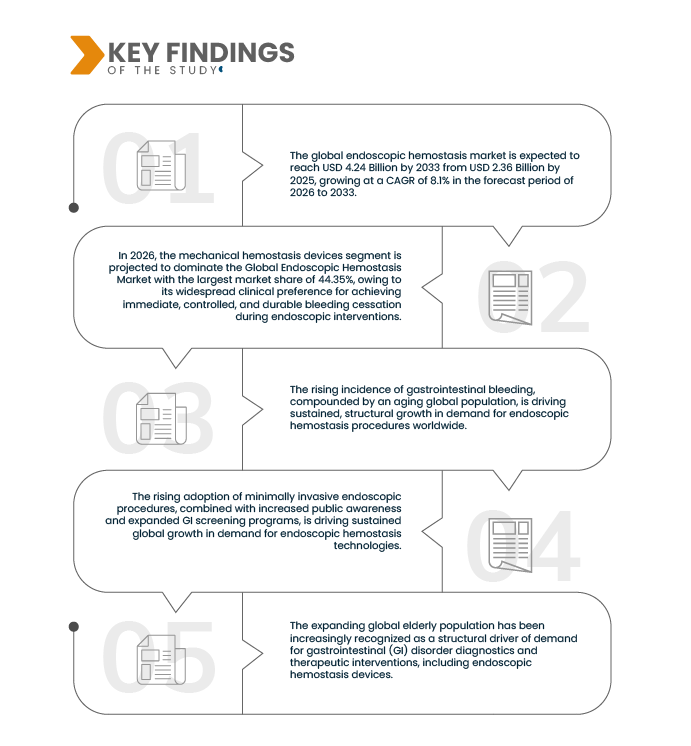

The rising incidence of gastrointestinal bleeding has been established as a foundational force propelling growth in the global endoscopic hemostasis market. As the prevalence of upper and lower gastrointestinal bleeding conditions increases worldwide, demand for minimally invasive, endoscopy-based therapeutic interventions has been intensified. Endoscopic hemostasis offers critical clinical advantages, including rapid bleeding control, reduced need for surgical intervention, lower transfusion requirements, and shorter hospital stays, thereby positioning it as a first-line treatment modality in acute and chronic gastrointestinal bleeding management. Consequently, the escalation in gastrointestinal bleeding cases—driven by aging populations, higher prevalence of liver disease, anticoagulant use, and delayed care access during systemic healthcare disruptions—has translated into higher procedural volumes and broader adoption of advanced endoscopic hemostasis devices across hospitals and endoscopy centers globally.

The global escalation in gastrointestinal bleeding incidence is being firmly established as a permanent structural growth engine for the endoscopic hemostasis market. The continuous rise in acute bleeding events, combined with expanding populations affected by chronic liver disease, antithrombotic medication use, and age-related gastrointestinal pathology, is creating a sustained and non-cyclical requirement for endoscopic bleeding control. As clinical guidelines increasingly prioritize endoscopic therapy as first-line management, reliance on hemostasis technologies for emergency intervention, recurrence prevention, and complication management is being structurally reinforced. Furthermore, improving survival rates are extending patient monitoring and repeat intervention cycles, thereby multiplying lifetime procedural demand. This dynamic is anchoring endoscopic hemostasis adoption closely to global epidemiological trends, positioning this driver as a long-term foundational pillar for market expansion across developed and emerging healthcare systems.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-endoscopic-hemostasis-market

Data Bridge market research analyzes that the Global Endoscopic Hemostasis Market is expected to reach USD 4.24 Billion by 2033 from USD 2.36 Billion in 2025, growing at a substantial CAGR of 8.1% in the forecast period of 2026 to 2033.

Key Findings of the Study

Aging Population Driving Increased Demand for GI Disorders.

The expanding global elderly population has been increasingly recognized as a structural driver of demand for gastrointestinal (GI) disorder diagnostics and therapeutic interventions, including endoscopic hemostasis devices. As life expectancy rises and the proportion of older adults grows, age-associated physiological changes in the gastrointestinal tract—such as altered motility, mucosal fragility, and increased comorbidity burdens—are leading to higher prevalence and severity of GI disorders among those aged 65 years and above, thereby straining healthcare systems and escalating utilization of endoscopic procedures. The ageing demographic is linked with increased risk for functional GI symptoms, complications including bleeding, diverticulosis, reflux disease, and other age-associated gastrointestinal conditions requiring clinical management. This demographic shift is directly correlated with greater procedural volumes and technology demand in GI therapeutic markets globally.

The global demographic shift toward a larger elderly population is driving sustained and structural growth in demand for gastrointestinal disorder management, including endoscopic hemostasis and related technologies. Age-associated physiological changes and increasing prevalence of GI symptoms in older adults are leading to higher clinical presentations and procedural requirements. With ageing populations projected to expand significantly in both developed and emerging economies, reliance on advanced endoscopic diagnostics and therapeutic interventions is being reinforced, positioning the aging demographic as a foundational long-term market driver for the global endoscopic hemostasis market.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2018-2024)

|

|

Quantitative Units

|

Revenue in USD Billion

|

|

Segments Covered

|

|

|

Countries Covered

|

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and PESTLE analysis

|

Segment Analysis

The global endoscopic hemostasis market is categorized into five key segments: product type, procedure, application, end user, and distribution channel.

- On the basis of product type, the Global endoscopic hemostasis market is segmented into mechanical hemostasis devices, thermal devices, topical agents and injectables, and others.

In 2026, the mechanical hemostasis segment is expected to dominate the market

On the basis of product type, the Global endoscopic hemostasis market is segmented into mechanical hemostasis devices, thermal devices, topical agents and injectables, and others. In 2026, the mechanical hemostasis devices segment is projected to dominate the Global Endoscopic Hemostasis Market with the largest market share of 44.35%, owing to its widespread clinical preference for achieving immediate, controlled, and durable bleeding cessation during endoscopic interventions. Mechanical solutions such as clips and banding devices are routinely favored for their ability to provide precise vessel closure without inducing thermal tissue damage, thereby lowering rebleeding rates and post-procedure complications. Their applicability across a broad spectrum of bleeding scenarios, including peptic ulcers, variceal hemorrhage, and post-polypectomy bleeding, has resulted in consistently high utilization in both emergency and elective endoscopic settings. The strong reliance on mechanical hemostasis as a first-line therapeutic approach underscores its substantial contribution to overall market revenues and reinforces its dominant position within the product type landscape throughout the forecast period.

On the basis of procedure, the market is segmented into upper gastrointestinal endoscopy, lower gastrointestinal endoscopy, bronchoscopic hemostasis, and others.

In 2026, the upper gastrointestinal endoscopy segment is expected to dominate the market

- In 2026, the upper gastrointestinal endoscopy segment is projected to dominate the Global Endoscopic Hemostasis Market with a market share of 44,09%, due to its extensive clinical adoption as the frontline procedural approach for managing acute and recurrent gastrointestinal bleeding. Upper GI endoscopy is widely relied upon for the diagnosis and immediate therapeutic control of bleeding ulcers, variceal hemorrhage, and Dieulafoy lesions, where rapid hemostatic intervention is clinically critical. The high procedural frequency in emergency departments and tertiary-care hospitals, combined with strong guideline support for early endoscopic intervention, is expected to sustain its leading market position. Its continued dominance is reflected in its substantial market share and steady growth trajectory through 2033, indicating persistent demand across both developed and emerging healthcare systems.

On the basis of application, the market is segmented into gastrointestinal bleeding, non-gastrointestinal bleeding, trauma management, and others.

In 2026, the gastrointestinal bleeding segment is expected to dominate the market

- In 2026, the gastrointestinal bleeding segment is projected to dominate the Global Endoscopic Hemostasis Market with a market share of 71.80%, owing to the high global prevalence of peptic ulcers, esophageal varices, and colorectal malignancies requiring endoscopic bleeding control. Gastrointestinal bleeding remains the most common indication for endoscopic hemostasis procedures, driving consistent utilization of mechanical, thermal, and topical hemostatic solutions across hospital and ambulatory care settings. The critical need for rapid bleeding control to reduce morbidity, hospital length of stay, and mortality is expected to reinforce sustained demand within this application segment. Its large share of total market value highlights the central role of gastrointestinal indications in shaping overall market dynamics during the forecast period.

On the basis of end user, the market is segmented into hospitals, ambulatory surgery centers, specialty clinics, and others.

In 2026, the hospitals segment is expected to dominate the market

- In 2026, the hospitals segment is projected to dominate the Global Endoscopic Hemostasis Market with the largest market share of 53.12%, due to the concentration of advanced endoscopy infrastructure, skilled gastroenterologists, and emergency care capabilities within hospital settings. Complex bleeding cases, including severe upper and lower gastrointestinal hemorrhage, are predominantly managed in public and private hospitals where comprehensive diagnostic and interventional resources are available. Higher patient inflow, greater procedural volumes, and established procurement frameworks further strengthen hospital demand for endoscopic hemostasis devices and consumables. This structural dependence on hospital-based care is expected to maintain the segment’s leading position through 2033 despite gradual growth in outpatient settings.

On the basis of distribution channel, the market is segmented into direct sales and indirect sales, with indirect sales further segmented into online and offline channels.

In 2026, the indirect sales segment is expected to dominate the market

- In 2026, the indirect sales segment is projected to dominate the Global Endoscopic Hemostasis Market with the largest market share of 58.86% as procurement is largely conducted through distributors, group purchasing organizations, and regional medical supply networks. Indirect channels are widely preferred due to their ability to offer bundled products, inventory management support, and broader geographic reach, particularly in emerging markets and decentralized healthcare systems. Hospitals and ambulatory centers frequently rely on distributor-led sourcing to ensure consistent availability of critical hemostasis devices while optimizing procurement costs. This distribution structure is expected to continue driving higher adoption of indirect sales channels throughout the forecast period..

Major Players

Micro-Tech Endoscopy (China), Taewoong Medical Co., Ltd. (South Korea), Ovesco Endoscopy AG (China), Apollo Endosurgery, Inc. (U.S.), Argon Medical Devices, Inc. (U.S.), Olympus Corporation (Japan), Boston Scientific Corporation (U.S.), CONMED Corporation (U.S.), Medtronic (Ireland), Cook (U.S.), ERBE Elektromedizin GmbH (China), Karl Storz SE & Co. KG (China), Pentax Medical (Japan), Endoskopie Technik Gerhard (China), Merit Medical Systems, Inc. (U.S.), Diversatek, Inc. (U.S.), STERIS plc (Japan), B. Braun SE (China), Duomed Group (Belgium).

Market Developments

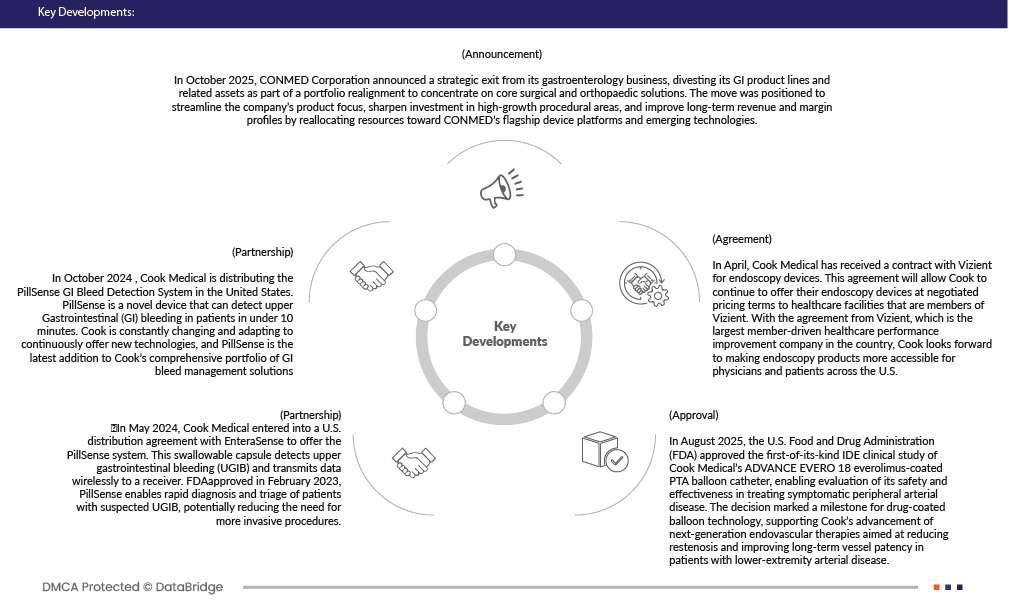

- In October 2025, CONMED Corporation announced a strategic exit from its gastroenterology business, divesting its GI product lines and related assets as part of a portfolio realignment to concentrate on core surgical and orthopaedic solutions. The move was positioned to streamline the company’s product focus, sharpen investment in high-growth procedural areas, and improve long-term revenue and margin profiles by reallocating resources toward CONMED’s flagship device platforms and emerging technologies

- In August 2025, the U.S. Food and Drug Administration (FDA) approved the first-of-its-kind IDE clinical study of Cook Medical’s ADVANCE EVERO 18 everolimus-coated PTA balloon catheter, enabling evaluation of its safety and effectiveness in treating symptomatic peripheral arterial disease. The decision marked a milestone for drug-coated balloon technology, supporting Cook’s advancement of next-generation endovascular therapies aimed at reducing restenosis and improving long-term vessel patency in patients with lower-extremity arterial disease

- In April 2023, Cook Medical has received a contract with Vizient for endoscopy devices. This agreement will allow Cook to continue to offer their endoscopy devices at negotiated pricing terms to healthcare facilities that are members of Vizient. With the agreement from Vizient, which is the largest member-driven healthcare performance improvement company in the country, Cook looks forward to making endoscopy products more accessible for physicians and patients across the U.S.

- In October, 2024, Cook Medical is distributing the PillSense GI Bleed Detection System in the United States. PillSense is a novel device that can detect upper Gastrointestinal (GI) bleeding in patients in under 10 minutes. Cook is constantly changing and adapting to continuously offer new technologies, and PillSense is the latest addition to Cook’s comprehensive portfolio of GI bleed management solutions

- In May 2024, Cook Medical entered into a U.S. distribution agreement with EnteraSense to offer the PillSense system. This swallowable capsule detects upper gastrointestinal bleeding (UGIB) and transmits data wirelessly to a receiver. FDAapproved in February 2023, PillSense enables rapid diagnosis and triage of patients with suspected UGIB, potentially reducing the need for more invasive procedures

As per Data Bridge Market Research analysis:

Geographically, the countries covered in the global Endoscopic Hemostasis Market report are North America, Euorpe, Asia-Pacific, Middle East and Africa, South America. The North America is further segmented into U.S., Canada, and Mexico. Europe is further segmented into Germany, U.K., France, Italy, Spain, Russia, Turkey, Netherlands, Norway, Finland, Denmark, Sweden, Poland, Switzerland, Belgium, and rest of Europe. The Asia-Pacific is further segmented into China, Japan, India, South Korea, Australia, Indonesia, Thailand, Malaysia, Singapore, Philippines, New Zealand, and rest of Asia-Pacific. The South America is further segmented into Brazil, Argentina, and rest of South America. The Middle East and Africa is further segmented into Saudi Arabia, U.A.E., South Africa, Egypt, Israel, Rest of Middle East and Africa.

North America Endoscopic Hemostasis Market Insight

The North America Endoscopic Hemostasis Market is gaining strong traction due to the country’s high volume of gastrointestinal endoscopic procedures and early adoption of advanced therapeutic endoscopy techniques. North America hospitals and specialty clinics place strong emphasis on clinical precision, procedural reliability, and evidence-based device selection, driving consistent demand for high-performance mechanical and energy-based hemostasis solutions. In addition, the presence of leading medical device manufacturers, well-established clinical training programs, and strict regulatory and quality standards is fostering rapid uptake of technologically advanced hemostasis devices. North America focus on procedural standardization, patient safety, and outcome optimization reinforces its position as a technology-led and innovation-driven market within Global.

Asia-Pacific Endoscopic Hemostasis Market Insight

The Asia-Pacific Endoscopic Hemostasis Market continues to expand as healthcare providers prioritize minimally invasive treatment pathways, efficiency in endoscopy units, and reduction of procedure-related complications. Rising incidence of gastrointestinal bleeding conditions, combined with increasing demand on NHS endoscopy services, is accelerating adoption of cost-effective, easy-to-use hemostasis devices that support high procedural throughput. Strong emphasis on clinical guidelines, value-based care, and standardized treatment protocols is shaping purchasing decisions, while growing use of ambulatory and day-care endoscopy settings is further supporting demand. These factors collectively position the Japan market as one driven by access, efficiency, and scalable clinical adoption rather than device manufacturing concentration.

For more detailed information about the global Endoscopic Hemostasis Market report, click here – https://www.databridgemarketresearch.com/reports/global-endoscopic-hemostasis-market