The Global Precision Gearbox Market encompasses the design, manufacturing, distribution, and commercialization of precision gearboxes in various types, including planetary, helical, harmonic, cycloidal, bevel, spur, worm, cylindrical, and others. Precision gearboxes are widely used across industries such as robotics, machine tools, material handling, automotive, aerospace and defense, medical, packaging, and food and beverages due to their ability to deliver high torque, low backlash, and accurate motion control. These gearboxes are produced using materials like steel, aluminum, plastics, and titanium, and are available in various configurations such as flange output, hollow shaft, tapped holes, and through holes. The market serves applications ranging from lightweight precision systems to high-torque industrial machinery, with torque capacities from below 50 Nm to above 3000 Nm. Key factors driving the market include the global push for automation, demand for high-efficiency motion systems, and technological advancements in gear design and materials. The market caters to OEMs, industrial automation providers, and end-users across both developed and emerging economies.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-precision-gearbox-market

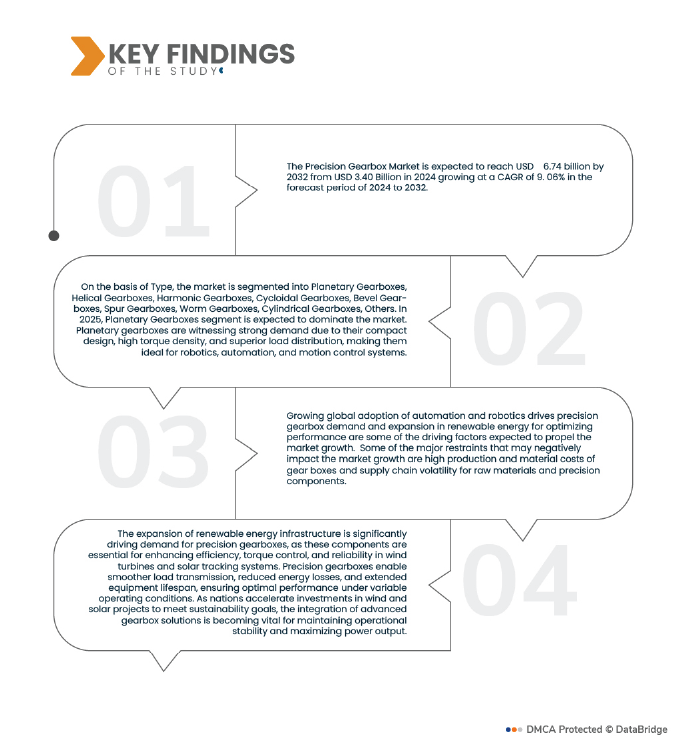

Data Bridge market research analyzes that The Global Precision Gearbox Market is expected to reach USD 674 Billion by 2032 from USD 3.40 Billion in 2024 growing at a CAGR of 9.06% in the forecast period of 2024 to 2032.

Key Findings of the Study

Expansion in Renewable Energy for Optimizing Performance

The expansion of renewable energy infrastructure is significantly driving demand for precision gearboxes, as these components are essential for enhancing efficiency, torque control, and reliability in wind turbines and solar tracking systems. Precision gearboxes enable smoother load transmission, reduced energy losses, and extended equipment lifespan, ensuring optimal performance under variable operating conditions. As nations accelerate investments in wind and solar projects to meet sustainability goals, the integration of advanced gearbox solutions is becoming vital for maintaining operational stability and maximizing power output.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2025 to 2032

|

|

Base Year

|

2024

|

|

Historic Years

|

2023 (Customizable to 2018-2022)

|

|

Quantitative Units

|

Revenue in USD Billion

|

|

Segments Covered

|

By Type (Planetary Gearboxes, Helical Gearboxes, Harmonic Gearboxes, Cycloidal Gearboxes, Bevel Gearboxes, Spur Gearboxes, Worm Gearboxes, Cylindrical Gearboxes, Others), Axis Orientation (In‑Line, Right Angle, Parallel), Bearing Type (Deep Groove Ball Bearings, Tapered Roller Bearings, Cylindrical Roller Bearings, Needle Roller Bearings, Cross Roller Bearings, Others), Mounting Style (Flange Output, Hollow Shaft, Tapped Holes, Through Holes, Others), Torque (UP TO 50 NM, 50-500 NM, 500-1000 NM, 1000-3000 NM, ABOVE 3000 NM), Material (Steel, Aluminum, Plastics, Titanium, Others), Axle Load Capacity (Up To 800 N, 800-1500 N, More Than 1500 N), Gearbox Stage (Multi Stage, Single, Double), Application (Robotics, Machine Tools, Material Handling, Construction Equipment, Automotive, Semiconductor Equipment, Aerospace and Defense, Agricultural, Packaging, Medical, Food and Beverages, Others) , Sales Channel ( Direct (OEM), Aftermarket)

|

|

Countries Covered

|

U.S., Canada and Mexico in North America, Germany, U.K., France, Spain, Belgium, Russia, Netherlands, Italy, Turkey, Switzerland, Sweden, Denmark, Norway, Finland, and Rest of Europe in Europe, India, China, Japan, Australia, South Korea, Singapore, Thailand, Indonesia, Taiwan, Hong Kong, Malaysia, New Zealand, Philippines, and Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), U.A.E, Saudi Arabia, South Africa, Egypt, Qatar, Kuwait, Bahrain, Oman, Israel, and Rest of Middle East and Africa as a part of Middle East and Africa (MEA), Brazil, Argentina and rest of South America as part of South America.

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis..

|

Segment Analysis

The Global Precision Gearbox market is segmented into nine segments based on type, Axis Orientation, Bearing Type, Mounting Style, Torque, Material, Axle Load Capacity, Gearbox Stage, and Application.

- On the basis of Type, the market is segmented into Planetary Gearboxes, Helical Gearboxes, Harmonic Gearboxes, Cycloidal Gearboxes, Bevel Gearboxes, Spur Gearboxes, Worm Gearboxes, Cylindrical Gearboxes, Others.

In 2025, the Planetary Gearboxes segment is expected to dominate the market

. In 2025, Planetary Gearboxes segment is expected to dominate the market. Planetary gearboxes are witnessing strong demand due to their compact design, high torque density, and superior load distribution, making them ideal for robotics, automation, and motion control systems. Their low backlash and high efficiency enable precise positioning and speed regulation. The growing adoption of collaborative robots (cobots), packaging machinery, and industrial automation lines is accelerating planetary gearbox deployment for smoother motion transmission and energy-efficient mechanical performance across diverse industrial applications.

- On the basis of Axis Orientation, the market is segmented into In Line, Right Angle, and Parallel.

In 2025, the In Line segment is expected to dominate the market

In 2025, the In Line segment is expected to dominate the market due to Line gearboxes, designed for linear motion applications, are increasingly adopted in automated assembly systems, material handling, and CNC machinery. Their high precision, rigidity, and low noise operation make them suitable for modern manufacturing environments emphasizing speed and accuracy. With the ongoing expansion of smart factories and automated production lines, line gearboxes enable synchronized motion control and improved process efficiency, driving their integration into industries prioritizing precision alignment and consistent mechanical performance.

- On the basis of Bearing Type, the market is segmented into Deep Groove Ball Bearings, Tapered Roller Bearings, Cylindrical Roller Bearings, Needle Roller Bearings, Cross Roller Bearings, and Others.

In 2025, the Deep Groove Ball Bearings segment is expected to dominate the market

In 2025, the Deep Groove Ball Bearings segment is expected to dominate the market due to their versatility, low friction, cost-effectiveness, and ability to handle both radial and axial loads in a wide range of precision gearbox applications Deep groove ball bearings play a crucial role in precision gearboxes by reducing friction, enhancing load-bearing capacity, and ensuring smooth rotational motion. Their high-speed capability and low maintenance requirements make them essential for robotics, medical equipment, and electric vehicle drivetrains. As manufacturers emphasize energy efficiency and compact design, the integration of high-performance deep groove ball bearings within gear mechanisms ensures longer service life, quieter operation, and improved gearbox efficiency under variable load conditions.

- On the basis of Mounting Style, the market is segmented into Flange Output, Hollow Shaft, Tapped Holes, Through Holes, and Others.

In 2025, the Flange Output segment is expected to dominate the market

In 2025, the Flange Output segment is expected to dominate the market due to its robust structural support, ease of alignment, high torque transmission capability, and widespread use in industrial automation and heavy-duty machinery applications.. Flange output gearboxes are gaining traction due to their versatility, easy mounting configuration, and ability to deliver high torque in compact assemblies. Widely used in automation and robotics, they ensure precise motion transfer and structural stability during high-speed operations. The rising demand for space-saving designs in production lines and the need for enhanced torque transmission in servo systems are key drivers propelling the use of flange output gearboxes across multiple industrial and robotic applications.

- On the basis of Torque, the market is segmented into UP TO 50 NM, 50-500 NM, 500-1000 NM, 1000-3000 NM, ABOVE 3000 NM. In 2025, the UP TO 50 NM segment is expected to dominate the market due to its high demand in compact and lightweight applications such as robotics, medical devices, and precision instruments where low torque and high accuracy are essential.

In 2025, the UP TO 50 NM segment is expected to dominate the market

In 2025, the UP TO 50 NM segment is expected to dominate the market due to its high demand in compact and lightweight applications such as robotics, medical devices, and precision instruments where low torque and high accuracy are essential. Gearboxes in the up to 50 Nm torque range are primarily used in light-duty automation, robotics, and packaging applications where precision and compactness are critical. Their ability to deliver smooth torque transmission in limited spaces supports miniaturized robotic arms and medical devices. Growing trends in collaborative robotics, laboratory automation, and lightweight industrial machinery are fueling demand for these gearboxes, as they offer the ideal balance between efficiency, accuracy, and operational flexibility.

- On the basis of Material, the market is segmented into Steel, Aluminum, Plastics, Titanium, and Others.

In 2025, the Steel segment is expected to dominate the market

In 2025, the Steel segment is expected to dominate the market due to its superior strength, durability, high load-bearing capacity, and widespread use in heavy-duty and high-performance precision gearbox applications across various industries. Steel-based precision gearboxes dominate due to their superior strength, durability, and heat resistance, enabling reliable operation under high-load conditions. Steel ensures longer service life, minimal wear, and high mechanical stability, making it the preferred material for heavy-duty industrial and robotics applications. The push toward sustainable manufacturing and precision machining has increased the use of hardened steel gears for better torque output, reduced vibration, and improved operational safety in demanding automation environments.

- On the basis of Axle Load Capacity, the market is segmented into Up To 800 N, 800-1500 N, and More Than 1500 N.

In 2025, the Up To 800 N segment is expected to dominate the market

In 2025, the Up To 800 N segment is expected to dominate the market due to due to its suitability for compact and lightweight applications, particularly in robotics, automation, and electronics, where lower load requirements and high precision are critical. Precision gearboxes designed for up to 800 N load capacity cater to medium-load applications in robotics, material handling, and automated inspection systems. Their ability to handle consistent mechanical stress while maintaining precision motion enhances productivity in industrial automation. Growing investment in mid-capacity robotic arms, packaging machines, and conveyor systems is driving demand for gearboxes in this range, offering optimal power density, low maintenance, and reliable performance in dynamic load environments.

- On the basis of Gearbox Stage, the market is segmented into Multi Stage, Single, and Double.

In 2025, the Multi Stage segment is expected to dominate the market

In 2025, the Multi Stage segment is expected to dominate the market due to its ability to provide higher torque output, better load distribution, and improved efficiency in complex industrial applications requiring precise motion control and greater speed reduction. Multi-stage gearboxes are increasingly preferred for their ability to provide high reduction ratios, enhanced torque output, and improved efficiency. Their layered configuration ensures precise motion control and superior load distribution, ideal for robotics, aerospace, and precision machinery applications. With industries focusing on energy-efficient and high-performance motion systems, multi-stage gearboxes deliver smoother transmission and minimal backlash, enabling optimized operational accuracy and reduced mechanical stress in complex automation processes.

- On the basis of Application, the market is segmented into Robotics, Machine Tools, Material Handling, Construction Equipment, Automotive, Semiconductor Equipment, Aerospace and Defense, Agricultural, Packaging, Medical, Food and Beverages, and Others.

In 2025, the Robotics segment is expected to dominate the market

In 2025, the Robotics segment is expected to dominate the market. In robotics, precision gearboxes are critical for ensuring accurate positioning, torque control, and repeatable motion across joints and actuators. The surge in automation, collaborative robots, and medical robotics is driving demand for compact, high-efficiency gearbox solutions. These gearboxes support fast response times and stable motion even under fluctuating loads. As industries transition toward intelligent, autonomous manufacturing systems, the integration of advanced precision gearboxes is central to achieving consistent, safe, and energy-efficient robotic performance.

In 2025, the Direct (OEM) segment is expected to dominate the market

In 2025, the Direct (OEM) segment is expected to dominate the market, driven by the strong preference of original equipment manufacturers for direct procurement of precision gearboxes to ensure quality, reliability, and seamless integration into new machinery and robotic systems. OEMs are increasingly prioritizing high-performance components that meet stringent specifications for industrial automation, automotive, and semiconductor applications, which further reinforces the dominance of this sales channel.

Major Players

Siemens AG (Germany), Nabtesco Corporation (Japan), Sumitomo Electric Industries (Japan), ABB Ltd (Switzerland), Bonfiglioli (Italy), Emerson Electric Co. (U.S.), Parker Hannifin Corporation (U.S.), Regal Rexnord Corporation (U.S.), Hiwin Corporation (Taiwan), STOBER Drives Inc. (U.S.), David Brown Santasalo (United Kingdom), Neugart GmbH (Germany), Dana Incorporated (U.S.), Apex Dynamics, Inc. (Taiwan), SEW-EURODRIVE GmbH & Co KG (Germany), Cone Drive (U.S.), Spinea s.r.o. (Slovakia), WITTENSTEIN SE (Germany), Horsburgh & Scott (U.S.), GAM Enterprises, Inc. (U.S.), Nidec Drive Technology America Corporation (U.S.), Curtis Machine Company (U.S.), Newstart Planetary Gear Boxes Co., Ltd (China), Onvio LLC (U.S.), Harmonic Drive LLC (U.S.), Riley Gear Corp (U.S.), Prime Transmission (India), ATLANTA Drive Systems, Inc. (U.S.), SMD Gearbox (India)among others.

Market Developments

- In September 2022, Gabriel-Chemie introduced a new series of halogen-free flame retardant masterbatches for the electrical conduits and tubes market, emphasizing the company's commitment to sustainability. These masterbatches comply with flame retardant standard EN 61386, halogen-free standard EN 50642, and low smoke standard IEC 61304-2. Benefits include reduced toxic gas emissions during fires, enhanced recyclability, and minimized corrosion of electronic equipment and machinery.

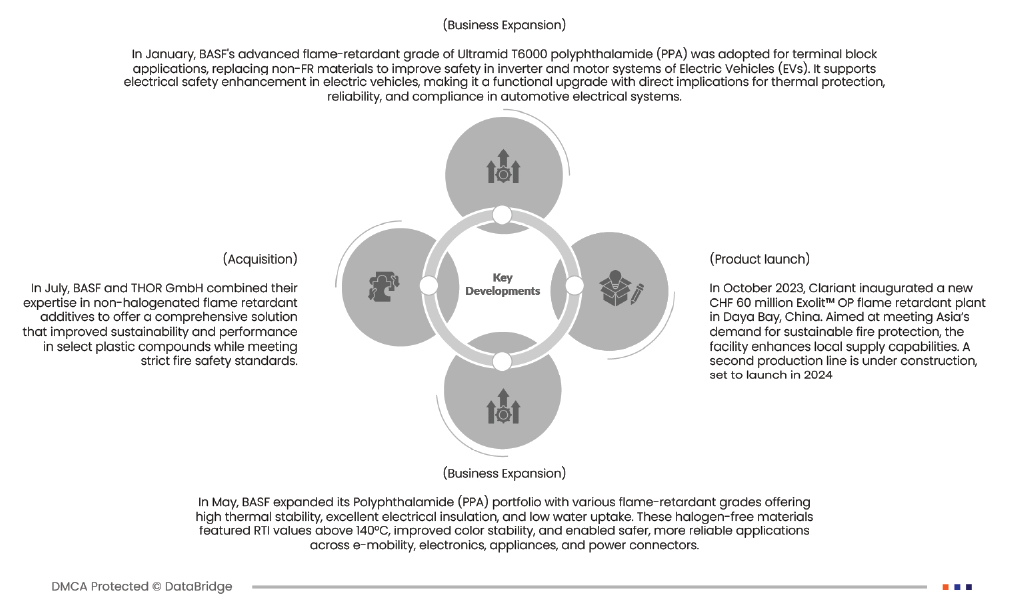

- In October 2023, Clariant inaugurated a new CHF 60 million Exolit™ OP flame retardant plant in Daya Bay, China. Aimed at meeting Asia’s demand for sustainable fire protection, the facility enhances local supply capabilities. A second production line is under construction, set to launch in 2024

- In May, BASF expanded its Polyphthalamide (PPA) portfolio with various flame-retardant grades offering high thermal stability, excellent electrical insulation, and low water uptake. These halogen-free materials featured RTI values above 140°C, improved color stability, and enabled safer, more reliable applications across e-mobility, electronics, appliances, and power connectors.

- In July, BASF and THOR GmbH combined their expertise in non-halogenated flame retardant additives to offer a comprehensive solution that improved sustainability and performance in select plastic compounds while meeting strict fire safety standards.

- In January, BASF's advanced flame-retardant grade of Ultramid T6000 polyphthalamide (PPA) was adopted for terminal block applications, replacing non-FR materials to improve safety in inverter and motor systems of Electric Vehicles (EVs). It supports electrical safety enhancement in electric vehicles, making it a functional upgrade with direct implications for thermal protection, reliability, and compliance in automotive electrical systems.

As per Data Bridge Market Research analysis:

For more detailed information about the Global Precision Gearbox Market report, click here – https://www.databridgemarketresearch.com/reports/global-precision-gearbox-market