Middle East Africa Hydrocolloids Market

Market Size in USD Billion

USD

690.50 Billion

USD

1,208.60 Billion

2024

2032

USD

690.50 Billion

USD

1,208.60 Billion

2024

2032

| 2025 - 2032 | |

| USD 690.50 Billion | |

| USD 1,208.60 Billion | |

| % | |

|

Hydrocolloids Market Size

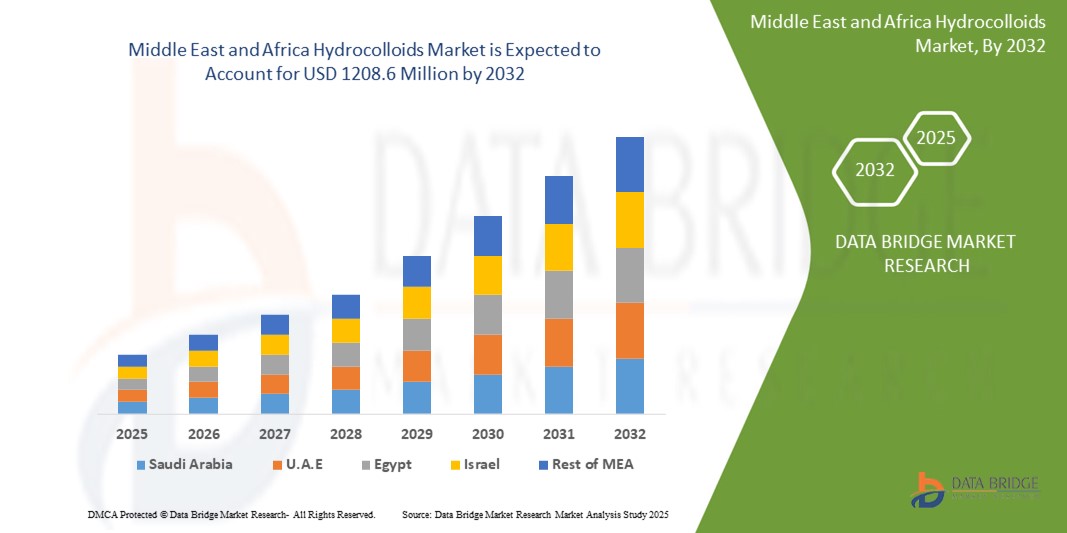

- The Middle East and Africa hydrocolloids market size was valued at USD 690.5 million in 2024 and is expected to reach USD 1,208.6 million by 2032, growing at a CAGR of 7.20% during the forecast period.

- The market growth is primarily driven by rising demand in food and beverage processing, expanding pharmaceutical applications, and the shift toward natural, plant-based stabilizers and thickeners.

Hydrocolloids Market Analysis

- Hydrocolloids are a class of high-molecular-weight polymers widely used for their gelling, thickening, stabilizing, and emulsifying properties. They are critical in enhancing texture, shelf life, and quality in food, pharmaceutical, and cosmetic formulations.

- The market is witnessing robust growth across MEA, propelled by changing dietary habits, urbanization, and a growing health-conscious population seeking clean-label, plant-derived ingredients in processed foods and personal care products.

- Saudi Arabia is expected to dominate the MEA hydrocolloids market with a market share of 33.81%, owing to its expanding food processing sector, increasing pharmaceutical manufacturing, and strong investment in health and wellness products.

- South Africa is projected to be the fastest-growing country in the hydrocolloids market during the forecast period, driven by rising consumption of functional foods and beverages, increasing local production of dairy and meat products, and greater use of hydrocolloids in pharmaceutical delivery systems.

- The gelatin segment is expected to lead the market with a share of 29.65%, due to its versatility in applications ranging from food to capsules, and its ability to provide excellent gelling and stabilizing functions, especially in confectionery, dairy, and nutraceutical formulations.

Report Scope and Hydrocolloids Market Segmentation

|

Attributes |

Hydrocolloids Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Hydrocolloids Market Trends

“Shift Toward Clean Label and Plant-Based Hydrocolloids”

- A key trend in the MIDDLE EAST AND AFRICA hydrocolloids market is the increasing preference for clean-label and plant-based hydrocolloids, driven by evolving consumer preferences and health-conscious dietary choices.

- This trend is fueled by the rising demand for natural food ingredients, increased awareness about synthetic additives, and the growing vegan and flexitarian population across the region.

- For instance, major players like CP Kelco and Cargill are focusing on developing hydrocolloids such as pectin, guar gum, and xanthan gum derived from plant-based sources to cater to food and beverage manufacturers aiming for clean-label formulations.

- The trend also aligns with the regulatory push for transparency in food labeling and the demand for allergen-free, gluten-free, and additive-free alternatives.

- As consumers increasingly scrutinize product labels and opt for natural alternatives, clean-label hydrocolloids are expected to drive innovation and market expansion in the food, pharmaceutical, and personal care sectors.

Hydrocolloids Market Dynamics

Driver

“Rising Demand for Functional Ingredients in Food & Beverage Industry”

- The booming food and beverage sector in the MIDDLE EAST AND AFRICA is a key driver for the hydrocolloids market, as hydrocolloids play a vital role in texture modification, shelf-life extension, and stabilization of food products.

- Rapid urbanization, growing disposable incomes, and the increasing popularity of convenience and processed foods are fueling demand for hydrocolloids across dairy, bakery, confectionery, and ready-to-eat segments.

- For instance, companies such as DuPont Nutrition & Biosciences and Ingredion Incorporated are expanding their product lines to offer customized hydrocolloids for local taste preferences and functional needs in processed food applications.

- Additionally, rising health awareness has led to the use of hydrocolloids in low-fat, low-sugar, and fiber-enriched formulations, further boosting their demand.

- As regional food processors modernize operations and innovate product lines, the adoption of functional hydrocolloids is expected to accelerate, driving sustained market growth.

Restraint/Challenge

“High Cost of Natural and Specialty Raw Materials”

- The hydrocolloids market in MEA faces challenges due to price volatility and supply chain instability of key raw materials, such as guar, locust bean, seaweed, and citrus peels.

- As hydrocolloids are largely derived from agricultural or marine sources, fluctuations in weather conditions, crop yields, and geopolitical instability can significantly impact their availability and cost structure.

- For instance, disruptions in guar gum supply due to erratic monsoons in major producing countries like India can directly affect pricing and delivery timelines for MEA manufacturers and suppliers.

- Additionally, the reliance on imports for specific raw materials increases exposure to currency fluctuations and global trade dynamics, making it difficult for local manufacturers to maintain stable pricing.

- These factors pose a major restraint, particularly for small and medium-sized food and cosmetic producers seeking cost-effective hydrocolloid solutions, and may hinder broader adoption across price-sensitive segments.

Hydrocolloids Market Scope

The market is segmented on the basis of type, and application.

- By Type

On the basis of type, the Middle East and Africa Hydrocolloids Market is segmented into Gelatin, Pectin, Carrageenan, Xanthan Gum, Agar, and Others. The Gelatin segment dominates the largest market revenue share of 38.6% in 2025, owing to its widespread use in food & beverage, pharmaceutical, and personal care applications. Its excellent gelling, stabilizing, and emulsifying properties make it a preferred choice in confectionery, capsules, and cosmetics.

However, the Pectin segment is expected to grow at the highest CAGR of 7.35% during the forecast period of 2025–2032. This growth is primarily driven by the rising demand for clean-label, plant-based ingredients in jams, jellies, beverages, and dairy products, along with growing consumer preference for natural and vegan thickeners.

- By Application

On the basis of application, the Middle East and Africa Hydrocolloids Market is segmented into Food & Beverage, Pharmaceuticals, Personal Care & Cosmetics, and Others. The Food & Beverage segment held the largest market share of 46.9% in 2025, driven by increasing utilization of hydrocolloids as thickening, gelling, and stabilizing agents in dairy products, bakery items, sauces, and meat alternatives. The demand is further fueled by the trend towards plant-based and clean-label formulations in Middle East and Africa.

However, the Pharmaceuticals segment is expected to witness the highest CAGR of 6.87% during the forecast period. This is attributed to the expanding use of hydrocolloids in drug delivery systems, tablet binding, wound care, and capsule manufacturing, as the pharmaceutical industry increasingly adopts biocompatible and functional excipients to improve product performance and patient outcomes.

Middle East and Africa Hydrocolloids Market Insight

The MIDDLE EAST AND AFRICA hydrocolloids market is projected to grow steadily through 2025, supported by rising demand for processed food, increasing health awareness, and the region’s expanding food manufacturing capabilities. Growth in the bakery, dairy, beverage, and convenience foods sectors is driving adoption of hydrocolloids for their gelling, stabilizing, thickening, and emulsifying properties. Additionally, increased demand from pharmaceutical, cosmetics, and personal care industries for natural and plant-based ingredients is further boosting market penetration. Regulatory shifts toward clean-label and halal-certified products are also positively influencing hydrocolloid consumption patterns across the region.

- Saudi Arabia Hydrocolloids Market Insight

Saudi Arabia holds the largest market share in the MIDDLE EAST AND AFRICA hydrocolloids market, driven by its well-established food processing industry and strong demand for functional and clean-label ingredients. The country’s growing population, increasing urbanization, and rising health consciousness have accelerated the consumption of low-calorie, natural, and gluten-free food products, all of which rely on hydrocolloids for formulation.

Government-led initiatives under Vision 2030, which emphasize local food production, industrial diversification, and health sector development, are creating new avenues for hydrocolloid applications in nutraceuticals and pharmaceuticals. International ingredient players are also expanding their footprint in Saudi Arabia to tap into its evolving consumer landscape and robust manufacturing base.

- Italy Hydrocolloids Market Insight

The South Africa hydrocolloids market is set to witness significant CAGR growth, driven by increasing demand for packaged food, dairy products, and ready-to-eat meals. The country’s expanding middle class, coupled with growing supermarket penetration, has led to higher consumption of convenience foods, thereby driving the use of hydrocolloids as stabilizers and thickeners.

Furthermore, South Africa’s pharmaceutical and personal care industries are increasingly adopting hydrocolloids in formulations for topical creams, drug delivery systems, and clean-label cosmetics. The country is also seeing a rise in awareness about plant-based and allergen-free ingredients, prompting local manufacturers to reformulate products with natural hydrocolloids such as guar gum, carrageenan, and pectin.

Supportive trade policies and the presence of regional distributors are enhancing accessibility, encouraging both domestic and foreign players to invest in hydrocolloid solutions tailored for South African consumers.

Hydrocolloids Market Share

The Hydrocolloids Market industry is primarily led by well-established companies, including:

- Evonik Industries AG (Germany)

- Hexion Inc. (U.S.)

- Huntsman International LLC (U.S.)

- Cardolite Corporation (U.S.)

- BASF SE (Germany)

- Arnette Polymers, LLC (U.S.)

- Aditya Birla Chemicals (India)

- Momentive Performance Materials Inc. (U.S.)

- Adeka Corporation (Japan)

- Air Products and Chemicals, Inc. (U.S.)

- Mitsubishi Chemical Corporation (Japan)

- Cargill, Incorporated (U.S.)

- Kukdo Chemical Co., Ltd. (South Korea)

- Nagase ChemteX Corporation (Japan)

- Atul Ltd. (India)

Latest Developments in Global Hydrocolloids Market

- In March 2025, CP Kelco announced the expansion of its distribution network across key MIDDLE EAST AND AFRICA markets, including the UAE and Saudi Arabia, through a strategic partnership with a leading regional food ingredients supplier. This move aims to enhance accessibility to CP Kelco’s portfolio of citrus fiber, pectin, and gellan gum, supporting the growing demand for clean-label and functional ingredients in the food, beverage, and personal care sectors.

- In January 2025, Ingredion Incorporated launched a new line of organic-certified starches and gum blends tailored for MEA applications in dairy and confectionery. These products are specifically formulated to meet regional preferences for texture, stability, and natural origin, and are expected to strengthen Ingredion’s presence in the MEA hydrocolloids market amid rising demand for halal, kosher, and plant-based formulations.

- In October 2024, Ashland Global Holdings Inc. introduced a novel hydrocolloid-based thickening agent under its Natrosol™ brand, targeting the booming skincare and personal care markets in South Africa and the Gulf region. The innovation offers enhanced viscosity control and compatibility with natural actives, aligning with consumer trends toward sustainable and natural cosmetic formulations.

- In August 2024, Cargill expanded its portfolio of seaweed-derived carrageenan products in response to increased demand for natural texturizers in MEA dairy and plant-based beverages. The company also announced its intent to localize part of its supply chain in North Africa to ensure better supply reliability and reduced lead times, reinforcing its commitment to the region’s rapidly evolving food processing sector.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Middle East Africa Hydrocolloids Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Middle East Africa Hydrocolloids Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Middle East Africa Hydrocolloids Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.