تشمل اضطرابات العمود الفقري مجموعة واسعة من الحالات التي تؤثر على العمود الفقري والحبل الشوكي والهياكل المرتبطة به. تساهم عدة عوامل في زيادة حالات اضطرابات العمود الفقري، وبالتالي في زيادة الطلب على مواد الطعوم الشوكية. يمكن أن تساهم أنماط الحياة العصرية، التي قد تشمل الجلوس لفترات طويلة، وقلة النشاط البدني، وسوء وضعية الجسم، في تطور اضطرابات العمود الفقري. يمكن لهذه العوامل أن تُسرّع من تآكل هياكل العمود الفقري وتزيد من خطر الإصابة بحالات مثل الانزلاق الغضروفي والتنكس القطني. يمكن أن تؤدي الإصابات الرضحية، مثل حوادث السيارات، والسقوط، والإصابات الرياضية، إلى كسور وخلع في العمود الفقري، وغيرها من اضطرابات العمود الفقري الشديدة. غالبًا ما تتطلب هذه الإصابات تدخلات جراحية واستخدام مواد الطعوم لإعادة بناء العمود الفقري.

إن الارتفاع المتزايد في حالات اضطرابات العمود الفقري يؤكد أهمية خيارات العلاج الفعالة، بما في ذلك الطعوم الشوكية، لمعالجة هذه الحالات وتحسين نوعية حياة المرضى.

يمكنك الوصول إلى التقرير الكامل على https://www.databridgemarketresearch.com/reports/europe-spinal-allografts-and-xenograft-market

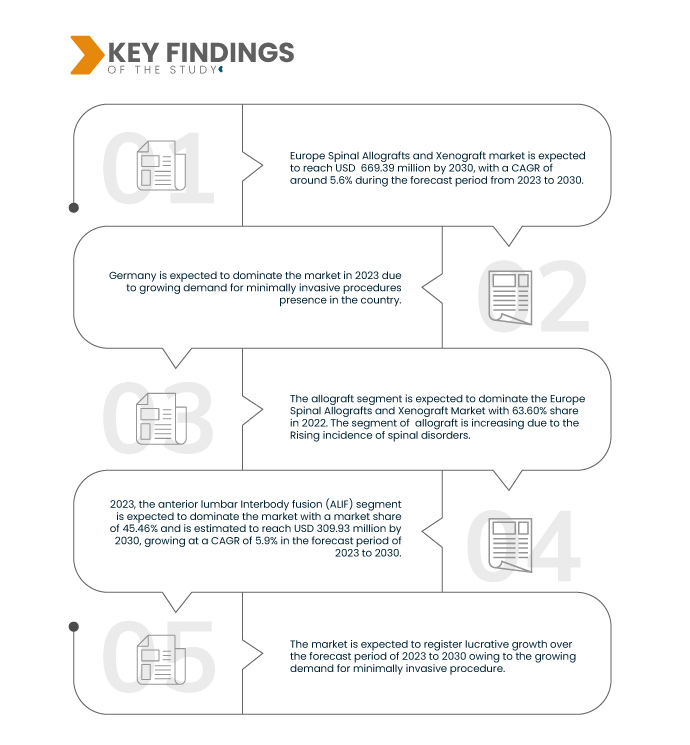

تحلل شركة Data Bridge Market Research أن سوق الطعوم الشوكية والزرع الغريب في أوروبا من المتوقع أن ينمو بمعدل نمو سنوي مركب قدره 5.6٪ في الفترة المتوقعة من 2023 إلى 2030 ومن المتوقع أن يصل إلى 669.39 مليون دولار أمريكي بحلول عام 2030. ومن المتوقع أن يدفع قطاع الطعوم الشوكية نمو السوق بسبب التقدم في التقنيات الجراحية المستخدمة في الطعوم الشوكية.

النتائج الرئيسية للدراسة

التطورات في الطب التجديدي

الطب التجديدي هو مجال سريع التطور يركز على تسخير قدرة الجسم الطبيعية على إصلاح وتجديد الأنسجة. تلعب الطعوم الخيفية والغريبة دورًا حاسمًا في الطب التجديدي من خلال العمل كمواد طعوم لإجراءات إصلاح الأنسجة والأعضاء المختلفة. تعمل تقنيات الطب التجديدي، مثل هندسة الأنسجة وعلاج الخلايا الجذعية ، على تطوير قدرات تجديد الأنسجة. غالبًا ما تُستخدم الطعوم الخيفية والغريبة كسقالات أو مصفوفات في تطبيقات هندسة الأنسجة. إن توافقها مع الأساليب التجديدية يجعلها ذات قيمة في تحقيق تجديد الأنسجة المحسن، مما يدفع الطلب على مواد الطعوم هذه. تُستخدم علاجات الخلايا الجذعية، بما في ذلك علاجات الخلايا الجذعية المتوسطة (MSC)، لتعزيز إصلاح الأنسجة وتجديدها. يمكن أن تعمل الطعوم الخيفية والغريبة كحاملات للخلايا الجذعية، مما يساعد على توصيلها ودمجها في الأنسجة التالفة. يوفر هذا التآزر بين مواد الطعوم وعلاجات الخلايا الجذعية فرصًا لعلاجات تجديدية مبتكرة.

أدى التطور في المواد الحيوية وتقنيات معالجة الطعوم إلى تطوير مواد طعوم أكثر توافقًا حيويًا وصديقة للأنسجة. يضمن هذا التوافق الحيوي المحسّن تحمّل الجسم لمواد الطعوم بشكل جيد، مما يقلل من خطر حدوث مضاعفات ويعزز تجديد الأنسجة بنجاح.

ومن ثم، فمن المتوقع أن يوفر التقدم في مجال الأدوية التجديدية فرصة لنمو السوق.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

من 2023 إلى 2030

|

سنة الأساس

|

2022

|

السنوات التاريخية

|

2021 (قابلة للتخصيص حتى 2015 - 2020)

|

الوحدات الكمية

|

الإيرادات بالملايين من الدولارات الأمريكية

|

القطاعات المغطاة

|

نوع المنتج (الطعم الخيفي، طعم غريب، مكملات طعم العظام)، والأساليب ( الاندماج القطني الأمامي (ALIF)، والاندماج القطني عبر الثقبة الفقرية (TLIF)، والاندماج القطني الخلفي (PLIF)، ونوع الجراحة (جراحة العمود الفقري المفتوحة وجراحة العمود الفقري الأقل توغلاً)، والمؤشرات (الأمراض التنكسية، وصدمات العمود الفقري أو الكسور، وأورام العمود الفقري، وجراحات المراجعة، والتهابات العمود الفقري (التهاب العظم والنقي أو التهاب القرص)، وتشوهات العمود الفقري، والتشوهات الخلقية في العمود الفقري، وغيرها)، والفئة العمرية (البالغين، وكبار السن، والأطفال)، والمستخدم النهائي (المستشفى، والعيادة المتخصصة، ومراكز الجراحة الخارجية، وغيرها)

|

الدول المغطاة

|

ألمانيا، فرنسا، المملكة المتحدة، إيطاليا، إسبانيا، روسيا، سويسرا، هولندا، تركيا، بولندا، السويد، بلجيكا، الدنمارك، فنلندا، النرويج، وبقية أوروبا

|

الجهات الفاعلة في السوق المغطاة

|

Medtronic (أيرلندا)، Arthrex, Inc. (الولايات المتحدة)، Stryker (الولايات المتحدة)، ZimVie Inc. (الولايات المتحدة)، Medical Devices Business Services, Inc. (الولايات المتحدة)، RTI Surgical (الولايات المتحدة)، Integra LifeSciences (الولايات المتحدة)، Orthofix US LLC. (الولايات المتحدة)، ATEC Spine, Inc. (الولايات المتحدة)، Globus Medical (الولايات المتحدة)، Exactech, Inc. (الولايات المتحدة)، Regenity (الولايات المتحدة)، Cerapedics.Inc (الولايات المتحدة)، Bioventus (الولايات المتحدة) وغيرها.

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، فإن تقارير السوق التي تم تنظيمها بواسطة Data Bridge Market Research تتضمن أيضًا تحليلًا متعمقًا من الخبراء وعلم الأوبئة للمرضى وتحليل خطوط الأنابيب وتحليل التسعير والإطار التنظيمي.

|

تحليل القطاعات:

يتم تقسيم سوق الطعوم الشوكية والزراعة الغريبة في أوروبا إلى ستة قطاعات بارزة بناءً على نوع المنتج والأساليب ونوع الجراحة والمؤشر والفئة العمرية والمستخدم النهائي.

- على أساس نوع المنتج، يتم تقسيم السوق إلى مكملات الطعم الخيفي، والطعم الغريب، والطعم العظمي.

في عام 2023، من المتوقع أن تهيمن شريحة زراعة النخاع الشوكي على سوق زراعة النخاع الشوكي في أوروبا

ومن المتوقع أن تهيمن شريحة زراعة الأعضاء على السوق في عام 2023 بحصة سوقية تبلغ 63.67% بسبب ارتفاع معدل الإصابة باضطرابات العمود الفقري في أوروبا.

- على أساس النهج، يتم تقسيم السوق إلى اندماج الفقرات القطنية الأمامية (ALIF)، واندماج الفقرات القطنية عبر الثقبة الفقرية (TLIF)، واندماج الفقرات القطنية الخلفية (PLIF).

في عام 2023، من المتوقع أن تهيمن شريحة اندماج الفقرات القطنية الأمامية (ALIF) على سوق الطعوم الشوكية والزرع الغريب في أوروبا

من المتوقع أن تهيمن شريحة اندماج الفقرات القطنية الأمامية (ALIF) على السوق في عام 2023 بحصة سوقية تبلغ 45.46٪ بسبب التقدم في التقنيات الجراحية المستخدمة في ترقيع العمود الفقري.

- بناءً على نوع الجراحة، يُقسّم السوق إلى جراحة العمود الفقري المفتوحة وجراحة العمود الفقري طفيفة التوغل. في عام ٢٠٢٣، من المتوقع أن يهيمن قطاع جراحة العمود الفقري المفتوحة على السوق بحصة سوقية تبلغ ٥٧.٤٢٪.

- بناءً على المؤشرات، يُقسّم السوق إلى أمراض تنكسية، وإصابات أو كسور في العمود الفقري، وأورام في العمود الفقري، وجراحات تصحيحية، والتهابات في العمود الفقري (التهاب العظم والنقي أو التهاب القرص)، وتشوهات في العمود الفقري، وتشوهات خلقية في العمود الفقري، وغيرها. ومن المتوقع أن يهيمن قطاع الأمراض التنكسية على السوق بحصة سوقية تبلغ 38.14% في عام 2023.

- بناءً على الفئات العمرية، يُقسّم السوق إلى فئات كبار السن، والبالغين، والأطفال. ومن المتوقع أن يهيمن قطاع البالغين على السوق بحصة سوقية تبلغ 50.40% في عام 2023.

بناءً على المستخدم النهائي، يُقسّم السوق إلى مستشفيات، وعيادات متخصصة، ومراكز جراحية خارجية ، وغيرها. وفي عام ٢٠٢٣، من المتوقع أن يهيمن قطاع المستشفيات على السوق بحصة سوقية تبلغ ٤٨.٨٠٪.

اللاعبون الرئيسيون

تعترف شركة Data Bridge Market Research بالشركات التالية باعتبارها اللاعبين الرئيسيين في سوق زراعة العمود الفقري وزراعة الخلايا الغريبة في أوروبا وهي Medtronic (أيرلندا)، وArthrex، Inc. (الولايات المتحدة)، وStryker (الولايات المتحدة)، وZimVie Inc. (الولايات المتحدة)، وMedical Devices Business Services، Inc. (الولايات المتحدة) وغيرها.

تطوير السوق

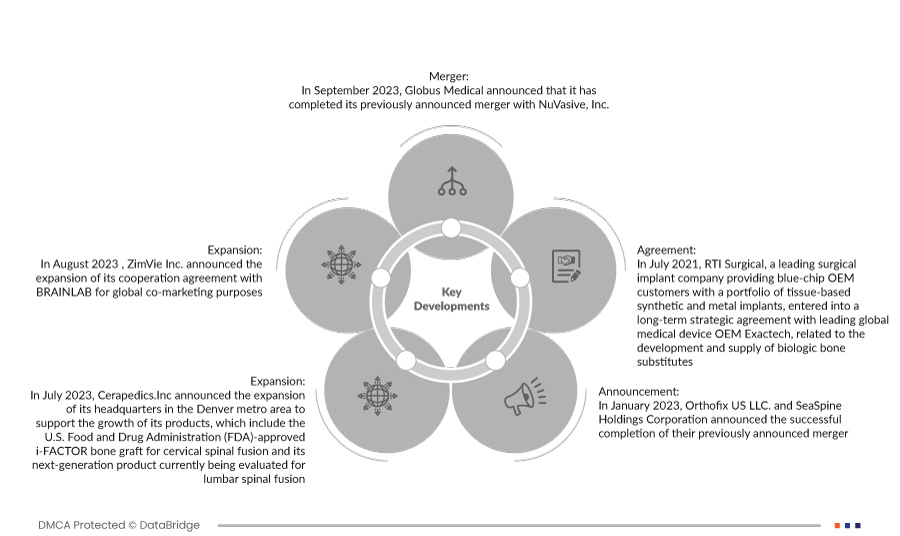

- في سبتمبر 2023، أعلنت شركة Globus Medical أنها أكملت اندماجها المعلن عنه سابقًا مع شركة NuVasive, Inc. ستوفر الشركة المدمجة للجراحين والمرضى أحد أكثر العروض شمولاً لحلول الإجراءات العضلية الهيكلية والتقنيات التمكينية للتأثير على استمرارية الرعاية.

- في أغسطس 2023، أعلنت شركة ZimVie Inc. عن توسيع اتفاقية تعاونها مع BRAINLAB لأغراض التسويق المشترك عالميًا. سيساعد هذا الشركة على تنمية إيراداتها السنوية. في يوليو 2022، أعلنت شركة AbbVie وشركة iSTAR Medical SA عن صفقة استراتيجية لمواصلة تطوير وتسويق جهاز MINIject من iSTAR Medical، وهو جهاز جراحي طفيف التوغل لعلاج الجلوكوما (MIGS) لمرضى الجلوكوما. تعزز هذه الصفقة قدرات الشركة على تطوير وتصنيع منتجات جراحة الجلوكوما لعملائها لاستخدامها في الإجراءات الجراحية طفيفة التوغل.

- في يوليو 2023، أعلنت شركة Cerapedics.Inc. عن توسعة مقرها الرئيسي في منطقة دنفر الحضرية لدعم نمو منتجاتها، والتي تشمل طُعم i-FACTOR العظمي المُعتمد من إدارة الغذاء والدواء الأمريكية (FDA) لدمج الفقرات العنقية، ومنتجها من الجيل التالي الذي يخضع حاليًا للتقييم لدمج الفقرات القطنية. سيؤدي هذا إلى زيادة الإيرادات السنوية للشركة.

- في يناير 2023، أعلنت شركة أورثوفكس يو إس إل إل سي وشركة سي سباين هولدينغز كوربوريشن عن إتمام اندماجهما المُعلن عنه سابقًا بنجاح. سيُساعد هذا الدمج الشركة على بناء صورة علامتها التجارية، إلى جانب العديد من المزايا الأخرى.

- في يوليو 2021، دخلت شركة RTI Surgical، وهي شركة رائدة في مجال زراعة الأعضاء الجراحية تقدم لعملاء OEM من الشركات الكبرى مجموعة من الغرسات الاصطناعية والمعدنية القائمة على الأنسجة، في اتفاقية استراتيجية طويلة الأجل مع شركة Exactech الرائدة عالميًا في مجال الأجهزة الطبية، فيما يتعلق بتطوير وتوريد بدائل العظام البيولوجية.

التحليل الإقليمي

من الناحية الجغرافية، البلدان التي يغطيها تقرير سوق الطعوم الشوكية والزراعة الأجنبية في أوروبا هي ألمانيا وفرنسا والمملكة المتحدة وإيطاليا وإسبانيا وروسيا وسويسرا وهولندا وتركيا وبولندا والسويد وبلجيكا والدنمارك وفنلندا والنرويج وبقية أوروبا.

وفقًا لتحليل Data Bridge Market Research:

ألمانيا هي الدولة المهيمنة والأسرع في سوق زراعة العمود الفقري والزراعة الأجنبية في أوروبا خلال الفترة المتوقعة 2023 - 2030.

من المتوقع أن تهيمن ألمانيا على أسرع الدول نمواً بسبب التقدم التكنولوجي العالي وتزايد حضور اللاعبين في السوق في البلاد.

للحصول على معلومات أكثر تفصيلاً حول تقرير سوق زراعة العمود الفقري في أوروبا، انقر هنا - https://www.databridgemarketresearch.com/reports/europe-spinal-allografts-and-xenograft-market