Global Marfan Syndrome Treatment Market

Market Size in USD Billion

USD

1.70 Billion

USD

2.87 Billion

2024

2032

USD

1.70 Billion

USD

2.87 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.70 Billion | |

| USD 2.87 Billion | |

| % | |

|

Marfan Syndrome Treatment Market Size

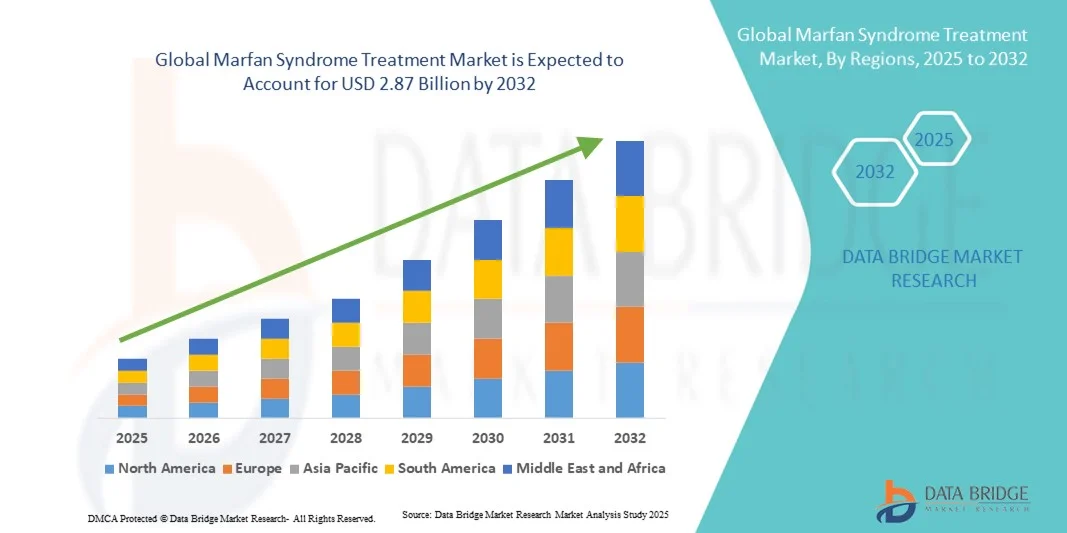

- The global Marfan Syndrome treatment market size was valued at USD 1.70 billion in 2024 and is expected to reach USD 2.87 billion by 2032, at a CAGR of 6.80% during the forecast period

- The market growth is largely fueled by the increasing prevalence of Marfan syndrome, advancements in treatment options, and rising awareness and early diagnosis among healthcare professionals and patients

- Furthermore, supportive government initiatives, multidisciplinary management approaches, and ongoing research for targeted therapies are enhancing patient outcomes and driving the adoption of Marfan syndrome treatments, thereby significantly boosting the industry's growth

Marfan Syndrome Treatment Market Analysis

- Marfan Syndrome treatment, including aortic dilation management, beta blockers, calcium channel blockers, ACE blockers, surgical interventions, bone and joint treatment, and eye treatment, are increasingly vital for improving patient outcomes and managing life-threatening cardiovascular, ocular, and skeletal complications associated with the disorder

- The escalating demand for Marfan Syndrome treatment is primarily fueled by the rising prevalence of the disorder, advancements in targeted therapies, increased awareness among healthcare professionals and patients, and early diagnosis enabling timely intervention

- North America dominated the Marfan Syndrome treatment market with the largest revenue share of 42.5% in 2024, characterized by advanced healthcare infrastructure, high treatment adoption rates, and a strong presence of key pharmaceutical and biotech companies focusing on innovative therapies and comprehensive care programs

- Asia-Pacific is expected to be the fastest growing region in the Marfan Syndrome treatment market during the forecast period, due to improving healthcare facilities, increasing awareness, and growing accessibility to specialized treatments in countries such as India and China

- Beta blockers dominated the Marfan Syndrome treatment market with a market share of 46.7% in 2024, driven by their widespread use in managing cardiovascular complications and improving patient prognosis

Report Scope and Marfan Syndrome Treatment Market Segmentation

|

Attributes |

Marfan Syndrome Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Marfan Syndrome Treatment Market Trends

Advancements in Targeted and Gene-Based Therapies

- A significant and accelerating trend in the Marfan syndrome treatment market is the development and adoption of targeted therapies and gene-based interventions, aimed at improving cardiovascular and skeletal outcomes

- For instance, ongoing clinical research on TGF-β signaling modulators is demonstrating potential in slowing aortic root dilation and improving long-term prognosis in patients

- Precision medicine approaches enable personalized treatment plans based on genetic profiling, optimizing drug efficacy and minimizing adverse effects, thereby enhancing overall patient management

- The integration of advanced diagnostics with targeted treatment protocols facilitates early intervention, enabling clinicians to tailor therapy based on disease severity and risk factors

- This trend towards personalized, gene-informed, and targeted treatment strategies is reshaping expectations for Marfan syndrome management, with companies such as CycloMedica focusing on innovative therapeutic solutions

- The demand for more effective and individualized Marfan syndrome treatments is growing rapidly across both pediatric and adult patient populations, as healthcare providers seek better long-term outcomes

Marfan Syndrome Treatment Market Dynamics

Driver

Rising Prevalence and Awareness Driving Treatment Adoption

- The increasing prevalence of Marfan syndrome, coupled with rising awareness among healthcare professionals and patients, is a significant driver for the heightened demand for effective treatment options

- For instance, improved screening programs and early diagnostic initiatives in North America and Europe have led to timely identification of patients at risk, increasing treatment uptake

- As patients and caregivers become more knowledgeable about the disease’s complications, the demand for comprehensive management, including medications and surgical interventions, rises steadily

- Furthermore, increasing investments in healthcare infrastructure and specialty clinics focused on connective tissue disorders are enhancing access to Marfan syndrome treatments

- The availability of multidisciplinary care involving cardiologists, geneticists, ophthalmologists, and orthopedic specialists further propels adoption, offering holistic management strategies

- Growing patient advocacy, awareness campaigns, and support networks are encouraging early treatment initiation, thereby boosting market growth across regions

Restraint/Challenge

High Treatment Costs and Limited Access in Emerging Regions

- The relatively high cost of advanced Marfan syndrome treatments, including medications, surgeries, and monitoring, poses a challenge for widespread market adoption, particularly in emerging regions

- For instance, the expense associated with aortic root replacement surgery or long-term use of beta blockers and ACE inhibitors may limit access for patients in low- and middle-income countries

- Limited availability of specialized healthcare facilities and trained clinicians in certain regions can delay diagnosis and treatment initiation, impacting overall patient outcomes

- Variability in healthcare reimbursement policies and insurance coverage across countries can hinder patient access to optimal treatment protocols

- In addition, the need for lifelong management and regular monitoring increases the overall treatment burden, which can discourage adherence and consistent care

- Overcoming these challenges through government support, subsidized treatment programs, and expansion of specialty care centers will be critical for sustained market growth

Marfan Syndrome Treatment Market Scope

The market is segmented on the basis of treatment type, route of administration, end-users, and distribution channel.

- By Treatment Type

On the basis of treatment type, the Marfan syndrome treatment market is segmented into aortic dilation, beta blocker, calcium channel blocker, ACE blocker, surgery, bone and joints treatment, eye treatment, and others. The beta blocker segment dominated the market with the largest revenue share of 46.7% in 2024, driven by its effectiveness in managing cardiovascular complications, particularly aortic root dilation, which is a life-threatening aspect of Marfan syndrome. Beta blockers are widely prescribed due to their proven safety profile and long-term benefits in reducing cardiac events. Healthcare providers often prioritize beta blockers for both pediatric and adult patients, leading to consistently high adoption rates. The segment also benefits from broad insurance coverage in key regions, making treatment accessible to a larger patient population. Furthermore, beta blockers are available in multiple formulations, enhancing compliance and convenience for patients requiring lifelong therapy. Their established clinical efficacy and widespread physician trust reinforce the dominance of this segment.

The surgery segment is anticipated to witness the fastest growth rate of 7.3% from 2025 to 2032, fueled by increasing adoption of advanced surgical techniques such as valve-sparing aortic root replacement and minimally invasive procedures. Surgical interventions are essential for patients with severe aortic complications, and growing awareness of timely intervention is driving demand. Technological advancements in surgical tools and postoperative care are reducing recovery times and improving outcomes. Hospitals and specialty cardiac centers are investing in training and infrastructure to support complex Marfan-related surgeries. Rising patient willingness to undergo early surgical procedures to prevent life-threatening complications further propels market growth. In addition, favorable reimbursement policies in developed countries encourage the adoption of surgical treatments, contributing to the segment’s rapid expansion.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The oral segment dominated the market in 2024 with a revenue share of 51.2%, driven by the widespread prescription of beta blockers, ACE inhibitors, and calcium channel blockers in oral form. Oral medications provide convenience for long-term daily therapy and are easily administered at home, improving patient adherence. Physicians often prefer oral therapy for chronic management due to ease of dosing and minimal invasiveness. Oral formulations are readily available across retail and hospital pharmacies, ensuring consistent patient access. The familiarity and acceptability of oral medications among patients further reinforce the segment’s dominance. In addition, oral route allows for titration and combination therapy, enhancing individualized treatment plans.

The parenteral segment is expected to witness the fastest CAGR of 6.9% from 2025 to 2032, driven by hospital-administered therapies for acute complications and perioperative management during surgical procedures. Parenteral administration ensures rapid drug action, which is critical in emergency situations or severe cardiovascular events. Advanced hospital infrastructure and increasing hospital admissions for complex Marfan cases support the growth of this segment. Innovations in IV formulations and injectable therapies are also improving patient safety and treatment outcomes. Growing awareness of hospital-based interventions for critical Marfan complications is accelerating adoption. Parenteral treatments are essential for high-risk patients, driving continued expansion of this segment.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, homecare, and others. The hospitals segment dominated the market in 2024 with a share of 44.8%, due to the high prevalence of specialized care and advanced cardiovascular facilities required for managing Marfan syndrome patients. Hospitals offer multidisciplinary teams, including cardiologists, geneticists, and orthopedic specialists, enabling comprehensive treatment. Availability of surgical infrastructure and inpatient monitoring further enhances the hospital segment’s dominance. Large-scale hospital networks and referral systems facilitate access for patients from remote regions. Hospitals also provide education and support programs, improving patient adherence and outcomes. The complexity of Marfan syndrome management necessitates hospital-based care, reinforcing the segment’s leading position.

The homecare segment is expected to witness the fastest growth rate of 8.1% from 2025 to 2032, driven by increasing adoption of remote monitoring, telemedicine consultations, and at-home administration of medications for stable patients. Homecare solutions improve patient convenience, reduce hospital visits, and support long-term adherence. Advances in wearable devices and mobile health apps enable continuous tracking of cardiovascular parameters. Patient preference for home-based management and supportive care services is rising globally. Homecare also helps reduce overall healthcare costs, driving its adoption among insurers and providers. The convenience and personalized care provided by home-based interventions are key factors for rapid segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment dominated the market in 2024 with a revenue share of 45.6%, due to the direct availability of prescribed medications during hospital visits and integrated care services. Hospital pharmacies ensure consistent supply and quality control of critical Marfan syndrome treatments. Patients undergoing surgery or acute care rely heavily on hospital pharmacies for immediate access. Close coordination between hospital pharmacies and treating physicians facilitates treatment adherence and monitoring. Bulk procurement and insurance coverage also strengthen hospital pharmacy dominance. The established trust and convenience associated with hospital pharmacies reinforce this segment’s leading market position.

The online pharmacy segment is expected to witness the fastest CAGR of 9.4% from 2025 to 2032, driven by increasing digital adoption, e-commerce penetration, and preference for home delivery of chronic medications. Online platforms offer convenience, subscription services, and discreet delivery for patients requiring long-term therapy. Telehealth integration and e-prescriptions further enhance accessibility. Rising smartphone usage and digital literacy support rapid growth of online pharmacies. Competitive pricing and promotional offers on online channels also attract patients seeking cost-effective solutions. The ease of ordering and home delivery ensures sustained expansion of this segment globally.

Marfan Syndrome Treatment Market Regional Analysis

- North America dominated the Marfan Syndrome treatment market with the largest revenue share of 42.5% in 2024, characterized by advanced healthcare infrastructure, high treatment adoption rates, and a strong presence of key pharmaceutical and biotech companies focusing on innovative therapies and comprehensive care programs

- Patients and clinicians in the region highly value access to specialized care, multidisciplinary management, and innovative therapies, including beta blockers, ACE inhibitors, and surgical interventions, which significantly improve long-term outcomes

- This widespread adoption is further supported by well-established healthcare facilities, strong insurance coverage, and government initiatives promoting early screening and treatment, establishing North America as the leading market for Marfan syndrome therapies in both pediatric and adult populations

U.S. Marfan Syndrome Treatment Market Insight

The U.S. Marfan syndrome treatment market captured the largest revenue share of 38% in 2024 within North America, fueled by advanced healthcare infrastructure, high awareness among clinicians, and widespread adoption of both pharmacological and surgical interventions. Patients and healthcare providers increasingly prioritize early diagnosis, continuous monitoring, and comprehensive management of cardiovascular and skeletal complications. The growing availability of multidisciplinary Marfan centers, combined with strong insurance coverage and government-supported screening programs, further propels the market. Moreover, ongoing clinical trials and innovative therapies for aortic dilation and related complications are significantly contributing to market expansion.

Europe Marfan Syndrome Treatment Market Insight

The Europe Marfan syndrome treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence, early screening initiatives, and the rising adoption of advanced therapies. The emphasis on patient safety and structured clinical management in hospitals and specialty clinics fosters the use of medications and surgical interventions. European patients are also drawn to comprehensive, multidisciplinary care approaches that address cardiovascular, ocular, and skeletal manifestations. The region is experiencing significant growth across hospital and homecare settings, with treatments increasingly incorporated into both routine management and specialized surgical programs.

U.K. Marfan Syndrome Treatment Market Insight

The U.K. Marfan syndrome treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness among healthcare professionals and patients, alongside government-led screening programs. Concerns regarding aortic complications and early intervention encourage both clinicians and patients to adopt pharmacological and surgical solutions promptly. The U.K.’s strong healthcare system, robust hospital network, and integration of specialized Marfan clinics are expected to continue stimulating market growth. In addition, increasing patient advocacy and support programs for rare genetic disorders are boosting demand for treatment accessibility.

Germany Marfan Syndrome Treatment Market Insight

The Germany Marfan syndrome treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced medical infrastructure, technological adoption, and increasing focus on rare disease management. Germany’s emphasis on preventive care, innovation in surgical techniques, and multidisciplinary patient management promotes treatment adoption. Hospitals and specialty clinics are integrating pharmacological and surgical care, ensuring comprehensive treatment of cardiovascular and skeletal complications. Patient preference for high-quality care and adherence to guideline-based management further strengthens market growth in Germany.

Asia-Pacific Marfan Syndrome Treatment Market Insight

The Asia-Pacific Marfan syndrome treatment market is poised to grow at the fastest CAGR of 9.5% during the forecast period of 2025 to 2032, driven by increasing urbanization, rising healthcare expenditure, and improving access to specialized care in countries such as China, India, and Japan. The region’s growing awareness of rare genetic disorders, combined with government initiatives supporting early diagnosis and treatment, is accelerating adoption. Furthermore, the expansion of hospital networks, telemedicine, and homecare solutions is improving treatment accessibility. Increasing affordability of medications and surgical procedures is also contributing to the region’s rapid growth.

Japan Marfan Syndrome Treatment Market Insight

The Japan Marfan syndrome treatment market is gaining momentum due to the country’s advanced healthcare system, high patient awareness, and demand for comprehensive care. Japanese patients place a strong emphasis on early intervention, multidisciplinary management, and long-term monitoring of cardiovascular and skeletal complications. The integration of genetic testing, specialized Marfan clinics, and advanced surgical procedures is fueling growth. In addition, the aging population and rising adoption of personalized medicine approaches are expected to spur demand for effective and convenient treatment options in both hospital and homecare settings.

India Marfan Syndrome Treatment Market Insight

The India Marfan syndrome treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to increasing awareness, growing healthcare infrastructure, and rising availability of specialized Marfan clinics. India’s expanding middle class and improved access to medications and surgical interventions are driving market growth. Early diagnosis initiatives, government-supported rare disease programs, and adoption of telemedicine solutions are enhancing treatment accessibility. Moreover, the availability of cost-effective therapies, alongside increasing patient education, is boosting adoption across hospitals, clinics, and homecare settings in India.

Marfan Syndrome Treatment Market Share

The Marfan Syndrome Treatment industry is primarily led by well-established companies, including:

- Mesa Associates, Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Aurobindo Pharma Limited (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Lupin (U.S.)

- AdvaCare Pharma (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- MEDICHEM SA (Spain)

- Changzhou Pharmaceutical Factory (China)

- Qualitek Pharma (U.S.)

- Alvogen (U.S.)

- Ipca Laboratories Ltd (India)

- Wockhardt (India)

- Farmhispania Group (Spain)

- Hanways Chempharm Co., Limited (China)

- Sneha MediCare (India)

- Glenmark Pharmaceuticals Inc. (U.S.)

- Novartis AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

What are the Recent Developments in Global Marfan Syndrome Treatment Market?

- In August 2025, The GenTAC Alliance, a collaborative effort in aortic disease research, was restructured and renamed as the Genetic Aortic Network, a division of the Marfan Foundation. This transition aims to enhance global scientific collaboration and focus on genetic aortic diseases, including Marfan syndrome, to improve patient outcomes through research and clinical advancements

- In July 2025, Researchers identified 20 previously unknown genetic variations in the FBN1 gene, which is responsible for Marfan syndrome. This discovery enhances the understanding of the genetic basis of the disorder and may lead to more accurate diagnostic tools and targeted therapies in the future

- In June 2025, Recent studies have provided new insights into the management of thoracic aortic aneurysms in Marfan syndrome patients, emphasizing the importance of early detection and personalized treatment strategies. These findings aim to improve long-term cardiovascular health and reduce complications associated with the condition

- In May 2025, The European Medicines Agency (EMA) designated allopurinol as the first orphan drug for Marfan syndrome, recognizing its potential to treat this rare connective tissue disorder. Allopurinol, traditionally used for gout, is now being explored for its efficacy in managing aortic aneurysms associated with Marfan syndrome. This designation provides incentives for further clinical development and accessibility

- In October 2024, The Marfan Trust hosted the Marfan Information Day 2024, featuring expert discussions on the manifestations of Marfan and Loeys-Dietz syndromes, including chronic pain, aortic disease, and new research into improved treatments. The event also emphasized the importance of self-advocacy for patients and families affected by these conditions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.