هناك زيادة مماثلة في الطلب على المواد التي يمكن أن تلبي المتطلبات المتنوعة لهذه العملية التصنيعية المبتكرة مع تبني الصناعات للقدرات الثورية للطباعة ثلاثية الأبعاد. يمتد تنوع الطباعة ثلاثية الأبعاد، والمعروف أيضًا باسم التصنيع الإضافي، إلى صناعات مثل الفضاء والرعاية الصحية والسيارات والسلع الاستهلاكية، حيث تُستخدم هذه التقنية في النماذج الأولية السريعة والإنتاج المخصص وتصنيع التصميمات المعقدة. العامل الذي يساهم في الطلب على مواد الطباعة ثلاثية الأبعاد هو قدرة التقنية على إنتاج مكونات معقدة ومخصصة للغاية. طرق التصنيع التقليدية ليست فعالة وسريعة للغاية حيث تسعى الصناعات إلى أجزاء أكثر تعقيدًا ودقة في التصميم. تعالج الطباعة ثلاثية الأبعاد هذه الفجوة من خلال السماح بإنشاء هياكل هندسية معقدة بكفاءة محسنة. وهذا يتطلب مجموعة واسعة من المواد المصممة لتطبيقات مختلفة - تتراوح من البلاستيك والمعادن إلى السيراميك والمواد المركبة. وبالتالي فإن تنوع تقنية الطباعة ثلاثية الأبعاد يدفع الطلب على مواد متنوعة يمكنها تلبية احتياجات صناعية محددة.

يمكنك الوصول إلى التقرير الكامل على https://www.databridgemarketresearch.com/reports/europe-3d-printing-materials-market

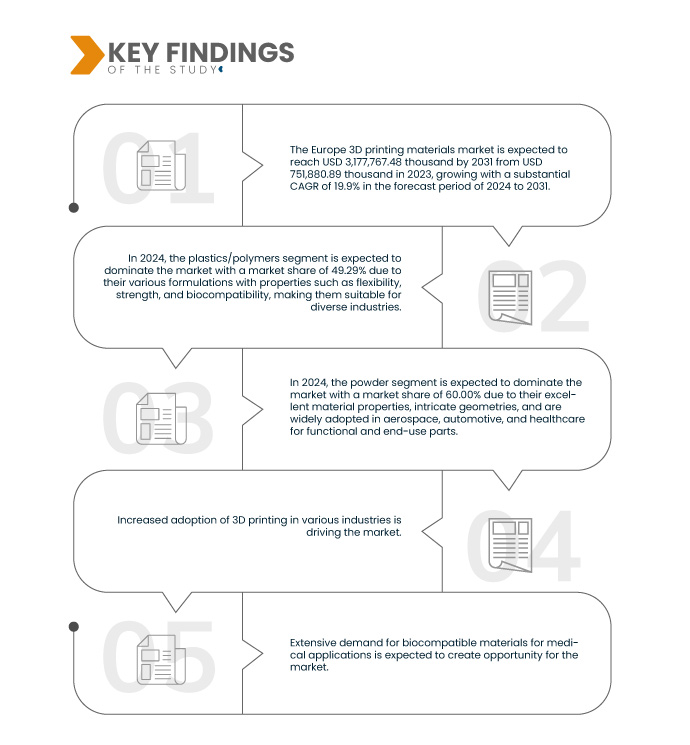

تحلل شركة Data Bridge Market Research أن سوق مواد الطباعة ثلاثية الأبعاد في أوروبا من المتوقع أن يصل إلى 3،177،767.48 ألف دولار أمريكي بحلول عام 2031، من 751،880.89 ألف دولار أمريكي في عام 2023، بنمو قدره 19.9٪ في الفترة المتوقعة من 2024 إلى 2031.

النتائج الرئيسية للدراسة

توسيع إمكانية الوصول إلى تقنيات الطباعة ثلاثية الأبعاد وقدرتها على تحمل التكاليف

هذا الارتفاع الكبير في اعتماد الطباعة ثلاثية الأبعاد يدفع الطلب على مجموعة متنوعة من المواد المناسبة لتطبيقات متنوعة. أصبحت مواد تتراوح من البوليمرات والمعادن إلى السيراميك والمواد المركبة جزءًا لا يتجزأ من تطبيقات وتقنيات الطباعة ثلاثية الأبعاد. وقد أدى تزايد إمكانية الوصول إلى هذه التقنيات إلى تنوع قاعدة المستخدمين، ولكل منهم متطلبات مادية فريدة. كما عززت سهولة الوصول إلى الطباعة ثلاثية الأبعاد ورخص أسعارها الابتكار في تطوير المواد. ويستثمر الباحثون والمصنعون في ابتكار مواد متخصصة تلبي الاحتياجات المتطورة لمختلف التطبيقات. وقد أدى ذلك إلى ظهور مواد متقدمة ذات خصائص مُحسّنة، مثل القوة والمرونة ومقاومة الحرارة المُحسّنة. وقد أدى ذلك إلى توسيع نطاق السوق المستهدفة لمواد الطباعة ثلاثية الأبعاد، مما أدى إلى زيادة استهلاك المواد.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

من 2024 إلى 2031

|

سنة الأساس

|

2023

|

السنوات التاريخية

|

2022 (قابلة للتخصيص حتى 2016-2021)

|

الوحدات الكمية

|

الإيرادات بالألف دولار أمريكي

|

القطاعات المغطاة

|

النوع (البلاستيك/البوليمرات، المعادن، السيراميك، وغيرها)، الشكل (مسحوق، خيوط، وسائل)، التكنولوجيا (نمذجة الترسيب المندمج (FDM)، التلبيد الانتقائي بالليزر (SLS)، الطباعة الضوئية المجسمة (SLA)، التلبيد المباشر بالليزر للمعادن (DMLS)، التصنيع الإضافي لمناطق كبيرة (BAAM)، التصنيع الإضافي لقوس الأسلاك (WAAM)، ColorJet، وغيرها)، الاستخدام النهائي (التصنيع الصناعي، السيارات، الفضاء والدفاع، الرعاية الصحية، السلع الاستهلاكية، الإلكترونيات، التعليم، البناء، وغيرها)

|

الدول المغطاة

|

ألمانيا، إيطاليا، المملكة المتحدة، فرنسا، إسبانيا، تركيا، روسيا، سويسرا، بلجيكا، هولندا، لوكسمبورج، وبقية أوروبا

|

الجهات الفاعلة في السوق المغطاة

|

Formlabs (الولايات المتحدة)، EOS (ألمانيا)، ENVISIONTEC US LLC (الولايات المتحدة)، American Elements (الولايات المتحدة)، Höganäs AB (السويد)، UltiMaker (هولندا)، Carbon, Inc. (الولايات المتحدة)، KRAIBURG TPE GmbH & Co. KG (ألمانيا)، Covestro AG (ألمانيا)، Markforged, Inc. (الولايات المتحدة)، Stratasys (الولايات المتحدة)، ExOne (الولايات المتحدة)، Arkema (فرنسا)، 3D Systems, Inc. (اليابان)، Evonik Industries AG (ألمانيا)، Materialise (بلجيكا)، BASF SE (ألمانيا)، Solvay (بلجيكا)، وSandvik AB (السويد)، وغيرها.

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، تتضمن تقارير السوق التي أعدتها شركة Data Bridge Market Research أيضًا تحليلًا متعمقًا من الخبراء والإنتاج والقدرة التمثيلية الجغرافية للشركة وتخطيطات الشبكة للموزعين والشركاء وتحليل اتجاهات الأسعار التفصيلية والمحدثة وتحليل العجز في سلسلة التوريد والطلب.

|

تحليل القطاعات

يتم تقسيم سوق مواد الطباعة ثلاثية الأبعاد في أوروبا إلى أربعة قطاعات بارزة بناءً على النوع والشكل والتكنولوجيا والاستخدام النهائي.

- على أساس النوع، يتم تقسيم سوق مواد الطباعة ثلاثية الأبعاد في أوروبا إلى البلاستيك/البوليمرات والمعادن والسيراميك وغيرها

في عام 2024، من المتوقع أن يهيمن قطاع البلاستيك/البوليمرات على سوق مواد الطباعة ثلاثية الأبعاد في أوروبا

ومن المتوقع أن تهيمن شريحة البلاستيك/البوليمرات على السوق في عام 2024 بحصة سوقية تبلغ 49.29% بسبب تركيباتها المتنوعة ذات الخصائص مثل المرونة والقوة والتوافق الحيوي، مما يجعلها مناسبة لصناعات متنوعة.

- على أساس الشكل، يتم تقسيم سوق مواد الطباعة ثلاثية الأبعاد في أوروبا إلى مسحوق وخيوط وسائل

من المتوقع أن يهيمن قطاع المسحوق على سوق مواد الطباعة ثلاثية الأبعاد في أوروبا في عام 2024

من المتوقع أن تهيمن شريحة المسحوق على السوق في عام 2024 بحصة سوقية تبلغ 60.00%، حيث توفر العمليات القائمة على المسحوق خصائص مادية ممتازة وهندسة معقدة، ويتم اعتمادها على نطاق واسع في صناعات الطيران والسيارات والرعاية الصحية للأجزاء الوظيفية والاستخدام النهائي.

- بناءً على التكنولوجيا، يُقسّم سوق مواد الطباعة ثلاثية الأبعاد في أوروبا إلى نمذجة الترسيب المندمج (FDM)، والتلبيد الانتقائي بالليزر (SLS)، والطباعة المجسمة (SLA)، والتلبيد المباشر بالليزر المعدني (DMLS)، والتصنيع الإضافي لمناطق واسعة (BAAM)، والتصنيع الإضافي لقوس الأسلاك (WAAM)، والطباعة بالألوان، وغيرها. في عام 2024، من المتوقع أن يهيمن قطاع نمذجة الترسيب المندمج (FDM) على السوق بحصة سوقية تبلغ 35.95%.

- بناءً على الاستخدام النهائي، يُقسّم سوق مواد الطباعة ثلاثية الأبعاد في أوروبا إلى قطاعات التصنيع الصناعي، والسيارات، والفضاء والدفاع، والرعاية الصحية، والسلع الاستهلاكية، والإلكترونيات، والتعليم، والبناء، وغيرها. ومن المتوقع أن يهيمن قطاع التصنيع الصناعي على السوق بحصة سوقية تبلغ 21.13% في عام 2024.

اللاعبون الرئيسيون

قامت شركة Data Bridge Market Research بتحليل شركات Stratasys (الولايات المتحدة)، وEOS (ألمانيا)، و3D Systems, Inc. (اليابان)، وBASF SE (ألمانيا)، وMaterialise (بلجيكا) باعتبارها اللاعبين الرئيسيين في سوق مواد الطباعة ثلاثية الأبعاد في أوروبا.

تطورات السوق

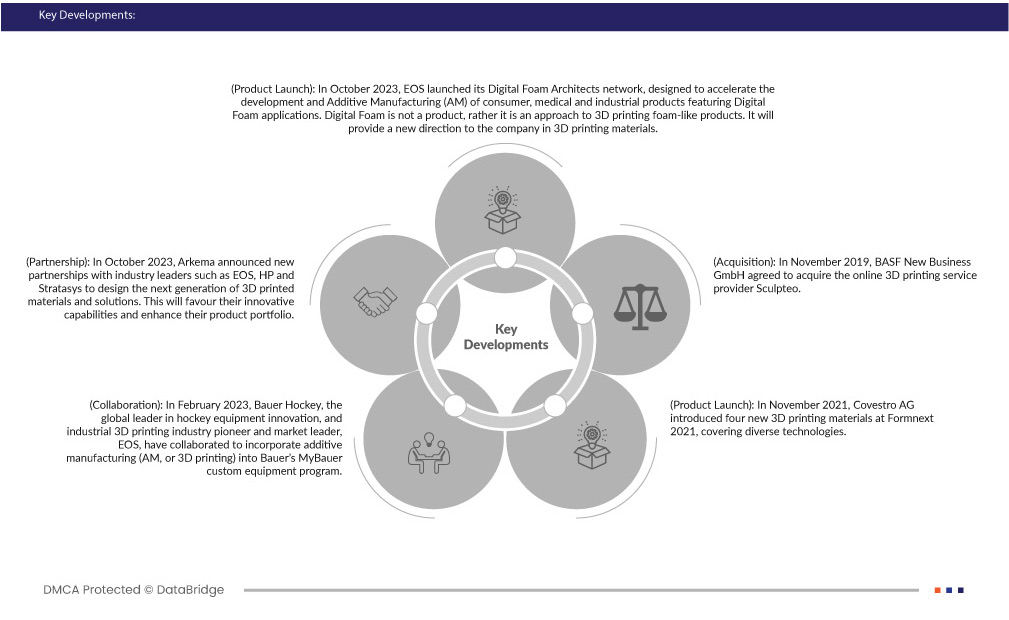

- في أكتوبر 2023، أطلقت شركة EOS شبكة "مهندسي الرغوة الرقمية"، المصممة لتسريع تطوير وتصنيع المنتجات الاستهلاكية والطبية والصناعية التي تستخدم تطبيقات الرغوة الرقمية. "الرغوة الرقمية" ليست منتجًا، بل هي نهج لطباعة منتجات شبيهة بالرغوة ثلاثية الأبعاد. وستوفر هذه الشبكة توجهًا جديدًا للشركة في مجال مواد الطباعة ثلاثية الأبعاد.

- في أكتوبر 2023، أعلنت أركيما عن شراكات جديدة مع شركات رائدة في هذا المجال، مثل EOS وHP وStratasys، لتصميم الجيل القادم من مواد وحلول الطباعة ثلاثية الأبعاد. سيعزز هذا قدراتها الابتكارية ويعزز محفظة منتجاتها.

- في فبراير 2023، تعاونت شركة باور هوكي، الرائدة في أوروبا في مجال ابتكار معدات الهوكي، مع شركة EOS، الرائدة في مجال الطباعة ثلاثية الأبعاد الصناعية والرائدة في السوق، لدمج التصنيع الإضافي (AM، أو الطباعة ثلاثية الأبعاد) في برنامج MyBauer للمعدات المخصصة من باور. وقد منحت EOS، ومنهجها الحاصل على براءة اختراع في طباعة البوليمرات بتقنية الرغوة الرقمية، باور، ميزةً مميزة. وسيعزز هذا حضور EOS في سوق مواد الطباعة ثلاثية الأبعاد في أوروبا.

- في نوفمبر 2021، طرحت شركة Covestro AG أربع مواد جديدة للطباعة ثلاثية الأبعاد في معرض Formnext 2021، تغطي تقنيات متنوعة. من بينها Addigy FPC SOL1 HT، وهي مادة دعم قابلة للذوبان تُستخدم في طباعة FDM للمواد عالية الحرارة، وتتميز بسهولة إزالتها واستدامة أدائها. كما حققت مادة Arnitel AM3001 (P) المخصصة لـ SLS، وهي مادة ناعمة ذات عائد طاقة مرتفع، نجاحًا في الطباعة ثلاثية الأبعاد مع الالتزام بمعايير سلامة الألعاب. كما أطلقت Covestro إصدارات SLS وHSS من مسحوق TPU الخاص بها، Addigy PPU 86AW6، المعروف بقدرته على الارتداد، وسهولة معالجته لاحقًا، وارتفاع معدل إعادة استخدامه. تُوسّع هذه الإضافات خيارات Covestro من البوليمرات للطباعة ثلاثية الأبعاد، بعد استحواذها على أعمال التصنيع الإضافي التابعة لشركة DSM في وقت سابق من هذا العام.

- في نوفمبر 2019، وافقت شركة باسف نيو بيزنس جي إم بي إتش على الاستحواذ على شركة سكالبتيو، مُزود خدمات الطباعة ثلاثية الأبعاد عبر الإنترنت. وُقِّعت الاتفاقية في 14 نوفمبر 2019، وكان من المتوقع أن تدخل حيز التنفيذ خلال الأسابيع القليلة المقبلة، بانتظار موافقة الجهات التنظيمية المختصة. وقد مكّن الاستحواذ على الشركة الفرنسية المتخصصة في الطباعة ثلاثية الأبعاد، ومقرها باريس وسان فرانسيسكو، شركة باسف ثري دي برينتينغ سوليوشنز جي إم بي إتش، وهي شركة تابعة مملوكة بالكامل لشركة باسف نيو بيزنس جي إم بي إتش، من تسويق وتطوير مواد طباعة ثلاثية الأبعاد صناعية جديدة بسرعة أكبر، مما عزز القدرة الإنتاجية لشركة باسف.

التحليل الإقليمي

من الناحية الجغرافية، البلدان التي تغطيها سوق مواد الطباعة ثلاثية الأبعاد في أوروبا هي ألمانيا وإيطاليا والمملكة المتحدة وفرنسا وإسبانيا وتركيا وروسيا وسويسرا وبلجيكا وهولندا ولوكسمبورج وبقية أوروبا.

وفقًا لتحليل Data Bridge Market Research:

من المتوقع أن تكون ألمانيا الدولة المهيمنة والأسرع نموًا في سوق مواد الطباعة ثلاثية الأبعاد في أوروبا

ومن المتوقع أن تكون ألمانيا الدولة المهيمنة والأسرع نمواً في السوق بسبب توسع إمكانية الوصول إلى تقنيات الطباعة ثلاثية الأبعاد وبأسعار معقولة في البلاد.

لمزيد من المعلومات التفصيلية حول تقرير سوق مواد الطباعة ثلاثية الأبعاد في أوروبا، انقر هنا - https://www.databridgemarketresearch.com/reports/europe-3d-printing-materials-market