Chronic Venous Disorders (CVDs) — including varicose veins, chronic venous insufficiency, edema, and venous leg ulcers — are costly, debilitating, and typically progressive. Global risk factors like aging, obesity, sedentary behavior, and hereditary predisposition combine to increase this burden. Compression therapy is the frontline non-surgical treatment recommended by vascular health experts. Because CVDs often require lifelong management, demand for compression garments and devices continues to grow sustainably. This escalating demand underscores the need for ongoing innovation in compression technologies, providing more comfortable and effective solutions.

Furthermore, increased awareness and early diagnosis are crucial for slowing disease progression and improving patient quality of life. The economic impact of CVDs also underscores the importance of preventative measures and accessible, long-term management strategies. Ultimately, a multi-pronged approach involving lifestyle modifications, early intervention, and advanced compression therapies is essential to mitigate the rising global burden of CVDs.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-heartstring-device-and-enclosure-device-market

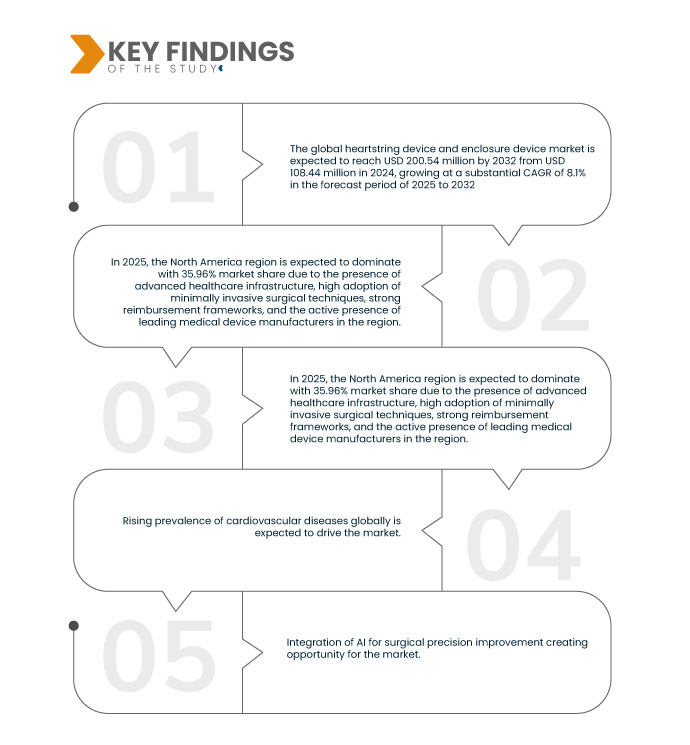

Data Bridge market research analyzes that the Global Heartstring Device and Enclosure Device Market is expected to reach USD 200.54 million by 2032 from USD 108,44 million in 2024, growing at a substantial CAGR of 8.1% in the forecast period of 2025 to 2032.

Key Findings of the Study

Rising Prevalence of Cardiovascular Diseases (CVDs) Globally

Cardiovascular Diseases (CVDs), encompassing ischemic heart disease, stroke, heart failure, congenital defects, and thromboembolic events, are the foremost global cause of death. Demographic shifts, chronic conditions like hypertension and diabetes, and risk behaviors such as smoking and physical inactivity are major contributors to escalating incidence rates. This trend fuels demand for a spectrum of preventive, diagnostic, interventional, and therapeutic technologies. Consequently, there's an urgent need for innovative medical devices and pharmaceuticals to combat this rising burden effectively.

Furthermore, public health initiatives that promote healthier lifestyles and early screening are crucial in mitigating risk factors. The increasing complexity of CVDs also necessitates advanced diagnostic tools capable of precise and timely detection. Ultimately, a multi-faceted approach combining technological innovation, public health efforts, and enhanced clinical interventions is essential to address this global health challenge.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2025 to 2032

|

|

Base Year

|

2024

|

|

Historic Years

|

2018-2023 (Customizable to 2013-2017)

|

|

Quantitative Units

|

Revenue in USD Million

|

|

Segments Covered

|

Product Type (Enclose Device, and Heartstring Device), Application (Coronary Artery Bypass Grafting (CABG), Aortic Anastomosis, Valve Surgery, and Other), Technology Type (Manual, Automated or Semi-Automated, and Others), End-User (Hospitals, Cardiac Surgery Centers, Academic & Research Institutes, and Others), Distribution Channel (Direct Tenders, Distributors & Dealers, Online Procurement Platforms, and Others)

|

|

Countries Covered

|

U.S., Canada, Mexico, China, Japan, India, South Korea, Singapore, Thailand, Indonesia, Philippines, Australia & New Zealand, Hong Kong, Taiwan, Vietnam, Uzbekistan, and Rest of Asia-Pacific, Germany, Italy, France, Spain, U.K., Switzerland, Netherlands, Belgium, Turkey, Russia, Denmark, Norway, Finland, Sweden, Rest of Europe, Brazil, Argentina, Chile, Colombia, Ecuador, Peru, Uruguay, Venezuela, Bolivia, Paraguay, Rest of South America, Saudi Arabia, United Arab Emirates, South Africa, Egypt, Israel, Qatar, Kuwait, Oman, Bahrain, Rest of Middle East and Africa

|

|

Market Players Covered

|

Peters Surgical (France), Getinge (Sweden), KARL STORZ (Germany), Johnson & Johnson (U.S.), Teleflex Incorporated (U.S.), Artivion, Inc. (U.S.), Cardinal Health (U.S.), Henry Schein, Inc. (U.S.), Medline Industries, LP (U.S.), Owens & Minor, Inc. (U.S.), Uniphar Group Plc. (Ireland), Medtronic (Ireland), Terumo Corporation (Japan), Sontec Instruments, Inc. (U.S.), Santair AE (Greece), Fumedica Medizintechnik GmbH (Switzerland)

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework.

|

Segment Analysis

Global heartstring device and enclosure device market is categorized into five notable segments which are based on product type, application, technology type, end-user, and distribution channel.

- On the basis of product type, global heartstring device and enclosure device market is segmented into enclose device and heartstring device

In 2025, the enclose device segment is expected to dominate the global heartstring device and enclosure device market

In 2025, the enclosed device segment is expected to dominate the heart stent market with a 64.46% share due to its enhanced safety profile, lower risk of infection, better procedural control, and growing preference among healthcare providers for devices that minimize exposure during implantation. Additionally, technological advancements and supportive regulatory approvals are driving higher adoption rates in both developed and emerging markets.

- On the basis of application, the global heartstring device and enclosure device market is segmented into Coronary Artery Bypass Grafting (CABG), aortic anastomosis, valve surgery, and other

In 2025, the Coronary Artery Bypass Grafting (CABG) segment is expected to dominate the global heartstring device and enclosure device market

In 2025, the Coronary Artery Bypass Grafting (CABG) segment is expected to dominate the market with a 73.48% share due to the high prevalence of coronary artery disease, increasing preference for surgical interventions, and the effectiveness of CABG in improving long-term patient outcomes.

- On the basis of technology type, the global heartstring device and enclosure device market is segmented into manual, automated or semi-automated, and others. In 2025, the manual segment is expected to dominate the market with a 64.49% share

- On the basis of end user, the global heartstring device and enclosure device market is segmented into hospitals, cardiac surgery centers, academic & research institutes, and others. In 2025, the hospitals segment is expected to dominate the market with a 62.64% share

- On the basis of distribution channel, the global heartstring device and enclosure device market is segmented into direct tenders, distributors & dealers, online procurement platforms, and others. In 2025, the direct tenders segment is expected to dominate the market with a 47.04% share

Major Players

Data Bridge Market Research Analyses KARL STORZ (Germany), Getinge (Sweden), Peters Surgical (U.K.) others as the major market players of the market.

Market Developments

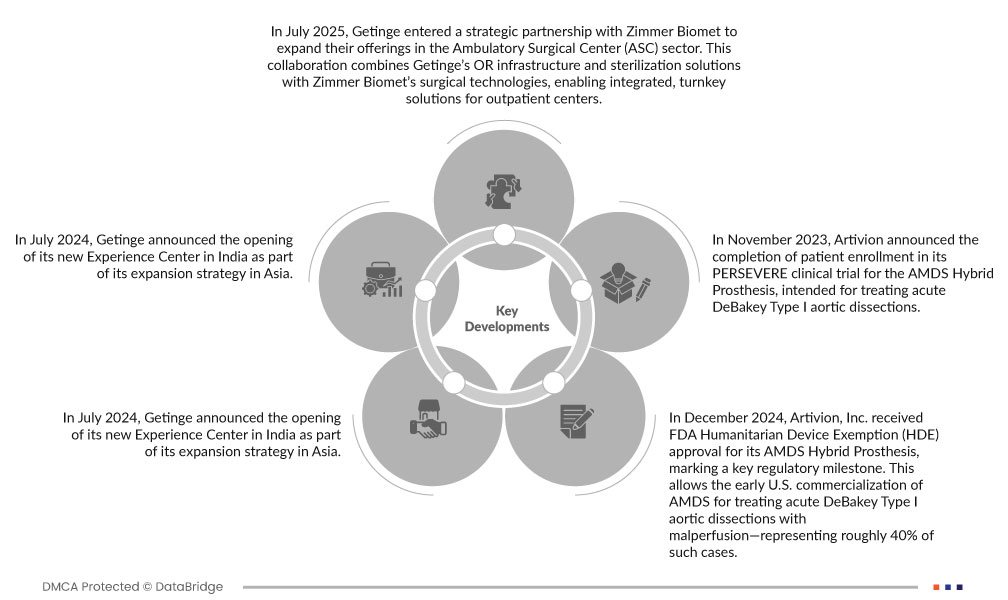

- In July 2025, Getinge entered a strategic partnership with Zimmer Biomet to expand their offerings in the Ambulatory Surgical Center (ASC) sector. This collaboration combines Getinge’s OR infrastructure and sterilization solutions with Zimmer Biomet’s surgical technologies, enabling integrated, turnkey solutions for outpatient centers. The partnership enhances Getinge’s market reach, strengthens its ASC positioning, and supports growth in minimally invasive surgical care

- In July 2024, Getinge announced the opening of its new Experience Center in India as part of its expansion strategy in Asia. This facility offers hands-on demonstrations of advanced surgical, intensive care, and sterile reprocessing solutions. The development enhances Getinge’s customer engagement, training capabilities, and strengthens its presence in a rapidly growing healthcare market

- In October 2023, Getinge acquired Healthmark Industries Co. Inc. for approximately USD 320 million. Healthmark is a key provider of instrument care and infection control consumables. This acquisition strengthens Getinge’s position in sterile reprocessing, particularly in the U.S., while supporting global expansion of Healthmark’s product offerings

- In December 2024, Artivion, Inc. received FDA Humanitarian Device Exemption (HDE) approval for its AMDS Hybrid Prosthesis, marking a key regulatory milestone. This allows the early U.S. commercialization of AMDS for treating acute DeBakey Type I aortic dissections with malperfusion—representing roughly 40% of such cases. The device also holds Breakthrough and Humanitarian Use Designation due to its life-saving potential in a rare, high-risk condition. This development strengthens Artivion’s leadership in the structural heart and aortic surgery market, expands its clinical footprint, and paves the way for broader Premarket Approval (PMA) coverage in the future

- In November 2023, Artivion announced the completion of patient enrollment in its PERSEVERE clinical trial for the AMDS Hybrid Prosthesis, intended for treating acute DeBakey Type I aortic dissections. The 93-patient, U.S.-based study will support a PMA (Premarket Approval) application to the FDA by 2025. This milestone strengthens Artivion’s position in the aortic and structural heart device market, targeting reduced mortality and complications in high-risk aortic surgery cases

Regional Analysis

Geographically, the countries covered in the global heartstring device and enclosure device market report are the U.S., Canada, Mexico, China, Japan, India, South Korea, Singapore, Thailand, Indonesia, Philippines, Australia & New Zealand, Hong Kong, Taiwan, Vietnam, Uzbekistan, and rest of Asia-Pacific, Germany, Italy, France, Spain, U.K., Switzerland, Netherlands, Belgium, Turkey, Russia, Denmark, Norway, Finland, Sweden, Rest of Europe, Brazil, Argentina, Chile, Colombia, Ecuador, Peru, Uruguay, Venezuela, Bolivia, Paraguay, rest of South America, Saudi Arabia, United Arab Emirates, South Africa, Egypt, Israel, Qatar, Kuwait, Oman, Bahrain, rest of Middle East and Africa.

As per Data Bridge Market Research analysis:

North America is the dominant region in the global heartstring device and enclosure device market

North America dominates the global heartstring and enclosure device market due to advanced healthcare infrastructure, high prevalence of cardiovascular diseases, growing geriatric population, strong government support for cardiac care, and presence of leading medical device manufacturers driving innovation and market growth in the region.

North America is estimated to be the fastest-growing region in the global heartstring device and enclosure device market

North America is expected to be the fastest-growing region in the global heartstring and enclosure device market from 2025 to 2052, driven by rising cardiovascular disease prevalence, increasing awareness and adoption of minimally invasive procedures, technological advancements, and expanding healthcare infrastructure.

As per Data Bridge Market Research analysis:

For more detailed information about the global heartstring device and enclosure device market report, click here – https://www.databridgemarketresearch.com/reports/global-heartstring-device-and-enclosure-device-market