North America Radio Immunoassay Ria Reagents And Devices Market

Market Size in USD Million

USD

470.00 Million

USD

638.29 Million

2025

2033

USD

470.00 Million

USD

638.29 Million

2025

2033

| 2026 - 2033 | |

| USD 470.00 Million | |

| USD 638.29 Million | |

| % | |

|

North America Radio Immunoassay (RIA) Reagents and Devices Market Size

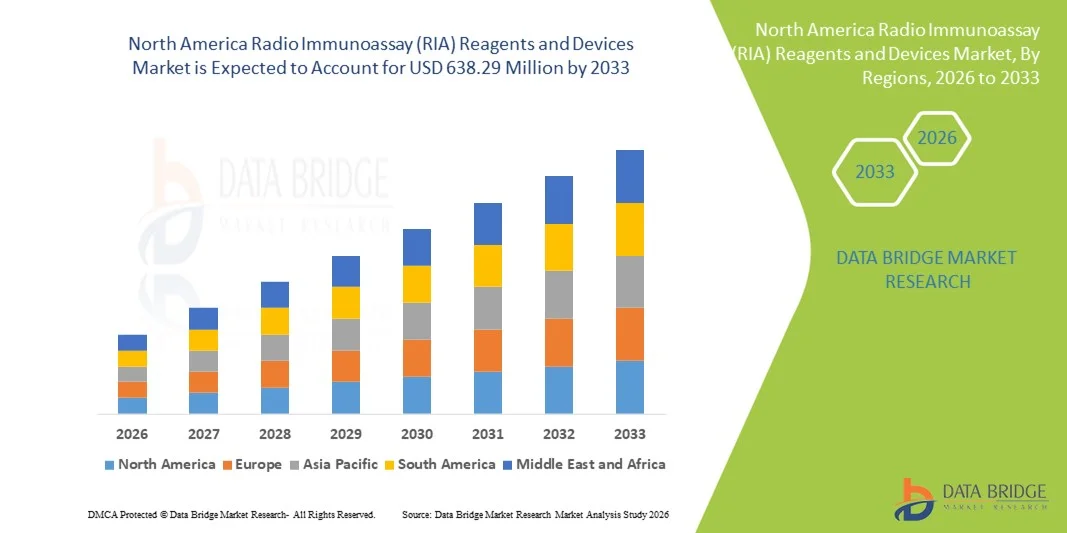

- The North America Radio Immunoassay (RIA) reagents and devices market size was valued at USD 470.00 million in 2025 and is expected to reach USD 638.29 million by 2033, at a CAGR of 3.9% during the forecast period

- The market growth is largely fueled by the increasing demand for highly sensitive and specific diagnostic testing solutions, particularly in endocrinology, oncology, infectious diseases, and therapeutic drug monitoring across clinical laboratories and research institutions

- Furthermore, continuous advancements in immunoassay technologies, expanding healthcare infrastructure, and rising focus on early disease detection and precision diagnostics are strengthening the role of RIA reagents and devices as reliable laboratory tools. These converging factors are accelerating adoption across hospitals, diagnostic centers, and research facilities, thereby significantly boosting the region’s market growth

North America Radio Immunoassay (RIA) Reagents and Devices Market Analysis

- Radio Immunoassay (RIA) reagents and devices, utilized for the highly sensitive quantification of hormones, drugs, and disease markers, remain critical components of clinical diagnostics and biomedical research across hospitals, diagnostic laboratories, and academic institutions due to their proven accuracy, specificity, and reliability in low-concentration analyte detection

- The escalating demand for RIA reagents and devices is primarily fueled by the rising prevalence of endocrine and chronic disorders, increasing demand for early and precise disease diagnosis, and continued reliance on established immunoassay techniques for specialized testing applications

- The United States dominated the North America Radio Immunoassay (RIA) reagents and devices market with the largest revenue share of 78.5% in 2025, characterized by advanced healthcare infrastructure, strong presence of leading diagnostic manufacturers, and high adoption of laboratory automation, with substantial demand across reference laboratories and research centers driven by continuous clinical research activities and stable reimbursement frameworks

- Canada is expected to witness steady growth in the Radio Immunoassay (RIA) reagents and devices market during the forecast period due to expanding diagnostic capabilities, rising investments in healthcare modernization, and increasing focus on specialized laboratory testing services

- Reagents & Kits segment dominated the North America Radio Immunoassay (RIA) reagents and devices market with a market share of 61.4% in 2025, driven by recurring consumption patterns, consistent laboratory testing volumes, and the essential role of assay kits in routine and specialized diagnostic workflows

Report Scope and North America Radio Immunoassay (RIA) Reagents and Devices Market Segmentation

|

Attributes |

North America Radio Immunoassay (RIA) Reagents and Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Radio Immunoassay (RIA) Reagents and Devices Market Trends

Growing Relevance in Specialized and High-Sensitivity Diagnostics

- A significant and accelerating trend in the North America Radio Immunoassay (RIA) reagents and devices market is the sustained demand for highly sensitive immunoassay techniques in endocrinology, oncology, and therapeutic drug monitoring applications. This continued clinical reliance is reinforcing the importance of RIA in specialized laboratory workflows

- For instance, leading diagnostic laboratories across the United States continue to utilize RIA kits for precise hormone level assessment, including thyroid and reproductive hormone testing, where ultra-low concentration detection remains critical

- Technological refinements in assay stability, reagent shelf life, and automation compatibility are enhancing laboratory efficiency and result reproducibility. For instance, modern RIA platforms are being optimized for integration with automated gamma counters and laboratory information systems to streamline diagnostic workflows

- The seamless integration of RIA reagents with broader in-vitro diagnostic platforms supports centralized laboratory operations. Through standardized protocols and improved quality controls, laboratories can manage RIA testing alongside other immunoassay formats within unified diagnostic infrastructures

- This trend toward improved assay reliability, workflow optimization, and compatibility with modern laboratory systems is reshaping expectations for legacy immunoassay technologies. Consequently, manufacturers are investing in advanced reagent formulations and automation-ready systems to maintain RIA’s clinical relevance

- The demand for highly specific and validated RIA kits remains strong across reference laboratories and research institutions, as healthcare providers continue to prioritize diagnostic precision and reproducibility in complex disease management

- In addition, stable reimbursement coverage for specific hormone and therapeutic monitoring tests in the United States is supporting continued utilization of RIA-based assays in clinical laboratories

North America Radio Immunoassay (RIA) Reagents and Devices Market Dynamics

Driver

Rising Prevalence of Endocrine and Chronic Disorders with Expanding Diagnostic Testing

- The increasing incidence of endocrine disorders, cancer cases, and chronic diseases, coupled with expanding diagnostic testing volumes, is a significant driver for the heightened demand for RIA reagents and devices

- For instance, in March 2025, a leading U.S.-based diagnostic laboratory network expanded its specialized hormone testing services to address growing patient volumes, strengthening demand for high-sensitivity immunoassay technologies. Such strategic expansions by laboratory service providers are expected to drive market growth during the forecast period

- As healthcare systems emphasize early disease detection and precise therapeutic monitoring, RIA offers highly accurate quantification of hormones, tumor markers, and drug concentrations, providing reliable clinical decision support

- Furthermore, the strong presence of established diagnostic manufacturers and advanced healthcare infrastructure in the United States and Canada is supporting sustained adoption of RIA technologies in hospitals and reference laboratories

- The growing focus on research activities, including clinical trials and biomarker validation studies, is propelling the utilization of RIA reagents in both academic and biopharmaceutical research settings. The expansion of laboratory automation and standardized testing protocols further contributes to consistent market demand

- Increasing geriatric population across North America, which is more susceptible to hormonal imbalances and chronic illnesses, is further accelerating the demand for sensitive diagnostic testing solutions including RIA

- In addition, ongoing investments in laboratory modernization and infrastructure upgrades are strengthening the capacity of healthcare systems to incorporate advanced immunoassay platforms, supporting long-term market expansion

Restraint/Challenge

Radiation Handling Regulations and Shift Toward Non-Radioactive Alternatives

- Concerns surrounding radiation safety requirements and stringent regulatory compliance for handling radioactive materials pose a significant challenge to broader adoption of RIA technologies. As RIA relies on radioisotopes, laboratories must adhere to strict licensing, storage, and disposal regulations, increasing operational complexity

- For instance, regulatory oversight from nuclear safety authorities in the United States requires laboratories to maintain specific compliance standards for isotope usage, which can discourage smaller facilities from adopting RIA-based testing

- Addressing these regulatory and safety challenges requires ongoing staff training, infrastructure investments, and compliance management systems. In addition, the growing availability of non-radioactive immunoassay alternatives such as ELISA and chemiluminescence assays presents competitive pressure on traditional RIA platforms

- While RIA remains highly sensitive and clinically validated, the operational costs associated with radioactive waste disposal and specialized equipment can limit adoption, particularly in smaller diagnostic centers. The perceived complexity of regulatory adherence may further slow expansion in certain healthcare settings

- Overcoming these challenges through improved isotope management solutions, regulatory support frameworks, and differentiation based on superior analytical sensitivity will be vital for sustained market growth in North America

- Furthermore, supply chain disruptions affecting the availability of medical-grade radioisotopes can impact assay production timelines and laboratory testing continuity

- Competition from fully automated, non-radioisotopic immunoassay platforms offering faster turnaround times may gradually reduce the preference for traditional RIA methodologies in routine diagnostics

North America Radio Immunoassay (RIA) Reagents and Devices Market Scope

The market is segmented on the basis of type, application, and end use.

- By Type

On the basis of type, the North America Radio Immunoassay (RIA) reagents and devices market is segmented into reagents & kits and analyzers. The reagents & kits segment dominated the market with the largest market revenue share of 61.4% in 2025, primarily driven by their recurring consumption in routine and specialized diagnostic procedures. RIA reagents and assay kits are essential components for hormone analysis, tumor marker detection, and therapeutic drug monitoring, ensuring consistent demand across clinical laboratories. The repeat purchase nature of reagents, coupled with the growing volume of endocrine and chronic disease testing, significantly contributes to revenue stability. In addition, advancements in reagent stability, sensitivity, and extended shelf life have improved laboratory efficiency and test accuracy. The strong presence of reference laboratories and hospital-based diagnostic centers in the United States further strengthens the dominance of this segment.

The analyzers segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing laboratory automation and modernization initiatives across North America. Healthcare facilities are increasingly investing in automated gamma counters and integrated diagnostic systems to enhance throughput and reduce manual errors. The growing emphasis on workflow optimization and data integration with laboratory information systems is supporting analyzer adoption. Furthermore, expansion of clinical research activities and pharmaceutical testing is encouraging demand for advanced and high-throughput RIA analyzers. Technological improvements that enhance precision, reduce turnaround time, and improve radiation safety compliance are also contributing to segment growth.

- By Application

On the basis of application, the market is segmented into research and clinical diagnostics. The clinical diagnostics segment dominated the market with the largest revenue share in 2025, driven by the high demand for hormone testing, oncology diagnostics, and therapeutic drug monitoring. Hospitals and diagnostic laboratories rely on RIA for its high sensitivity in detecting low-concentration analytes, particularly in endocrinology. The increasing prevalence of thyroid disorders, reproductive health issues, and chronic diseases across North America supports sustained testing volumes. Established reimbursement frameworks for specific diagnostic assays further strengthen segment stability. In addition, the need for precise and reproducible results in patient management reinforces the clinical reliance on RIA-based testing.

The research segment is expected to witness the fastest growth during the forecast period, supported by expanding biomedical research and pharmaceutical development activities. Academic institutions and biopharmaceutical companies are increasingly utilizing RIA techniques for biomarker validation and drug development studies. The method’s proven sensitivity makes it valuable in experimental protocols requiring accurate quantification. Rising investments in clinical trials and translational research across the United States and Canada are further accelerating adoption. In addition, collaborations between research organizations and diagnostic manufacturers are fostering the development of specialized RIA assays tailored to niche research applications.

- By End Use

On the basis of end use, the market is segmented into hospital, pharmaceutical industry, academics, and clinical diagnostic labs. The clinical diagnostic labs segment dominated the market with the largest revenue share in 2025, attributed to high testing volumes and centralized laboratory operations. Reference laboratories process large numbers of hormone and therapeutic drug monitoring tests daily, ensuring consistent demand for RIA reagents. Their advanced infrastructure and trained personnel enable efficient management of radioactive materials in compliance with regulatory standards. The integration of automated analyzers within these laboratories enhances throughput and operational efficiency. Furthermore, partnerships with hospitals and healthcare providers contribute to steady sample inflow and revenue generation.

The pharmaceutical industry segment is projected to witness the fastest growth from 2026 to 2033, driven by increasing drug development and clinical trial activities. RIA plays a crucial role in pharmacokinetic and pharmacodynamic studies requiring precise quantification of drug concentrations. Growing investments in biologics and hormone-based therapies are further supporting the need for sensitive assay techniques. Pharmaceutical companies are increasingly collaborating with contract research organizations that utilize RIA in specialized testing protocols. In addition, regulatory requirements for accurate drug monitoring and validation processes are reinforcing the adoption of RIA technologies within pharmaceutical research environments.

North America Radio Immunoassay (RIA) Reagents and Devices Market Regional Analysis

- The United States dominated the North America Radio Immunoassay (RIA) reagents and devices market with the largest revenue share of 78.5% in 2025, characterized by advanced healthcare infrastructure, strong presence of leading diagnostic manufacturers, and high adoption of laboratory automation

- Healthcare providers in the region highly value the high sensitivity, specificity, and reliability offered by RIA techniques for hormone quantification, oncology diagnostics, and therapeutic drug monitoring, particularly in complex disease management scenarios

- This widespread adoption is further supported by robust reimbursement frameworks, increasing prevalence of endocrine and chronic disorders, and substantial investments in laboratory automation and biomedical research, establishing RIA reagents and devices as essential components of diagnostic and research workflows across hospitals, reference laboratories, and pharmaceutical companies

The U.S. Radio Immunoassay (RIA) Reagents and Devices Market Insight

The U.S. Radio Immunoassay (RIA) reagents and devices market captured the largest revenue share within North America in 2025, driven by advanced healthcare infrastructure and high diagnostic testing volumes across hospitals and reference laboratories. Clinical laboratories in the country continue to rely on RIA for highly sensitive hormone quantification, oncology marker analysis, and therapeutic drug monitoring. The growing prevalence of endocrine disorders and chronic diseases is significantly strengthening demand for accurate immunoassay solutions. Moreover, strong reimbursement frameworks and substantial investments in biomedical research are further contributing to sustained market expansion.

Canada Radio Immunoassay (RIA) Reagents and Devices Market Insight

The Canada Radio Immunoassay (RIA) reagents and devices market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by expanding diagnostic capabilities and modernization of laboratory infrastructure. Increasing focus on early disease detection and precision medicine is fostering the adoption of highly sensitive immunoassay technologies. Canadian healthcare institutions emphasize reliable and standardized testing procedures, supporting the continued use of RIA in specialized diagnostics. In addition, growing investments in clinical research and academic collaborations are expected to stimulate consistent market growth across hospitals and research laboratories.

Mexico Radio Immunoassay (RIA) Reagents and Devices Market Insight

The Mexico Radio Immunoassay (RIA) reagents and devices market is expected to witness moderate growth during the forecast period, supported by improving healthcare access and gradual expansion of diagnostic laboratory networks. Rising awareness regarding early disease diagnosis and increasing prevalence of chronic and endocrine disorders are contributing to demand for specialized immunoassay testing. Public and private sector investments in healthcare infrastructure modernization are enhancing laboratory capabilities across major urban centers. Furthermore, growing collaboration with international diagnostic manufacturers is facilitating technology transfer and improving the availability of RIA reagents and equipment in the country.

North America Radio Immunoassay (RIA) Reagents and Devices Market Share

The North America Radio Immunoassay (RIA) Reagents and Devices industry is primarily led by well-established companies, including:

- PerkinElmer Inc. (U.S.)

- Beckman Coulter, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Abbott (U.S.)

- Bio‑Rad Laboratories, Inc. (U.S.)

- DRG International, Inc. (U.S.)

- MP Biomedicals, LLC (U.S.)

- MilliporeSigma (U.S.)

- iZotope, Inc. (U.S.)

- DIAsource (U.S.)

- Luminex Corporation (U.S.)

- Ortho Clinical Diagnostics (U.S.)

- Agilent Technologies, Inc. (U.S.)

- BD (U.S.)

- Bio‑Techne Corporation (U.S.)

- Quidel Corporation (U.S.)

- Ortho‑Clinical Diagnostics (U.S.)

- Randox Laboratories Ltd. (U.K.)

- Solaris Diagnostics (U.S.)

What are the Recent Developments in North America Radio Immunoassay (RIA) Reagents and Devices Market?

- In April 2025, DiaSorin Group announced the acquisition of the diagnostic immunoassay business of Bio-Rad Laboratories, expanding DiaSorin’s clinical immunoassay portfolio with technologies that include highly sensitive assays applicable to RIA-style diagnostic platforms

- In January 2025, the U.S. Food and Drug Administration (FDA) cleared a new automated immunoassay test (though not strictly RIA) for quantitative hormone detection on platforms used commonly in clinical labs a regulatory news development that impacts high-precision hormone detection technologies closely related to traditional RIA tests

- In May 2024, PerkinElmer publicly confirmed a strategic collaboration with the University of California, San Francisco (UCSF) to co-develop advanced immunoassay research platforms, supporting enhanced RIA-relevant assay development for academic and clinical research use

- In February 2024, the U.S. Department of Energy Isotope Program announced that Oak Ridge National Laboratory (ORNL) restarted domestic production of Iridium-192 (Ir-192) a widely used medical radioisotope that supports various nuclear diagnostics, including RIA workflows in clinical labs, after nearly two decades

- In November 2023, global news outlets reported that radioactive isotope shortages were affecting cancer diagnostics in the U.S. and Europe due to nuclear reactor outages highlighting supply challenges for radioisotopes used in RIA tests and nuclear medicine more broadly

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.