Global Smart Warehousing Market

Market Size in USD Billion

USD

27.67 Billion

USD

64.94 Billion

2025

2033

USD

27.67 Billion

USD

64.94 Billion

2025

2033

| 2026 - 2033 | |

| USD 27.67 Billion | |

| USD 64.94 Billion | |

| % | |

|

What is the Global Smart Warehousing Market Size and Growth Rate?

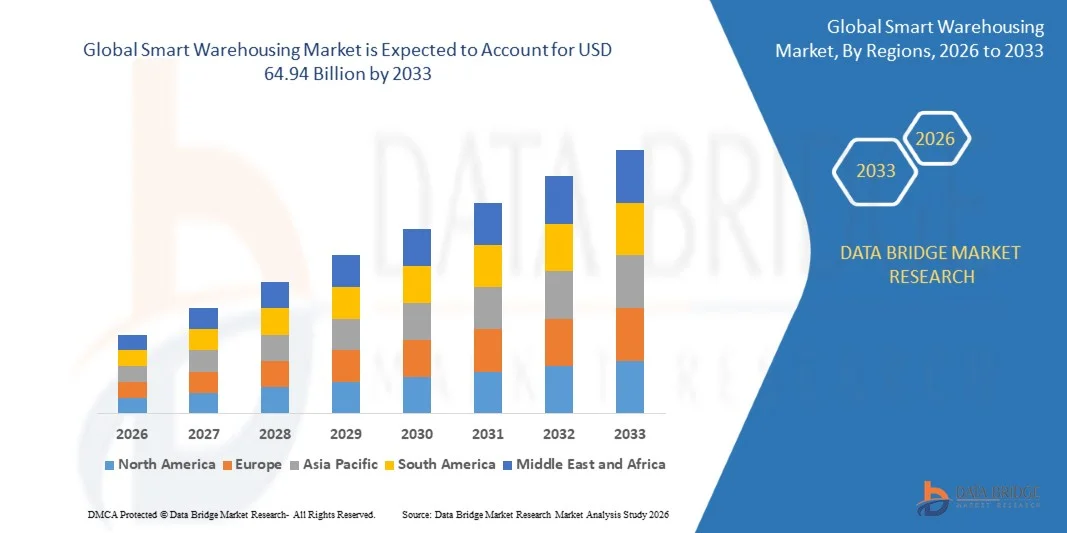

- The global Smart Warehousing market size was valued at USD 27.67 billion in 2025 and is expected to reach USD 64.94 billion by 2033, at a CAGR of 11.25% during the forecast period

- Increasing adoption of automation, robotics, IoT, and AI technologies in warehouse operations is driving market growth

- Rising demand for real-time inventory tracking, efficient order fulfillment, and predictive analytics in e-commerce, retail, and logistics sectors, coupled with rapid urbanization, expanding industrialization, and the need for efficient supply chain management, are major factors propelling the Smart Warehousing market

What are the Major Takeaways of Smart Warehousing Market?

- Growing investments in technology modernization, smart infrastructure, and digital transformation in warehouses are creating new opportunities for market expansion

- However, high initial implementation costs, cybersecurity concerns, and lack of skilled workforce in emerging regions are key challenges restraining market growth, which may limit adoption in certain areas

- North America dominated the Smart Warehousing market with a 32.2% revenue share in 2025, driven by widespread adoption of advanced warehouse automation, robotics, IoT-based monitoring, and AI-enabled inventory management across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 10.1% from 2026 to 2033, fueled by rapid urbanization, rising e-commerce, and growing adoption of smart logistics solutions in China, India, Japan, and Southeast Asia

- The Hardware segment dominated the market with a revenue share of 42.5% in 2025, driven by the increasing adoption of automated storage systems, robotics, IoT sensors, and smart conveyors in warehouses

Report Scope and Smart Warehousing Market Segmentation

|

Attributes |

Smart Warehousing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Smart Warehousing Market?

“Rising Adoption of Intelligent, Automated, and Sustainable Smart Warehousing Solutions”

- The smart warehousing market is witnessing a key trend of increasing adoption of automation, robotics, IoT-enabled devices, AI analytics, and eco-friendly storage solutions. This trend is driven by growing demand for operational efficiency, real-time inventory management, and reduced environmental footprint, especially among large e-commerce, retail, and logistics operators globally

- For instance, companies such as Manhattan Associates, Honeywell, and Zebra Technologies are implementing AI-powered robotics, automated guided vehicles (AGVs), and smart sensors to optimize warehouse operations and reduce human error

- Rising demand for faster order fulfillment, accurate inventory tracking, and energy-efficient storage systems is accelerating adoption

- Manufacturers are integrating AI analytics, predictive maintenance, and IoT monitoring to enhance warehouse efficiency, reduce downtime, and lower operational costs

- Increasing R&D on energy-efficient automation, smart robotics, and integrated software platforms is fostering innovation in warehousing

- As businesses continue prioritizing digitalization, efficiency, and sustainability, Smart Warehousing solutions are expected to remain central to modern supply chain operations

What are the Key Drivers of Smart Warehousing Market?

- Growing demand for automation, operational efficiency, and real-time inventory tracking is a major driver of market growth

- For instance, in 2025, Honeywell, IBM, and SAP expanded their warehouse automation and AI analytics solutions targeting large-scale retail and e-commerce operators

- Rising adoption of IoT-enabled devices, robotics, and AI-powered software is driving implementation across North America, Europe, and Asia-Pacific

- Technological advancements in cloud deployment, predictive analytics, and AR/VR-based warehouse management are enabling high-performance operations

- Increased integration of smart systems in order fulfillment, inventory control, and asset tracking is further supporting global market expansion

- With continued investment in automation, AI, and sustainable warehouse solutions, the smart warehousing market is expected to maintain strong growth momentum in the coming years

Which Factor is Challenging the Growth of the Smart Warehousing Market?

- High initial investment in robotics, IoT devices, and AI analytics limits large-scale adoption, particularly for small and medium-sized warehouses

- For instance, during 2024–2025, rising costs of automated machinery, sensors, and cloud software affected deployment in cost-sensitive markets

- Complexity in integrating multiple technologies, ensuring data security, and complying with regional safety and environmental regulations increases operational challenges

- Limited skilled workforce to operate and maintain advanced smart systems hinders adoption, especially in emerging regions

- Competition from traditional warehouse setups and low-tech storage solutions creates pricing pressure and affects market penetration

- To overcome these challenges, market participants are investing in cost-efficient automation, scalable software platforms, workforce training, and strategic partnerships to ensure effective and high-quality Smart Warehousing implementation

How is the Smart Warehousing Market Segmented?

The market is segmented on the basis of component, deployment, technology, application, warehouse size, and vertical.

- By Component

On the basis of component, the smart warehousing market is segmented into Hardware, Software, and Services. The Hardware segment dominated the market with a revenue share of 42.5% in 2025, driven by the increasing adoption of automated storage systems, robotics, IoT sensors, and smart conveyors in warehouses. Hardware investments enable real-time inventory tracking, automated picking, and efficient material handling, which reduce operational costs and enhance productivity. Software solutions, including warehouse management systems (WMS), AI analytics, and cloud-based platforms, are widely deployed for inventory optimization and predictive insights. Services, encompassing maintenance, consulting, and integration, complement hardware and software deployment.

The Services segment is projected to grow at the fastest CAGR from 2026 to 2033 due to rising demand for managed smart warehousing solutions and outsourcing of maintenance and technology integration, especially among SMEs and e-commerce operators. Overall, component investments are central to operational efficiency and technological adoption in modern warehouses.

- By Deployment

On the basis of deployment, the smart warehousing market is segmented into Cloud and On-Premises. The On-Premises segment dominated the market with a 54.1% revenue share in 2025, driven by large enterprises preferring direct control over data, security, and IT infrastructure for mission-critical warehouse operations. On-premises solutions offer customization, seamless integration with legacy systems, and enhanced control over automated machinery, robotics, and sensors.

The Cloud segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by rising adoption of SaaS-based warehouse management systems, AI analytics, and IoT monitoring platforms. Cloud deployment enables scalability, remote access, and subscription-based pricing models, appealing especially to small and medium-sized warehouses and logistics providers seeking cost-effective, flexible solutions. The choice of deployment significantly influences operational efficiency, IT management, and overall cost optimization in smart warehousing.

- By Technology

On the basis of technology, the smart warehousing market is segmented into IoT, Robotics and Automation, AI and Analytics, Networking and Communication, AR and VR, and Others. Robotics and Automation dominated the market with a revenue share of 38.7% in 2025, driven by high adoption of automated guided vehicles (AGVs), conveyor systems, and robotic picking solutions in large-scale warehouses. Robotics improve operational efficiency, reduce human error, and enhance throughput, making them a critical investment for modern warehouses. IoT sensors and AI-powered analytics are widely used for real-time monitoring, predictive maintenance, and inventory optimization.

The AR and VR segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by increasing use of augmented reality for operator training, order picking visualization, and virtual warehouse layout planning. Technology deployment is central to warehouse automation, operational accuracy, and future-ready supply chains.

- By Application

On the basis of application, the smart warehousing market is segmented into Inventory Management, Order Fulfillment, Asset Tracking, Predictive Analytics, and Others. The Inventory Management segment dominated the market with a revenue share of 40.6% in 2025, fueled by demand for real-time stock visibility, automated replenishment, and reduced stock-outs across retail, e-commerce, and manufacturing sectors. Solutions include AI-driven demand forecasting, RFID tagging, and barcode scanning to optimize warehouse throughput and operational efficiency.

The Predictive Analytics segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing adoption of AI and machine learning to anticipate demand, optimize labor deployment, and improve equipment utilization. Application-specific adoption enhances accuracy, reduces operational costs, and improves overall warehouse performance across industries globally.

- By Warehouse Size

On the basis of warehouse size, the smart warehousing market is segmented into Small, Medium, and Large. The Large warehouse segment dominated the market with a revenue share of 45.2% in 2025, supported by the presence of expansive fulfillment centers, distribution hubs, and logistics parks that leverage robotics, automated storage, and AI analytics for high-volume operations. Medium-sized warehouses are adopting modular and flexible solutions to support growing e-commerce demands.

The Small warehouse segment is projected to grow at the fastest CAGR from 2026 to 2033 due to rising deployment of compact automation solutions, cloud-based WMS, and IoT-enabled monitoring in SMEs and regional distribution centers. Warehouse size directly influences technology adoption, automation level, and operational efficiency.

- By Vertical

On the basis of vertical, the smart warehousing market is segmented into Transportation & Logistics, Retail & E-commerce, Manufacturing, Healthcare, Energy & Utilities, Automotive, Food & Beverages, and Others. The Retail & E-commerce vertical dominated the market with a revenue share of 41.8% in 2025, fueled by the surge in online shopping, rapid order fulfillment requirements, and high consumer expectations for quick delivery. Advanced automation, AI-powered sorting, and robotics are extensively deployed in fulfillment centers for large e-commerce platforms.

The Food & Beverages vertical is projected to grow at the fastest CAGR from 2026 to 2033, driven by cold chain requirements, perishable goods handling, and the integration of real-time tracking and predictive analytics to maintain quality and reduce spoilage. Vertical-specific solutions are critical for operational efficiency, regulatory compliance, and customer satisfaction.

Which Region Holds the Largest Share of the Smart Warehousing Market?

- North America dominated the smart warehousing market with a 32.2% revenue share in 2025, driven by widespread adoption of advanced warehouse automation, robotics, IoT-based monitoring, and AI-enabled inventory management across the U.S. and Canada

- High industrialization, strong e-commerce penetration, and established logistics infrastructure contribute to market leadership. Key players are leveraging innovative solutions in predictive analytics, smart conveyors, and cloud-based warehouse management systems to meet growing operational efficiency demands

- Urbanization, rising disposable income, and increasing adoption of e-commerce and retail automation are driving higher demand across the region

U.S. Smart Warehousing Market Insight

The U.S. is the largest contributor to the North American market, supported by high adoption of smart warehousing solutions in retail, e-commerce, manufacturing, and logistics sectors. Companies are investing in robotics, AI-powered inventory tracking, and cloud-based warehouse management systems to optimize operations, reduce costs, and enhance productivity. Expanding deployment across small, medium, and large-scale warehouses ensures broad market coverage. Technological modernization and focus on operational efficiency further strengthen the U.S. market position.

Canada Smart Warehousing Market Insight

Canada contributes steadily to the North American market, driven by increasing investments in warehouse automation, predictive analytics, and IoT-enabled monitoring. Retail, food & beverage, and logistics industries are adopting AI and robotics to enhance warehouse efficiency and accuracy. Integration of cloud-based platforms and collaborative solutions further supports operational growth. Government initiatives and rising interest in eco-friendly and energy-efficient warehouse solutions enhance adoption.

Asia-Pacific Smart Warehousing Market Insight

Asia-Pacific is projected to register the fastest CAGR of 10.1% from 2026 to 2033, fueled by rapid urbanization, rising e-commerce, and growing adoption of smart logistics solutions in China, India, Japan, and Southeast Asia. The region benefits from expanding industrial hubs, growing retail and e-commerce networks, and increasing investments in warehouse automation. IoT-based inventory monitoring, AI-driven predictive analytics, and robotic automation are gaining traction. Rising demand for operational efficiency, cost reduction, and real-time supply chain visibility drives adoption across the region.

China Smart Warehousing Market Insight

China leads the Asia-Pacific market, supported by large-scale adoption of warehouse robotics, automated storage & retrieval systems, and AI-enabled inventory management. The country’s expanding e-commerce and retail sectors are driving smart warehousing investments. Strong logistics infrastructure, government incentives, and increasing focus on automation and digitalization strengthen market growth. Continuous technology integration and operational optimization remain key drivers.

India Smart Warehousing Market Insight

India is emerging as a key contributor to regional growth, driven by rising e-commerce penetration, logistics modernization, and increasing industrialization. Companies are deploying AI, IoT sensors, and automated storage systems to improve operational efficiency and scalability. Growth is further supported by government initiatives in smart logistics, warehousing modernization, and industrial policy reforms. Rising adoption of predictive analytics and cloud-based warehouse management platforms is expected to sustain long-term growth in India.

Which are the Top Companies in Smart Warehousing Market?

The smart warehousing industry is primarily led by well-established companies, including:

- Honeywell International Inc. (U.S.)

- Siemens (Germany)

- Zebra Technologies Corporation (U.S.)

- IBM Corporation (U.S.)

- Oracle Corporation (U.S.)

- SAP SE (Germany)

- KION Group AG (Germany)

- Cognex Corporation (U.S.)

- ABB Ltd. (Switzerland)

- Tecsys, Inc. (Canada)

- Manhattan Associates (U.S.)

- PSI Logistics (Germany)

- Reply (Italy)

- Körber (Germany)

- Samsung SDS (South Korea)

- Infor (U.S.)

- Blue Yonder (U.S.)

- Generix Group (France)

- Microlistics (U.K.)

- Microsoft (U.S.)

- Foysonis (U.K.)

- Increff (India)

- Locus Robotics (U.S.)

- ShipHero (U.S.)

What are the Recent Developments in Global Smart Warehousing Market?

- In May 2025, Blue Yonder acquired Pledge Earth Technologies Ltd., aiming to expand its end-to-end supply chain platform with accredited carbon emissions reporting. Pledge’s software enables businesses to monitor and manage their carbon footprint across logistics operations, aligning with global sustainability standards. This acquisition strengthens Blue Yonder’s position in sustainable and transparent supply chain management

- In May 2025, Samsung SDS and SAP strengthened their collaboration to expand cloud ERP services, focusing on regulated industries such as finance, public, and defense sectors. The partnership supports cloud ERP migration and integrates AI and hyper-automation technologies, enhancing operational efficiency and warehouse and supply chain compliance. This collaboration is expected to drive innovation in smart logistics solutions

- In April 2025, Uniserve partnered with Logistics Reply to implement LEA Reply, a cloud-native, microservices-based warehouse management system (WMS). The partnership improves scalability, operational efficiency, and real-time inventory visibility across Uniserve’s supply chain. Future integration of AI, inventory drones, yard management, and dock scheduling will further optimize warehouse operations

- In January 2025, Blue Yonder and Rhenus Warehousing Solutions formed a strategic partnership to standardize warehouse operations globally. The collaboration focuses on deploying Blue Yonder’s WMS across Rhenus facilities to enhance efficiency, scalability, and consistency in warehouse processes. This alliance reinforces global operational standardization and productivity

- In December 2024, Körber and KKR acquired MercuryGate, a transportation management system (TMS) provider, to enhance their supply chain execution suite. The acquisition aims to deliver integrated solutions across order, warehouse, and transportation management, improving efficiency and visibility from procurement to delivery. This move strengthens their end-to-end supply chain capabilities

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.