation in trauma care devices

- The growing prevalence of orthopedic injuries due to road accidents, sports-related trauma, and age-associated fractures is accelerating the adoption of internal and external fixation systems in the region. Investments in surgical innovation and patient recovery initiatives are fueling demand, particularly in orthopedic centers and high-volume hospitals. The segment delivering internal fixator devices dominated revenue in 2024, reflecting the preference for stable, long-term bone stabilization solutions

- Technological advancements in materials and device design—including titanium and locking plate systems, customizable implants, and streamlined surgical instrumentation—are further elevating market growth, particularly in institutions focused on improving clinical outcomes and reducing recovery times. North America’s leadership is bolstered by robust R&D, rapid regulatory approvals, and collaboration between manufacturers and healthcare providers

U.S. Trauma Fixation Market Insight

The U.S. trauma fixation market continues to dominate the North America Trauma Fixation market, commanding the largest revenue share of approximately 85.4% in 2024. This market leadership is underpinned by the country’s highly developed orthopedic surgery infrastructure, which includes an extensive network of specialized trauma centers, advanced surgical facilities, and a robust post-operative rehabilitation ecosystem. The U.S. is also home to several globally recognized market players—such as Johnson & Johnson (DePuy Synthes), Stryker, and Zimmer Biomet—whose headquarters and R&D hubs are instrumental in driving innovation in trauma fixation devices. Technological advancements, including patient-specific implants, titanium locking plates, biodegradable screws, and computer-assisted surgical navigation, have significantly enhanced surgical precision and patient recovery outcomes. Furthermore, continuous investments in trauma care research, coupled with broad insurance coverage for orthopedic procedures, enable a higher rate of adoption for both traditional and next-generation fixation solutions. The country’s high incidence of road traffic accidents, sports-related injuries, and fracture cases among the elderly population further sustains demand for advanced fixation devices.

Canada Trauma Fixation Market Insight

The Canada trauma fixation market is positioned as the fastest-growing country in the North America Trauma Fixation market, projected to record a CAGR of 10.9% from 2025 to 2032. This robust growth trajectory is supported by increasing government healthcare spending aimed at modernizing trauma care infrastructure and ensuring accessibility in both urban hospitals and remote medical facilities. The expansion of specialized trauma units, along with the integration of advanced surgical technologies such as minimally invasive fixation techniques and hybrid plating systems, is transforming orthopedic care delivery in the country. Additionally, Canada is witnessing a demographic shift marked by a rapidly growing geriatric population, which is more susceptible to osteoporosis-related fractures and other skeletal injuries. Public awareness campaigns, particularly in rural and underserved areas, are also encouraging early diagnosis and treatment, leading to a higher uptake of advanced fixation solutions. The supportive reimbursement environment and collaborative efforts between Canadian hospitals and global orthopedic device manufacturers are further accelerating the adoption of cutting-edge trauma fixation devices.

North America Trauma Fixation Market Share

The trauma fixation industry is primarily led by well-established companies, including:

- Weigao Group (China)

- Orthofix Medical Inc. (U.S.)

- CONMED Corporation (U.S.)

- Wright Medical Group N.V. (Netherlands)

- OsteoMed (U.S.)

- Invibio Ltd. (U.K.)

- Medtronic (Ireland)

- Smith + Nephew (U.K.)

- Zimmer Biomet (U.S.)

- B. Braun SE (Germany)

- Stryker (U.S.)

- Implantate AG (Germany)

- Johnson & Johnson and its affiliates (U.S.)

- Inion OY (Finland)

- Arthrex Inc. (U.S.)

- Jeil Medical Corporation (South Korea)

- Bioretec Ltd. (Finland)

Latest Developments in North America Trauma Fixation Market

- In August 2021, Zimmer Biomet Holdings Inc., announced that the company had received FDA clearance of the ROSA Hip system for the treatment of total hip arthroplasty. This robotic system is designed to aid surgeons in the evaluation and execution of their surgical plan while measuring cup orientation, leg length, and offset intra-operatively

- In March 2024, Stryker Corporation launched the SmartScrew Pro, an advanced trauma fixation device equipped with real-time bone healing monitoring capabilities. This innovation aims to enhance patient outcomes by providing surgeons with immediate feedback on the healing process, thereby improving surgical precision and recovery times.

- In January 2024, Zimmer Biomet introduced the BioFIX Absorbable System, a bioresorbable plating system primarily designed for pediatric trauma cases. Clinical trials in the European Union demonstrated a 42% reduction in the need for secondary surgeries, highlighting the system's potential to improve patient recovery and reduce healthcare costs.

- In September 2023, Orthofix announced the full commercial launch of its Galaxy Fixation Gemini System. This system is designed for orthopedic trauma procedures, offering enhanced stability and flexibility in treating fractures of the lower and upper limbs. The launch signifies Orthofix's commitment to advancing trauma care through innovative solutions

- In October 2024, a study introduced the "StraightTrack" system, a mixed reality navigation system designed to assist in the precise placement of Kirschner wires (K-wires) during percutaneous pelvic trauma surgery. This system provides real-time 3D visualization and guidance, enhancing the accuracy of wire placement and reducing complications associated with misplacement

- In May 2024, a study proposed an automatic genetic algorithm framework for optimizing three-dimensional surgical plans for forearm corrective osteotomies. This framework utilizes patient-specific 3D models and multi-objective optimization to determine the optimal position and orientation of the osteotomy plane and fixation hardware, aiming to improve surgical outcomes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.