يلبي سوق الأدوات الكهربائية احتياجات مجموعة واسعة من المستخدمين النهائيين، مقسمين بشكل رئيسي إلى قطاعين: الصناعي/المهني والسكني. يشمل هذا القطاع قطاعات البناء والتصنيع ومختلف المهن، معتمدين على الأدوات الكهربائية لتحقيق الدقة والكفاءة. أما المستخدمون السكنيون، بمن فيهم هواة الأعمال اليدوية، فيستخدمون الأدوات الكهربائية في مشاريعهم المنزلية. تتكون قنوات البيع من المبيعات غير المباشرة، التي تشمل الموزعين وتجار التجزئة، والمبيعات المباشرة، حيث يبيع المصنعون منتجاتهم مباشرةً للعملاء. يضمن هذا التنوع سهولة الوصول إلى الأدوات الكهربائية وفعاليتها في مختلف الصناعات والتطبيقات.

يمكنك الوصول إلى التقرير الكامل على https://www.databridgemarketresearch.com/reports/europe-power-tools-market

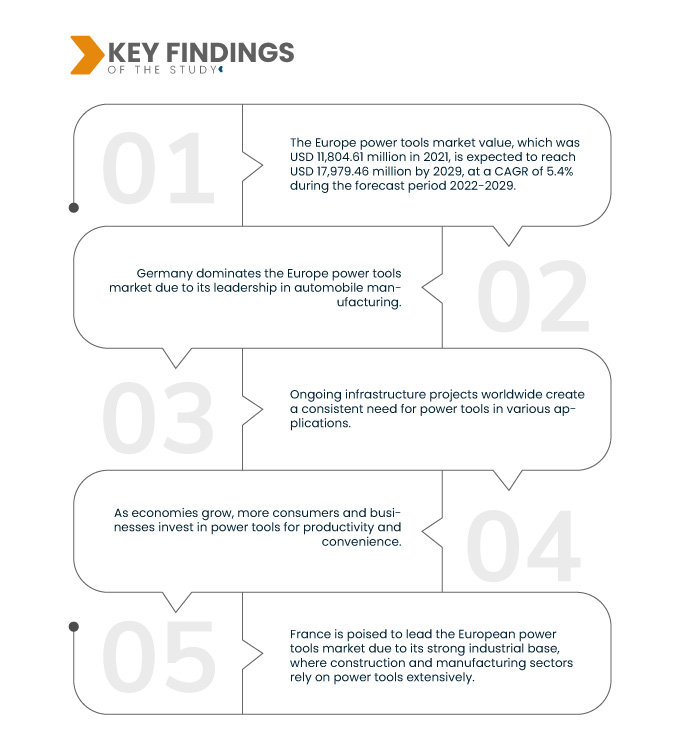

تشير تحليلات شركة داتا بريدج لأبحاث السوق إلى أن قيمة سوق الأدوات الكهربائية في أوروبا ، والتي بلغت 11,804.61 مليون دولار أمريكي في عام 2021، من المتوقع أن تصل إلى 17,979.46 مليون دولار أمريكي بحلول عام 2029، بمعدل نمو سنوي مركب قدره 5.4% خلال الفترة المتوقعة 2022-2029. ويُعد الإقبال المتزايد على مشاريع "اصنعها بنفسك" بين أصحاب المنازل والهواة محركًا رئيسيًا لسوق الأدوات الكهربائية. ويعزز هذا التوجه الطلب على الأدوات الكهربائية المنزلية، حيث يسعى المزيد من الأفراد إلى أدوات لتحسين منازلهم ومشاريعهم الإبداعية.

النتائج الرئيسية للدراسة

ومن المتوقع أن يؤدي النمو الصناعي إلى دفع معدل نمو السوق

يُحفّز التصنيع السريع وازدهار قطاع البناء سوق الأدوات الكهربائية من خلال خلق طلب قوي في مختلف القطاعات. تعتمد قطاعات التصنيع والبناء بشكل كبير على الأدوات الكهربائية لتحقيق الدقة والكفاءة والإنتاجية. علاوة على ذلك، يُسهم توسّع البنية التحتية ومشاريع العقارات حول العالم في زيادة الحاجة إلى الأدوات الكهربائية. ومع نمو هذه القطاعات، يشهد السوق طلبًا ثابتًا، مما يجعل أنشطة التصنيع والبناء محركًا رئيسيًا في صناعة الأدوات الكهربائية.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

من 2022 إلى 2029

|

سنة الأساس

|

2021

|

السنوات التاريخية

|

2020 (قابلة للتخصيص حتى 2014-2019)

|

الوحدات الكمية

|

الإيرادات بالملايين من الدولارات الأمريكية، والحجم بالوحدات، والتسعير بالدولار الأمريكي

|

القطاعات المغطاة

|

النوع (أدوات النشر والقطع، أدوات الحفر والتثبيت، أدوات الهدم، المسامير، أدوات التوجيه، قواطع محمولة، أدوات تعمل بالهواء المضغوط، أدوات إزالة المواد، الأسلاك والمقابس الكهربائية، ملحقات الأزاميل، وغيرها)، طريقة التشغيل (كهربائية، أداة تعمل بالوقود السائل، هيدروليكية، هوائية، أدوات تعمل بالمسحوق)، التطبيق (الخرسانة والبناء، النجارة، تشغيل المعادن، اللحام، وغيرها)، المادة (الخرسانة، الخشب/المعادن، الطوب/البلوك، الزجاج، وغيرها)، المستخدم النهائي (صناعي/مهني، سكني)، قناة المبيعات (المبيعات غير المباشرة، المبيعات المباشرة)

|

الدول المغطاة

|

ألمانيا، فرنسا، المملكة المتحدة، هولندا، سويسرا، بلجيكا، روسيا، إيطاليا، إسبانيا، تركيا، بقية دول أوروبا في أوروبا.

|

الجهات الفاعلة في السوق المغطاة

|

أطلس كوبكو (السويد)، ستانلي بلاك آند ديكر (الولايات المتحدة)، سناب أون (الولايات المتحدة)، روبرت بوش (ألمانيا)، كوكي هولدينغز المحدودة (اليابان)، إيمرسون إلكتريك (الولايات المتحدة)، فيستول (ألمانيا)، كيوسيرا (اليابان)، إنجرسول راند (أيرلندا)، ماكيتا (اليابان)، هيلتي (ليختنشتاين)، هوسكفارنا (السويد)، باناسونيك أوروبا (شركة تابعة لشركة باناسونيك) (هولندا)، تيكترونيك إندستريز المحدودة (هونغ كونغ)، أبيكس تول جروب (الولايات المتحدة)، 3 إم (الولايات المتحدة)، دلتا باور إكويبمنت (الولايات المتحدة)، سي آند إي فين (ألمانيا)

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، تتضمن تقارير السوق التي تم تنظيمها بواسطة Data Bridge Market Research أيضًا تحليلًا متعمقًا من الخبراء والإنتاج والقدرة التمثيلية الجغرافية للشركة وتخطيطات الشبكة للموزعين والشركاء وتحليل اتجاهات الأسعار التفصيلية والمحدثة وتحليل العجز في سلسلة التوريد والطلب.

|

تحليل القطاعات:

يتم تقسيم سوق أدوات الطاقة في أوروبا على أساس النوع وطريقة التشغيل والتطبيق والمادة والمستخدم النهائي وقناة المبيعات.

- على أساس النوع، يتم تقسيم السوق إلى أدوات النشر والقطع، وأدوات الحفر والتثبيت، وأدوات الهدم، والمسامير، وأدوات التوجيه، والقواطع المحمولة، والأدوات التي تعمل بالهواء المضغوط، وأدوات إزالة المواد، والأسلاك والمقابس الكهربائية، والأزاميل، والملحقات، وغيرها.

- على أساس طريقة التشغيل، يتم تقسيم السوق إلى أدوات كهربائية، وأدوات تعمل بالوقود السائل، وأدوات هيدروليكية، وأدوات تعمل بالهواء المضغوط، وأدوات تعمل بالمسحوق.

- على أساس التطبيق، يتم تقسيم السوق إلى الخرسانة والبناء، والنجارة، والعمل المعدني، واللحام، وغيرها.

- على أساس المادة، يتم تقسيم السوق إلى الخرسانة والخشب / المعادن والطوب / الكتل والزجاج وغيرها.

- على أساس المستخدم النهائي، يتم تقسيم السوق إلى صناعي/مهني، وسكني.

- على أساس قناة المبيعات، يتم تقسيم السوق إلى مبيعات غير مباشرة، ومبيعات مباشرة.

اللاعبون الرئيسيون

تعترف شركة Data Bridge Market Research بالشركات التالية باعتبارها اللاعبين الرئيسيين في سوق أدوات الطاقة في أوروبا وهي Atlas Copco AB (السويد)، وStanley Black & Decker, Inc. (الولايات المتحدة)، وSnap-on Incorporated (الولايات المتحدة)، وRobert Bosch GmbH (ألمانيا)، وKoki Holdings Co.، Ltd. (اليابان)، وEmerson Electric Co. (الولايات المتحدة)، وFestool GmbH (ألمانيا)، وKYOCERA Corporation (اليابان).

تطورات السوق

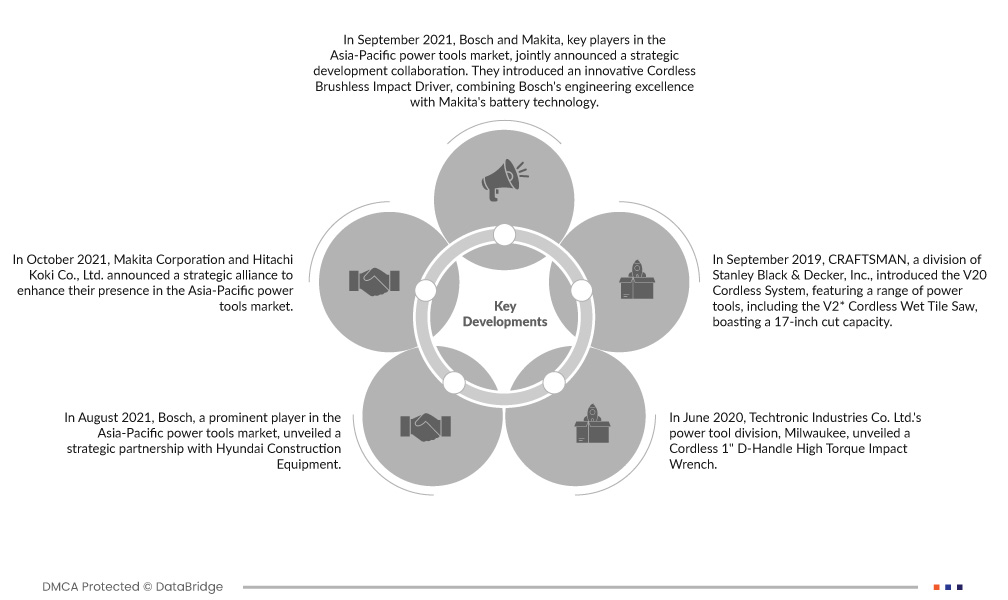

- في سبتمبر 2021، أعلنت بوش وماكيتا، الشركتان الرائدتان في سوق الأدوات الكهربائية في منطقة آسيا والمحيط الهادئ، عن تعاون استراتيجي في مجال التطوير. وقد طرحتا مفك براغي لاسلكي مبتكر بدون فرشاة، يجمع بين التميز الهندسي لبوش وتقنية بطاريات ماكيتا. يوفر هذا المنتج كفاءة فائقة في تطبيقات التثبيت، ويمثل إنجازًا هامًا في تعاونهما، إذ يُحسّن أداء الأدوات ويزيد من رضا العملاء.

- في أكتوبر 2021، أعلنت شركة ماكيتا وشركة هيتاشي كوكي المحدودة عن تحالف استراتيجي لتعزيز حضورهما في سوق الأدوات الكهربائية في منطقة آسيا والمحيط الهادئ. وستُطوّر هذه الشراكة أدوات لاسلكية متطورة وحلولاً مبتكرة، بالاستفادة من خبرات الشركتين. ومن المتوقع أن يُسهم هذا التعاون في تعزيز ابتكار المنتجات وتوسيع نطاق وصولهما إلى السوق في المنطقة.

- في أغسطس 2021، أعلنت شركة بوش، الرائدة في سوق الأدوات الكهربائية في منطقة آسيا والمحيط الهادئ، عن شراكة استراتيجية مع شركة هيونداي لمعدات البناء. تركز هذه الشراكة على دمج أدوات بوش الكهربائية اللاسلكية المبتكرة مع معدات هيونداي الثقيلة، مما يعزز الكفاءة والأداء في مواقع البناء. ويهدف هذا التعاون إلى تقديم حلول بناء فائقة من خلال دمج أحدث الأدوات والمعدات.

- في يونيو 2020، كشفت ميلووكي، قسم الأدوات الكهربائية في شركة تيكترونيك إندستريز المحدودة، عن مفتاح ربط صدمي لاسلكي عالي عزم الدوران بمقبض على شكل حرف D مقاس بوصة واحدة. صُمم هذا المنتج لتثبيت براغي بقياس بوصتين، ويتميز بعزم دوران مذهل يصل إلى 2000 رطل-قدم، مما يجعله إضافة قوية ومتعددة الاستخدامات لأدوات السوق.

- في سبتمبر 2019، طرحت شركة كرافتسمان، التابعة لشركة ستانلي بلاك آند ديكر، نظام V20 اللاسلكي، الذي يضم مجموعة من الأدوات الكهربائية، بما في ذلك منشار البلاط الرطب اللاسلكي V2*، الذي يتميز بقدرة قطع تصل إلى 17 بوصة. وقد مثّل هذا الابتكار إضافةً مهمةً إلى خط إنتاجها، مما عزز تنوع وقدرات نظام V20 اللاسلكي.

التحليل الإقليمي

جغرافيًا، البلدان التي يغطيها تقرير سوق أدوات الطاقة في أوروبا هي ألمانيا وفرنسا والمملكة المتحدة وهولندا وسويسرا وبلجيكا وروسيا وإيطاليا وإسبانيا وتركيا وبقية دول أوروبا في أوروبا

وفقًا لتحليل Data Bridge Market Research:

ألمانيا هي المنطقة المهيمنة في سوق الأدوات الكهربائية في أوروبا خلال الفترة المتوقعة 2022-2029

تُهيمن ألمانيا على سوق الأدوات الكهربائية الأوروبية بفضل ريادتها في تصنيع السيارات. يعتمد قطاع السيارات بشكل كبير على الأدوات الكهربائية في عمليات التجميع، مما يُسهم بشكل كبير في نمو سوق الأدوات الكهربائية. وتُعدّ قاعدة التصنيع القوية في ألمانيا ودورها المحوري في إنتاج السيارات محركًا رئيسيًا لقطاع الأدوات الكهربائية في المنطقة الأوروبية.

من المتوقع أن تهيمن فرنسا على سوق الأدوات الكهربائية في أوروبا في الفترة المتوقعة 2022-2029

فرنسا مهيأة لقيادة سوق الأدوات الكهربائية الأوروبية بفضل عدة عوامل. فهي تتمتع بقاعدة صناعية متينة، حيث يعتمد قطاعا البناء والتصنيع على الأدوات الكهربائية بشكل كبير. إضافةً إلى ذلك، يُعزز الاستثمار المتزايد في تطوير البنية التحتية وتنامي ثقافة "اصنعها بنفسك" بين المستهلكين الطلب. كما أن موقع فرنسا الاستراتيجي ونفوذها الاقتصادي في أوروبا يجعلها لاعبًا رئيسيًا في سوق الأدوات الكهربائية المزدهر في جميع أنحاء القارة.

لمزيد من المعلومات التفصيلية حول تقرير سوق أدوات الطاقة في أوروبا، انقر هنا - https://www.databridgemarketresearch.com/reports/europe-power-tools-market