Global Pfeiffer Syndrome Market

Market Size in USD Million

USD

750.50 Million

USD

1,100.41 Million

2024

2032

USD

750.50 Million

USD

1,100.41 Million

2024

2032

| 2025 - 2032 | |

| USD 750.50 Million | |

| USD 1,100.41 Million | |

| % | |

|

Pfeiffer Syndrome Market Size

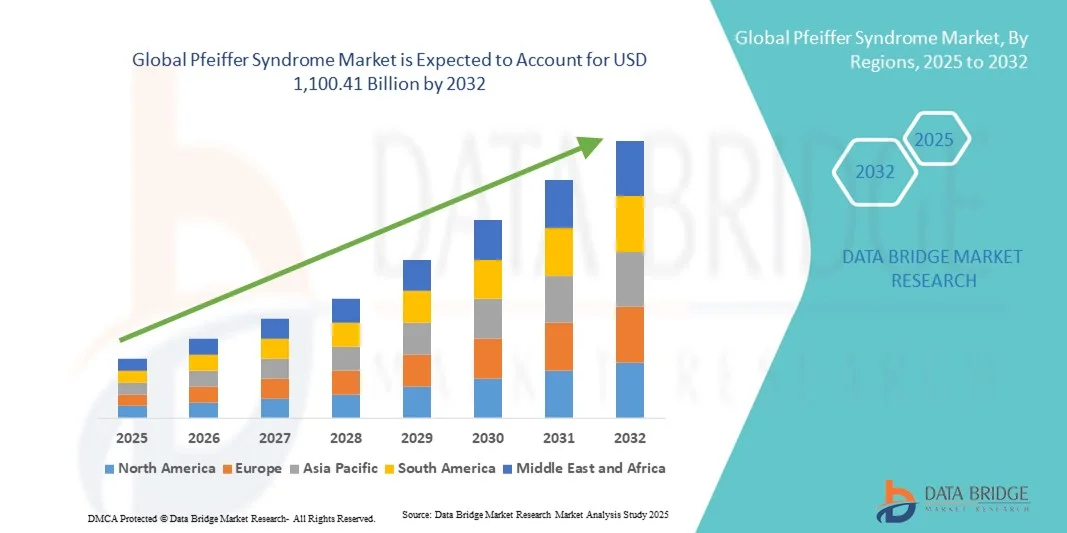

- The global Pfeiffer Syndrome market size was valued at USD 750.50 million in 2024 and is expected to reach USD 1,100.41 billion by 2032, at a CAGR of 4.90% during the forecast period

- The market growth is primarily driven by increasing awareness, advancements in genetic testing, and growing availability of targeted therapies for rare congenital disorders, including craniosynostosis syndromes such as Pfeiffer syndrome

- In addition, expanding research on fibroblast growth factor receptor (FGFR) mutations, improved diagnostic infrastructure, and rising healthcare expenditure are fostering earlier detection and intervention. These collective factors are propelling the demand for innovative treatment options, thereby significantly boosting the industry's growth

Pfeiffer Syndrome Market Analysis

- Pfeiffer Syndrome, a rare genetic disorder characterized by premature fusion of skull bones (craniosynostosis) and limb abnormalities, is increasingly drawing attention within the rare disease and genetic therapy landscape due to rising diagnostic awareness and advancements in genomic medicine

- The growing demand for effective treatment options is primarily fueled by improvements in molecular diagnostics, expanding research on FGFR gene mutations, and greater access to specialized craniofacial surgery and supportive care services

- North America dominated the Pfeiffer Syndrome market with the largest revenue share of 41.6% in 2024, supported by strong genetic research infrastructure, well-established healthcare systems, and the presence of leading academic and biotechnology institutions driving innovation in rare disease therapeutics

- Asia-Pacific is expected to be the fastest-growing region in the Pfeiffer Syndrome market during the forecast period, driven by improving healthcare access, growing government initiatives for rare disease management, and rising awareness among clinicians and parents

- The Pfeiffer syndrome type I segment dominated the Pfeiffer Syndrome market with a market share of 47.1% in 2024, attributed to its higher prevalence, earlier diagnosis rates, and broader availability of surgical and supportive treatment options compared to the more severe subtypes

Report Scope and Pfeiffer Syndrome Market Segmentation

|

Attributes |

Pfeiffer Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Pfeiffer Syndrome Market Trends

Advancements in Gene-Targeted Therapies and Personalized Treatment Approaches

- A significant and accelerating trend in the global Pfeiffer syndrome market is the growing focus on precision medicine and gene-targeted therapies aimed at addressing FGFR gene mutations responsible for the condition. This shift toward molecular-level treatment is transforming how rare craniofacial disorders are managed globally

- For instance, research institutions and biotech firms are increasingly exploring FGFR inhibitors and gene-editing technologies to correct or mitigate the underlying genetic abnormalities, offering hope for long-term disease modification. Similarly, academic collaborations are fostering innovation in gene-based therapeutic models to improve patient outcomes

- Integration of genetic research with advanced imaging technologies enables early diagnosis, surgical planning, and personalized care, reducing complications and improving craniofacial reconstruction accuracy. For instance, AI-assisted craniofacial modeling is now being utilized to simulate surgical outcomes and enhance procedural success rates. Furthermore, genomic sequencing initiatives are improving mutation detection efficiency, leading to more targeted clinical interventions

- The convergence of genomics, digital diagnostics, and regenerative medicine is paving the way for comprehensive care approaches that combine surgical, genetic, and supportive therapies. Through a multidisciplinary interface, clinicians can manage cranial deformities, airway issues, and neurological complications more effectively

- This trend toward more targeted, predictive, and personalized healthcare solutions is fundamentally reshaping treatment expectations for rare syndromes. Consequently, companies and research centers are accelerating investment in FGFR-focused R&D programs and advanced craniofacial reconstruction technologies

- The demand for innovative, gene-based, and patient-specific treatment options is expanding rapidly across major healthcare markets, as families and clinicians increasingly prioritize long-term functional and aesthetic outcomes for affected individuals

Pfeiffer Syndrome Market Dynamics

Driver

Growing Research Focus and Expanding Genetic Testing Capabilities

- The increasing prevalence of advanced genetic testing capabilities, combined with a rising global focus on rare disease research, is a significant driver for the growing Pfeiffer syndrome market

- For instance, in May 2024, several biotech companies announced initiatives to develop FGFR-targeted therapeutic platforms, marking a crucial step in advancing personalized medicine for craniosynostosis syndromes. Such research-based strategies are expected to drive the market growth in the forecast period

- As medical communities become more aware of rare craniofacial syndromes and the role of FGFR mutations, the demand for early diagnosis and precision care continues to rise, leading to improved survival rates and treatment quality

- Furthermore, the growing adoption of genetic counseling and prenatal screening is enabling earlier identification of at-risk infants, offering families access to timely surgical and therapeutic interventions

- The increasing collaboration between hospitals, universities, and pharmaceutical firms to develop multidisciplinary care frameworks is propelling the availability of advanced reconstructive and supportive therapies worldwide

- The trend toward patient-specific interventions and precision healthcare continues to expand treatment accessibility and innovation

Restraint/Challenge

High Treatment Costs and Limited Accessibility to Specialized Care

- The high cost associated with genetic testing, reconstructive surgeries, and long-term care for Pfeiffer syndrome poses a major challenge to market expansion, particularly in developing healthcare systems

- For instance, limited insurance coverage and high procedural costs in rare disease management have restricted accessibility for many families, especially in regions with underdeveloped rare disease support infrastructure

- Addressing these financial and infrastructure barriers through improved reimbursement frameworks, government funding, and public-private partnerships is crucial to ensuring equitable access to care. Companies and NGOs are increasingly advocating for broader coverage under rare disease policies to mitigate this burden. In addition, a shortage of skilled craniofacial surgeons and limited availability of multidisciplinary treatment centers further constrain the global reach of specialized care

- While international organizations are promoting awareness and funding for rare disease treatment, unequal healthcare resources remain a significant challenge for consistent global adoption of advanced therapies

- Overcoming these challenges through cost-effective innovations, enhanced training programs, and policy-driven support for rare disease management will be essential for sustaining long-term market growth

Pfeiffer Syndrome Market Scope

The market is segmented on the basis of type, diagnosis, treatment, mode of administration, distribution channel, and end user.

- By Type

On the basis of type, the Pfeiffer syndrome market is segmented into Pfeiffer syndrome type I, Pfeiffer syndrome type II, and Pfeiffer syndrome type III. The Pfeiffer syndrome type I segment dominated the market with the largest revenue share of 47.1% in 2024, primarily due to its higher prevalence and milder clinical presentation compared to other subtypes. This form is often more responsive to surgical correction and supportive therapies, leading to improved survival rates and better quality of life. Early identification through genetic and clinical screening supports timely treatment interventions, further strengthening its market share. Hospitals and specialty centers report a higher treatment success rate for type I cases, making it the most manageable form. Furthermore, growing awareness and improved pediatric craniofacial surgery infrastructure continue to support the dominance of this segment globally.

The Pfeiffer syndrome type II segment is expected to witness the fastest growth rate during the forecast period, driven by the rising clinical research into severe craniosynostosis syndromes and improvements in neonatal intensive care. Type II presents more complex skull deformities and neurological complications, prompting increased research and innovation in surgical and genetic interventions. The adoption of AI-based cranial modeling and 3D reconstruction tools is aiding better treatment planning for these cases. For instance, academic collaborations in North America and Europe are advancing surgical precision and postoperative outcomes. In addition, growing inclusion of type II in rare disease funding programs is fueling research and treatment development, accelerating its growth in the coming years.

- By Diagnosis

On the basis of diagnosis, the market is segmented into clinical findings, molecular genetic testing for FGFR1, AND MOLECULAR GENETIC TESTING for FGFR2. The Clinical Findings segment dominated the market in 2024 as the primary approach for early identification remains based on visible craniofacial abnormalities, limb malformations, and imaging-based skull assessment. Experienced pediatric and genetic specialists often diagnose Pfeiffer syndrome at birth or early infancy through characteristic physical traits and radiological evidence. This diagnostic method is especially significant in regions with limited access to advanced molecular testing, ensuring timely intervention. The use of 3D cranial CT scans and MRI further enhances diagnostic accuracy, guiding surgical planning. In addition, clinical diagnosis remains the first line of assessment before confirming through molecular testing, maintaining its market dominance.

The Molecular Genetic Testing for FGFR2 segment is projected to grow at the fastest rate during the forecast period, owing to FGFR2 being the most commonly implicated gene mutation in Pfeiffer syndrome. Advanced genomic technologies such as next-generation sequencing (NGS) and polymerase chain reaction (PCR)-based tests are driving wider adoption of genetic diagnostics. For instance, leading genetic laboratories are expanding testing portfolios to include comprehensive FGFR mutation panels, offering greater precision. Early detection through FGFR2 testing supports genetic counseling, family planning, and prenatal screening initiatives. The increasing affordability of genetic testing and integration into newborn screening programs are expected to further accelerate the segment’s growth.

- By Treatment

On the basis of treatment, the market is segmented into surgery, drugs, physical therapy, and others. The Surgery segment dominated the market in 2024 as surgical interventions remain the cornerstone of Pfeiffer syndrome management, addressing cranial deformities and preventing neurological damage. Procedures such as cranial vault remodeling, midface advancement, and airway correction are widely performed to enhance both function and appearance. The growing adoption of minimally invasive surgical techniques and computer-assisted 3D planning has significantly improved outcomes and reduced recovery times. For instance, advanced pediatric craniofacial units in the U.S. and Europe are increasingly performing early corrective surgeries to optimize brain development. Collaborative care models involving neurosurgeons, maxillofacial experts, and pediatric anesthesiologists further strengthen the role of surgery as the dominant treatment option.

The Drugs segment is expected to experience the fastest growth over the forecast period, supported by the rise in research on targeted therapies that modulate FGFR signaling pathways. While surgery remains essential, pharmacologic approaches are emerging as complementary solutions to manage bone overgrowth and inflammation. For instance, biotech firms are investigating small molecule FGFR inhibitors for their potential to regulate abnormal bone fusion. Increased clinical trials for rare genetic craniosynostosis syndromes are expected to yield new treatment options. Furthermore, expanding access to supportive drugs such as anti-inflammatory and pain management therapies for post-surgical recovery is also driving this segment’s growth.

- By Mode of Administration

On the basis of mode of administration, the market is segmented into injectable, oral, and others. The Injectable segment dominated the market in 2024 due to its critical role in post-surgical care and experimental therapeutic delivery. Injectable formulations are often used for delivering anti-inflammatory drugs, antibiotics, and potential gene-targeted agents in controlled hospital settings. Their high bioavailability and immediate efficacy make them suitable for acute care and post-operative management. For instance, ongoing clinical studies on injectable FGFR inhibitors are demonstrating promising results in managing cranial bone overgrowth. The preference for injectable delivery in clinical trials and hospital-based therapies strengthens its dominance in the treatment landscape. In addition, hospitals’ preference for precise dosage control and medical supervision supports this segment’s continued leadership.

The Oral segment is anticipated to witness the fastest growth rate during the forecast period, fueled by the development of oral formulations of targeted drugs and supportive therapies. Oral administration offers ease of use, better patient compliance, and suitability for long-term therapy. For instance, pharmaceutical companies are focusing on developing orally available small molecules targeting FGFR-related pathways. The rising popularity of home-based rare disease management and improvements in bioavailability of oral formulations are expanding this segment’s adoption. Moreover, patients and caregivers increasingly prefer oral drugs for their safety, convenience, and reduced need for clinical visits, making this segment the most dynamic in upcoming years.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The Hospital Pharmacies segment dominated the market in 2024, as most treatment interventions, including surgical procedures and post-operative medication, are conducted in hospital settings. Hospitals remain the central hub for diagnosis, drug dispensation, and post-surgical follow-up care. Their ability to ensure the availability of specialized drugs and emergency medicines supports consistent treatment delivery. For instance, leading children’s hospitals maintain dedicated rare disease pharmacies to support multidisciplinary treatment protocols. The integration of pharmacy services with hospital information systems enhances accuracy and patient safety, further strengthening their market position. Moreover, growing hospital-based rare disease programs across North America and Europe continue to sustain this segment’s dominance.

The Online Pharmacies segment is projected to grow at the fastest rate during the forecast period, propelled by the digital transformation of healthcare delivery and growing access to specialized medications online. For instance, online pharmacy platforms are increasingly offering rare disease support medications and genetic test kits for home use. The COVID-19 pandemic accelerated digital adoption, improving convenience and access for patients in remote areas. The ability to compare prices, receive doorstep delivery, and access medical guidance online is expanding consumer trust. In addition, partnerships between online pharmacies and genetic testing providers are improving patient engagement and adherence to follow-up therapies.

- By End User

On the basis of end user, the market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment dominated the Pfeiffer syndrome market in 2024, owing to their role as the primary centers for diagnosis, complex surgical procedures, and multidisciplinary patient management. Hospitals offer integrated care involving neurosurgery, maxillofacial surgery, and intensive postoperative monitoring. For instance, tertiary hospitals in the U.S., U.K., and Japan are leading centers for craniofacial reconstruction and rare genetic disease management. The presence of genetic counseling units and neonatal care facilities also supports their market leadership. Furthermore, the availability of advanced imaging technologies and surgical navigation systems enhances treatment precision and success rates in hospital settings.

The Specialty Clinics segment is anticipated to experience the fastest growth rate during the forecast period, supported by the increasing establishment of rare disease and craniofacial specialty centers worldwide. Specialty clinics focus on personalized care, long-term rehabilitation, and follow-up management for patients with congenital syndromes. For instance, genetic and craniofacial clinics are integrating molecular testing, physiotherapy, and counseling under one roof. Their patient-centric model, shorter wait times, and tailored treatment plans are attracting more families seeking specialized attention. In addition, partnerships between clinics and research institutions are accelerating access to clinical trials and innovative therapies, fostering rapid market expansion.

Pfeiffer Syndrome Market Regional Analysis

- North America dominated the Pfeiffer Syndrome market with the largest revenue share of 41.6% in 2024, supported by strong genetic research infrastructure, well-established healthcare systems, and the presence of leading academic and biotechnology institutions driving innovation in rare disease therapeutics

- Consumers and healthcare providers in North America place high value on early diagnosis, multidisciplinary care, and access to innovative surgical and therapeutic interventions for rare congenital disorders

- This leadership is further supported by favorable reimbursement policies, significant government funding for rare disease research, and the growing involvement of patient advocacy groups promoting awareness and treatment accessibility, firmly positioning North America as the global hub for Pfeiffer syndrome management and innovation

U.S. Pfeiffer Syndrome Market Insight

The U.S. Pfeiffer syndrome market captured the largest revenue share of 82% in 2024 within North America, fueled by strong research funding and the presence of advanced genetic and craniofacial treatment facilities. The country’s well-developed healthcare infrastructure and availability of multidisciplinary care teams contribute significantly to improved diagnosis and management outcomes. Increasing adoption of next-generation sequencing (NGS) and FGFR-targeted therapies are driving early intervention strategies. Moreover, growing patient advocacy and federal support for rare disease programs are further strengthening the U.S. market landscape.

Europe Pfeiffer Syndrome Market Insight

The Europe Pfeiffer syndrome market is projected to expand at a substantial CAGR during the forecast period, driven by supportive regulatory frameworks and growing government initiatives promoting rare disease awareness and treatment. The region’s focus on specialized healthcare centers and cross-border collaboration for rare conditions is fueling diagnosis rates. Rising research investments in craniosynostosis and genetic mutation studies, combined with a growing number of clinical trials, support market growth. Increasing patient access to advanced surgical and gene-based therapies is also a key growth driver.

U.K. Pfeiffer Syndrome Market Insight

The U.K. Pfeiffer syndrome market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by advancements in precision medicine and a strong presence of leading genetic research institutions. The implementation of the Genomic Medicine Service and partnerships between the NHS and biotech firms are enhancing early genetic screening and diagnosis. Growing awareness of craniofacial syndromes, coupled with government funding for pediatric rare disease care, continues to strengthen the country’s position in this market.

Germany Pfeiffer Syndrome Market Insight

The Germany Pfeiffer syndrome market is expected to expand at a considerable CAGR during the forecast period, supported by robust healthcare infrastructure and high investment in rare disease genomics research. The nation’s emphasis on innovation, precision diagnostics, and early intervention is boosting treatment adoption. German hospitals’ growing use of 3D imaging and surgical navigation systems enhances craniofacial reconstruction outcomes. In addition, collaboration among research institutes, healthcare providers, and biotech companies is fostering steady market development.

Asia-Pacific Pfeiffer Syndrome Market Insight

The Asia-Pacific Pfeiffer syndrome market is poised to grow at the fastest CAGR of 23.7% during the forecast period of 2025 to 2032, driven by rising awareness, expanding access to specialized genetic care, and improving healthcare expenditure in countries such as China, Japan, and India. Government-led digital health and genomics initiatives are increasing diagnostic capabilities across the region. Furthermore, growing partnerships with global biotech firms and expanding medical tourism for craniofacial surgery are accelerating market expansion.

Japan Pfeiffer Syndrome Market Insight

The Japan Pfeiffer syndrome market is gaining momentum due to the nation’s advancements in regenerative medicine, 3D imaging, and precision genetic testing. High healthcare standards and increasing collaborations between universities and biotech companies are supporting the development of innovative treatment options. The country’s proactive stance on early screening and use of AI in medical imaging are further improving diagnostic accuracy and treatment planning for rare craniofacial disorders.

India Pfeiffer Syndrome Market Insight

The India Pfeiffer syndrome market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to growing investments in healthcare infrastructure, expanding genomic research capabilities, and rising awareness of rare genetic disorders. The government’s focus on rare disease policy implementation and affordable access to advanced diagnostics is driving market growth. Increasing collaborations with international research centers and domestic healthcare advancements are enabling earlier diagnosis and improved management of Pfeiffer syndrome cases.

Pfeiffer Syndrome Market Share

The Pfeiffer Syndrome industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Novartis AG (Switzerland)

- Takeda Pharmaceutical Company Limited (Japan)

- Incyte Corporation (U.S.)

- Illumina, Inc. (U.S.)

- Invitae Corporation (U.S.)

- GeneDx, LLC (U.S.)

- Blueprint Genetics Oy (Finland)

- BGI Genomics (China)

- Stryker (U.S.)

- Medtronic (Ireland)

- Zimmer Biomet (U.S.)

- Integra LifeSciences Corporation (U.S.)

- KLS Martin Group (Germany)

- Materialise NV (Belgium)

- 3D Systems Corporation (U.S.)

- Siemens Healthineers AG (Germany)

- GE HealthCare. (U.S.)

What are the Recent Developments in Global Pfeiffer Syndrome Market?

- In July 2025, a prenatal diagnosis case of Pfeiffer syndrome type II was reported in a fetus carrying a de novo FGFR2 c.1019A>G p.(Tyr340Cys) variant. The study demonstrated the increasing clinical use of rapid fetal exome sequencing alongside high-resolution ultrasound imaging for early detection of craniosynostosis syndromes. This advancement marks a crucial step toward earlier and more accurate prenatal identification of FGFR2-related disorders

- In April 2025, a clinical genetics study identified two pediatric patients initially diagnosed with Pfeiffer syndrome who were later found to have osteoglophonic dysplasia (OGD). The discovery emphasized the complexity of FGFR1 and FGFR2 variant interpretation, underscoring the need for precise molecular testing to avoid misclassification of overlapping syndromes

- In September 2024, An expert consensus guideline was developed aiming to standardize the diagnosis and treatment pathways of FGFR gene‐altered conditions (including FGFR2 mutations). This consensus highlights the push toward structured management frameworks for rare FGFR-mediated syndromes, which supports better care delivery for disorders such as Pfeiffer syndrome

- In February 2024, Researchers reported the identification of a mosaic activating variant in FGFR2 (c.1647T>G p.(Asn549Lys)) in a patient initially diagnosed with a neurocutaneous syndrome. The study concluded the correct clinical–molecular diagnosis was an FGFR2-associated neurocutaneous syndrome, thereby expanding the known genotypic & phenotypic spectrum of FGFR2-related disorders

- In January 2024, A review article published on craniofacial disorders and dysplasias took an updated molecular, clinical and management perspective on syndromic craniosynostoses. The paper underlined the increasing role of molecular diagnostics, imaging and multidisciplinary care in improving outcomes for rare craniosynostosis syndromes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.