Global Cancer Care Market

Market Size in USD Billion

USD

244.40 Billion

USD

505.14 Billion

2025

2033

USD

244.40 Billion

USD

505.14 Billion

2025

2033

| 2026 - 2033 | |

| USD 244.40 Billion | |

| USD 505.14 Billion | |

| % | |

|

What is the Cancer Care Market Size and Overview?

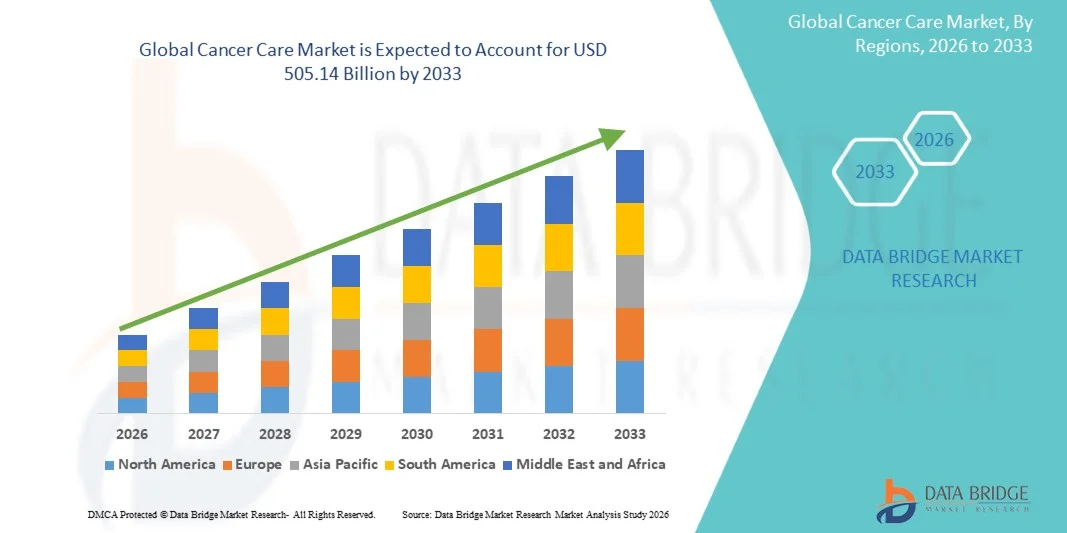

As per Data Bridge Market Research Analysis the Cancer Care Market was valued at USD 244.40 billion in 2025 and is projected to reach USD 505.14 billion by 2033, growing at a CAGR of 9.50% from 2026 to 2033. The market is experiencing consistent growth driven by the rising global cancer burden, increasing adoption of advanced oncology therapies, and growing investments in healthcare infrastructure and precision medicine technologies. Expanding access to cancer screening programs, increasing awareness regarding early cancer diagnosis, and rapid advancements in immunotherapy, targeted therapy, and radiation oncology solutions are further supporting market expansion across both developed and emerging economies.

The increasing prevalence of breast cancer, lung cancer, colorectal cancer, and other chronic oncological conditions globally, combined with rising demand for personalized treatment approaches and improved patient outcomes, is compelling hospitals, cancer research institutes, and healthcare providers to adopt advanced cancer care solutions. AI-enabled diagnostic platforms, robotic-assisted surgeries, precision oncology technologies, and integrated cancer treatment systems are increasingly replacing conventional treatment approaches in many healthcare facilities, offering improved treatment accuracy, early diagnosis, enhanced patient monitoring, and better long-term survival outcomes.

Key Market Trends & Insights

- North America dominated the Cancer Care Market with the largest revenue share of 39.24% in 2025, supported by advanced oncology infrastructure, strong adoption of precision medicine, and increasing investments in cancer research and immunotherapy development.

- The Chemotherapy segment led the market with a 34.86% share in 2025, driven by its widespread use as a primary treatment option across multiple cancer types including breast, lung, and blood cancers.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by rising cancer prevalence, expanding healthcare infrastructure, increasing healthcare expenditure, and growing access to advanced oncology treatments across China, India, and Japan.

- The Immunotherapy segment is the fastest-growing treatment type, projected to register a CAGR of 9.2%, reflecting increasing adoption of checkpoint inhibitors, CAR-T cell therapies, and personalized cancer treatment approaches globally.

- The Breast Cancer segment dominates the cancer type category with a 24.67% revenue share in 2025, led by rising global incidence, increasing awareness regarding early diagnosis, and strong adoption of targeted and hormonal therapies.

- Hospitals account for 52.14% of the market, preferred due to availability of multidisciplinary oncology care, advanced diagnostic technologies, radiation therapy infrastructure, and specialized cancer treatment services.

- The G-CSFs segment is the fastest-growing therapeutic class category, with a CAGR of 7.8%, driven by increasing use in chemotherapy-induced neutropenia management and rising adoption of supportive oncology care therapies globally.

Market Size & Forecast

- Global Market Value (2025): USD 244.40 Billion

- Expected Market Value (2033): USD 505.14 Billion

- Forecast CAGR (2026–2033): 9.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Cancer Care Market Segmentation

Attributes |

Cancer Care Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• F. Hoffmann-La Roche Ltd. (Switzerland) |

|

Market Opportunities |

· Expansion of Precision Oncology and Personalized Cancer Therapies · Rising Adoption of Immunotherapy and Cell-Based Cancer Treatments · Growth of Tele-Oncology and Digital Cancer Care Solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

What is the Key Trend in the Cancer Care Market?

Trend: Rising Adoption of Precision Oncology and AI-Enabled Cancer Care

Healthcare providers and oncology companies are increasingly adopting AI-powered diagnostics, precision medicine, and personalized cancer therapies to improve treatment outcomes and patient survival rates. Advanced genomic sequencing, biomarker testing, and AI-assisted imaging platforms are enabling clinicians to identify cancer mutations more accurately and deliver targeted treatment strategies. In addition, the growing adoption of immunotherapy, CAR-T cell therapy, and robotic-assisted oncology procedures is transforming cancer management across hospitals and specialty cancer centers globally.

For instance, in March 2024, Tempus AI, Inc. expanded its AI-enabled oncology platform to support precision diagnostics and personalized treatment recommendations for multiple cancer indications. Similarly, in 2024, F. Hoffmann-La Roche Ltd. strengthened its oncology diagnostics portfolio through advancements in companion diagnostic technologies supporting targeted cancer therapies. Increasing integration of digital pathology and cloud-based oncology analytics platforms across U.S. and Germany is further accelerating adoption of data-driven cancer care solutions.

Cancer Care Market Dynamics

Key Market Driver: Rising Global Cancer Burden and Increasing Demand for Advanced Oncology Treatments

The increasing prevalence of cancer worldwide is a major factor driving demand for cancer care solutions across diagnosis, treatment, and supportive care services. Rising incidence of breast cancer, lung cancer, colorectal cancer, and blood cancer, combined with aging populations and unhealthy lifestyle factors, is significantly expanding the global oncology patient pool. According to the World Health Organization, cancer remains one of the leading causes of death globally, accounting for nearly 10 million deaths annually.

Hospitals, cancer centers, and healthcare providers are increasingly investing in advanced oncology therapies including immunotherapy, targeted therapy, radiation oncology, and minimally invasive surgical technologies to improve patient outcomes and survival rates. In addition, increasing government initiatives for early cancer screening, reimbursement support, and cancer awareness programs across countries such as United States, Japan, and Germany are accelerating adoption of advanced cancer care solutions globally.

Key Restraint/Challenge: High Cost of Advanced Cancer Treatments and Limited Accessibility

A significant challenge in the Cancer Care Market is the high cost associated with advanced oncology therapies, precision diagnostics, and long-term treatment management. Immunotherapies, targeted biologics, CAR-T cell therapies, and personalized oncology treatments often require substantial financial investment, limiting accessibility for patients in low- and middle-income countries. In addition, expenses related to hospitalization, radiation therapy, chemotherapy cycles, and supportive care significantly increase the overall treatment burden.

For instance, certain CAR-T cell therapies and immuno-oncology treatments can cost several hundred thousand dollars per patient in developed healthcare markets. Furthermore, limited oncology infrastructure, shortage of trained oncologists, and unequal access to advanced cancer diagnostics across rural regions in India, Brazil, and parts of Africa continue to create major barriers for early diagnosis and treatment adoption.

Key Market Opportunity: Expansion of Digital Oncology, Telemedicine, and Personalized Cancer Care

The increasing integration of digital health technologies into oncology care is creating strong growth opportunities for cancer care providers and pharmaceutical companies globally. AI-powered diagnostic imaging, tele-oncology consultations, wearable patient monitoring systems, and cloud-based cancer management platforms are helping healthcare providers improve treatment efficiency, patient engagement, and long-term disease monitoring.

The growing focus on precision medicine and biomarker-based therapies is further supporting development of personalized oncology treatment models. In 2024, GE HealthCare Technologies Inc. expanded its AI-enabled oncology imaging and diagnostic solutions designed to improve cancer detection and treatment planning workflows. Similarly, several healthcare systems across China and India are increasingly investing in tele-oncology infrastructure to improve access to cancer specialists in underserved regions. Rising healthcare digitization and expanding oncology research investments are expected to further accelerate the adoption of integrated and personalized cancer care solutions globally.

Cancer Care Market Scope

The Cancer Care market is segmented on the basis of treatment type, cancer type, end user, and therapeutic class.

By Treatment Type

On the basis of treatment type, the Cancer Care Market is segmented into chemotherapy, targeted therapy, immunotherapy, hormonal therapy, and other treatment types. The Chemotherapy segment dominated the market with a share of 34.86% in 2025 due to its widespread use as a first-line treatment across multiple cancer indications including breast cancer, lung cancer, blood cancer, and gastrointestinal cancers. High adoption is supported by increasing global cancer incidence, broad availability of chemotherapeutic drugs, and strong integration into combination treatment regimens. In addition, growing healthcare infrastructure, rising oncology patient admissions, and increasing government support for cancer treatment programs are reinforcing the dominance of this segment. Chemotherapy continues to play a critical role in both curative and palliative cancer management across hospitals and oncology centers globally. The availability of generic chemotherapy drugs and expanding reimbursement coverage across developed economies are further accelerating market penetration. Moreover, increasing use of chemotherapy alongside radiation therapy and immunotherapy is supporting treatment effectiveness and improving patient outcomes across advanced-stage cancers worldwide.

The Immunotherapy segment is expected to witness the fastest CAGR of 9.2% from 2026 to 2033, driven by increasing adoption of immune checkpoint inhibitors, CAR-T cell therapies, monoclonal antibodies, and cancer vaccines across multiple oncology applications. Rising success rates of immuno-oncology therapies in treating lung cancer, melanoma, blood cancer, and colorectal cancer are significantly driving segment growth. In addition, increasing FDA approvals, expanding oncology clinical trials, and rising investments by pharmaceutical companies in next-generation immunotherapies are accelerating market expansion. Healthcare providers are increasingly integrating immunotherapy into precision oncology programs due to improved survival rates and reduced long-term toxicity compared to traditional therapies. Furthermore, advancements in biomarker testing, genomic profiling, and personalized medicine approaches are improving patient selection and treatment response, further strengthening growth opportunities for the immunotherapy segment globally.

By Cancer Type

On the basis of cancer type, the Cancer Care Market is segmented into blood cancer, breast cancer, prostate cancer, gastrointestinal cancer, gynecologic cancer, respiratory/lung cancer, and other cancer types. The Breast Cancer segment dominated the market with a share of 24.67% in 2025 due to the rising prevalence of breast cancer globally and increasing awareness regarding early diagnosis and treatment. Strong adoption of targeted therapies, hormonal therapies, chemotherapy, and immunotherapy across breast cancer treatment programs is supporting segment dominance. In addition, growing implementation of mammography screening initiatives, expanding access to oncology care, and rising healthcare expenditure across developed and emerging markets are accelerating treatment adoption. Pharmaceutical companies are increasingly investing in HER2-targeted therapies and personalized oncology solutions to improve patient survival outcomes. Moreover, increasing government-led awareness campaigns, rising female aging population, and strong presence of specialized breast cancer treatment centers continue to strengthen the segment’s leading position in the Cancer Care Market.

The Respiratory/Lung Cancer segment is expected to witness the fastest CAGR of 8.8% from 2026 to 2033, driven by the increasing global burden of lung cancer associated with smoking, air pollution, occupational exposure, and lifestyle-related risk factors. Rising adoption of precision diagnostics, immunotherapy, and targeted therapies for non-small cell lung cancer (NSCLC) is significantly supporting segment growth. In addition, increasing investments in AI-enabled imaging technologies, liquid biopsy diagnostics, and personalized treatment approaches are improving early detection and treatment efficiency. Pharmaceutical companies are expanding oncology pipelines focused on EGFR inhibitors, PD-1 inhibitors, and advanced biologics for lung cancer management. Furthermore, growing adoption of minimally invasive surgeries, robotic-assisted thoracic procedures, and radiation oncology technologies is enhancing clinical outcomes and accelerating expansion of the respiratory/lung cancer segment globally.

By End User

On the basis of end user, the Cancer Care Market is segmented into hospitals, specialty clinics, and cancer & radiation therapy centers. The Hospitals segment dominated the market with a share of 52.14% in 2025 due to the availability of comprehensive oncology infrastructure, multidisciplinary treatment capabilities, and access to advanced diagnostic and therapeutic technologies. Hospitals continue to serve as primary centers for chemotherapy, immunotherapy, radiation therapy, oncology surgery, and supportive cancer care services globally. High patient inflow, increasing cancer hospitalization rates, and strong integration of precision diagnostics and imaging technologies are driving segment dominance. In addition, expanding investments in oncology departments, specialized cancer units, and robotic-assisted surgical platforms are improving treatment accessibility and patient outcomes. The presence of experienced oncologists, radiation specialists, and advanced pathology laboratories further reinforces the leading position of hospitals in the Cancer Care Market.

The Cancer & Radiation Therapy Centers segment is projected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by increasing demand for specialized oncology treatment facilities and advanced radiation therapy technologies. Rising adoption of proton therapy, stereotactic radiosurgery, intensity-modulated radiation therapy (IMRT), and precision oncology solutions is accelerating segment expansion. In addition, growing preference for outpatient cancer treatment services, shorter treatment cycles, and cost-effective specialized oncology care is supporting market growth. Governments and private healthcare organizations are increasingly investing in dedicated cancer treatment centers to improve access to advanced oncology therapies. Furthermore, increasing collaborations between cancer research institutes and radiation therapy providers are enhancing innovation, clinical trial participation, and personalized cancer treatment capabilities globally.

By Therapeutic Class

On the basis of therapeutic class, the Cancer Care Market is segmented into G-CSFs, bisphosphonates, antiemetic, opioids, NSAIDs, and ESAs. The Antiemetic segment dominated the market with a share of 28.43% in 2025 due to the widespread use of antiemetic drugs for managing chemotherapy-induced nausea and vomiting (CINV) among cancer patients. Increasing chemotherapy adoption across hospitals and oncology clinics, along with rising emphasis on supportive cancer care and patient quality of life, is significantly driving segment demand. Healthcare providers are increasingly integrating serotonin antagonists, NK1 receptor antagonists, and corticosteroid-based antiemetic therapies into oncology treatment protocols to improve patient comfort and treatment adherence. In addition, rising awareness regarding supportive oncology care and growing availability of advanced antiemetic formulations are supporting market expansion. The increasing incidence of cancer worldwide and higher chemotherapy utilization rates continue to reinforce the segment’s dominant market position globally.

The G-CSFs segment is expected to witness the fastest CAGR of 7.8% from 2026 to 2033, driven by increasing use in managing chemotherapy-induced neutropenia and reducing infection-related complications among oncology patients. Growing adoption of biosimilar G-CSFs, rising cancer treatment volumes, and expanding supportive oncology care programs are significantly supporting segment growth. In addition, increasing focus on improving chemotherapy adherence, reducing hospitalization rates, and enhancing patient recovery outcomes is accelerating demand for granulocyte colony-stimulating factor therapies. Pharmaceutical companies are increasingly investing in long-acting G-CSF formulations and biosimilar development to improve accessibility and treatment affordability. Furthermore, rising adoption of combination cancer therapies and expanding oncology treatment infrastructure across emerging healthcare markets are expected to further strengthen growth opportunities for the G-CSFs segment globally.

Cancer Care Market Regional Analysis

North America dominated the Cancer Care market and accounted for the largest revenue share of 39.24% in 2025, supported by advanced oncology infrastructure, strong adoption of precision medicine, and increasing investments in cancer research and immunotherapy development. The region also benefits from favorable reimbursement frameworks, high availability of targeted therapies, and strong presence of leading pharmaceutical and biotechnology companies. Increasing clinical trial activity, rising adoption of AI-assisted diagnostics, and growing demand for personalized cancer treatment solutions continue to strengthen North America’s leadership position in the global market.

U.S. Cancer Care Market Insight

The U.S. Cancer Care market is witnessing strong growth due to rising cancer prevalence, increasing adoption of immunotherapies and targeted therapies, and substantial investments in oncology research and precision medicine. The country’s advanced healthcare infrastructure, strong presence of leading cancer treatment centers, and high utilization of AI-enabled diagnostics are driving demand across hospitals, specialty clinics, and research institutions. In addition, increasing FDA approvals for novel oncology drugs and growing focus on early cancer detection are accelerating market expansion across the United States.

Europe Cancer Care Market Insight

The Europe Cancer Care market remains a major contributor to global revenue, driven by increasing government support for cancer screening programs, rising adoption of advanced oncology therapeutics, and strong healthcare infrastructure. The widespread use of radiotherapy, targeted therapies, and immuno-oncology treatments across countries such as Germany, France, and the U.K. is supporting market expansion throughout the region. In addition, increasing investments in precision oncology, growing clinical research activities, and rising awareness regarding early cancer diagnosis continue to enhance adoption of advanced cancer care solutions across Europe.

U.K. Cancer Care Market Insight

The U.K. Cancer Care market is experiencing steady growth, supported by increasing government initiatives for cancer awareness, rising investments in precision medicine, and expanding access to advanced oncology therapies. Growing adoption of immunotherapy, radiotherapy, and AI-assisted cancer diagnostics is improving treatment outcomes and accelerating market growth. Furthermore, strong collaborations between research institutes, pharmaceutical companies, and the National Health Service (NHS) are supporting innovation in cancer treatment and patient care management across the U.K.

Germany Cancer Care Market Insight

The Germany Cancer Care market is expanding steadily due to the country’s advanced healthcare infrastructure, strong pharmaceutical manufacturing capabilities, and increasing adoption of innovative oncology treatments. Hospitals and cancer research centers are increasingly utilizing precision medicine, genomic testing, and targeted therapies for personalized cancer management. Continuous advancements in radiotherapy systems, immuno-oncology drugs, and digital pathology technologies, along with rising investments in cancer research, are further driving market growth in Germany.

Asia-Pacific Cancer Care Market Insight

The Asia-Pacific Cancer Care market is expected to witness rapid growth, driven by rising cancer prevalence, expanding healthcare infrastructure, and increasing healthcare expenditure across countries such as China, India, and Japan. Growing awareness regarding early cancer diagnosis, increasing adoption of advanced oncology therapeutics, and improving access to cancer treatment services are supporting regional market expansion. In addition, rising government initiatives for cancer screening, growing pharmaceutical investments, and increasing availability of targeted therapies and immunotherapies are accelerating market growth across Asia-Pacific.

Japan Cancer Care Market Insight

The Japan Cancer Care market is witnessing consistent growth due to rising investments in oncology research, increasing adoption of minimally invasive cancer treatments, and strong government support for precision medicine initiatives. Hospitals and research institutes are increasingly utilizing advanced radiotherapy systems, targeted therapies, and AI-based diagnostic technologies to improve treatment efficiency and patient outcomes. Moreover, the country’s aging population and increasing focus on early cancer detection programs are further contributing to market growth in Japan.

China Cancer Care Market Insight

The China Cancer Care market is growing rapidly, driven by rising cancer incidence, expanding healthcare infrastructure, and increasing government investments in oncology treatment and research. Growing adoption of targeted therapies, immunotherapies, and advanced diagnostic technologies across hospitals and cancer treatment centers is significantly boosting market demand. In addition, increasing healthcare expenditure, rising awareness regarding early cancer screening, and rapid expansion of domestic biopharmaceutical companies are positioning China as one of the fastest-growing markets for Cancer Care globally.

Cancer Care Market Share

The Cancer Care industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Johnson & Johnson (U.S.)

- AstraZeneca PLC (U.K.)

- Eli Lilly and Company (U.S.)

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

- GSK plc (U.K.)

- Sanofi S.A. (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Bayer AG (Germany)

- BeiGene Ltd. (China)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Seagen Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- Daiichi Sankyo Company, Limited (Japan)

Latest Developments in Cancer Care Market

- In January 2021, Bristol Myers Squibb announced that the U.S. FDA approved Opdivo (nivolumab) in combination with Cabometyx (cabozantinib) for first-line treatment of advanced renal cell carcinoma. The approval strengthened the company’s immuno-oncology portfolio and expanded the adoption of combination therapies in advanced cancer treatment

- In February 2021, EMD Serono received U.S. FDA accelerated approval for Tepmetko (tepotinib) for metastatic non-small cell lung cancer with MET exon 14 skipping alterations. The approval highlighted the growing importance of precision medicine and biomarker-driven oncology therapies in cancer care

- In September 2021, Pfizer Inc. completed the acquisition of Trillium Therapeutics to strengthen its oncology and immunotherapy pipeline focused on hematologic malignancies and CD47-targeted therapies. The acquisition reflected increasing investment in next-generation immuno-oncology platforms and cancer drug innovation

- In March 2022, Illumina, Inc. continued expansion of its oncology diagnostics capabilities following the acquisition of GRAIL, a company specializing in blood-based multi-cancer early detection technologies. The development accelerated advancements in liquid biopsy and early cancer screening solutions across global oncology markets

- In May 2022, Amgen Inc. highlighted the commercial expansion of Lumakras (sotorasib), the first KRAS inhibitor approved for non-small cell lung cancer, reflecting a major breakthrough in targeted oncology treatment for previously hard-to-treat mutations

- In August 2023, AstraZeneca PLC and Daiichi Sankyo expanded the global commercialization of Enhertu (trastuzumab deruxtecan) following increasing regulatory approvals for HER2-positive breast cancer and gastric cancer indications. The development strengthened the role of antibody-drug conjugates (ADCs) in precision oncology treatment

- In February 2024, Iovance Biotherapeutics received U.S. FDA approval for Amtagvi (lifileucel), the first tumor-infiltrating lymphocyte (TIL) therapy approved for advanced melanoma. The approval represented a significant advancement in personalized cell therapy and adoptive immunotherapy for cancer treatment

- In April 2024, Johnson & Johnson expanded oncology research collaborations focused on AI-enabled cancer diagnostics and precision oncology platforms to improve early detection and personalized treatment planning across multiple cancer types

- In October 2024, Merck & Co., Inc. continued expanding clinical applications of Keytruda (pembrolizumab) across multiple solid tumor indications, reinforcing its leadership in immuno-oncology therapies and precision cancer treatment globally. The company also advanced research into subcutaneous immunotherapy delivery systems to improve patient convenience and treatment accessibility

- In January 2025, Roche Holding AG expanded its oncology diagnostics and digital pathology portfolio through increased deployment of AI-powered cancer diagnostic solutions aimed at improving pathology workflow efficiency and precision medicine adoption in hospitals and cancer centers globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.