Global Post Acute Care Coordination Services Market

Market Size in USD Billion

USD

3.46 Billion

USD

9.86 Billion

2025

2033

USD

3.46 Billion

USD

9.86 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.46 Billion | |

| USD 9.86 Billion | |

| % | |

|

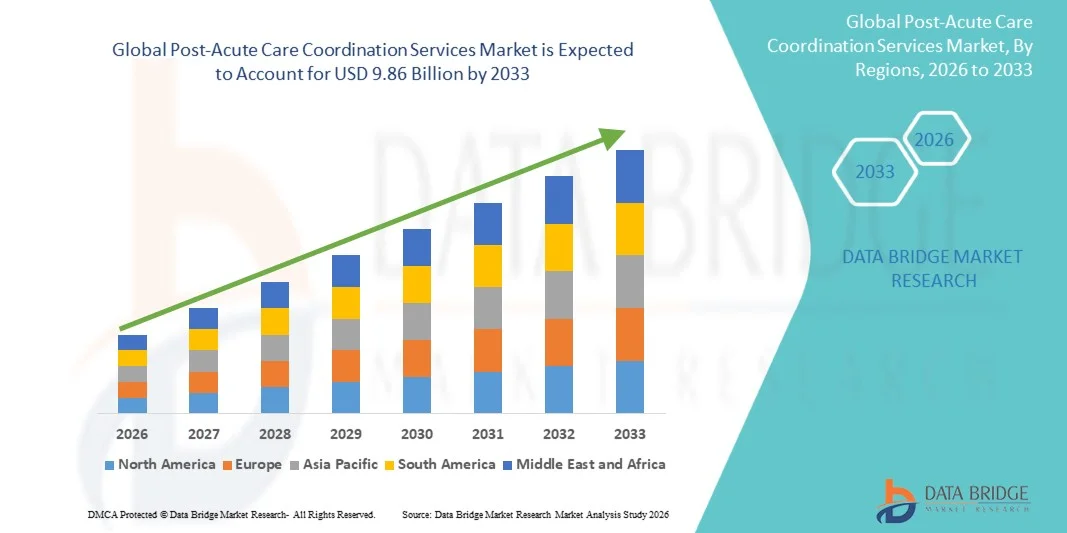

Post-Acute Care Coordination Services Market Size

- The global post-acute care coordination services market size was valued at USD 3.46 billion in 2025 and is expected to reach USD 9.86 billion by 2033, at a CAGR of 14.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases, aging population, and the rising need for efficient patient transition management across healthcare settings, leading to greater emphasis on continuity of care and cost optimization

- Furthermore, growing demand for integrated, patient-centric care models along with advancements in healthcare IT, telehealth, and value-based reimbursement systems is establishing post-acute care coordination as a critical component of modern healthcare delivery. These converging factors are accelerating the adoption of coordinated care services, thereby significantly boosting the industry's growth

Post-Acute Care Coordination Services Market Analysis

- Post-acute care coordination services, which focus on managing patient transitions across healthcare settings such as hospitals, rehabilitation centers, and home care, are increasingly vital components of modern healthcare systems due to their ability to improve patient outcomes, reduce readmissions, and ensure continuity of care

- The escalating demand for post-acute care coordination services is primarily fueled by the rising prevalence of chronic diseases, growing geriatric population, and increasing emphasis on value-based care models that prioritize cost efficiency and quality outcomes

- North America dominated the post-acute care coordination services market with the largest revenue share of 40.01% in 2025, characterized by advanced healthcare infrastructure, high adoption of digital health solutions, and strong presence of key market players, with the U.S. experiencing significant growth driven by reimbursement reforms and widespread use of care management technologies

- Asia-Pacific is expected to be the fastest growing region in the post-acute care coordination services market during the forecast period due to improving healthcare infrastructure, increasing healthcare expenditure, and rising awareness regarding coordinated care approaches

- Home Health Agencies segment dominated the post-acute care coordination services market with a market share of 43.2% in 2025, driven by increasing patient preference for home-based care, cost-effectiveness, and advancements in remote monitoring and telehealth technologies

Report Scope and Post-Acute Care Coordination Services Market Segmentation

|

Attributes |

Post-Acute Care Coordination Services Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Post-Acute Care Coordination Services Market Trends

“Digital Integration and AI-Driven Care Coordination”

- A significant and accelerating trend in the global post-acute care coordination services market is the growing integration of artificial intelligence (AI) and digital health platforms such as telehealth systems, electronic health records (EHRs), and remote monitoring tools. This convergence of technologies is significantly enhancing care coordination efficiency and patient outcomes

- For instance, care coordination platforms are increasingly integrating with EHR systems and telehealth solutions, allowing providers to monitor patient progress remotely and ensure seamless transitions between care settings. Similarly, digital care platforms enable real-time communication between multidisciplinary teams, improving decision-making and care delivery

- AI integration in post-acute care coordination enables features such as predictive analytics to identify high-risk patients, optimize discharge planning, and reduce hospital readmissions. For instance, some platforms utilize AI algorithms to analyze patient data and generate alerts for potential complications, while remote monitoring tools track vital signs and trigger interventions when necessary. Furthermore, digital communication tools offer providers the ability to coordinate care efficiently across multiple touchpoints

- The seamless integration of care coordination services with broader healthcare IT ecosystems facilitates centralized management of patient data and care plans. Through a unified interface, healthcare providers can manage patient transitions, monitor recovery progress, and coordinate with caregivers and specialists, creating a streamlined and patient-centric care experience

- This trend towards more intelligent, data-driven, and interconnected care coordination systems is fundamentally reshaping healthcare delivery models. Consequently, companies such as care management solution providers are developing AI-enabled platforms with features such as automated care pathways, predictive risk scoring, and interoperability with major healthcare systems

- The demand for advanced care coordination solutions that offer seamless digital integration and data-driven insights is growing rapidly across healthcare providers and payers, as stakeholders increasingly prioritize efficiency, cost reduction, and improved patient outcomes

- Growing focus on personalized care pathways and patient-centric models is encouraging providers to leverage data analytics and digital tools to tailor post-acute care plans based on individual patient needs and recovery patterns

Post-Acute Care Coordination Services Market Dynamics

Driver

“Rising Demand for Value-Based Care and Aging Population”

- The increasing shift towards value-based care models, coupled with the rising geriatric population, is a significant driver for the heightened demand for post-acute care coordination services

- For instance, in recent years, healthcare systems and payers have implemented bundled payment programs and accountable care models aimed at improving care quality while reducing costs. Such strategies by key stakeholders are expected to drive the market growth in the forecast period

- As healthcare providers focus on reducing hospital readmissions and improving patient outcomes, care coordination services offer structured pathways, real-time monitoring, and enhanced communication across care settings, making them essential in modern healthcare systems

- Furthermore, the growing prevalence of chronic diseases and the increasing need for long-term care management are driving the adoption of coordinated care services, ensuring continuity of care beyond hospital discharge

- The convenience of integrated care planning, remote patient monitoring, and improved collaboration among healthcare providers are key factors propelling the adoption of post-acute care coordination services across hospitals, rehabilitation centers, and home care settings. The trend towards digital health transformation and increasing investments in healthcare IT further contribute to market growth

- Increasing healthcare expenditure and government initiatives aimed at improving care transitions and reducing hospital burden are further accelerating the adoption of post-acute care coordination services globally

- Rising demand for home-based care and patient preference for receiving treatment in familiar environments is also driving the expansion of coordinated care services outside traditional healthcare facilities

Restraint/Challenge

“Data Interoperability Issues and Regulatory Compliance Hurdles”

- Concerns surrounding data interoperability challenges and stringent healthcare regulations pose a significant barrier to the widespread adoption of post-acute care coordination services. As these services rely heavily on digital platforms and data sharing, inconsistencies in systems and standards can hinder seamless information exchange

- For instance, variations in electronic health record systems and regulatory requirements across regions can create difficulties in integrating patient data and ensuring compliance, leading to inefficiencies in care coordination

- Addressing these interoperability and regulatory concerns through standardized data protocols, secure data exchange frameworks, and compliance with healthcare regulations is crucial for building trust among providers and patients. Companies are increasingly focusing on developing interoperable platforms and ensuring adherence to data privacy laws to facilitate adoption

- In addition, the high implementation costs associated with advanced care coordination systems and the need for skilled personnel can be a barrier for smaller healthcare providers, particularly in developing regions

- While digital health adoption is increasing, the complexity of integrating new technologies into existing healthcare workflows and the resistance to change among healthcare professionals can further hinder market growth. Overcoming these challenges through technological standardization, regulatory alignment, and cost-effective solutions will be vital for sustained market expansion

- Limited digital infrastructure in emerging economies can restrict the effective deployment of advanced care coordination platforms, thereby slowing market penetration in these regions

- Concerns related to data privacy and cybersecurity risks in handling sensitive patient information can further challenge adoption, requiring continuous investment in secure systems and compliance measures

Post-Acute Care Coordination Services Market Scope

The market is segmented on the basis of service, patient demographics, and end user.

- By Service

On the basis of service, the global post-acute care coordination services market is segmented into skilled nursing facilities, inpatient rehabilitation facilities, home health agencies, long-term acute care hospitals, hospice & palliative care, outpatient rehabilitation services, and others. The home health agencies segment dominated the market with the largest revenue share of 43.2% in 2025, driven by increasing patient preference for receiving care in home settings, cost-effectiveness compared to institutional care, and advancements in remote monitoring and telehealth technologies. Home-based care enables continuous patient engagement and reduces hospital readmissions, making it a preferred option for both providers and payers. In addition, supportive reimbursement policies and growing elderly population further strengthen the dominance of this segment. The ability to deliver personalized and flexible care plans also contributes significantly to its widespread adoption globally.

The inpatient rehabilitation facilities segment is anticipated to witness the fastest growth rate during the forecast period, fueled by the rising incidence of chronic diseases, orthopedic conditions, and neurological disorders requiring intensive rehabilitation. These facilities offer specialized, multidisciplinary care with advanced therapeutic interventions, which significantly improves patient recovery outcomes. Increasing awareness regarding the benefits of structured rehabilitation programs and growing investments in rehabilitation infrastructure are further driving segment growth. Moreover, the integration of advanced technologies such as robotics and AI in rehabilitation is enhancing treatment effectiveness and attracting higher patient inflow.

- By Patient Demographics

On the basis of patient demographics, the global post-acute care coordination services market is segmented into elderly patients, patients with chronic illnesses, post-surgical patients, patients requiring rehabilitation, and others. The elderly patients segment dominated the market with the largest revenue share in 2025, driven by the rapidly aging global population and the higher prevalence of multiple chronic conditions among older individuals. Elderly patients often require continuous monitoring, medication management, and coordinated care transitions, making them the primary users of post-acute care services. The growing burden on healthcare systems to manage geriatric care efficiently has further increased reliance on coordinated care solutions. In addition, favorable government initiatives and insurance coverage for elderly care contribute to the dominance of this segment. The complexity of care required by this population ensures sustained demand for coordination services.

The patients with chronic illnesses segment is expected to witness the fastest growth rate during the forecast period, driven by the increasing global burden of diseases such as diabetes, cardiovascular disorders, and respiratory conditions. These patients require long-term, continuous care management and frequent transitions between care settings, necessitating effective coordination services. Rising awareness about disease management and preventive care is also contributing to segment growth. Furthermore, advancements in digital health tools and remote monitoring technologies are enabling better management of chronic conditions outside hospital settings. This shift towards proactive and continuous care models is accelerating the adoption of coordination services for chronic disease patients.

- By End User

On the basis of end user, the global post-acute care coordination services market is segmented into hospitals, rehabilitation centers, home care providers, long-term care facilities, government health programs, private health insurers, and others. The hospitals segment dominated the market with the largest revenue share in 2025, driven by their central role in patient discharge planning and care transition management. Hospitals are increasingly adopting care coordination services to reduce readmission rates, improve patient outcomes, and comply with value-based care models. The integration of digital health systems within hospitals further enhances coordination efficiency across different care settings. In addition, hospitals act as primary hubs for initiating post-acute care pathways, thereby maintaining strong control over patient flow and coordination processes.

The home care providers segment is anticipated to witness the fastest growth rate during the forecast period, fueled by the increasing demand for home-based healthcare services and patient preference for receiving care in familiar environments. Home care providers are leveraging digital tools and remote monitoring technologies to deliver efficient and coordinated care outside traditional healthcare facilities. The cost advantages associated with home care compared to hospital stays are also driving segment growth. Furthermore, the expansion of telehealth services and supportive reimbursement frameworks are enabling home care providers to play a more significant role in post-acute care coordination. This shift towards decentralized healthcare delivery is expected to significantly boost the growth of this segment.

Post-Acute Care Coordination Services Market Regional Analysis

- North America dominated the post-acute care coordination services market with the largest revenue share of 40.01% in 2025, characterized by advanced healthcare infrastructure, high adoption of digital health solutions, and strong presence of key market players

- Healthcare providers in the region highly prioritize improved patient outcomes, reduced hospital readmissions, and seamless coordination across care settings through the use of advanced digital health technologies and integrated care platforms

- This widespread adoption is further supported by advanced healthcare infrastructure, high healthcare expenditure, favorable reimbursement policies, and the strong presence of key market players, establishing post-acute care coordination services as a critical component in enhancing healthcare delivery across the region

U.S. Post-Acute Care Coordination Services Market Insight

The U.S. post-acute care coordination services market captured the largest revenue share of 81% in 2025 within North America, fueled by the strong adoption of value-based care models and the increasing focus on reducing hospital readmissions. Healthcare providers are increasingly prioritizing efficient care transitions through coordinated services and digital health platforms. The growing preference for integrated care delivery, combined with robust demand for remote patient monitoring and care management solutions, further propels the market. Moreover, the increasing integration of healthcare IT systems, such as electronic health records and telehealth platforms, is significantly contributing to the market's expansion.

Europe Post-Acute Care Coordination Services Market Insight

The Europe post-acute care coordination services market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent healthcare regulations and the increasing need for efficient patient care transitions. The rise in aging population, coupled with the demand for integrated healthcare services, is fostering the adoption of care coordination solutions. European healthcare providers are also drawn to the cost-efficiency and improved patient outcomes these services offer. The region is experiencing significant growth across hospitals, rehabilitation centers, and home care settings, with coordinated care services being incorporated into both public and private healthcare systems.

U.K. Post-Acute Care Coordination Services Market Insight

The U.K. post-acute care coordination services market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing demand for streamlined patient discharge processes and improved continuity of care. In addition, concerns regarding hospital overcrowding and healthcare efficiency are encouraging providers to adopt coordinated care solutions. The UK’s advancement in digital health infrastructure, alongside its strong public healthcare system, is expected to continue to stimulate market growth.

Germany Post-Acute Care Coordination Services Market Insight

The Germany post-acute care coordination services market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of integrated healthcare delivery and the demand for efficient post-discharge care solutions. Germany’s well-developed healthcare infrastructure, combined with its focus on innovation and patient-centered care, promotes the adoption of coordination services, particularly in hospitals and rehabilitation facilities. The integration of digital health platforms with care coordination systems is also becoming increasingly prevalent, with a strong preference for efficient and quality-driven healthcare solutions aligning with local expectations.

Asia-Pacific Post-Acute Care Coordination Services Market Insight

The Asia-Pacific post-acute care coordination services market is poised to grow at the fastest CAGR of 24% during the forecast period of 2026 to 2033, driven by increasing healthcare expenditure, rising prevalence of chronic diseases, and improving healthcare infrastructure in countries such as China, Japan, and India. The region's growing focus on healthcare accessibility, supported by government initiatives promoting digital health, is driving the adoption of care coordination services. Furthermore, as APAC emerges as a key region for healthcare innovation and service expansion, the accessibility and implementation of coordinated care solutions are expanding to a broader patient population.

Japan Post-Acute Care Coordination Services Market Insight

The Japan post-acute care coordination services market is gaining momentum due to the country’s aging population, advanced healthcare system, and increasing demand for efficient long-term care management. The Japanese market places a strong emphasis on patient outcomes, and the adoption of care coordination services is driven by the increasing need for continuous monitoring and rehabilitation services. The integration of coordination services with digital health technologies, such as remote monitoring and telehealth, is fueling growth. Moreover, Japan's elderly population is likely to spur demand for accessible, efficient care solutions in both residential and institutional healthcare settings.

India Post-Acute Care Coordination Services Market Insight

The India post-acute care coordination services market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country's expanding healthcare infrastructure, rapid urbanization, and increasing adoption of digital health solutions. India stands as one of the fastest-growing markets for healthcare services, and care coordination is becoming increasingly important in hospitals, home care, and rehabilitation settings. The push towards improving healthcare access and the availability of cost-effective care solutions, alongside growing private sector participation, are key factors propelling the market in India.

Post-Acute Care Coordination Services Market Share

The Post-Acute Care Coordination Services industry is primarily led by well-established companies, including:

- PointClickCare Corp. (Canada)

- Bamboo Health, Inc. (U.S.)

- CareCentrix, Inc. (U.S.)

- naviHealth, Inc. (U.S.)

- Amedisys, Inc. (U.S.)

- LHC Group, Inc. (U.S.)

- Encompass Health Corporation (U.S.)

- Genesis HealthCare, Inc. (U.S.)

- Brookdale Senior Living Inc. (U.S.)

- AccentCare, Inc. (U.S.)

- Aveanna Healthcare LLC (U.S.)

- VITAS Healthcare Corporation (U.S.)

- Interim HealthCare Inc. (U.S.)

- Select Medical Holdings Corporation (U.S.)

- National HealthCare Corporation (U.S.)

- Trilogy Health Services, LLC (U.S.)

- Sonida Senior Living, Inc. (U.S.)

- BAYADA Home Health Care, Inc. (U.S.)

- Addus HomeCare Corporation (U.S.)

- Optum, Inc. (U.S.)

What are the Recent Developments in Global Post-Acute Care Coordination Services Market?

- In May 2025, CMS introduced new care models aimed at improving patient transitions and reducing discharge delays, with a strong focus on incentivizing care coordination and minimizing avoidable hospital readmissions. These initiatives emphasize the growing importance of structured post-acute care coordination in enhancing healthcare efficiency and patient outcomes across systems

- In December 2024, the Centers for Medicare & Medicaid Services (CMS) reported that over 366 hospitals had participated in the Acute Hospital Care at Home initiative, treating more than 31,000 patients through coordinated home-based care models. This development highlights the rapid expansion of integrated post-acute care coordination programs leveraging remote monitoring and multidisciplinary care teams to improve patient outcomes and reduce hospital burden

- In May 2024, U.S. hospitals accelerated the expansion of hospital-at-home and remote care programs, enabling patients to receive post-acute and follow-up care in home settings instead of traditional facilities. These initiatives, supported by telehealth and digital monitoring tools, aim to reduce hospital burden, improve care continuity, and lower costs, highlighting a major shift toward decentralized care coordination models

- In April 2024, Kaiser Permanente expanded its Advanced Care at Home program, combining telehealth, home visits, and remote monitoring coordinated through centralized command centers. This model demonstrated lower 30-day readmission rates and improved patient experience, reinforcing the role of digitally enabled care coordination in post-acute care delivery

- In May 2021, Mayo Clinic and Kaiser Permanente partnered with Medically Home to expand hospital-at-home programs, enabling coordinated acute and post-acute care delivery in patients’ homes. This collaboration marked a significant advancement in care coordination, leveraging remote monitoring and integrated care teams to improve patient outcomes and reduce hospital congestion

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.